Radiology Partners Completes $2.3 Billion Debt Refinancing to Strengthen Financial Foundation and Accelerate Strategic Growth

RP

Diagnostic and Interventional Radiology Service Provider

Recently, Radiology Partners (RP), the largest medical imaging services company in the United States, announced the completion of a $2.3 billion (approximately RMB 16.4 billion) debt refinancing.

As one of the largest financing rounds since RP’s inception in 2012, this transaction has significantly optimized its capital structure by extending debt maturities and reducing interest costs, marking a pivotal turning point for the company as it moves away from financial pressure toward stable operations.

RP’s latest round of debt refinancing is not a strategic move for proactive expansion, but an inevitable choice to address financial distress under the dual pressures of policy and market conditions.

RP Secures $2.3 Billion in Debt Refinancing, News Report Source: Radiology Partners Official Website

The direct trigger for this refinancing was the cash flow crisis and debt pressure that RP faced for two consecutive years, with the root cause traceable to the compounded impact of both internal and external environments.

From a policy perspective, the No Surprises Act (NSA), which took effect in 2022, restricts healthcare institutions from charging patients “out-of-network fees” (detailed later), directly impacting RP’s core revenue streams. Although RP achieved an 85% win rate in related claims cases, its actual collection rate was only 15%, with a large volume of accounts receivable remaining uncollected. This resulted in negative cash flow for two consecutive years (2022–2023), serving as the first straw that broke the camel’s back financially.

From the perspective of the market environment, the Federal Reserve’s continuous interest rate hikes in 2023 triggered a surge in financing costs, while RP’s debt-to-earnings ratio had already reached as high as 11x, indicating elevated financial leverage. In January 2024, S&P Global Ratings classified its debt as “distressed,” downgraded its credit rating to “CC” (speculative grade), and explicitly highlighted the risk that “interest expenses are consuming cash flow.” More severely, the earlier debt restructuring attempt in early 2024 was deemed by S&P as a “distressed exchange” (a form of default) due to insufficient compensation to creditors, further exacerbating the difficulty in securing financing.

Furthermore, as the largest imaging services provider in the United States, RP serves 3,260 healthcare institutions; however, rising labor costs and declining accounts receivable turnover efficiency continue to erode profits. The contradiction between high leverage and low cash flow has triggered liquidity warnings, and without debt restructuring, the debt maturing in 2029 will face default risk.

To alleviate short-term cash flow pressures, RP initiated this transaction, which Moody’s—one of the three most authoritative international credit rating agencies—explicitly characterized in its rating report as a “comprehensive restructuring of first-lien debt.” The core objective is to achieve financial relief through maturity extensions, structural reorganization, and cost optimization.

In terms of maturity adjustment, the company extended the maturity date of its existing first-lien debt from 2029 to 2032, thereby securing a longer breathing space for itself.

The debt structure has been reorganized into three components: a $390 million revolving credit facility (maturing in 2030), a $1.5 billion term loan (maturing in 2032), and $800 million in notes (maturing in 2032), thereby establishing a more robust debt framework.

A particularly critical optimization measure was converting a significant portion of previously outstanding payment-in-kind (PIK) debt into cash-payment obligations, thereby further reducing future interest burdens and improving cash flow.

Notably, this transaction did not increase the debt scale but instead unlocked liquidity through debt extension and structural adjustments. As of March 31, 2024, RP held $130 million in cash and had $390 million in undrawn revolving credit facilities, establishing a safety cushion for subsequent operations.

RP CEO Rich Whitney stated, “The refinancing not only demonstrates our strong financial performance but also reflects investors’ confidence in our business model and strategy.” This successful capital operation has also cleared major obstacles for RP’s future development.

This round of debt refinancing has become a significant turning point for RP’s financial position and industry standing, with its impact evident in two dimensions: the company itself and the broader market landscape.

For RP, financial health has been restored: as of March 31, 2024, the debt-to-earnings ratio (leverage ratio) decreased from 10x to 7.7x, with Moody’s forecasting a further decline to 7x within the next 18 months.

More importantly, the company expects to generate over $75 million in free cash flow in 2024 and has uniformly extended its debt maturities to 2032, thereby eliminating near-term default risk and securing a critical window for operational recovery.

Capital market reactions have further corroborated this point. Although its credit rating remains in the high-risk category, both S&P and Moody’s have upgraded their outlooks to “Stable,” indicating market recognition of its financial recovery trajectory. Having emerged from the survival crisis, RP has been able to redirect resources toward core technologies and strategic mergers and acquisitions, thereby consolidating its market leadership position.

For the industry as a whole, the case of Radiology Partners (RP) serves as an important bellwether. It has demonstrated to the market that, even amid stringent policy challenges such as the No Surprises Act, the business model of large healthcare service providers remains resilient through proactive legal strategies (with high litigation success rates) and sophisticated capital operations.

This has not only revitalized long-term confidence in the capital markets toward “essential” medical services, but may also accelerate industry consolidation. RP, with its ample cash reserves, is well-positioned to proactively acquire small and mid-sized imaging centers, while highly leveraged peers face mounting pressure, signaling a further increase in industry concentration.

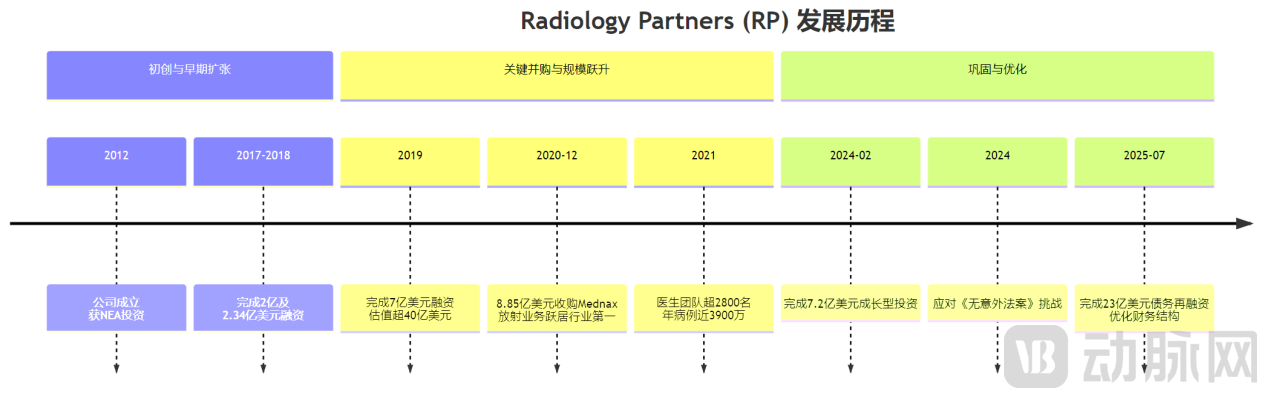

The growth trajectory of RP serves as a classic case study of rapid expansion in the healthcare services sector through capital infusion and mergers and acquisitions.

Key Milestones in the Development of RP

In 2012, Rich Whitney, former Chief Financial Officer of DaVita, the second-largest dialysis service provider in the United States, founded RP in California. From its inception, the company established an integration model centered on “co-ownership,” rapidly building a nationwide service network by acquiring local radiology practices and inviting physicians to become shareholders.

During this phase, New Enterprise Associates (NEA) became the core capital backer of RP, providing critical funding for its early expansion. In May 2017, RP completed a $200 million financing round. In March 2018, RP secured an additional $234 million in equity financing, with Australia’s sovereign wealth fund, Future Fund, joining as a new investor. This development marked cross-regional capital recognition of RP’s business model. By the end of 2018, RP had preliminarily established a multi-state service network, laying the foundation for subsequent large-scale expansion.

2019 marked a watershed moment for RP’s development, with substantial financing and landmark mergers and acquisitions propelling it to the top position in the industry. RP completed a $700 million strategic financing round exclusively invested by Starr Investment Holdings, a century-old insurance giant, which pushed the company’s valuation beyond $4 billion. At that time, RP had approximately 1,400 radiologists, with its service network covering all states across the U.S., providing support to over 1,000 hospitals and outpatient centers.

Following the closing of its financing, RP immediately launched a landmark industry acquisition. In December 2020, RP acquired the radiology specialty business of Mednax (now known as Pediatrix) for $885 million. This merger not only propelled a significant expansion in RP’s physician team and coverage scale but also established it as the largest third-party provider of radiology services in the United States.

Following the acquisition, RP’s business scale expanded significantly: total revenue for 2021 was projected to reach $1.9 billion. As of July 2021, the company had more than 2,800 radiologists, with operations in 33 states, serving over 3,400 healthcare facilities and 140 medical imaging centers across all 50 U.S. states, and interpreting approximately 39 million cases annually, thereby firmly consolidating its position as an industry leader.

After 2022, RP gradually shifted its focus to internal integration and financial health management. In response to the industry challenges posed by the implementation of the U.S. No Surprises Act, the company actively addressed cash flow pressures by optimizing contract negotiation and arbitration strategies.

In February 2024, RP secured $720 million in growth equity investment, bringing its cumulative fundraising to over $1.8 billion and placing it among the top-funded companies in the health technology sector. In July 2025, the company further completed a $2.3 billion debt refinancing, significantly extending debt maturities and reducing capital costs, marking RP’s entry into a new development phase centered on robust operations and profit enhancement.

As of 2025, RP has over 3,900 radiologists serving 3,260 hospitals and outpatient facilities across the United States. Building on an optimized financial structure, the company continues to increase its investment in technological innovation, collaborating with generative AI firm RADPAIR to develop intelligent diagnostic tools, and further solidifying its industry leadership through strategic mergers and acquisitions. Currently valued at approximately RMB 24 billion, RP has become an industry benchmark combining economies of scale with technological barriers.

Overview of RP's Fundraising History

The key to RP becoming the largest radiology service provider in the United States lies in its successful integration of technology, talent, and scaled operations into a robust network, ultimately precisely enhancing physicians’ capabilities and clinical value.

RP Core Technology Advantages Framework

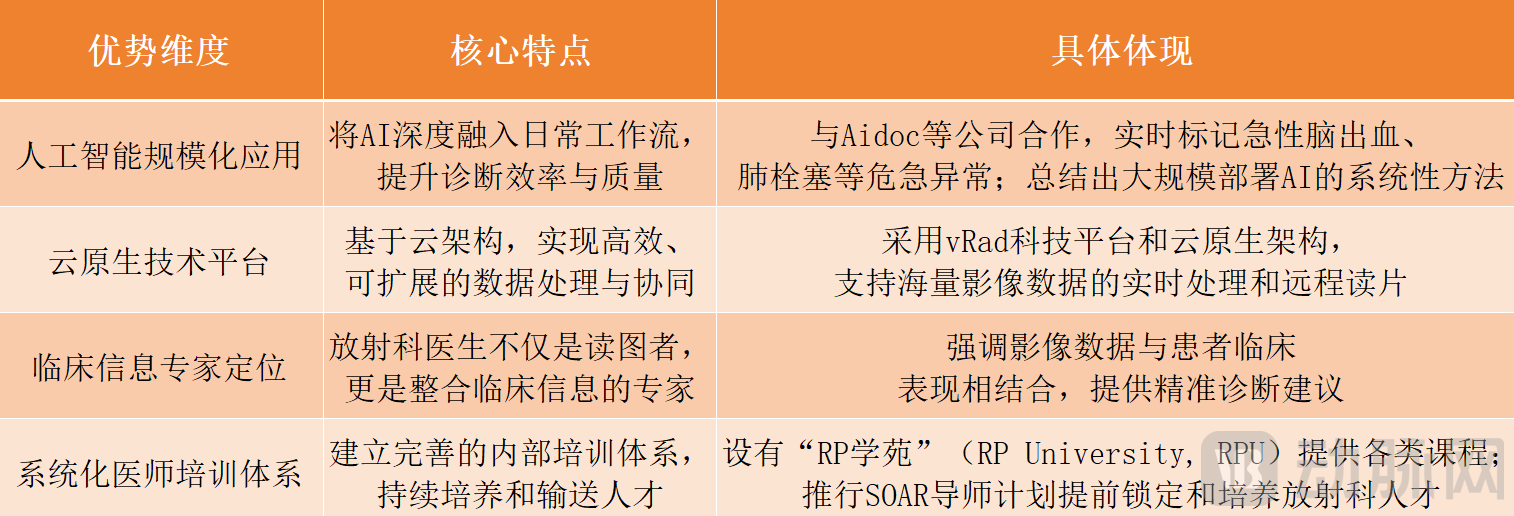

● AI-Driven, Enhancing Diagnostic Efficiency and Accuracy

RP recognized early on that the value of AI lies in assisting rather than replacing physicians, and has therefore actively integrated AI technologies into its daily diagnostic workflows. By partnering with AI medical imaging companies such as Aidoc, RP employs algorithms to instantly flag critical abnormalities, including acute intracranial hemorrhage and pulmonary embolism. This approach not only enhances diagnostic sensitivity but also reduces report turnaround time (TAT) by at least 30%. Currently, this solution is adopted by more than 500 medical centers worldwide, helping RP improve healthcare quality and patient satisfaction.

At the practical level, RP has accumulated valuable experience in large-scale AI deployment. Dr. Nina Kottler of the company has shared key insights: AI applications not only enhance radiologists’ efficiency in handling negative studies but can also lead to unexpected findings. For instance, algorithms designed to detect rib fractures may simultaneously flag pneumothorax or identify bone metastases, demonstrating the complementary advantages of human-AI collaboration.

● Cloud-native architecture support, enabling data transfer in seconds

To support its extensive network of physicians and massive volume of imaging data, RP has adopted the vRad technology platform. Built on a cloud-native architecture, this platform integrates Picture Archiving and Communication Systems (PACS) with workflow solutions and incorporates medical AI technologies. It enables efficient data management and real-time processing, facilitating clinical and telemedicine applications while ensuring service reliability and scalability.

Meanwhile, RP has established a dedicated IT department to provide 24/7 medical equipment repair, system maintenance, and consulting services for AI system implementation. RP believes that cloud-native platforms, capable of dynamically allocating resources based on demand, are the key infrastructure supporting the large-scale acquisition and real-time processing of unstructured radiology data.

● SOAR Program + RP Academy: Building a Pipeline of Clinical Information Experts

RP emphasizes that radiologists are not merely interpreters of images, but experts who integrate clinical information, dedicated to providing more in-depth diagnostic recommendations.

To ensure the sustained advantage of its talent pool, RP has established a systematic training framework. In response to the current shortage of radiologists, RP launched the SOAR Mentorship Program. This program provides one-on-one mentoring for fourth-year radiology residents (R4) and facilitates their placement at RP-affiliated medical institutions upon completion, thereby proactively cultivating a pipeline of future radiologists.

Meanwhile, “RP University” (RPU) offers a range of courses spanning from executive leadership and management to clinical education and training, fostering the continuous enhancement of the team’s professional capabilities. In addition, RP has established the RP Research Center, which encourages academic exchange and innovation among its affiliated physicians through activities such as hosting academic symposia and recruiting cross-specialty research projects, thereby driving the overall improvement of the team’s professional standards.

In summary, the core technical advantages of RP form an organic whole. It lies not merely in the acquisition of AI software or the establishment of a specific platform, but rather in its capacity to systematically integrate technological innovation with clinical practice, talent development, and scaled operations. This model positions RP not only as a healthcare service provider but also as a clinical ecosystem platform capable of continuous learning, adaptation, and leadership in driving industry transformation.

RP’s core business model can be summarized as “alliance and empowerment,” which significantly differentiates it from traditional healthcare service providers and constitutes its central appeal to investors.

Doctor Alliance: Anchoring Core Talent Through Equity Acquisition to Fortify the Foundation of Service QualityWhen acquiring local radiology practices, RP aligns the personal interests of practice physicians with corporate growth by making them company shareholders. This mechanism not only ensures clinical service quality and team stability but also successfully attracts a large number of high-quality physicians and practices, building a stable nationwide physician network across the United States.

Headquarters Empowerment: Handling Non-Clinical Administrative Tasks to Allow Physicians to Focus Solely on Patient Care.RP headquarters provides comprehensive middle- and back-office support to its affiliated clinics and physicians, covering non-clinical operations such as insurance reimbursement coordination, contract negotiations, IT system maintenance, and financial compliance. This model allows physicians to focus exclusively on clinical care without being distracted by administrative tasks, significantly enhancing operational efficiency and service quality.

Network effects, achieved through a network of 3,900 physicians covering all 50 states, create dual barriers in both cost and service.RP’s extensive service network delivers a dual advantage: on one hand, economies of scale and bargaining power reduce costs for equipment and consumables; on the other, its cross-regional resource allocation capability enables rapid response to diagnostic and treatment demands across different regions and time periods, creating a service flexibility that competitors find difficult to replicate.

This business model has not only ensured RP’s service quality and operational efficiency, but also made it a favorite in the capital markets, with cumulative financing exceeding $1.8 billion. Despite being impacted by the No Surprises Act, the successful refinancing of $2.3 billion in debt further validated the resilience of its business model.

The healthcare services industry has always operated within the dual gravitational fields of policy and market forces. Since 2022, the U.S. healthcare sector has faced simultaneous challenges from the macroeconomic environment and industry regulation, providing a representative case for observing the industry’s resilience.

Industry Stress Test Under Policy Changes

At the macro level, the Federal Reserve’s sustained interest rate hikes to curb inflation have significantly increased corporate financing costs, triggering a wave of corporate debt crises and bankruptcies, including in the healthcare sector. A more direct impact stems from the implementation of the No Surprises Act, which aims to protect patients from “surprise medical bills” but has profoundly reshaped the payment ecosystem for healthcare services.

Following the implementation of the legislation, conflicts between payers (insurance companies) and healthcare providers have become increasingly pronounced. Healthcare institutions generally believe that this effectively shifts costs onto service providers, as insurance reimbursement rates often fail to cover the actual costs of services rendered. This dispute has directly led to legal lawsuits filed by multiple industry organizations, including the American Hospital Association.

Against this backdrop, healthcare companies have faced a sharp increase in operational pressure. A landmark event was the 2023 bankruptcy filing by Envision Healthcare, a major U.S. healthcare services provider, partly attributable to cash flow pressures stemming from the Act. As an industry leader, Radiology Partners (RP) has also been significantly affected. Its legal disputes with major insurers such as UnitedHealthcare center on reimbursement for out-of-network services, involving substantial sums.

Against this backdrop, RP achieved financial structure optimization through successful debt refinancing, which not only alleviated its own pressures but also demonstrated the resilience of its business model to the market. This case provides an important reference for the survival and development of the entire industry in a complex regulatory environment.

Implications for China’s Healthcare Services

For insights into China’s healthcare services, the strategic interplay between Radiology Partners (RP) and the No Surprises Act holds particular practical reference value.

China’s healthcare industry has always operated in an environment of intensive policy adjustments. Currently, China’s healthcare reform is being systematically advanced along three main lines: “strengthening primary care, controlling costs, and promoting innovation.”Healthcare Infrastructure Strengthening ProjectFocus on enhancing county-level medical service capacity and promoting the downward allocation of resources;DRG/DIP Payment Reformand normalized, refinedCentralized Procurement of Drugs and Medical Consumables, profoundly reshaping the revenue models and cost structures of healthcare institutions; meanwhile, policies explicitly encourage digital transformation, represented by AI empowerment, regarding it as key to enhancing the quality and efficiency of the healthcare system.

Against this specific policy backdrop, RP’s experience can be translated into several concrete and actionable strategic implications.

RP’s “acquisition and equity participation” model offers valuable insights for China’s ongoing promotion of multi-site physician practice and the development of medical consortiums. Tertiary hospitals can provide expertise, technical support, and management assistance to establish a community of shared interests with primary-care physicians, thereby effectively aligning with the policy directive to “strengthen primary care.”

At the operational level, Radiology Partners’ (RP) experience in scaling AI-assisted diagnosis offers a key lesson for Chinese healthcare institutions: under the DRG/DIP payment framework, investing in technologies that enhance diagnostic and treatment efficiency and control costs—such as AI-assisted diagnosis and clinical pathway optimization systems—is no longer optional, but a necessity for survival and competitiveness.

More critically, the RP case underscores the importance of shifting from “reactive response” to “proactive management” of policy risks. Chinese healthcare institutions should establish specialized policy research teams to gain a deep understanding of policy intentions, actively participate in processes such as public consultations on policy drafts and pilot programs, articulate industry concerns through compliant channels, and internalize external policy variables into their own strategic management capabilities.

The case of RP demonstrates that during periods of intensive policy adjustment, the long-term development of healthcare institutions depends on building systemic advantages. For healthcare providers in China, the core capability to achieve sustainable growth and truly navigate economic cycles lies in transforming into a modern healthcare service platform centered on physician value, supported by technological platforms, and grounded in sound financial management.