Domestic Players Lead the Emerging High-End Imaging Equipment Segment: 3D C-Arm Market Revolution

First Imaging

Medical 3D Imaging Equipment R&D Service Provider

Tuodao Medical

Surgical Robot Developer

Perlove Medical

Developer, Manufacturer, and Distributor of Medical X-ray Imaging Equipment

Mobile C-arm systems, known as the “eyes of surgery,” play a crucial role in clinical operations. They provide precise preoperative positioning, intraoperative fluoroscopic visualization, and postoperative recovery assessment for procedures such as orthopedic internal fixation, joint replacement, and vertebroplasty for thoracolumbar compression fractures. Consequently, they are widely available in hospitals; based on current installed base averages, nearly every operating room is equipped with one unit.

However, over the past three decades, the global C-arm market has been firmly dominated by imaging giants such as GPS. Leveraging first-mover technological advantages and comprehensive industrial chain layouts, these companies have established formidable market barriers. Domestic manufacturers have long remained in a catch-up phase regarding core technologies, product performance, and clinical recognition, making their path to breakthrough exceedingly difficult.

The turning point began with the iteration of technology and the explosive growth in demand for precision imaging.

Rapid advancements in minimally invasive surgery, precision orthopedics, and other technologies have recently generated new clinical demands for intraoperative 3D imaging, low radiation dose, and intelligent navigation. These requirements call for higher image dimensionality and quality, exceeding the capabilities of traditional 2D C-arm systems, thus urgently necessitating an imaging revolution to break through current bottlenecks.

Some domestic manufacturers have keenly seized this opportunity, leveraging 3D C-arm systems to capitalize on the window for equipment upgrades and iterations. In just ten years, a group of Chinese enterprises, including First Imaging, Perlove Medical, and Tuodao Medical, has rapidly risen. They have not only mastered core technologies such as cone-beam CT reconstruction algorithms and dynamic flat-panel detectors but also independently manufacture a full range of C-arm models, catering to complex surgical procedures in tertiary hospitals as well as basic needs in primary care clinics.

Today, the breach they have created is gradually taking shape. According to statistics from MDCLOUD (Medical Device Data Cloud), in the first half of 2023, the ratio of winning bids to total sales volume (including traditional C-arm machines and 3D C-arm machines) for First Imaging and Perlove Medical was 1.6% and 1.3%, respectively. They have secured the top two positions in the 3D C-arm machine market in China, reshaping a market landscape long dominated by international brands. Based on bidding data from the first half of 2025, First Imaging has surpassed imported brands to become the number one player in terms of market share for 3D C-arm machines in China.

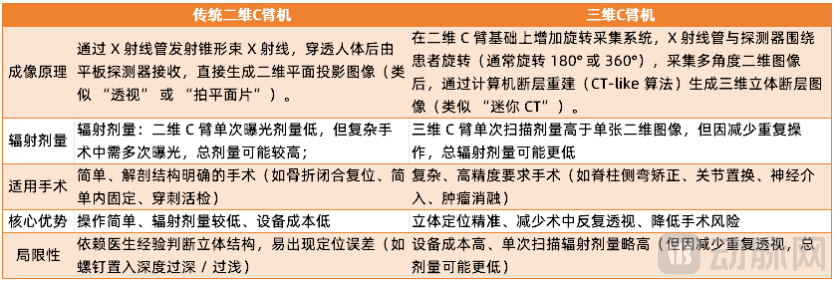

The so-called 3D C-arm refers to a system that employs cone-beam CT (CBCT) imaging technology, in which the C-arm drives the X-ray tube and flat-panel detector to rotate around the human body. During rotation, the detector acquires projection data of X-rays passing through the body from multiple angles. These data contain information from various anatomical planes and perspectives. With the aid of computers and specific algorithms, the acquired large volume of projection data is processed and reconstructed into three-dimensional images.

Compared to traditional C-arm systems that only provide two-dimensional planar images, 3D C-arm systems can generate cross-sectional, sagittal, and coronal tomographic images as well as three-dimensional volumetric images. This enables a 360° comprehensive visualization of the surgical site, allowing physicians to more intuitively analyze the three-dimensional spatial relationship between lesions and surrounding tissues.

In terms of imaging speed, traditional C-arm systems require multiple repositioning and angle adjustments to acquire multi-angle data, resulting in prolonged overall procedure time. In contrast, certain 3D C-arm systems can complete intraoperative 3D scanning within one minute. Taking First Imaging’s 3D C-arm system as an example, the device completes 3D image acquisition in under 30 seconds and is compatible with mainstream navigation and robotic systems to enable autonomous registration and alignment, thereby saving significant time during surgery.

Furthermore, 3D C-arm systems are typically equipped with large-sized dynamic flat-panel detectors. For instance, the PLX C7500A by Nanjing Perlove Medical Equipment Co., Ltd. adopts a 30 cm × 30 cm dynamic flat-panel detector with a 16-bit grayscale depth, enabling the output of high-resolution images that clearly display the position and contours of implants. Meanwhile, certain 3D C-arm systems feature isocentric scanning technology, which helps avoid artifacts caused by C-arm gantry movement, thereby further enhancing image clarity.

Radiation Dose Is a Growing Concern Among Patients. Although traditional C-arm systems deliver a low radiation dose per exposure, they often require multiple exposures during surgery. In contrast, while a single scan with a 3D C-arm system delivers a higher radiation dose than a single 2D image, it captures complete imaging data in just one exposure. In complex surgical procedures, the total radiation dose from a 3D C-arm system is likely lower than that from a traditional C-arm system, significantly reducing the number of radiation exposures for both physicians and patients.

Comparison of Advantages Between 2D C-arm and 3D C-arm Systems

Overall, in the niche market of C-arm systems, 3D-enabled devices can achieve comprehensive upgrades in functions such as 3D reconstruction, surgical path planning, real-time navigation support, precise lesion localization, and surgical outcome assessment, thereby fully replacing traditional C-arm systems. Furthermore, as technologies like surgical navigation/robotics and artificial intelligence are increasingly implemented in hospitals, the clinical value of 3D imaging will become ever more prominent.

However, while 3D C-arm systems have significantly expanded performance capabilities compared to traditional C-arm systems, they have also led to a sharp increase in price. According to Tuodao Medical, the prices of imported 3D C-arm systems from brands such as Siemens and Ziehm Imaging are generally around RMB 3 million to 6 million, while those of domestic brands fall within the range of RMB 2 million to 3 million.

Compared to traditional C-arm machines, which are priced under one million yuan, the higher cost of 3D C-arm systems has somewhat hindered their market penetration. In an economic downturn, not every medical institution can afford the relatively expensive new-generation C-arm machines.

Despite its disadvantage in unit price, the 3D C-arm system is still rapidly capturing the market share held by traditional C-arm systems at a visibly accelerating pace.

Data provided by First Imaging shows that traditional 2D C-arm systems currently dominate the market, with annual sales of approximately 3,000–4,000 units. Although 3D C-arm systems hold only a 5% market share, they are experiencing significant growth, with an annual growth rate of 15%–20%, far exceeding the 5%–8% annual growth rate of 2D systems.

In the first half of 2024, both the market size and market share of domestic 2D mobile C-arms in China showed a downward trend. The market size decreased by 36.27% compared to the same period in 2023, while the market share dropped by 23.54%. In contrast, the market size and market share of 3D C-arm systems exhibited an upward trend. The market size increased by 36% year-on-year compared to the same period in 2023, and the sales volume (in units) accounted for a 50% year-on-year increase in market share.

At the current stage, the motivations for medical institutions to acquire 3D C-arm systems can be categorized into two types: first, routine equipment replacement within the existing market, where hospitals that have previously purchased C-arm systems naturally upgrade to imaging devices with superior performance; second, integration with surgical robots, which predominantly belongs to the incremental market, enabling innovations in surgical procedures or indications and enhancing hospital competitiveness.

Tuodao Medical told VCBeat that routine equipment upgrades at medical institutions currently account for the vast majority of 3D C-arm system sales. With incomparable advantages over traditional equipment in terms of imaging quality, speed, and coverage, the transition from 2D to 3D imaging is irreversible.

In the short term, the penetration rate of 3D C-arm systems will remain limited; however, as the previous generation of 2D C-arm systems is fully phased out, 3D C-arm systems will gradually capture the market.

Although the incremental market brought by surgical robots is currently small, it holds promising future prospects. First Imaging believes that, just as GPS navigation is to autonomous driving, intraoperative imaging serves as the "eyes" of surgical navigation systems and robots. Especially in the era of precision medicine, intraoperative imaging equipment has evolved from mere visualization tools into "data hubs," providing three-dimensional anatomical structures while also enabling deep processing of imaging data.

Adapting between different hardware systems is no easy task. Domestic latecomers such as First Imaging have introduced the RoboLINK protocol, capitalizing on the trend toward synergy between 3D C-arm machines and surgical robots. Tuodao Medical has also independently developed an endoscopic surgical robot following the launch of its 3D C-arm machine, taking an indirect route into the surgical robotics market.

In terms of competitiveness, with the widespread adoption of hybrid operating rooms, many multinational corporations have achieved deep integration of 3D C-arm systems with technologies such as robotic systems and augmented reality. For example, Medtronic’s O-Arm works in synergy with the Mazor spinal robot.

Domestic companies, though slightly behind, are poised to leverage their industrial strengths in deep learning to integrate features such as 3D image denoising and automated anatomical recognition into their equipment, thereby establishing a unique advantage in the digitalization and intelligentization of medical devices.

In the future, the incremental market driven by surgical robots may rival the existing market, becoming the greatest impetus for the commercial adoption of 3D C-arm systems.

According to bidding data from 2024 and the first half of 2025, the number of standalone tenders for 3D C-arm systems (excluding those bundled with navigation or robotic systems) has also shown rapid growth, confirming that 3D high-definition imaging technology is accelerating its penetration into clinical applications. As minimally invasive surgery evolves toward greater precision and intelligence, 3D imaging technology, with its multifaceted advantages, has become one of the core tools for enhancing surgical safety and efficiency. The transition of this technology from an “innovative option” to a “standard configuration” fully reflects the industry’s widespread recognition of the clinical value of 3D imaging, which is poised to further reshape the new paradigm of surgical practice.

Driven by these two key factors, high-end, tertiary Grade-A demonstration hospitals have already established complete 3D C-arm systems to address intraoperative imaging and visualized digitalization challenges in complex surgeries.

For prefecture-level hospitals and those that have not developed distinct advantages in complex surgical specialties, there is a reserved attitude toward the procurement of 3D C-arm systems. They will comprehensively evaluate factors such as cost-effectiveness, policy drivers, and the extent of adoption of digital surgery before selecting brands and equipment within an appropriate range.

It should be noted that the trade-in program for medical equipment in county-level medical consortia, launched in 2025, along with centralized procurement by provincial and municipal health commissions, may to some extent curb the widespread adoption of 3D C-arm systems.

After all, in the trade-in programs for medical equipment within county-level medical consortia in certain provinces and cities, C-arm machines originally priced at over one million yuan have been driven down to under 200,000 yuan. This strategy of exchanging price for volume is bound to capture a portion of the market that may have upgrade needs.

Fortunately, 3D C-arm systems were not included in this round of centralized procurement, and the likelihood of their inclusion in future rounds remains extremely low.

It is foreseeable that the next 3–5 years will be a critical juncture for startups in the 3D C-arm sector. Remaining outside the scope of centralized volume-based procurement allows them to retain profit margins, and the accumulated profits will become their core strength in catching up with multinational corporations (MNCs).