Sinopharm Subsidiary Lists 51% Stake in Guoyao Hasen for RMB 155 Million Amid Strategic Restructuring

On July 31, 2025, Shanghai Modern Pharmaceutical Co., Ltd. (hereinafter referred to as “Sinopharm Modern”), a listed company under China National Pharmaceutical Group Corporation, announced that it had publicly listed for transfer its 51% equity interest in Shanghai Xiandai Hasen (Shangqiu) Pharmaceutical Co., Ltd. (hereinafter referred to as “Sinopharm Hasen”) at the Shanghai United Assets and Equity Exchange on July 30, 2025, with a minimum listing price of RMB 155.192541 million (over RMB 155 million).

In fact, on July 1, 2025, Shanghai Modern Pharmaceutical Co., Ltd. disclosed the “Announcement on the Pre-listing for Public Transfer of Equity in a Controlled Subsidiary.” To advance the implementation of the company’s medium- and long-term strategic plan, optimize resource allocation, and improve the operational efficiency of corporate assets, the company intends to publicly list and transfer its 51% equity stake in its controlled subsidiary, Shanghai Xiandai Hasen (Shangqiu) Pharmaceutical Co., Ltd. This listing formally disclosed the reserve price.

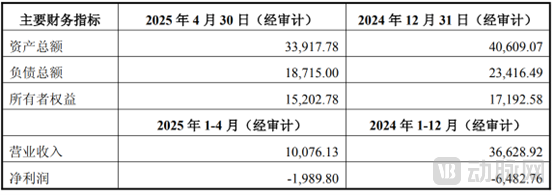

According to the announcement, as of April 30, 2025, Sinopharm Hasen’s net assets amounted to RMB 152.0278 million. Based on the asset appraisal report, with April 30, 2025 as the valuation reference date and using the asset-based approach, the assessed value of Sinopharm Hasen’s total shareholders’ equity was RMB 304.2991 million, representing an increase of RMB 152.2713 million over the audited book value of net assets, with a premium rate of 100.16%.

The integration of production, academia, and research has taken shape, yet the company has failed to turn losses into profits.

Sinopharm Hasen is a holding company invested and established by Sinopharm Modern, a listed company. Its controlling shareholder is China National Pharmaceutical Group Corporation (Sinopharm). Currently, it has developed into a diversified and modern national essential medicine production base integrating pharmaceutical R&D, manufacturing, and sales.

To date, Sinopharm Hasen covers an area of over 500 mu, with a registered capital of RMB 83.29 million and total assets exceeding RMB 600 million. The company employs more than 1,600 staff members, including over 800 professional and technical personnel. It has obtained marketing authorizations for 163 pharmaceutical products and operates GMP-compliant production lines for various dosage forms, including small-volume injections, oral solid dosages (including tablets, capsules, and granules), and active pharmaceutical ingredients (APIs). The annual production capacity stands at 4 billion units for small-volume injections, 6 billion units (tablets, capsules, or sachets) for oral solid dosages, and 1,200 metric tons for APIs.

Sinopharm Hasen, formerly known as Shangqiu Hasen Pharmaceutical Co., Ltd., was established on November 12, 1999. Located at No. 12 Yong’an Street, Shangqiu City, the company is a corporate entity formed through the bankruptcy restructuring of the former Shangqiu Pharmaceutical Factory. In August 2004, the company entered into an equity partnership with Sinopharm Holdings and was renamed Shanghai Xiandai Hasen (Shangqiu) Pharmaceutical Co., Ltd., with Sinopharm Modern holding a 51% stake and the original individual shareholders of Shangqiu Hasen Pharmaceutical retaining a 49% stake.

Sinopharm Hasen was recognized as a “High-Tech Enterprise” in 2009; in April 2010, Sinopharm Hasen was integrated into Sinopharm Group together with Shanghai Modern Pharmaceutical; in 2014, Sinopharm Hasen established the Henan Branch of the Shanghai Institute of Pharmaceutical Industry.

In 2016, Sinopharm Group restructured Shanghai Modern Pharmaceutical Co., Ltd. (Shanghai Modern), designating it as the group’s industrial platform for chemical pharmaceuticals, with Shanghai Xiandai Hasen (Shangqiu) Pharmaceutical Co., Ltd. becoming a holding subsidiary of Shanghai Modern. By December 2016, the company had completed its overall relocation to the Sinopharm Industrial Park within the Liangyuan Industrial Agglomeration Zone in Shangqiu City, and its registered address was changed to No. 166 Xinxing Road, Liangyuan District, Shangqiu City.

Notably, leveraging the product R&D background and technical support of Sinopharm Group, the company established the Henan Branch of the China National Pharmaceutical Industry Research Institute and set up various R&D platforms, including a Postdoctoral Workstation for Overseas Returnees, an Academician Workstation for High-End Crystalline Drug R&D in Henan Province, and the Henan Provincial Engineering Technology Research Center for Antifungal Drugs. This has fostered an integrated model of production, education, and research. The company has successively undertaken national-level Torch Program projects, as well as Henan Provincial high-tech industrialization and key scientific and technological tackling projects.

Furthermore, Sinopharm Hasen possesses quality testing instruments at a leading domestic level and has established a comprehensive quality assurance system, strictly implementing production and quality management in accordance with GMP standards. According to its official website, the company is also poised to become the largest manufacturer of small-volume injections and specialized chemical active pharmaceutical ingredients (APIs) in the bordering regions of Henan, Shandong, Jiangsu, and Anhui provinces, as well as the largest national essential medicines production base for Sinopharm Group in Henan Province.

In fact, if backed by robust hospital channels and a distribution network, Sinopharm Hasen’s current layout could unlock new business possibilities.

However, the transfer announcement bluntly points out the predicament of Sinopharm Hasen.

According to the announcement, Sinopharm Hasen currently has a small scale of products on sale, weak market competitiveness, and a high degree of product overlap with other subsidiaries under the company; since 2021, Sinopharm Hasen has been under continuous operational pressure, with consecutive losses. From past data, it is true that Sinopharm Hasen has fallen into a situation of continuous losses after 2021. In 2024, its revenue was 366 million yuan, but it lost 64.83 million yuan; from January to April 2025, its revenue was 101 million yuan, still losing 19.898 million yuan.

The company’s product portfolio has a limited scale of marketed varieties and exhibits a high degree of overlap with those of other subsidiaries under Shanghai Modern Pharmaceutical Co., Ltd. The cumulative effect of these factors has gradually made Shanghai Xiandai Hasen (Shangqiu) Pharmaceutical Co., Ltd. an operational burden on Shanghai Modern Pharmaceutical Co., Ltd.

An In-Depth Analysis of the Reasons for the Decline in Performance: The sales volume and prices of certain penicillin active pharmaceutical ingredients (APIs) and intermediates decreased year-on-year. In the formulation business segment, the sales revenue of certain cephalosporin, hormonal, and neurological products declined year-on-year, affected by factors such as centralized drug procurement and reduced end-user demand.

This transfer of equity in Sinopharm Hasen will help the Company continue to focus on its areas of competitive advantage and key development directions, further optimize its asset structure and resource allocation, improve the operational efficiency of its assets, and promote high-quality development.

From Scale to Efficiency: The Shift in Competition Among Traditional Giants

The “China Resources System,” often mentioned alongside the “Sinopharm System,” along with a host of other domestic pharmaceutical giants, began frequently listing non-core assets for sale in 2024. However, whether it is the “Sinopharm System” or the “China Resources System,” the intensive listing of subsidiaries—appearing as a “fire sale”—is in fact a proactive measure taken by state-owned pharmaceutical enterprises at the inflection point of the industry cycle.

A more significant turning point emerged at the end of 2024. In December 2024, the State-owned Assets Supervision and Administration Commission (SASAC) of the State Council incorporated the divestiture of “non-core businesses and non-performing assets” into the annual performance assessments of central state-owned enterprises (SOEs), establishing mandatory targets. Within less than six months of the policy’s implementation, two industry giants initiated a wave of “clearance-style” listings: Shanghai Modern Pharmaceutical Co., Ltd. offered a 51% equity stake in Shanghai Xiandai Hasen (Shangqiu) Pharmaceutical Co., Ltd. with a reserve price of RMB 155 million; China Resources Sanjiu transferred its 51% equity interest in Jointown Pharmaceutical Technology for RMB 10.86 million; while Boya Bio-pharmaceutical Group lowered its asking price three times yet still struggled to find a buyer.

Behind the flurry of activity lies the same cold calculation.

First, inefficient assets are dragging down the overall return on investment. Taking Sinopharm Hasen as an example, it incurred a loss of nearly RMB 20 million in the first four months of 2024. Moreover, its product portfolio in respiratory and central nervous system therapies overlaps with that of Sinopharm Modern. Continued financial support from the group will only exacerbate internal friction.

Secondly, the normalization of centralized procurement and declining gross margins have rapidly eroded the "scale dividend." The sales volume and prices of certain penicillin active pharmaceutical ingredients (APIs) and intermediates under Sinopharm Hasen declined year-on-year. In the finished dosage form segment, the sales revenue of certain cephalosporin, hormonal, and neurological products decreased year-on-year, affected by factors such as national centralized drug procurement and reduced terminal demand.

Therefore, against the backdrop of shrinking profit margins, “downsizing” has become the most direct approach to cost reduction: divesting loss-making or marginally profitable assets can generate immediate cash inflows.

Meanwhile, the sellers themselves are also “reshuffling their portfolios.” While divesting Haisen and Xinlibang, Sinopharm has consecutively acquired Pailin Bio and Shandong Pharmaceutical Glass, thereby extending its reach into downstream plasma resources and upstream pharmaceutical packaging materials. CR Sanjiu, for its part, has taken a controlling stake in Tasly and, through Kunyao, acquired Shenghuo, focusing on the high-barrier segments of CHC (Consumer Health Care) products and prescription drugs.

In other words, traditional giants are divesting “unprofitable” assets while doubling down on the “most profitable” ones. In essence, this involves withdrawing significant capital from inefficient businesses and reallocating it to sectors that align with policy directives, possess technological barriers, and enable channel synergies.

Therefore, this wave of “divestitures” is not a simple contraction, but a turning point for central state-owned pharmaceutical enterprises as they shift from the previous scale competition driven by “acquisition sprees” to an “efficiency race.”