China's Aesthetic Medicine Industry Faces Collective Growth Slowdown and Major Structural Adjustment

Galderma

Developer of Dermatological Medical Solutions

“Aesthetic medicine clinics are under significant pressure to grow their performance; even leading upstream companies are performing very poorly in China, with first-half performance completion rates below 50%.” This is the sentiment of a practitioner at an aesthetic medicine clinic located in the city center of a major Chinese metropolis.

The “2025 Annual Insights Report on China’s Medical Aesthetics Industry,” jointly released by Allergan Aesthetics and Deloitte, corroborates this sentiment: the overall growth of medical aesthetics institutions across China has slowed, with some regions even experiencing a short-term wave of clinic closures in 2024. The trend of consumption downgrading is gradually impacting the revenue side of the industry, leading to reduced income and customer inflows for medical aesthetics providers. This may help explain why “commercial battles” have frequently erupted in the medical aesthetics market.

When industry growth curves collectively stall, it may appear on the surface to be a market contraction, but in essence, it represents a reset of the rules of competition.

A senior insider in the medical aesthetics industry told VCBeat, “The ‘2025 Annual Insight Report on China’s Medical Aesthetics Industry’ shows that in 2024, the average transaction value per customer in the medical aesthetics sector decreased by 10% year-on-year, while the consumer base continued to expand. In 2024, the number of medical aesthetics consumers increased by 10.7% year-on-year, reaching 31 million.”

Based on current observations, the medical aesthetics industry is not experiencing a continuous decline but is undergoing structural adjustment.The supply side is undergoing accelerated reshuffling and differentiation, with the industry moving toward “compliance, quality, and branding.” Institutions that are non-compliant or offer poor service quality will gradually be eliminated, while those that are safe, high-quality, and transparent in pricing will enjoy greater room for development.

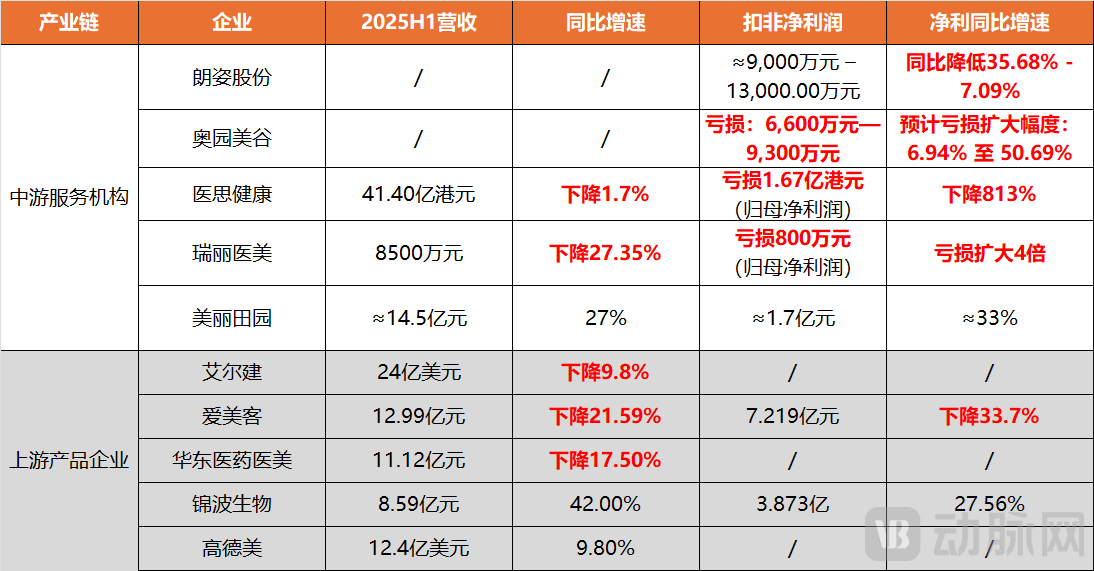

Performance of Selected Listed Medical Aesthetics Companies in the First Half of 2025 (Due to some companies issuing earnings forecasts, complete revenue data has not yet been disclosed, resulting in incomplete data presentation; EC Healthcare’s data is from its annual report as of March 31, 2025)

According to the financial reports for the first half of 2025 disclosed recently, multiple listed medical aesthetics companies have been affected by headwinds in the medical aesthetics market.

Market headwinds first hit midstream service providers.Taking Lancy Co., Ltd., Aoyuan Beauty Valley Technology Co., Ltd., and EC Healthcare as examples, these enterprises, despite owning multiple general hospitals or dozens of outpatient clinics under their banners, have generally experienced a decline in performance. Taking Lancy Co., Ltd. as an example, among its seven major medical aesthetics brands, six brands other than Jinfu Medical Aesthetics saw a significant drop in net profit in the first quarter of 2025, with declines exceeding 50% in nearly all cases.

Performance of Lancy Co., Ltd.'s Medical Aesthetics Divisions in Q1 2025

The collapse in performance of these large, integrated medical aesthetic hospitals is due to the market’s shift from a focus on plastic surgery to anti-aging treatments.“2025 Annual Insights Report on China’s Medical Aesthetics Industry” indicates that plastic surgery was once a significant revenue source for large institutions, contributing approximately 20% of their performance. However, due to high surgical risks, prolonged recovery periods, and irreversible outcomes, 62% of potential consumers have reduced their demand for plastic surgery, leading to a precipitous decline in the treatment rate for related procedures.

The headwinds in the medical aesthetics market have not only swept through midstream service providers but also extended upstream. Even hyaluronic acid and recombinant collagen, once regarded as growth myths, were not spared.

Juvéderm, the hyaluronic acid filler with the highest market share in China, is also unable to withstand the decline.Juvederm, hailed as the “Hermès of hyaluronic acid fillers,” is a product of Allergan, the world’s largest upstream company in the medical aesthetics industry. According to AbbVie’s Q2 2025 financial report, Allergan’s parent company, global sales in its aesthetics business amounted to approximately $1.3 billion, representing an 8% year-over-year decline. This downward trend has persisted for multiple consecutive quarters, indicating that the medical aesthetics business is unlikely to improve in the short term. In the Chinese market, Allergan has felt the chill even more acutely. During the Q1 2025 earnings conference call, Allergan specifically highlighted that headwinds in the Chinese economy led to a significant drop in Juvederm sales, which became the primary driver of the international performance decline in its aesthetics business.

Imeik, the domestic leader in hyaluronic acid fillers, also recorded its first post-IPO decline in revenue.. According to the 2025 semi-annual report disclosed by Imeik, the company achieved an operating revenue of RMB 1.299 billion during the reporting period, representing a year-on-year decline of 21.59%; net profit attributable to shareholders of the parent company amounted to RMB 789 million, with a year-on-year decrease of 29.57%.

The former growth myth—recombinant collagen—has not been spared, with its growth rate beginning to slow.Jinbo Bio, the leader in recombinant collagen, maintained growth in its performance in the first half of 2025; however, its year-on-year revenue growth rate of 42.43% and net profit growth rate of 26.65% both hit five-year lows.

It is not difficult to observe that the medical aesthetics market is undergoing a challenging period of adjustment, with overall growth facing significant headwinds.

However, there are also a few lucky ones among the listed companies in China's medical aesthetics market.Among midstream service providers, both Beauty Farm and So-Young’s light medical aesthetic clinics achieved revenue growth. In H1 2025, Beauty Farm recorded growth in both revenue and net profit, driven by its “dual beauty + dual healthcare” business model. In Q2 2025, So-Young’s revenue from aesthetic treatment services reached RMB 144.4 million, representing a 46% quarter-on-quarter increase.

Beauty Farm positions itself as a high-end dual-beauty institution; against the backdrop of a market downturn, its premium customer base demonstrates stronger counter-cyclical resilience.Strategically, Beauty Farm has also made early moves to expand its service categories through acquisitions, thereby enhancing its risk resilience. In 2024, it acquired Nayrier, a health and wellness institution, to increase its member assets and resources. By using body care services as an entry point to channel traffic to medical aesthetics, the company leverages the high-frequency consumption of lifestyle beauty services to drive its low-frequency medical aesthetics business.

SoYoung’s performance in personally entering the light medical aesthetics clinic sector also exceeded expectations.In the second quarter of this year, So-Young’s revenue from aesthetic treatment services reached RMB 144.4 million, representing a year-on-year increase of 426.1%. The revenue from aesthetic treatment services was primarily driven by So-Young’s chain of light medical aesthetic clinics. In November last year, So-Young officially launched its new light medical aesthetic chain brand, “So-Young Youth Clinic.”Currently, So-Young has opened 29 stores under its light medical aesthetics chain brand. Against the backdrop of a market downturn, 25 of these stores achieved positive monthly operating cash flow in June this year.

SoYoung stated to VCBeat: “SoYoung continues to explore service models that offer high quality at competitive prices. By integrating the industry and restructuring our cost structure through self-built marketing channels, centralized procurement, and digital-intelligent management, we enhance service quality and efficiency. This allows us to focus more on medical delivery rather than operations, diligently improving the quality of medical services to provide transparent, reasonable, safe, and consistently high-quality care. We believe that if consumers can find an institution that offers high-quality service, reasonable pricing, and satisfactory results, they will naturally return and recommend it to those around them.”

Upstream companies have also found new growth points in the fiercely competitive battlefield, with Galderma achieving strong growth in the Chinese market thanks to its new product, Sculptra.Galderma boasts a core product portfolio that includes hyaluronic acid dermal fillers, botulinum toxin, and Sculptra (poly-L-lactic acid). In the first half of 2025, Galderma’s injectable aesthetics business generated $1.24 billion in revenue, representing a year-on-year increase of 9.8%. The company highlighted particularly strong growth in injectable aesthetics across Brazil, Canada, China, Mexico, and the United Kingdom.The high growth achieved in the Chinese market is primarily attributable to the launch of the new product, Sculptra® (poly-L-lactic acid injectable filler), also known as the “youth-restoring injection.”

Insights from the “lucky ones” reveal that amid sluggish industry growth, traditional growth models have become ineffective. Only by adapting to the times, innovating products, and rediscovering and understanding user needs can sustainable growth be achieved.

What are the main factors posing challenges to the current growth of the medical aesthetics industry, amid coexisting risks and opportunities?

First, macroeconomic uncertainty is affecting consumer confidence.The overall macroeconomic situation influences residents’ income and consumer confidence, leading some individuals to reduce or defer spending on medical aesthetics due to financial pressures. Data from the “2025 Annual Insights Report on China’s Medical Aesthetics Industry” indicates that, overall, middle- and high-income consumers are adopting a more conservative approach to medical aesthetics expenditures: in 2024, 78% of consumers maintained or increased their spending on medical aesthetics; looking ahead to 2025, this proportion has declined to 57%.

Second, the increasingly fierce competition in the medical aesthetics industry also poses challenges to the sector.“A senior industry insider stated, ‘From the perspective of the medical aesthetics industry, in addition to the continuous expansion of traditional medical aesthetic institutions over the past two years, e-commerce platforms and cosmetics companies have been continuously entering the downstream segment of the medical aesthetics sector, further intensifying industry competition.’”

Third, beyond consumption downgrading and intensifying competition, another major challenge facing the industry is that numerous medical aesthetic institutions remain stubbornly clinging to a sinking ship amidst the sector’s dramatic upheaval.

A SoYoung representative pointed out, “A major challenge stems from industry inertia. The medical aesthetics sector’s business model, characterized by high average transaction values and heavy reliance on marketing, achieved success in the past. However, as demand shifts from surgical procedures to anti-aging treatments, consumers become increasingly rational, and average transaction values continue to decline, this marketing-driven approach will hinder institutional growth. There is an urgent need to transform downstream pricing, service, and sales systems. Currently, many medical aesthetic institutions remain focused on competing for high-spending customer segments. In fact, there is a substantial consumer base seeking both quality service and cost-effectiveness, representing a significant new growth market. Guided by this insight, SoYoung Youth Clinic strives to establish a standardized service model that delivers both quality and value.”

Aesthetic medicine consumption is expanding from a luxury to a mass-market category, and as the consumer base broadens, the logic driving market growth is also shifting.

Amid the combined pressures of consumption downgrading, intensifying industry competition, and a paradigm shift in industry development, the supply side of the medical aesthetics sector is overly saturated, while demand has become more rational and diversified, making an industry adjustment period inevitable.

During the industry adjustment period, the medical aesthetics sector has initiated consolidation. Currently, the midstream service providers in China’s medical aesthetics market feature low entry barriers and low concentration, with a CR5 of only 0.7%. Following structural adjustments, industry consolidation is expected to accelerate, driving an increase in market concentration. Taking Beauty Farm as an example, it has continuously expanded its market share through acquisitions in recent years.

Rather than a market downturn, the medical aesthetics industry is witnessing a seismic shift in consumer demand. Only enterprises capable of precisely meeting these demands and exercising refined cost control can successfully navigate economic cycles.

References:

"2025 Annual Insights Report on China's Medical Aesthetics Industry" – Deloitte & Allergan

Zhou Min, CFO of Beauty Farm: Aiming to Become a RMB 10 Billion Enterprise — CFO Career Circle