LB Pharmaceuticals Raises $285 Million in IPO with Single CNS Asset LB-102

LB Pharma

Antipsychotic Drug Developer

On September 11, 2025, local time, as the opening bell rang on the Nasdaq, LB Pharmaceuticals (NASDAQ: LBRX, hereinafter referred to as “LB Pharma”), a neuroscience biotechnology company focused on psychiatric disorders, made a high-profile debut, dispelling the gloom that had hung over biotech listings in the U.S. stock market since the beginning of 2025.

LB Pharma completed its upsized IPO on September 10, 2025, pricing shares at $15 each. The offering of 19 million shares raised net proceeds of $285 million, significantly exceeding the initial target of $228.5 million, and was thus regarded by the industry as a breakthrough signal amid the financing “winter.”

A Differentiated Pipeline Underpins Asset Quality

LB Pharma’s official website lists only one core product: LB-102.

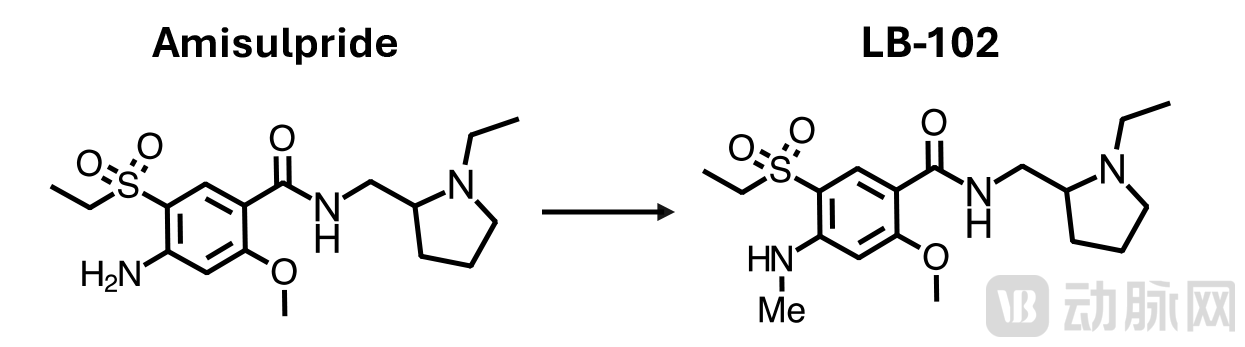

LB-102 is a methylated derivative of amisulpride. Amisulpride is a second-generation antipsychotic drug that has been approved in more than 50 countries (excluding the United States).

Therefore, to understand the mechanism of action of LB-102, it is essential to mention amisulpride. This dopamine antagonist, developed over four decades ago, primarily acts on D2, D3, and 5-HT7 receptors and is used in the treatment of schizophrenia. A 2019 network meta-analysis of 32 antipsychotic medications published in the top-tier journal The Lancet ranked amisulpride second in overall efficacy, first in improvement of positive symptoms, and third in improvement of negative symptoms. Subsequent head-to-head trials from the BeSt InTro study further confirmed its superiority over aripiprazole and olanzapine.

In terms of safety, amisulpride carries a significantly lower risk of weight gain than olanzapine and causes milder extrapyramidal symptoms, but it has two major drawbacks: hyperprolactinemia and QT interval prolongation.

Among more than 30 psychotropic agents, amisulpride ranks last in blood-brain barrier penetration. Consequently, its clinical dosage is as high as 400–800 mg/day, far exceeding that of cariprazine (1.5 mg) or brexpiprazole (4 mg). Such high doses inevitably lead to a sharp increase in systemic exposure, resulting primarily in amplified side effects (e.g., hyperprolactinemia and increased risk of long QT syndrome) and secondarily precluding the development of long-acting injectable (LAI) formulations. It must be acknowledged that this limitation is quite critical, as it runs counter to the current trend toward “long-acting, low-dose” therapies.

Thus, the development rationale for LB-102 is easy to understand.

LB-102 is a novel benzamide antipsychotic under development for the treatment of schizophrenia. The development of LB-102 aims to address the key limitations of amisulpride and existing therapies. Built upon the chemical foundation of amisulpride, LB-102 incorporates a subtle structural modification (a single methyl group) that enhances its ability to cross the blood-brain barrier while maintaining receptor potency and selectivity. This targeted modification enables once-daily oral administration and allows LB-102 to be dosed at lower levels than twice-daily amisulpride, with the goal of minimizing side effects, improving clinical outcomes, and enhancing patient adherence.

Through N-monomethylation of the benzamide ring, LB-102 achieved triple optimization:

Blood-brain barrier permeability increased by approximately 10-fold (PET brain uptake study);

Maintain high affinity and selectivity for D2/D3/5-HT7 receptors;

Allows for once-daily oral administration (50–100 mg), with a dose reduction of 75%–87.5% compared to the parent compound, potentially reducing the risk of hyperprolactinemia and QT prolongation.

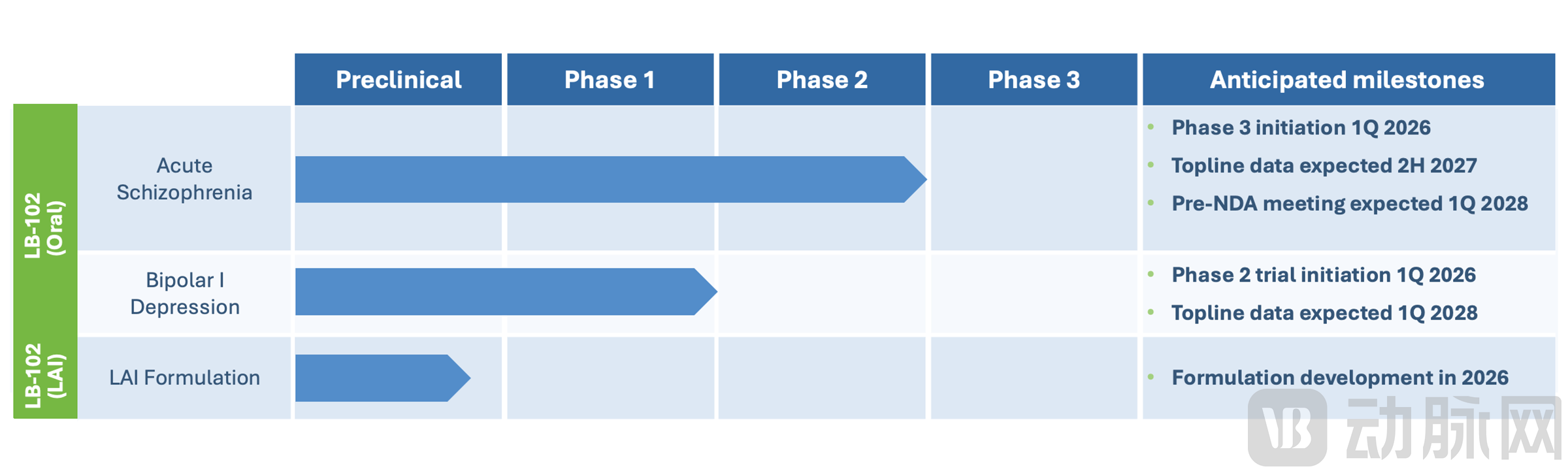

In early 2025,LB PharmaAnnounced that its investigational potential “first-in-class” benzamide antipsychotic drug successfully met the primary endpoint in Phase II clinical trials, paving the way for entry into the pivotal Phase III stage.

Top-line data from the Phase II trial (n=359) demonstrated: a significant improvement in the primary endpoint, total PANSS score, at 4 weeks (p<0.01); signals were also observed in the negative symptom subscale, suggesting the potential for “comprehensive symptom control”; the safety profile was similar to that of the parent drug, with no signals of extrapyramidal symptoms (EPS) and a low risk of QTc prolongation.

Meanwhile, LB Pharma is also developing a long-acting injectable (LAI) formulation of LB-102 as an alternative to the oral formulation, which has the potential to deliver better clinical outcomes and treatment adherence for patients with schizophrenia and bipolar depression. If approved, the long-acting formulation of LB-102 would offer additional advantages, including extending commercial protection for LB-102, providing a superior alternative to the currently limited number of approved LAI antipsychotics for treating other neuropsychiatric disorders such as bipolar disorder or Alzheimer’s disease psychosis, and strengthening LB-102’s global competitive barriers.

In the field of schizophrenia, there has been a lack of effective medications for negative symptoms; if Phase III trials are successful, LB-102 is poised to enter the high-end segment of the $6 billion global antipsychotic market.

Breaking Out of the U.S. Stock Market Slump Through Intense Competition

As such, LB Pharma’s 2025 IPO was regarded as a major highlight in the U.S. biotechnology sector, yet it is difficult to assert that capital markets will reignite their enthusiasm for the biopharmaceutical segment. Amid the triple pressures of macroeconomic policies, industry cycles, and investor sentiment, LB Pharma’s successful listing on Nasdaq reflects more a triumph of its own clinical data and the scarcity value of its therapeutic niche than a signal of a broad market recovery.

First, policy uncertainty remains the “Sword of Damocles” hanging over the entire industry. Since the Trump administration, U.S. domestic policies to curb drug prices have continued to escalate, with Medicare negotiation mechanisms for psychiatric and chronic disease medications becoming increasingly stringent, directly compressing the pricing space for future marketed drugs.

Anxiety over policy uncertainty has directly transmitted to the corporate valuation stage. In its initial prospectus filed in August 2025, LB Pharma planned to raise $100 million, but less than two weeks later, it increased the offering size to $285 million, with an issue price set at $15 per share, implying a market capitalization of approximately $300 million. However, this valuation level represents a discount compared to peer companies in the schizophrenia therapeutic area in 2024, indirectly reflecting investment banks’ discounted pricing for policy risks.

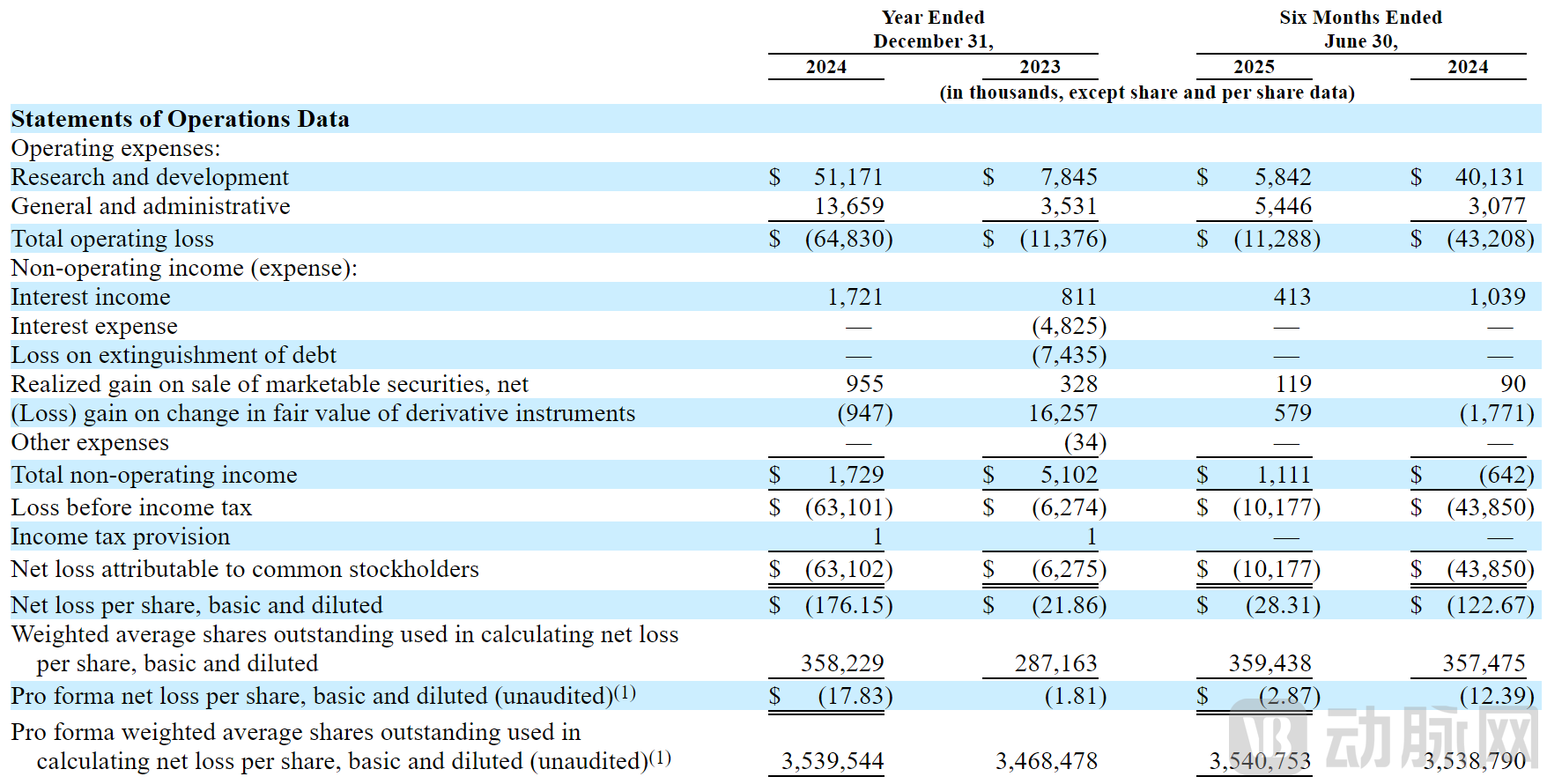

Notably, the prospectus reveals that LB Pharma currently has no revenue. Its operating losses for 2013 and 2024 were $11.38 million and $64.83 million, respectively, while net losses attributable to common shareholders were $6.28 million and $63.10 million, respectively. In the first half of 2025, LB Pharma reported an operating loss of $11.29 million, compared with an operating loss of $43.21 million in the same period of the previous year; its net loss attributable to common shareholders was $10.18 million, compared with $43.85 million in the same period of the previous year.

In summary, LB Pharma’s recent financing round was large in scale but valued relatively low, resulting in dilution of shareholders’ equity.

Moreover, if the majority of the funds raised in this offering are allocated to Phase III clinical trials, the company’s overall ability to withstand clinical development volatility will remain fragile.

The cooling sentiment in the U.S. biotech IPO market in 2025 has further amplified this vulnerability. Morgan Stanley pointed out that the U.S. biotechnology industry typically sees at least 12 companies go public each year, but in the first half of 2025, there were very few biotech IPOs on the U.S. stock market. According to data from Renaissance Capital, the number of biotech IPOs in the first half of 2025 fell to its lowest level since 2012.

The flip side of capital’s trend toward extreme rationality is the complete disenchantment with “startup stories.” Before 2021, a company could secure a valuation of hundreds of millions of dollars based solely on a novel dopamine receptor target or an AI-driven drug discovery algorithm. Today, investors demand hard metrics: at least completion of clinical trials, a clear regulatory pathway, and an indication with a market size meeting certain thresholds. LB Pharma has been fortunate in that its pipeline candidate, LB-102, precisely meets these three criteria: it achieved its primary endpoint in Phase II clinical trials; its Phase III protocol has reached a written agreement with the FDA; and there is a large patient population in the United States for mental disorders, coupled with significant unmet clinical needs.

LB Pharma also disclosed in its prospectus a five-year plan for indication expansion, including bipolar depression and agitation associated with Alzheimer’s disease, with peak sales estimated at $1.5 billion. These figures precisely tapped into investors’ current obsession with stability. This also explains the 20% surge in LB Pharma’s stock price on its first day of trading: it was not a renewed market favor toward biotech companies, but rather a one-time premium paid for “scarce certainty.”

Speculation on LB Pharma’s IPO in Hong Kong

Given this reality, one cannot help but wonder: if LB Pharma were a Chinese company listing in Hong Kong, what would the scenario look like? With the same molecule and the same clinical data, it would nonetheless follow a markedly different path to capitalization, owing to the vastly different institutional, financial, and policy environments.

Nearly half of the capital in the Hong Kong stock market is dominated by overseas institutions, aggregating financial resources from Europe, the United States, Southeast Asia, and other regions. This not only provides ample liquidity but also introduces cutting-edge technical insights and opportunities for cross-regional industrial synergy. Consequently, it was once regarded by domestic biotech companies as the core engine for establishing international commercialization channels.

In 2025, the healthcare sector in the Hong Kong stock market maintained strong financing momentum and innovative vitality, driven by policy support and market demand. Continuous optimizations of the Hong Kong listing rules have provided convenient financing channels for pre-profit biotechnology companies, while the introduction of various supportive policies has facilitated the research and development as well as market application of innovative drugs. Well-known pharmaceutical companies such as WuXi AppTec, Innovent Biologics, and Akeso all conducted secondary offerings at high valuations and gained market recognition.

At the institutional level, the Hong Kong Stock Exchange’s Chapter 18A listing rules and the recently introduced “Special Channel for Science and Technology Enterprises” have provided important financing avenues for pre-profit biotechnology companies and streamlined the IPO process.

Notably, amendments to the Hong Kong stock exchange listing rules have also been introduced, primarily optimizing the listing framework for specialized and sophisticated technology companies, particularly under Chapter 18C of the Main Board Listing Rules (hereinafter referred to as “Chapter 18C”). These revisions lower the minimum market capitalization thresholds for both commercialized and pre-commercialized companies and encourage technology companies already listed in Hong Kong to spin off eligible divisions for separate listings.

The contrast on the funding side is even more pronounced. In 2025, Hong Kong’s capital market witnessed a significant rebound. According to data from Sina Finance, IPO fundraising in the Hong Kong stock market reached HK$132.9 billion in the first eight months, hitting a four-year high and representing a 50% increase over the full-year total of 2024. More notably, the follow-on offering market performed even more strongly during the same period, with fundraising totaling HK$190.5 billion. This figure not only far exceeded IPO fundraising but also marked a 3.8-fold increase compared to the full-year follow-on offering volume of 2024. The average fundraising amount per transaction reached HK$1.1 billion, making it one of the key drivers boosting activity in the Hong Kong stock market.

From the perspective of industry financing, the top three sectors by financing volume are Information Technology, Consumer Discretionary, and Healthcare. Among these, the Healthcare sector raised HK$37 billion, occupying a significant position in the Hong Kong stock market’s secondary offering landscape. Notably, among the top ten largest refinancing deals in the Hong Kong stock market in 2025, innovative drug companies accounted for four spots, with a combined fundraising total of HK$19.9 billion. If a “Chinese version” of LB Pharma were to list in Hong Kong, backed by such a substantial capital pool, it would be highly likely to effectively avoid equity dilution.

Policy dividends have propelled biotech companies toward a higher dimension of certainty. The Several Measures to Support the High-Quality Development of Innovative Drugs (hereinafter referred to as the “Measures”), issued by the State Council in 2025, explicitly call for accelerating the review and approval process for market authorization of innovative drugs, particularly those addressing urgent clinical needs, thereby clearing obstacles to their rapid market launch.

When benchmarked against LB Pharma’s LB-102, the Measures not only focus on first-in-class (FIC) drugs but also support best-in-class (BIC) improved new drugs and generic drugs with significant clinical value, thereby building a diversified ecosystem for innovative drug research and development. This is precisely the positioning of LB-102.

A more subtle difference lies in the exit logic. The cooling IPO window in the U.S. stock market has forced venture capital firms to accept discounted M&A deals, while the new IPO regulations in Hong Kong have “loosened restrictions” on issuers, effectively opening a secondary exit channel for early-stage investors.

Thus, the same LB-102 has emerged as a top performer on NASDAQ and may also become a benchmark case in the wave of innovative drugs on the Hong Kong Stock Exchange: with a shorter regulatory pathway, a deeper capital pool, and more substantial policy dividends, both valuation and certainty are amplified in tandem. The intersection of these two trajectories reveals not the inherent quality of the company, but rather how different ecosystems shape the fate of the same seed. In the global race for innovative drugs, those who can provide a more favorable regulatory environment, more sustained funding, and greater policy certainty will enable biotech companies to fully realize their narratives.

The Global Investment Logic for Biotech Is Being Reshaped

However, whether on the Nasdaq or the Hong Kong Stock Exchange, “differentiated innovation” remains the common currency.

The investment thesis for LB Pharma’s U.S. listing rests on its significant reduction of QTc prolongation risk associated with legacy drugs, directly addressing a globally recognized clinical pain point. In the Hong Kong stock market, two companies with standout performance in 2025—GenFleet Therapeutics and Yinnuo Medicine—secured approval for China’s first KRAS G12C inhibitor and GLP-1 single-target injectable, respectively. Both share the common distinction of being “first-in-China,” leveraging regional scarcity to drive valuation.

Thus, LB Pharma’s IPO can be framed in two narratives: In the U.S. stock market, it stands as a unique case with breakthrough clinical value, demonstrating that only global best-in-class assets can pry open the frozen IPO window; in the mirrored imagination of the Hong Kong stock market, LB Pharma also holds the promise of leveraging the same Phase II data to secure a higher valuation and a faster listing.

At present, market divergence is no longer a cyclical fluctuation but a long-term structural pattern shaped by institutional frameworks, capital flows, and geopolitical factors. For Chinese biotech companies with drug pipelines in hand, choosing a market is tantamount to adopting a specific valuation paradigm. While both paths lead to capital, the barriers to entry, valuation premiums, and policy risks are incomparable to those of just a few years ago.

In the short term, the bullish momentum in Hong Kong stocks is likely to persist, driven by clear policy support and capital inflows; meanwhile, the recovery path for U.S. stocks remains fraught with challenges, hinging on policy clarity and the macroeconomic environment.

Returning to LB Pharma’s dramatic IPO. Undoubtedly, its impressive performance has injected a shot of adrenaline into the U.S. biotech sector, but this is more akin to an affirmation of “high-quality assets” rather than a clarion call for a comprehensive industry recovery.

On the other hand, the significance of this IPO extends far beyond a single company’s public listing; it serves as a “litmus test” for the biotechnology sector. LB Pharma’s listing has ended the prolonged IPO drought in the U.S. biotech market and provides a reference for other biotech firms awaiting their turn to go public. If LB Pharma’s stock price remains stable in the aftermath, it could spur more pharmaceutical companies to launch their own IPOs; conversely, if the stock falls below its offering price, it may prolong the sector’s slump and even force some companies to pivot toward private financing.

In the long run, the fundamental value of biotechnology lies in addressing unmet medical needs. Regardless of market fluctuations, companies with genuine innovative capabilities will ultimately find their place in the capital markets.