FDA Moves to Phase Out Animal Testing: Organoid + CRO Unlocks a $100B Market — Chinese Companies Lead the Global Race

When a new drug costs an average of $2 billion and takes 10 years to develop, yet the clinical translation rate remains below 10%, the entire pharmaceutical industry is waiting for a “game-changer.” Now, a new FDA policy provides the answer: phasing out animal testing and strongly promoting organoid technology, directly igniting a multi-billion-dollar market for alternatives. Even more encouragingly, Chinese companies have already taken an early lead in this arena, reshaping the drug R&D value chain with “miniature human organs”!

I. The Disruptive Moment: Why Are Organoids Leading the FDA to “Abandon” Animal Testing?

First, let’s understand the key player—organoids. These are not merely simple “cell clusters,” but 3D miniature organs “grown” from stem cells in the laboratory. They can replicate the authentic structure and function of livers, intestines, and even tumors, effectively creating an “in vitro human testing ground.”

Compared with traditional R&D tools, its advantages can be described as a "dimensionality-reduction strike":

Comparison Dimensions | Animal Models | 2D Cell Model | Organoids |

Structure and Function | Species-specific structures, significantly different from those in humans | Monolayer Cells, Without Organ-Level Structures | Replicate the 3D structure of human organs with a functional match rate > 80% |

Clinical Translation Efficiency | Clinical Failure Rate of Oncology Drugs > 90% | Inability to simulate complex physiological environments and low translational efficiency | Accurately Recapitulate Pathological States, Boosting Conversion Efficiency by Over 30% |

Drug Screening Cycle | 6–12 Months | 2–4 weeks (but with a single function) | 4–8 Weeks (Full Functionality) |

Single Screening Capability | Supports testing for only 1–2 drugs | Supports 100+ Drug Tests | Supports high-throughput screening of 100+ drugs |

Core Limitations | Species Differences Lead to Distorted Results | Unable to simulate inter-organ interactions | Maturity of Certain Complex Organs (e.g., the Brain) Remains to Be Improved |

When the FDA officially announced in April 2025 its “priority use of organoids to replace animal testing,” it effectively charted a new course for the industry: whoever masters organoid technology holds the “golden key” to drug development.

II. Policy Winds Blow Strongly! China, the U.S., and Europe Join Forces, Fully Opening Up Market Gaps

Not just the FDA, but regulatory agencies worldwide are giving the green light to organoids, with policy benefits becoming visibly abundant:

• U.S. FDA:Mandatory preclinical animal testing for new drugs was abolished in 2022; in 2025, further requirements were introduced to shorten the experimental cycle for monoclonal antibodies by 1–3 years, with organoid data becoming the “default standard” for regulatory submissions within five years, thereby reducing animal experiments to an “alternative option.”

• China CDE:In June 2025, organoids were directly incorporated as a core data source for rare disease drug development, addressing the pain points of “limited patient populations and challenging clinical trials,” and helping pharmaceutical companies bypass the traditional R&D “valley of death.”

• EU:In July 2024, a roadmap was finalized for release in Q1 2026 to comprehensively phase out animal testing for chemicals, with subsidies available to support the transition of small and medium-sized enterprises.

This is not merely policy support, but a global pharmaceutical industry “technology shift mandate.” As the traditional path of animal testing becomes blocked, the new route of organoids combined with CROs has instantly become the “golden channel” to a market worth hundreds of billions.

III. Capital Frenzy! Chinese Enterprises Secure Over 100 Million in Financing, Technical Prowess Rivals Global Standards

Capital always detects opportunities first. The domestic organoid sector has long been fiercely competitive, with leading companies securing hundreds of millions in financing based on their core strengths and even gaining endorsement from internationally recognized authorities:

• Danwang Medical:Established the world’s largest library of gastrointestinal organoid models (covering 1,000+ models and multiple organ-on-a-chip platforms), serving 300+ pharmaceutical companies; additionally, it has received endorsement from Hans Clevers, a leading authority in the field known as the “father of organoids,” gaining international recognition for its technological prowess and industry influence, and completed its Series A+ financing round in 2024.

• Oak Technology:A leading Chinese company in the commercialization of organ-on-a-chip technology, featuring 4 proprietary chip models and over 50 culture reagent kits, directly accelerates Investigational New Drug (IND) applications for pharmaceutical companies; it secured nearly RMB 100 million in Pre-B series financing in 2022.

• Xigeshengke:Leveraging the “AI + Organoids” Combo, It Raised Over RMB 70 Million in Its Pre-A Round in 2024, Optimizing Drug Screening Efficiency with Intelligent Algorithms to Become the New Favorite in the Sector

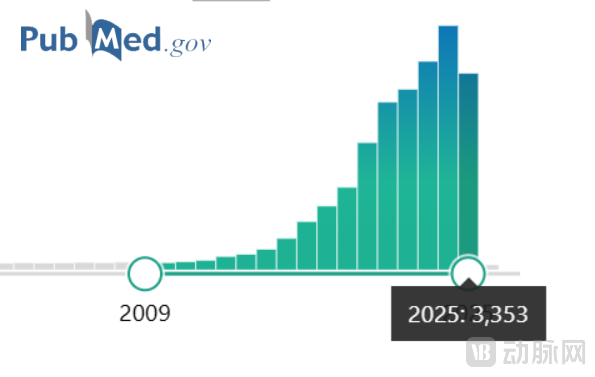

More notably, China has firmly secured the second position globally in organoid research, with 4,189 related papers published in 2024—a 116-fold increase from 2009. Underpinned by robust scientific research and fueled by capital investment, Chinese enterprises are transitioning from “followers” to “leaders.”

Number of Publications with "Organoids" in the Title Among Winning Bids from 2009 to 2025 (as of August 2025)

IV. How to Divide the RMB 100 Billion Cake? Preclinical CROs Emerge as the Biggest Beneficiaries

The explosion of organoids has directly activated the preclinical CRO sector, a “must-have” track:

• Global Market:Market size reached USD 5.72–20.91 billion in 2025 and is projected to surge to USD 36.96 billion by 2032, with a CAGR exceeding 8%.

• China Market:Accounted for 28.7% of the global market in 2024, it is projected to reach $2.1 billion by 2030, with a growth rate of 11.7%.

The integration of organoids is upgrading the CRO industry from “traditional contract manufacturing” to “precision empowerment.” While the past relied on animal testing as a matter of “trial and error,” organoids now enable precise screening, reducing ineffective R&D investment by over 30%. More importantly, the market for organoids and organ-on-a-chip technologies is projected to reach $15.6 billion by 2030, with a CAGR of 24%—three times that of traditional CROs!

V. The Future Is Here: These Three Types of Companies Will Have the Last Laugh

In the organoid + CRO sector, not every player can get a slice of the pie. Those who ultimately prevail will invariably possess these three traits:

1. Technical Barriers:Proprietary model library, self-developed equipment, or AI algorithms to address the pain points of “standardization and low cost”

2. Commercialization Capability:Capable of penetrating high-value scenarios such as IND filings for pharmaceutical companies and clinical antimicrobial susceptibility testing, avoiding the role of a mere “laboratory showpiece.”

3. Global Compliance:Data can be recognized by the FDA and CDE, obtaining a “pass” to enter the international market.

Conclusion: From “animal testing” to “organoids,” pharmaceutical R&D is undergoing a revolution. As the FDA’s new policies dismantle old regulations and Chinese companies’ technological prowess takes center stage on the global platform, the opportunities in this hundred-billion-yuan replacement market are now within reach. For practitioners, choosing the right technological direction is more critical than sheer effort; for investors, backing enterprises that excel in both “scientific research” and “commercialization” means seizing the next major industry trend.