Medical Equipment Sector Plunges into Price War Amid Nationwide Centralized Procurement

Having just emerged from a period of sluggish sales, the industry now faces a pricing dilemma.

Around 2025, provinces including Sichuan, Henan, Hebei, and Xinjiang successively launched centralized procurement of medical equipment, with a major transformation hidden behind the “price-for-volume” strategy.

This round of volume-based procurement price reductions applies regardless of brand, category, or product tier, with particularly drastic cuts in the mid-to-low-end segments. Taking equipment upgrades within county-level medical consortia as an example, 1.5T MRI scanners priced at RMB 2 million per unit, 64-slice CT scanners at RMB 1 million per unit, and whole-body ultrasound systems at under RMB 500,000 per unit have driven medical device prices down to levels previously unimaginable.

Furthermore, purchasers commonly require manufacturers to provide five-year equipment maintenance and warranty services, further squeezing already thin profit margins or even driving them into negative territory.

From the payer’s perspective, pharmaceuticals, reagents, and consumables have been subject to centralized procurement for many years; as a major component of expenditures, medical equipment should not be exempt from this process.

Domestic medical device manufacturers also have their own struggles: it has only been a few years since they broke free from the dominance of multinational corporations, and before they could fully enjoy the benefits, they were already caught up in price wars.

After One Harsh Winter Comes Another: What Lies Ahead for Medical Devices?

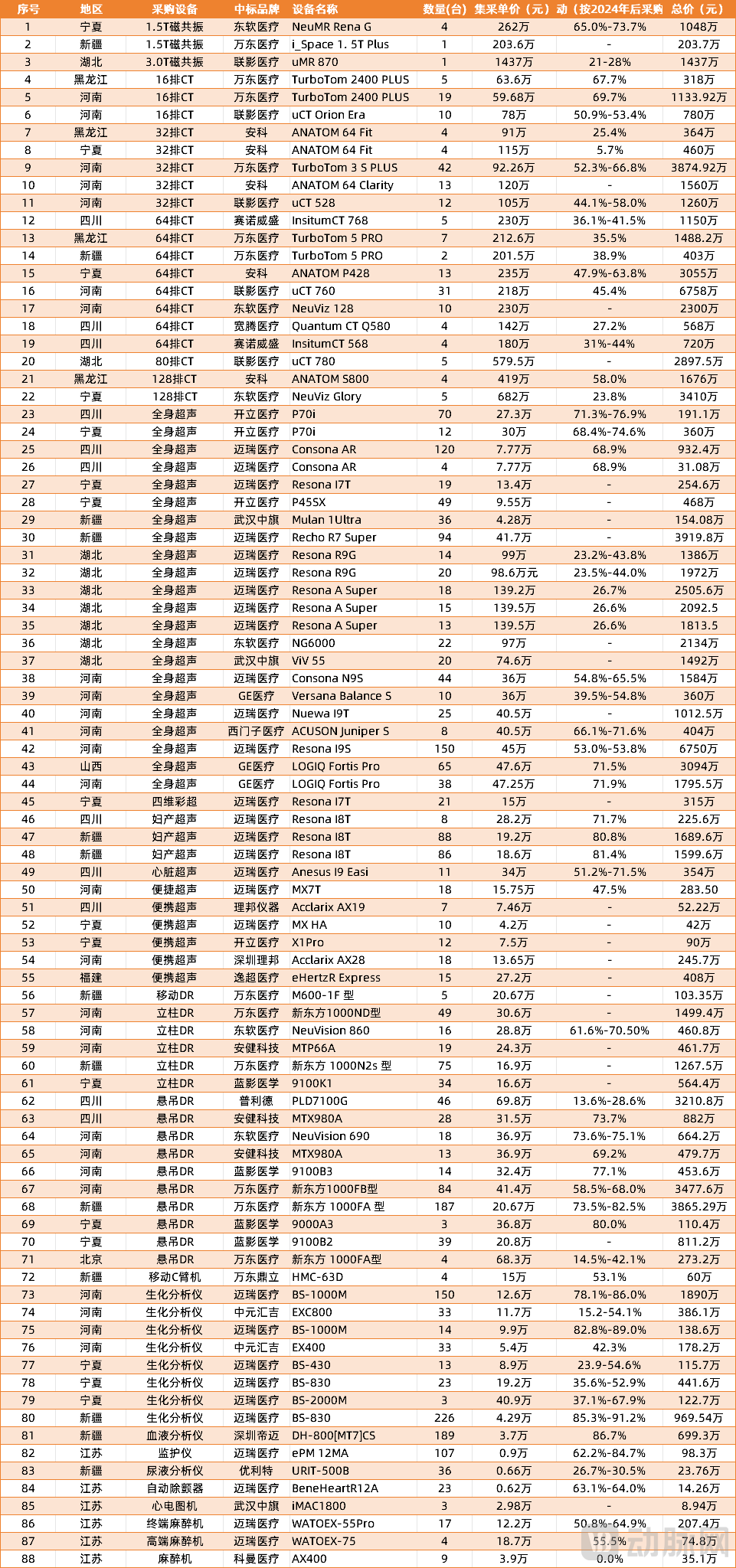

Estimation of Price Decline for Medical Equipment in Centralized Procurement under the County-level Medical Community Equipment Renewal Program

Data source: Public bidding data from eight provinces and municipalities, including Ningxia, Xinjiang, Henan, Beijing, Sichuan, Jiangsu, Hubei, and Heilongjiang.

(Price changes are referenced against publicly disclosed tendering and bidding prices after 2024, excluding the impact of configuration reductions; certain equipment models with undisclosed procurement information are not included in the table, which may result in some discrepancies.)

In July last year, the National Development and Reform Commission and the Ministry of Finance issued the "Preliminary Notice on Doing a Good Job in Equipment Renewal in the Medical and Health Field in 2024," the "Implementation Plan for Promoting Equipment Renewal in the Medical and Health Field," and "Several Measures to Strengthen Support for Large-Scale Equipment Renewal and Consumer Goods Trade-In," aiming to address the issues of unmet equipment needs in some hospitals and the prolonged service life of existing equipment.

At that time, some experts had predicted that the “trade-in” program might be implemented through centralized procurement, but few anticipated that the price reductions for medical equipment would be driven down step by step to their current level.

VCBeat’s analysis of publicly available tender and bidding data from eight provinces and municipalities—Ningxia, Xinjiang, Henan, Beijing, Sichuan, Jiangsu, Hubei, and Heilongjiang—revealed that:

Industry leaders secured the vast majority of contracts in centralized procurement.

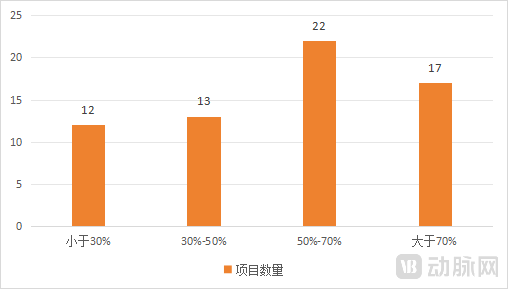

Among projects with accessible public bidding data for non-volume-based procurement after 2024, only 39% of equipment prices decreased by less than 50%, approximately 34% saw price reductions in the 50%-70% range, and another 27% experienced declines exceeding 70%.

Distribution of Price Declines for Medical Equipment Updated Through Centralized Procurement in County-Level Medical Consortia

Among these, ultrasound equipment accounted for the highest procurement volume in the centralized bulk purchasing initiatives for county-level medical consortia, and it also registered one of the largest average price reductions. In this niche segment, Mindray emerged as the biggest winner, securing 13 orders each valued at over RMB 10 million. Notably, under Henan Province’s equipment renewal program for county-level medical consortia, Mindray sold 150 units of its Resona I9S model at a unit price of RMB 450,000, generating a single-batch revenue of RMB 67.5 million.

However, sales volume does not correlate with profitability. The price reduction for the Resona I9S compared to 2024 levels was approximately 53.0%–53.8%, leaving it still “profitable”; in contrast, devices such as the Resona I8T and Anesus I9 Easi saw price cuts exceeding 60%, making it largely difficult to generate profits.

The price reduction for DR systems is similar to that of ultrasound equipment. Despite orders reaching the 30-million level, manufacturers such as Wandong, Neusoft, and Blue Eagle often cut prices by more than 60% for both floor-mounted and ceiling-suspended DR systems, while also providing five-year maintenance warranties, thereby driving prices to rock bottom.

The pricing situation for CT and MRI is more favorable than that for DR and ultrasound, with most price reductions concentrated within 50%, likely because the historical gross margins for CT and MRI were already relatively low. From the results, a 1.5T MRI scanner priced at RMB 2 million and a 64-slice CT scanner priced at RMB 1 million are approaching the actual cost of the equipment, nearly exhausting all room for further price reductions.

In contrast, the volume-based procurement of high-end and ultra-high-end medical devices remains within a controllable range. These devices inherently carry high premiums and have low sales volumes. The relatively modest price reductions under volume-based procurement have actually boosted sales, ensuring substantial profits despite the price cuts.

Taking the recently concluded centralized procurement of imaging equipment in Zhejiang Province as an example, the project had a total budget of RMB 233 million, with a maximum price ceiling set at RMB 162 million, and planned to procure 12 ultra-high-end CT scanners.

“Announcement of the Winning Bid (Transaction) Results for the Zhejiang Provincial Health Commission’s Ultra-High-End CT Procurement Project (I) by the Zhejiang Provincial Government Procurement Center” shows that United Imaging and GE Healthcare split this order. The GE 256-slice Quantum CT Revolution Apex Expert was priced at RMB 15.937 million per unit, with four units sold in a single transaction, representing a price decrease of 21.3%–37.1% compared to the publicly tendered prices in 2024. The price reduction for United Imaging’s 320-slice uCT960 was slightly greater, at RMB 9.89 million per unit, with three units sold in a single transaction, reflecting a price decrease of 37.4%–41.1%.

Procurement Status of the Zhejiang Provincial Health Commission's Ultra-High-End CT Procurement Project

(Price changes are referenced from public tender prices after 2024; there may be discrepancies compared to actual market performance.)

As evidenced by the volume-based procurement (VBP) outcomes in the first half of the year, it is becoming the new normal for medical device manufacturers to incur losses on low-end products, break even on mid-range products, and generate profits from high-end products. With the further advancement of VBP, the medical device industry is poised to undergo a comprehensive restructuring.

As the role of distributors weakens following centralized procurement, whole-system manufacturers with strong channel advantages, such as GPS and United Imaging, will experience some loss in market share, while companies like Sinovision and Anke will see increased opportunities.

However, once they break into the first tier, these companies can rapidly generate substantial cash flow through volume-based procurement (VBP), thereby supporting the iteration of their existing products and the R&D of high-end offerings, which may in fact accelerate their development. Consequently, the gap between leading original equipment manufacturers (OEMs) and non-leading OEMs is likely to widen further in the post-VBP era.

Non-leading enterprises, squeezed by industry leaders, will have to seek opportunities only in the non-centralized procurement market (accounting for approximately 20% of the total market), assuming that centralized procurement rules remain unchanged. In response to this situation, they must either implement differentiated improvements to their equipment to address previously unmet clinical needs, or seek acquisition by leading companies and exit direct market competition.

For distributors, the post-centralized procurement era necessitates a restructuring of their core functions. With channel profits significantly compressed, they must seek new sources of value by identifying innovative products or enhancing auxiliary services such as maintenance and equipment management.

Imaging AI companies, though not directly involved in centralized procurement, have also been affected. In Henan Province’s county-level medical consortium equipment upgrade project, AI software was bundled with imaging devices. The 16-slice CT scanners included in the province’s centralized procurement were priced lower than single-disease AI solutions from around 2020, and came with several AI modules, thereby squeezing the pricing power of standalone imaging AI products.

However, it is too early to determine whether volume-based procurement (VBP) is beneficial or detrimental to AI in medical imaging in the short term. Although price reductions for medical equipment will inevitably exert downward pressure on pricing mechanisms for associated software, AI-powered imaging solutions have effectively become standard features post-VBP. If equipment manufacturers lack sufficient AI capabilities, they may resort to bulk procurement of AI solutions from specialized medical imaging AI companies, thereby creating new opportunities for such firms.

Overall, policymakers hope that the prices of low- to mid-end medical devices will return to their intrinsic value, as the historically high gross profit margins of 50%–150% have indeed placed significant pressure on payers.

At the same time, they also expect leading domestic equipment manufacturers to strive to catch up with the world’s top equipment companies, compete vigorously in non-centralized procurement environments, and even guide the development of the industry.

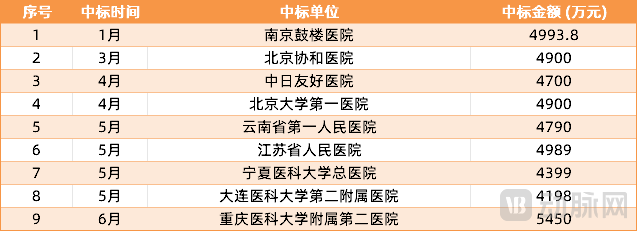

As for the specific types of equipment to be developed, Siemens Healthineers’ photon-counting CT can be regarded as a typical case. In the first half of 2025, Siemens Healthineers sold nine photon-counting CT systems, matching the full-year figure for 2024, while the average price decreased by approximately RMB 3 million.

After all, it represents the most cutting-edge demands of hospitals and demonstrates the value of innovation for corporate commercialization, potentially serving as a guiding beacon for the next phase of development for leading manufacturers such as United Imaging, Neusoft, and Wandong.

2025 Siemens Photon-Counting CT Bid Award Status

Regarding centralized procurement of medical devices, the policy itself also requires continuous refinement in practice.

From a statistical perspective, most provinces and municipalities have driven the prices of devices within the same category to very similar levels during equipment upgrades and replacements. This may indicate that the National Health Commission has placed greater emphasis on price when evaluating medical equipment, thereby overlooking, to some extent, the inherent differences among the devices themselves.

In practice, many products priced slightly above the average possess unique advantages that effectively meet specific clinical needs of hospitals; however, they lose their competitiveness because their prices fall below the purchaser’s expected price range.

For county-level medical institutions developing specialized departments, high-cost products that meet regional diagnostic and treatment needs will deliver value far exceeding that of ordinary products.

Therefore, the future direction of volume-based procurement will shift from “prioritizing low prices” to “balancing low prices with demand,” striving to create a fair competitive environment.

Currently, some provinces and municipalities have conducted systematic surveys prior to centralized procurement to evaluate the application foundation and actual usage of equipment from various brands, taking into account the alignment between the equipment and the actual clinical needs of local county-level institutions. Additionally, certain provinces and municipalities have introduced relevant policies to prevent companies from engaging in malicious low-price bidding.

Although the dominance of leading enterprises in the market has become inevitable, we also hope that the centralized procurement system can be further improved to create some opportunities for startups, ensuring a steady influx of fresh blood into the equipment market and sustaining long-term market vitality through competition.