Medical Giants Bet Big on Surgical Robots Amid Market Transformation

Olympus

Precision Machinery and Instrumentation R&D, Production, and Sales

United Imaging

High-end Medical Device Developer

Mindray

Medical Device R&D Manufacturer

Amid the turbulent times for surgical robots, medical giants are placing heavy bets.

United Imaging’s uIntervC550 percutaneous interventional robot has just received regulatory approval, prompting Mindray to immediately announce its acceleration of technological breakthroughs and scaled development in surgical robotics, aiming to reach world-class standards and directly challenge the da Vinci system.

In less than a month, Olympus, the global leader in endoscopy, joined forces with Revival Healthcare Capital to make a significant investment of up to $458 million (approximately RMB 3.272 billion) in establishing Swan EndoSurgical, making a decisive entry into the surgical robotics sector and stirring up the multi-billion-dollar market.

Surgical robots possess an aesthetic of economic upswing.

Surgical Robots: A Convergence of Love and Hope

After the first batch of patents for the da Vinci Surgical System expired in 2018, medical device giants such as Medtronic, Johnson & Johnson, Siemens, and Stryker collectively invested $6.7 billion to acquire entry into the surgical robotics market through acquisitions. Globally, a wave of startups has emerged to explore the application of this technology across various surgical procedures. In the Chinese market, there have been over 100 financing rounds in the past five years alone, with 110 products receiving regulatory approval.

However, after several years of development, this market has been missing onlythe presence of China's medical device giants. Yet, innovation in robotic systems for digestive endoscopic surgery remains scarce., it was not until late last year that Endoquest Robotics became the only company to receive an Investigational Device Exemption (IDE) from the U.S. FDA.

United Imaging, Mindray, and Olympus have finally stepped out of their comfort zones and are attempting to reshape this landscape.

Unlike Medtronic, Johnson & Johnson, Siemens, and Stryker, which have expanded their corporate footprints through acquisitions, latecomers such as United Imaging, Mindray, and Olympus have all chosen the path of independent R&D.

Behind this choice lies the three giants’ clear-eyed assessment of the sector’s development stage: Today’s surgical robots are no longer in the early “land grab” phase of a blank slate. Localized innovation can hardly be achieved through acquisitions; entering the market now almost exclusively requires in-house R&D to precisely align with clinical needs. To build defensible moats in this crowded arena, companies must extend their core corporate DNA and establish new, closed-loop business models.

Faced with this challenging path, the three companies have carved out differentiated strategies based on their respective endowments.

United ImagingAdopting a high-stakes, all-scenario self-development strategy in an attempt to replicate the breakthrough path of past domestication efforts for high-end medical equipment;MindrayLeveraging a steady advancement strategy rooted in deep industrial chain integration, it has built the momentum to catch up with da Vinci in the field of endoscopic surgery; andOlympusIt leverages the differentiated strategic resolve of an endoscopy market leader to lay the groundwork for reshaping the rules in the blue ocean of digestive endoscopic surgical robots.

The Landscape of Surgical Robots: A New Set of Survival Rules and Clear Generational Divides

Breaking the Deadlock: United Imaging Has Many Paths to Choose From.

As one of the few companies worldwide capable of providing high-end imaging equipment such as CT, MRI, and PET-CT, United Imaging has devoted significant efforts in recent years to developing clinical diagnosis and treatment solutions. Its full-chain technical system, spanning from hardware design to algorithm optimization, combined with its deep strategic layout in fields such as minimally invasive surgery, cardiac health management, and dual-guidance visualization systems, has laid the groundwork for United Imaging’s multi-pronged breakthroughs in the surgical robotics sector.

United Imaging, which for the first time disclosed its surgical robot portfolio in its 2024 annual report,The product line has expanded to cover multiple scenarios, including neurosurgery, orthopedics, percutaneous puncture, and endoscopy.. In the uNav-Brain 550 neurosurgical robot, United Imaging further leverages its independently developed innovative platform to achieve preoperative multimodal image fusion and reconstruction, lesion segmentation and quantification, and stereotactic surgical planning through real-time CT imaging guidance.

United Imaging's core strengths lie in“AI + Imaging + Devices”Tripartite In-House R&D. By modularizing imaging technologies to form a reusable technical middle platform, and extending algorithmic capabilities into the field of surgical robotics, United Imaging has established a foundation for its development in this sector. Furthermore, the in-house research, development, and manufacturing of core components across various product lines have significantly improved the calibration and adaptation efficiency between hardware components, as well as between hardware and software. This enables low-latency real-time response, which has become a differentiated advantage for United Imaging.

This fully self-developed ecosystem model has enabled United Imaging to continuously break the foreign monopoly in the high-end sector and bring multiple industry-first products to market.

However, this relatively aggressive approach is not replicable by all enterprises and is also forcing the industry to accelerate independent research and development across the entire value chain.

In contrast, Mindray has pursued a steady and pragmatic growth strategy.

AtIn 2012, Mindray acquired Hangzhou Guangdian, entering the minimally invasive surgery industry.Mindray recognized the potential of the minimally invasive surgery market at an early stage and has continuously strengthened its presence in the advanced minimally invasive surgical instruments market in recent years. However, it has not been as aggressive as United Imaging in the field of surgical robots, only officially announcing its active exploration of the surgical robot business in 2023.

Mindray’s core strength lies in its status as an all-around player in the “small equipment” sector.The company excels at developing products that require no dedicated departmental adaptation, operate efficiently within limited spaces, and enjoy strong demand from hospitals—a domain in which Mindray has virtually no rivals in China.However, Mindray’s prior involvement in the research, development, and commercialization of high-end medical equipment has been relatively limited.Entering the surgical robotics market marks Mindray’s first step into the field of high-end, large-scale medical equipment.

This is far from a simple business expansion for Mindray; rather, it represents a strategic move in its transformation from a medical device manufacturer to a healthcare technology platform. Through technological synergy, full-industry-chain integration, and global deployment, Mindray is poised to seize the initiative in the wave of domestic substitution and compete on equal footing with giants such as the da Vinci Surgical System in the international market.

Compared with United Imaging and Mindray, Olympus’s choice is more ambitious. AsThe Giant Holding a 70% Share of the Global Gastrointestinal Endoscopy Market, it did not choose to lay out its strategy based on the existing technological pathways in the market, but ratherLeveraging its absolute monopoly in gastrointestinal endoscopy, it is betting on digestive endoscopic surgical robots (natural orifice surgical robots).

Due to the extremely high technical barriers associated with natural orifice surgical robots, the development of this technology remains in its early stages across various countries. In terms of approved products and the overall market landscape in China, natural orifice surgical robots still represent a blue ocean opportunity. Currently, the approved products are primarily the Monarch bronchoscopic surgical robot under Johnson & Johnson and the Ion bronchoscopic surgical robot under Intuitive Surgical. Domestic manufacturers such as Allwell Medical, RoboMedical, Longhe Medical, and Qiaojie Li are all in the product research and development phase.

In this field,Olympus has not followed the technological paths of Johnson & Johnson and Intuitive Surgical; instead, it has focused on entering the market through the treatment of gastrointestinal diseases, with its core advantage being its proprietary endoscopic imaging technology.

Olympus aims to define new surgical standards in fields such as the gastrointestinal tract by combining imaging with flexible robotic arms, evolving from an endoscopy leader into a rule-maker for natural orifice robots.

Generally, natural orifice surgical robots comprise one camera and two robotic arms, with the end-effectors of the arms equipped with forceps and an electrocautery knife, respectively. In 2018, EndoPicasso, China’s first digestive endoscopic surgical robot developed by RoboMedical, adopted a master-slave control architecture. It features one camera embedded within the endoscope, two robotic arms with end-effectors consisting of forceps and an electrocautery knife, as well as gas and fluid channels. Its design has evolved from initially mounting operating arms on the exterior of conventional endoscopes to later integrating the endoscope and operating arms into a single ultra-thin tube, while continuously reducing the diameter of the operating arms and optimizing the design to minimize the diameter of the ultra-thin tube.

Despite its seemingly simple structure, this technology presents two major challenges: the imaging system and the surgical instruments.

Currently, the endoscopic systems integrated by manufacturers that have publicly disclosed product information mainly adopt existing laparoscopic systems available on the market. However, surgical instruments must overcome the movement limitations of rigid joints in Da Vinci-style laparoscopic robotic systems, while strictly controlling their dimensions to balance force and flexibility within narrow, tortuous natural lumens, thereby enabling diagnostic and therapeutic procedures such as biopsy and resection. Furthermore, these flexible robotic arms impose extremely high requirements on the interaction between physicians and the system. Fully flexible systems or those compatible with general-purpose endoscopes remain virtually nonexistent both domestically and internationally.

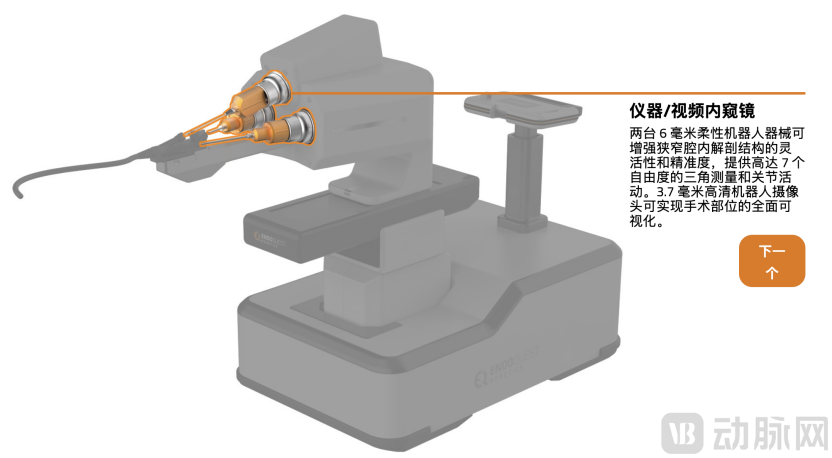

In this field, only Endoquest Robotics has obtained an Investigational Device Exemption (IDE) from the U.S. FDA. Its developed system provides complete visualization of the surgical site while simultaneously manipulating two 6-mm surgical instruments and one 3.7-mm third-party flexible endoscope (Olympus GIF-XP190).

This detail is precisely the key signal:Endoquest Robotics, a leader in development pace, still relies on Olympus for its core endoscopic components.Leveraging its optical technology barriers, Olympus dominates the gastrointestinal endoscopy market with a 70% share.

Just as da Vinci established an advantage in image quality by leveraging its exclusive monopoly on German laparoscopic modules, Olympus’s absolute dominance in endoscopic imaging technology will also build an unshakable industry position for the company.

Strategic choices rooted in its genetic makeup may well be the key source of confidence enabling Olympus to break through in high-barrier sectors. Armed with the dual advantages of its proprietary imaging systems and market dominance, Olympus enjoys broader room for R&D and technological exploration, holding significant potential to create new possibilities for the development of gastrointestinal surgical robots.

Next, the challenges remaining for Olympus may be limited to issues such as how to perfectly couple the force control of flexible robotic arms with the complex environment of natural orifices. The solutions to these problems will determine whether Olympus can truly evolve from a dominant player in endoscopy into the definer of natural orifice robots.

In the surgical robotics arena, both United Imaging and Mindray are striving to break out of their comfort zones while completing their business portfolios. Given the relatively mild impact of centralized procurement on high-end medical devices driven by hard technology, this move serves not only as a strategic response to centralized procurement but also as a key step toward internationalization and unlocking new growth avenues. Meanwhile, Olympus faces an increasingly competitive endoscopy market, where it is building a closed-loop system from diagnosis to treatment in an effort to identify new sources of business growth.

At the heart of this competition lies not merely who breaks through first, but who can most deeply couple their strengths with clinical needs. From Johnson & Johnson, Medtronic, and Stryker to today’s United Imaging, Mindray, and Olympus, the golden age of surgical robotics may only just be beginning.