Unisound, the First AGI Stock on HKEX, Goes Public Today!

After Four Attempts at the Secondary Market, China’s AGI Leader Unisound Finally Rings the Bell at the HKEX Today.

As one of the first technology companies in China with AI as its core competency, Unisound AI Technology Co., Ltd. completed a total of 10 rounds of financing within 13 years since its establishment, raising over RMB 2 billion. Its investors include prominent institutions such as China Internet Investment Fund, Qiming Venture Partners, CICC Huirong, and JD Shangke. Upon its listing on the Hong Kong Stock Exchange, Unisound set its IPO price at HKD 205 per share, with net proceeds amounting to HKD 206 million.

Unisound’s forward-looking understanding of technological transformation has been instrumental in securing long-term favor from investors in the primary market. Entering the market in 2012, precisely at the inflection point when AI transitioned from academic research to commercial application, Unisound strategically differentiated itself by betting on AI-powered speech technology and rapidly expanding its footprint across multiple sectors, including IoT and healthcare.

In terms of R&D, Unisound achieved breakthroughs in Transformer algorithms as early as 2017, and subsequently developed its own BERT-based large language model, UniCore, thereby establishing its core platform, the “Unisound Brain.”

In 2023, as the wave of large language models began to rise, Unisound’s new “Shanhai” large model was already supported by 60 billion parameters, enabling it to handle various general-purpose tasks akin to OpenAI.

However, Unisound has also failed to overcome the common ailment of “high investment and heavy losses” plaguing AI application-level enterprises worldwide.

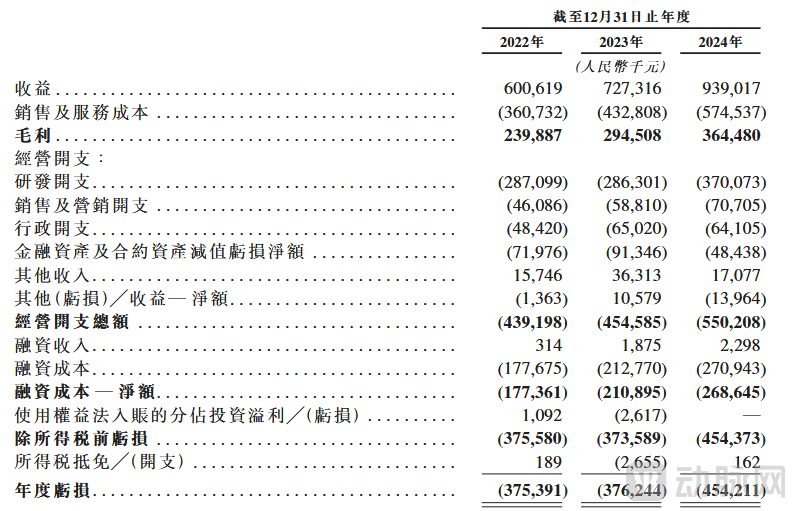

From 2022 to 2024, Unisound AI Technology Co., Ltd. recorded operating revenues of RMB 601 million, RMB 727 million, and RMB 939 million, respectively; with corresponding net losses of RMB 375 million, RMB 376 million, and RMB 454 million, accumulating nearly RMB 1.2 billion in losses over the three-year period.

Now that a new round of funding is in place, does it face mere survival or true rebirth?

Unisound Comprehensive Statement of Profit or Loss (Source: Unisound Prospectus)

Unisound is not a medical AI company in the strict sense.

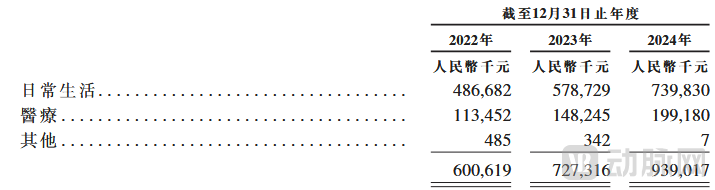

Although the two major business segments of “Smart Living” and “Smart Healthcare” contribute over 99% of Unisound’s revenue, Smart Living is the core driver of the company’s revenue growth. In 2024, this segment achieved a growth rate of 27.8%, accounting for nearly 80% of total revenue.

Distribution of Unisound’s Main Business Revenue (Source: Unisound Prospectus)

Prospectus data shows that Unisound’s Smart Life segment primarily comprises personalized solutions and AI capability APIs, with the former serving as its main revenue source.

Personalized solutions span a wide range of scenarios, covering multiple sectors such as smart homes, intelligent transportation, and in-vehicle voice systems. While market competition is intense, the growth potential remains substantial.

In the smart home sector, Unisound collaborates with industry leaders such as Midea and Gree to provide voice interaction technologies. Its AI solutions cover more than 700 categories of home appliances, capturing a 70% market share in voice interaction for white goods.

In the realm of smart transportation, Unisound provides voice-activated ticketing system services for Shenzhen Metro Line 20, reducing ticket purchase time from 15 seconds to 1.5 seconds and serving over 30,000 passengers on average per day.

To support the aforementioned business operations, Unisound AI Technology Co., Ltd. has successively launched the “Swift” and “Hummingbird” voice AI chips, as well as the automotive-grade “Snow Leopard” voice AI chip. Sales volume reached 12.8 million, 24.5 million, and 36 million units in 2022, 2023, and 2024, respectively, with year-over-year growth rates of 91.4% and 46.9%.

Beyond its current impressive figures, Unisound’s strategic bets on smart home and in-vehicle voice solutions are also industry hotspots in the era of large language models, with promising prospects. If the company can maintain high growth while controlling costs, it still has the potential to turn losses into profits.

As its second growth curve, Unisound’s healthcare segment has also seen its revenue soar in recent years.

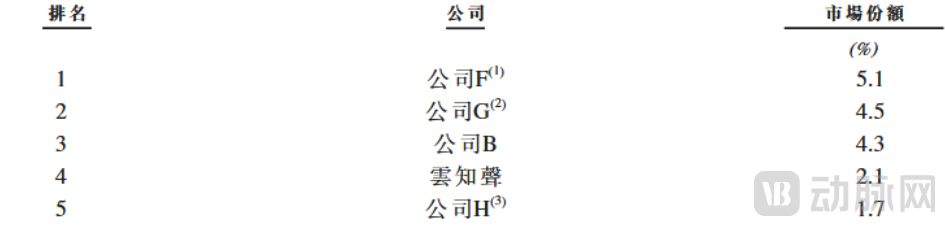

Prospectus data shows that from 2022 to 2024, Unisound AI Technology Co., Ltd. recorded revenues of RMB 113 million, RMB 148 million, and RMB 199 million, respectively. The compound annual growth rate (CAGR) of revenue from its major customers was 36.6%, and it currently ranks fourth in China’s AI market for medical services and treatment with a 2.1% market share.

The market shares of the three companies ahead of Unisound are 5.1%, 4.5%, and 4.3%, respectively. Based solely on data metrics, Unisound has the potential to catch up; however, when considering its specific application scenarios, we find that related businesses have already approached their short-term market ceiling, making further breakthroughs difficult to achieve.

Top Five AI Solution Providers for Medical Services and Treatment in China by Revenue in 2024 (Source: Unisound Prospectus)

Currently, Unisound’s revenue generation in the healthcare sector primarily relies on four AI-driven business lines: voice-based medical record entry, medical record quality control, single-disease quality control, and health insurance payment management. The first three categories have gradually reached saturation amid competition over the past five years. While there is some room for breakthrough in insurance payment management, it remains challenging to reduce costs.

Taking large-scale Clinical Decision Support Systems (CDSS) with mature market demand as an example, general practice CDSS faces direct competition from companies such as iFlytek Healthcare, Baidu Lingyi, and Jiahe Meikang. Furthermore, expansion into specialized fields requires contending with established medical informatics enterprises like Huimei Technology and Senyi Intelligence, which have been deeply entrenched in the sector for many years, making it challenging to break through the market.

Furthermore, hospital information technology (IT) construction has entered the era of general contracting. Hospital-wide projects—such as electronic medical record (EMR) grading, interoperability certification, and data center development—often involve investments reaching tens of millions of yuan. These initiatives are typically led by enterprises capable of providing systemic solutions, representing a significant avenue for medical IT companies to expand their revenue.

However, Unisound’s modular applications—such as voice input for medical records, medical record quality control, and single-disease quality control—have limited bargaining power. Developing a comprehensive solution would require an excessive leap, with neither the time nor the cost allowing for a transition to systematic project R&D.

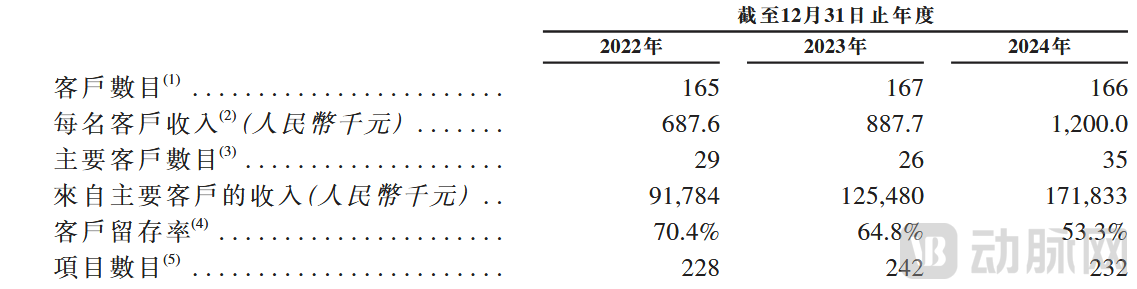

Under these circumstances, Unisound’s current strategy is to consolidate its existing healthcare business while striving for breakthroughs in its business model. In recent years, it has focused on key clients such as West China Hospital, driving up the average transaction value per project, which has led to simultaneous growth in both revenue per customer and total operating revenue.

As a consequence, Unisound’s medical customer retention rate has been on a downward trend, dropping to just 53.3% in 2024, while the number of medical customers declined from 242 in 2023 to 232.

It is foreseeable that Unisound’s healthcare business is unlikely to undergo significant adjustments in the coming years. Scenarios such as smart home and in-vehicle voice assistants are evolving rapidly, with end consumers serving as the ultimate payers. In contrast, the healthcare industry changes at a slower pace, making it difficult to cultivate a new breakout growth point in the short term.

Business Operations of Unisound’s Smart Healthcare Segment (Source: Unisound Prospectus)

Business Operations of Unisound’s Smart Healthcare Segment (Source: Unisound Prospectus)

By examining the operational performance of Unisound’s healthcare business, we may gain insight into the current state of China’s medical AI industry.

First is the dilemma of product homogenization.

The demands in the medical field differ from those in the consumer market. On one hand, genuine needs are relatively scarce; on the other, while enterprises may develop a corresponding demo within just a few months after identifying a real need, it can take several years to achieve large-scale market implementation and gain acceptance among physicians of varying expertise levels across different regions for the changes brought by technology.

Therefore, in the healthcare sector, particularly in healthtech, the slow pace of product scaling has afforded competitors ample opportunities to follow suit with incremental innovations. By the time market demand matures, the landscape is already saturated with a large number of homogeneous products.

Unisound serves as a prime example. As early as 2014, it began developing voice-enabled electronic medical record (EMR) systems leveraging AI technologies such as intelligent speech recognition, natural language understanding, and clinical knowledge graphs. However, its commercial operations did not gain significant traction until after 2020. With the market now saturated with AI-based quality control solutions and AI-enhanced Clinical Decision Support Systems (CDSS), Unisound finds it challenging to establish a competitive advantage solely through technological barriers.

Next is the dilemma of missing payers.

Smart hospital development is inherently a long-term investment, with the benefits accruing from its implementation increasing over time.

Under the DRG system, the operational logic of hospitals has undergone a fundamental shift. With the gradual reduction or elimination of revenue streams from drug and medical device markups, as well as laboratory and diagnostic testing fees, many hospitals have yet to adapt to the new business model and are already facing financial distress. Consequently, they are either cutting smart hospital initiatives to reduce costs or delaying and scaling back planned construction projects.

At this juncture, hospitals prefer to allocate funds to IT infrastructure that is mandated by policy, essential, and revenue-generating. As a result, AI companies, including Unisound AI Technology Co., Ltd., are struggling to identify new growth opportunities in this sector.

The current state of Unisound’s medical division can be seen as a microcosm of the medical AI industry: while AI indeed delivers substantial value in healthcare settings, competition is overly intense due to product homogenization; although high-quality AI products can be commercialized, profitability remains difficult to scale due to environmental constraints.

For medical AI companies, the solution to the aforementioned dilemma lies in patience. Most already have a comprehensive product portfolio; what they need now is time for their solutions to mature and for revenue scale to gradually take shape.

But Unisound had no time to wait. Under the pressure of redeeming liabilities, it had to play its final card: an IPO.

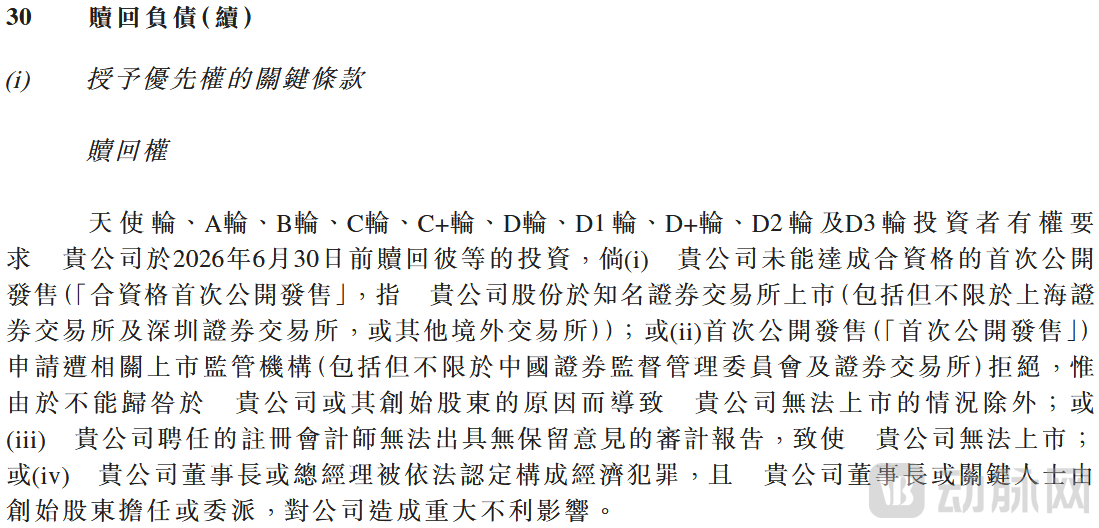

Under the redemption liability agreement, Unisound is required to complete its IPO by the agreed-upon deadline (Image source: Unisound’s prospectus)

Under the redemption liability agreement, Unisound is required to complete its IPO by the agreed-upon deadline (Image source: Unisound’s prospectus)

In recent years, Unisound’s external visibility in the healthcare sector has significantly diminished compared to before, as the company has redirected more resources toward smart living and intensified its promotion of businesses such as AGI and chips.

Today, Unisound has entered its most critical year. The smart healthcare segment struggles to bear the burden of short-term loss mitigation, while the smart living sector has indeed demonstrated the potential for a turnaround.