U.S. Proposes Six Strategic Measures in Response to the Rise of China's Biopharmaceutical Industry

On June 18 local time, the U.S. Food and Drug Administration (FDA) announced an immediate review of new clinical trials. Any trial found to involve sending live cells from U.S. citizens to certain countries, including China, for genetic engineering before infusing them back into U.S. patients will be terminated.

FDA Announcement (Screenshot from the FDA Official Website)

This marks another recent U.S. move to restrict China’s development in the biotechnology sector, with rhetoric more intense than ever before. In light of a series of recent actions, it is evident that the United States now views China as a significant threat in the biomedical field and may introduce further measures targeting the development of China’s biotechnology industry.

Foreign institutions have also offered various recommendations and perspectives on future U.S. measures. Although these do not represent official positions, they hold significant reference value for decision-making by professionals in China’s biotechnology industry. Accordingly, VCBeat has compiled these viewpoints.

The notion of a “China threat” in the biotechnology sector is not new, but it has only been taken seriously and elevated to the official level in the past two years. In late 2023, the United States introduced the draft Biosecurity Act, which restricts commercial cooperation between U.S. federal agencies and foreign biotechnology companies under the guise of “national security,” specifically naming five companies affiliated with the WuXi AppTec group and the BGI group.

The draft was passed by the U.S. Senate with an overwhelming majority in September 2024 (306 votes in favor and 81 against). Although it has not yet been enacted into law due to legislative procedural reasons, there is a significant possibility that it will be reintroduced into the legislative process this year.

In April this year, the U.S. National Security Commission on Emerging Biotechnology (NSCEB) released another weighty report, comprehensively examining the global competitive landscape facing U.S. biotechnology from a national security perspective for the first time, and identifying China’s biomedical industry as the most strategically challenging competitor.

An obvious fact is that, after years of sustained development, China's biomedical industry has indeed made significant progress.

From 2016 to 2021, the market capitalization of China’s biotechnology companies grew 100-fold, reaching approximately $300 billion, making it the world’s second-largest biotechnology market after the United States.

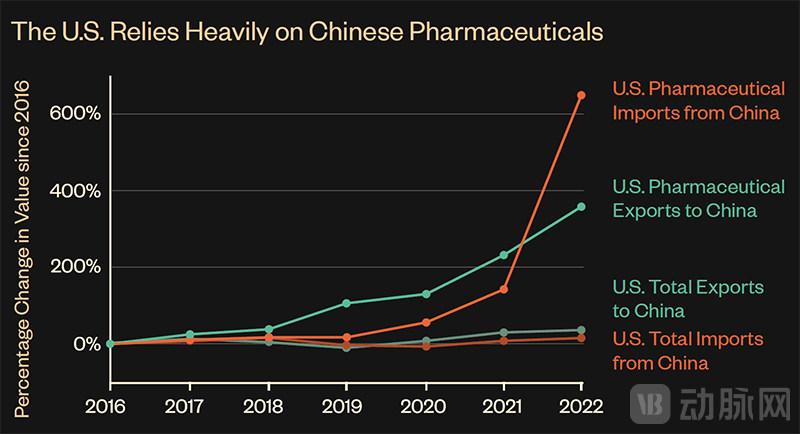

Pharmaceutical Trade Between China and the United States (Image sourced from the NSCEB report “Changing the Future of Biotechnology”)

In terms of manufacturing scale, China's share of global pharmaceutical production rose from approximately 5% in 2002 to nearly 25% in 2019, making it a major global producer of active pharmaceutical ingredients for various drugs.

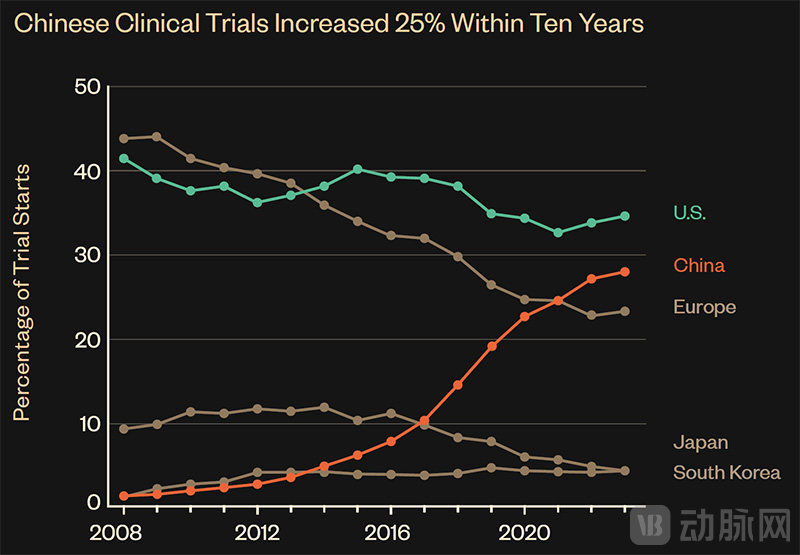

Proportion of Clinical Trials by Country in Recent Years (Image Source: NSCEB Report “Shaping the Future of Biotechnology”)

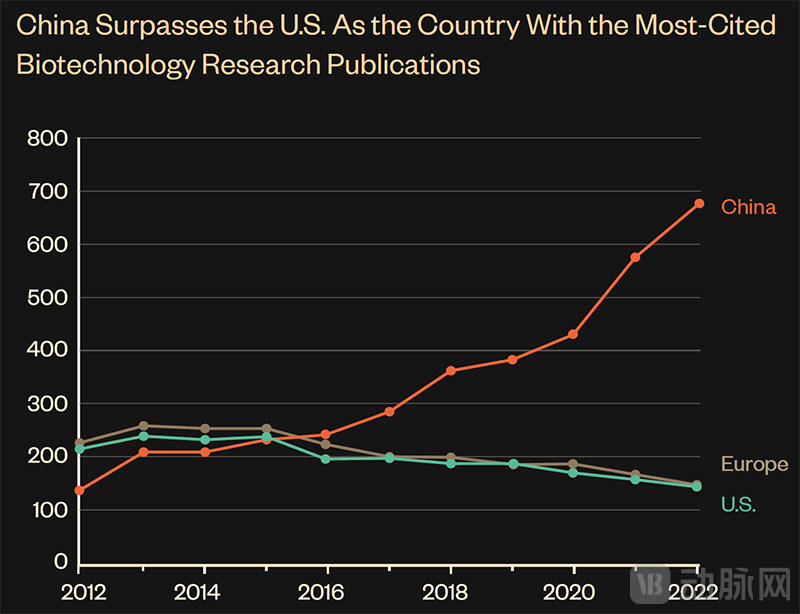

Share of Highly Cited Papers by Country/Region in Recent Years (Image from the NSCEB Report “Shaping the Future of Biotechnology”)

In terms of academic research, the United States accounted for 45% of the most-cited synthetic biology papers globally in 2010, while China accounted for only 13%. By 2023, China’s share had risen to 60%, whereas that of the United States had dropped to just 7%.

More notably, according to GlobalData statistics, the total value of licensing deals between multinational corporations (MNCs) and Chinese biotech firms reached $41.5 billion in 2024, a 66% increase from 2023, setting a new record high. Data from DealForma further shows that as of June, Chinese companies accounted for as much as 42% of licensing agreements with upfront payments exceeding $50 million in 2025.

The magnitude of progress is too significant to be ignored.

There is a broad consensus among foreign researchers on why China’s biopharmaceutical industry has made such significant progress in recent years.

First, policy support is indispensable. Since biopharmaceuticals and high-performance medical devices were designated as key areas for breakthrough development in the “Made in China 2025” initiative, China has increased innovation investment in this sector and gradually built an innovative ecosystem for biopharmaceuticals through comprehensive measures.

Taking regulatory oversight as an example, since joining the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH) in 2017, China has introduced more than 100 ICH guidelines and implemented transformative reforms in its review processes—such as priority review and conditional approval—gradually aligning its drug regulatory system with international standards. This has also laid the foundation for the subsequent rapid acceleration of the biopharmaceutical industry.

Secondly, there are differences in cost and efficiency; in both aspects, China’s biopharmaceutical industry ranks among the top globally. The advantage is particularly pronounced in the early stages of clinical trials—startups in China can progress from initiation to entering clinical trial phases within 18 months or less, far shorter than the several years typically required in the United States. Meanwhile, patient recruitment for clinical trials in China is faster, and labor and supply chain costs are significantly lower, with the average cost of a Phase I clinical trial being only one-third of that in the U.S.

Since 2018, China has officially transitioned its clinical trial review mechanism from the previous “approval system” to an “implied permission” model, akin to that of the U.S. FDA. Under this framework, a clinical trial application is deemed approved if no objections are raised by regulatory authorities within the stipulated 60-day period. Prior to this reform, the review process often took six months to over a year.

Following this reform, the proportion of clinical trials conducted by Chinese biopharmaceutical companies globally began to rise rapidly. In 2013, China’s share stood at merely 3%. By 2023, this figure had climbed to approximately 29%, while North America and Europe accounted for only 17% and 16%, respectively.

This is regarded as one of the most core competitive advantages of China’s biomedical industry.

Not long ago, the National Medical Products Administration (NMPA) drafted the “Announcement on Optimizing the Review and Approval of Clinical Trials for Innovative Drugs (Draft for Comments),” which plans to shorten the review period for clinical trial applications of qualifying innovative drugs to 30 days. This move will further accelerate the review process in the biopharmaceutical sector and reinforce this competitive advantage.

Furthermore, China’s biomedical industry boasts a complete supply chain and has similarly benefited from the country’s status as a global manufacturing hub, resulting in significant cost advantages. It is estimated that the average unit cost for CRO/CDMO services in China is only about 60–70% of that in Europe and the United States.

This is of significant importance to multinational corporations (MNCs) facing continuously rising R&D costs for new drugs, leading them to increasingly source from Chinese suppliers and thereby fostering the development of China’s related industrial chain. International observers believe that, barring unforeseen circumstances, China’s CDMO capacity could account for half of the global total biologic manufacturing capacity by 2035.

This is also considered one of the core advantages driving the rapid development of China's biopharmaceutical industry.

Finally, China has also performed well in talent development, recruitment, and capital markets. Statistics show that Chinese nationals accounted for as much as 36% of all foreign students who earned doctoral degrees in science and engineering from U.S. institutions in 2023. It is projected that by 2025, Chinese universities will produce 77,000 STEM PhD graduates annually, nearly twice the total number in the United States, with life sciences accounting for approximately one-fifth of this figure.

It is the continuous accumulation of these factors that has led to the strong development momentum of China's biopharmaceutical industry today.

Since the United States has explicitly identified China as its largest competitor in the field of biotechnology, what measures might it take in response? Drawing on various international perspectives, the U.S. is expected to adopt a two-pronged strategy: enhancing its own biomedical capabilities while simultaneously curbing the development of China’s biomedical sector.

At the specific implementation level, the NSCEB report provides quite concrete and actionable measures.

First, prioritize biotechnology at the national level. The report argues that U.S. government policies are fragmented and lack a coordination mechanism. It recommends establishing a National Biotechnology Coordination Office within the Executive Office of the President, with a director appointed by the President. This office would be responsible for coordinating interagency actions on biotechnology competition and regulation, as well as formulating a series of national-level support policies.

Second, encourage the private sector to scale up U.S. biologics production. To achieve this goal, the measure plans to streamline regulations for U.S. biotechnology companies; encourage private investment in technology startups that are critical to national and economic security; establish a nationwide network of bio-manufacturing facilities to assist pre-commercialization startups; and include biotechnology infrastructure and data within the scope of “critical infrastructure” for prioritized protection.

In addition to strengthening its own capabilities, the report also outlines a series of measures aimed at curbing the development of China’s industries. These include requiring listed companies to disclose vulnerabilities in their foreign-based supply chains, such as single-source or primary-source dependencies; prohibiting companies that collaborate with the federal government from using Chinese suppliers deemed to pose security threats; enhancing scrutiny of Chinese investments through institutional and procedural reforms; and employing “anti-dumping” measures against Chinese biological products.

Interestingly, while the report argues that the Chinese government heavily subsidizes “companies unable to compete in normal market conditions” and attracts foreign innovators seeking commercialization, emphasizing the need to counter China’s “brute-force economic policies,” it simultaneously relies on similar supportive measures to enhance its own capabilities, revealing a conspicuous double standard.

Third, the report further proposes introducing biotechnological innovations into the defense sector, such as establishing corresponding production facilities through collaborations between the military and startups; expanding military procurement to support relevant enterprises via defense contracts. The report even specifically mentions that, to prevent adversaries from “misusing” biotechnology, the United States needs to possess the capability to “detect and characterize as broad a range of biological threats as possible at an early stage,” and requires the military to incorporate the military applications of emerging biotechnologies into its exercises.

Meanwhile, the report also calls for strengthening oversight of U.S. capital to prevent it from investing in biotechnologies developed in China that may pose national security risks, and for implementing export controls on specific biological products to prevent their use for military purposes, among other measures.

Fourth, strengthen research and development innovation in the field of biotechnology. To this end, the report recommends elevating biological data to the status of a strategic resource and establishing a series of measures around this objective, such as building a national biological data network and a “cloud laboratory” network equipped with various tools, as well as preventing China from accessing sensitive U.S. biological data.

Furthermore, the report also mentions maintaining the United States' advantage in the research and development innovation of frontier biotechnology by establishing special funds and infrastructure.

Fifth, strengthen talent development to enable the United States to lead global biotechnology innovation. These measures include enhancing government capacity through hiring and retraining, strengthening the existing education system, and easing restrictions on the recruitment of foreign biotechnology professionals.

Sixth, the report argues that the United States needs to strengthen cooperation with its allies in relevant fields. For instance, it should seek to streamline and expand market access among allies to replace supply chains from China, aggregate demand among allies to boost the need for biotechnology products, ensure that biotechnology is not misused through multilateral controls, jointly develop norms and standards, and standardize methods for protecting biotechnology.

It is worth noting that researchers abroad have also stated that past experience has demonstrated the biopharmaceutical industry to be highly dependent on international cooperation. This is particularly evident in basic biotechnology research. For instance, Chinese institutions and researchers have played an extremely important role in biotechnological innovation in the United States through U.S.-based R&D centers, incubators, and collaborative partnerships. Meanwhile, innovative drugs from China have benefited American patients with lower prices and superior clinical outcomes, helping to save substantial healthcare expenditures.

Furthermore, the U.S. biopharmaceutical industry relies heavily on China’s biopharmaceutical capabilities. China produces 40–50% of the global supply of active pharmaceutical ingredients (APIs), and for many APIs, China is the primary or even sole supplier to the United States. Within the supply chain, the U.S. also depends significantly on Chinese contract development and manufacturing organizations (CDMOs) for research reagents and clinical-grade biologics.

This makes it unrealistic for the United States to exclude China’s biotechnology sector in the short term, as the cost would be prohibitively high. According to an October 2024 survey conducted abroad, 79% of U.S. biopharmaceutical companies have at least one project whose cell banks or plasmids originate from China, and achieving “U.S. substitution” would require at least 2–8 years. Meanwhile, a 2022 study estimated that completely replacing Chinese production capacity in the biopharmaceutical sector would incur a one-time cost of $18 billion, followed by additional annual labor costs of at least $12 billion.

Meanwhile, China has also benefited from advanced foreign equipment and technology. Taking specialty and fine chemicals as an example, China’s import value reached $358 billion from January to August 2024, resulting in an overall trade deficit of $172 billion in this critical sector. Furthermore, China relies heavily on imports for laboratory equipment.

It is precisely for this reason that international cooperation and healthy competition, rather than containment and suppression, should serve as the effective remedy to drive the development of global biotechnology.

It is not difficult to see that the United States has indeed identified China as a major competitor in the biopharmaceutical sector, conducted in-depth research on China’s biopharmaceutical industry, and formulated rather detailed countermeasures.

Although most of these measures currently remain on paper and have not been systematically implemented, practitioners in China’s biopharmaceutical industry must still plan ahead and take proactive steps.