XOMA Royalty Files Prospectus: Transforming Biotech Failures into Cash Flow Through Pipeline Acquisitions and Royalty Monetization

XOMA Royalty

--

Acquire pipelines, bet on projects, and cash in on milestones—turning others’ “failed drugs” into your own “cash cows.”

XOMA Royalty, a company with just 29 employees, completed six acquisitions in the first half of 2025, generating $2 million in annual revenue per employee—far exceeding the industry average. Unlike traditional pharmaceutical companies that focus heavily on R&D, it operates more like a “pawnshop,” accepting biotech firms’ most valuable assets (future revenue rights from drug pipelines) as “collateral” in exchange for immediate cash relief.

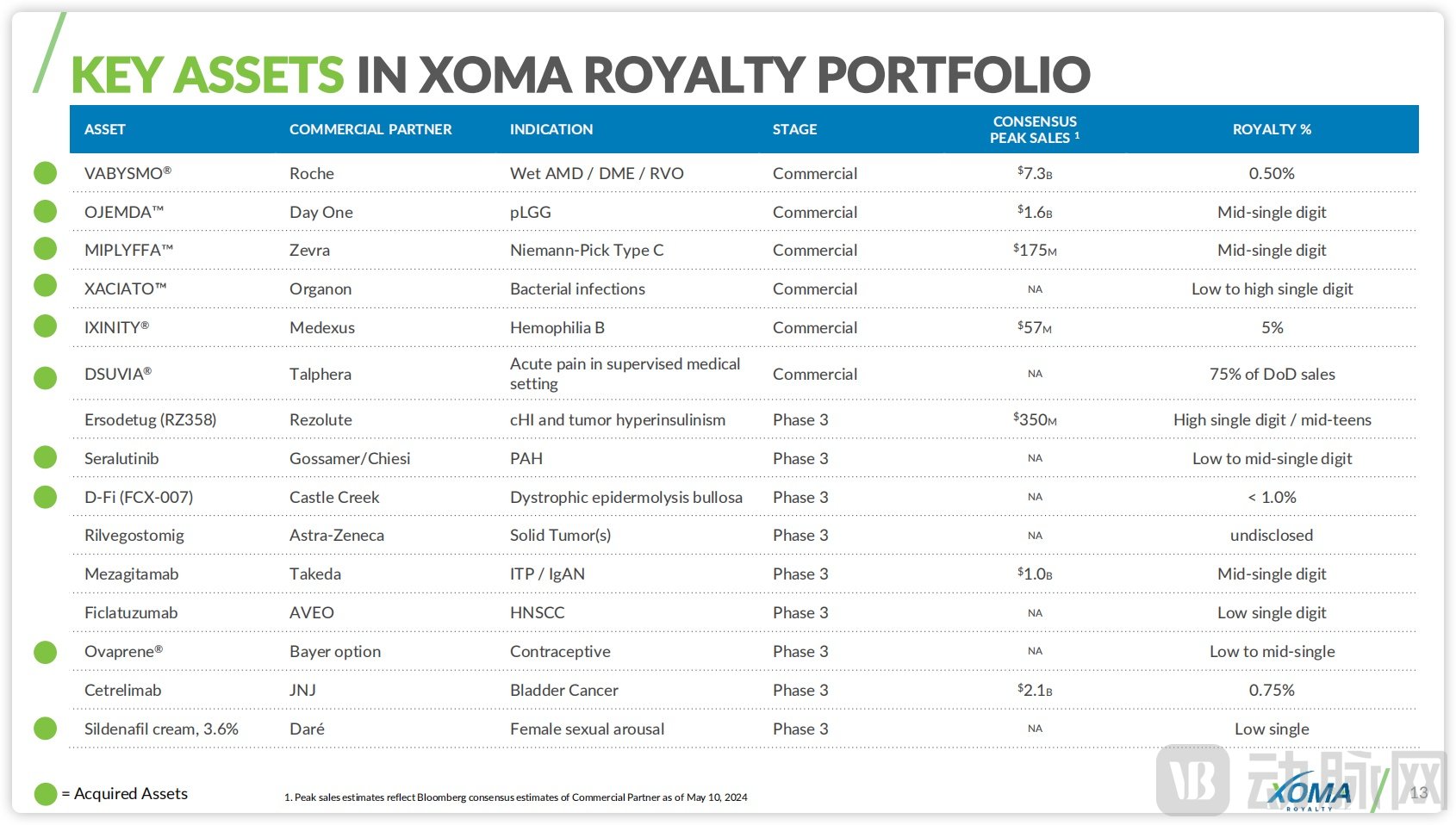

XOMA’s Core Assets, Image Source: Corporate Website

From 2021 to the present, XOMA’s R&D expense ratio has dropped from 15% to 0% in 2024, completely eliminating in-house research and development in favor of acquiring off-the-shelf pipelines. Yet its revenue has quintupled, and net profit has increased tenfold, achieving a compound annual cash growth rate exceeding 30% by leveraging “clinical trials paid for by others.” In doing so, it has forcefully transformed the biotech industry’s traditional “cash-burn” model into a “rent-collecting” cash flow stream. How exactly did it accomplish this?

A single R&D risk has given rise to a new Biotech development model.

XOMA Royalty traces its history back to 1981. Like most biotech companies, it once engaged in high-risk drug development. The turning point came in 2015, when disappointing clinical results from its core pipeline made a strategic transformation imperative. In response, XOMA sold off physical assets, including R&D equipment and manufacturing facilities, and significantly reduced operating expenses.

By 2017, XOMA had finally solidified its new strategic direction: centering on the acquisition and integration of pipeline intellectual property, licensing pipeline assets to multinational corporations (MNCs) or biotech companies, and securing future potential milestone-based economic rights, thereby building a portfolio characterized by low R&D risk and stable cash flows.

In simple terms, XOMA leverages its decades of expertise in drug development to evaluate pipeline assets, acquiring rights to future milestone payments and sales royalties for drugs in clinical stages or already on the market. By making a one-time cash payment, XOMA secures the future cash flows generated by these assets, while the selling biotech company can either obtain non-dilutive financing and continue advancing the project or choose to cease operations and recoup part of its costs.

As of the first half of 2025, XOMA has amassed a portfolio of over 120 pipeline assets, spanning oncology, autoimmune diseases, and rare disorders. Due to near-bankruptcy in its early stages caused by R&D challenges, XOMA has adopted a new business model in which it does not conduct internal R&D or assume the risk of clinical failure. Instead, it mitigates uncertainty by selecting mid-stage clinical projects that have already secured collaboration agreements with major pharmaceutical companies.

XOMA Management Team, Image Source: Corporate Website

The distinctiveness of XOMA is also evident in the composition of its core management team. For instance, current CEO Owen Hughes previously spent 16 years on Wall Street, primarily engaged in investment activities. Although he has served as CEO of several biotech companies, his primary focus and leadership during those tenures centered on driving mergers and acquisitions between these enterprises and multinational corporations (MNCs).

Similarly, the resumes of Chief Financial Officer Thomas Burns and Chief Investment Officer Bradley Sitko feature extensive experience in intellectual property, financing, restructuring, and mergers and acquisitions. It is evident that XOMA’s core management team does not possess the deep medical backgrounds typical of a biotech company; instead, their profiles are more heavily weighted toward finance, which indirectly reflects the distinctiveness of its business model.

1 year, net profit of $150 million, ROI exceeding 120%.

In February 2024, XOMA announced the acquisition of oncology drug developer Kinnate Biopharma for a total consideration of approximately $118 million, at a price of $2.3352 per share. The transaction covers all five of Kinnate’s investigational pipelines, which target multiple oncology indications and mechanisms. The lead asset is KIN-2787, which has received Fast Track designation from the U.S. FDA for the treatment of patients with Stage IIb to IV malignant melanoma harboring BRAF Class II or III alterations and/or NRAS mutations.

In addition, XOMA acquired Kinnate’s remaining cash reserves, contractual rights from previously executed agreements, and all intellectual property. To facilitate the smooth closure of the transaction, XOMA specifically structured a Contingent Value Right (CVR) arrangement, allowing Kinnate’s original shareholders to participate in a portion of the proceeds from future asset sales. Thanks to this structure, the acquisition was rapidly completed in April 2024.

In April 2025, XOMA announced the bundled sale of all five assets acquired from Kinnate for $270 million. XOMA is also eligible to receive future sales royalties ranging from low single digits to mid-teens percentages; under the CVR structure, Kinnate shareholders will also receive a portion of the proceeds, with the benefit period extending until April 2029.

In other words, after acquiring five pipelines at a relatively low cost, XOMA did not continue to inject capital for their development. Instead, one year later, it realized a $150 million profit through buying low and selling high, while retaining the right to ongoing sales royalties for the next five years.

An analysis of this transaction reveals the distinctiveness of XOMA’s strategy.

At the time, Kinnate Biopharma, as the seller, had several pipelines whose progress was less than satisfactory, and it also faced significant difficulties in securing financing. Meanwhile, delays in R&D progress weighed on its stock price, causing its market value to fall below its book value and posing substantial operational risks. Although the project held certain potential, large pharmaceutical companies were reluctant to assume such risks. However, Kinnate’s shareholders had a strong desire to exit and cut their losses. XOMA emerged as one of the few buyers in the market willing to proceed with the deal, and it structured the transaction in three steps.

First, accurately identify targets with "negative value."

For XOMA’s “buy low, sell high” strategy to succeed, it must identify companies whose market capitalization is lower than their cash reserves while still possessing tradable assets. At the time, Kinnate had announced a 70% workforce reduction in late 2023 to cut operating expenses due to slow R&D progress, leading to a continuous decline in its stock price. This layoff involved shutting down Kinnate’s R&D units worldwide, including its wholly-owned subsidiary in China, and suspending the advancement of most products in its pipeline. In other words, Kinnate became a typical target: one with cash on hand exceeding its market cap, and an early-stage yet highly promising pipeline.

Next is to design a “win-win” transaction structure.

For XOMA to profit from the transaction, rapid closing was a prerequisite. To facilitate deal completion, XOMA structured a Contingent Value Right (CVR) arrangement, allowing original shareholders to retain a portion of future upside, thereby reducing resistance to the transaction. Meanwhile, by combining cash with future earnings distributions, XOMA lowered the total transaction value and avoided a large one-time cash outlay. As a result, the entire transaction was closed in less than two months, significantly reducing uncertainty.

Finally, there are highly liquid assets.

Less than a year after the acquisition, XOMA bundled and sold off all its assets. This move strongly demonstrates its commercialization capabilities. The transaction agreement also reflects XOMA’s sophistication: for instance, it established tiered royalty rates based on sales volumes, agreeing to reduce certain milestone payments in exchange; alternatively, it adjusted payment schedules to save the buyer tens of millions of dollars, thereby securing higher profits for itself.

On the surface, XOMA employs a combined strategy of buying low and selling high, asset-light operations, and short-cycle transactions. In essence, however, it productizes its specialized capabilities in asset valuation, cash flow management, legal affairs, and taxation to precisely capitalize on biotech companies struggling during the capital winter.

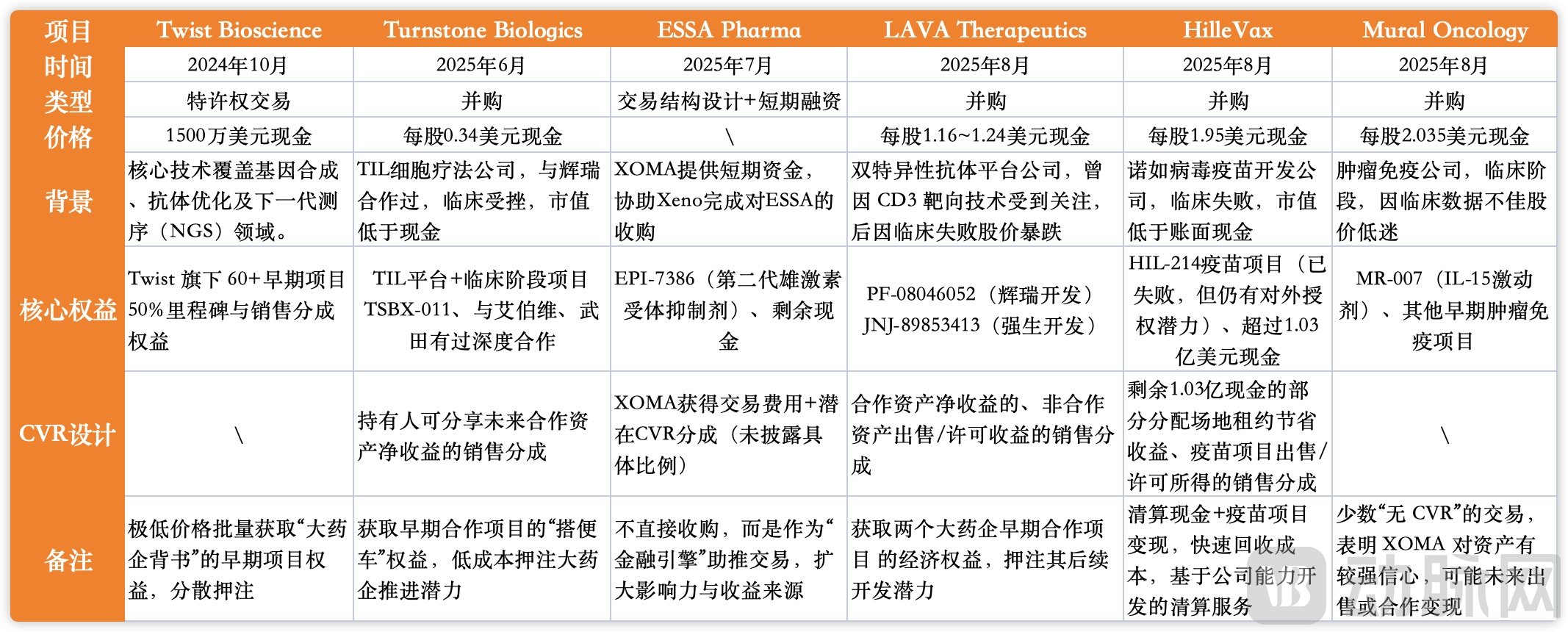

XOMA Accelerated Its Acquisition Pace in 2025.

From June 2025 to September 2025, XOMA executed five transactions within a mere three months. When combined with one additional transaction in late 2024, XOMA has fully leveraged and refined its business model.

Selected XOMA Transactions Over the Past Year, Compiled from Public Information

Based on these recent transactions, the deal types include liquidation-style (HilleVax), early-stage platform-building (LAVA and Turnstone), royalty wholesale-style (Twist), structured finance-style (ESSA Pharma), and pure asset acquisition-style (Mural). Meanwhile, tools such as Contingent Value Rights (CVRs), payment schedules, and additional clauses are employed to design transaction structures that align with the interests of both parties.

Take the acquisition of Turnstone Biologics as an example. Turnstone was no obscure player; it had already entered into a deep collaboration with AbbVie in 2017, whereby AbbVie secured options on three of Turnstone’s oncolytic virus immunotherapies, with its candidate Ad-MG1-MAGEA3 drawing particular attention. In 2019, Turnstone further struck a licensing deal for its oncolytic candidates with Takeda Pharmaceutical Company, valued at nearly $1 billion.

However, by February 2025, Turnstone issued a statement announcing the termination of development for its clinical-stage candidate drug TIDAL-01. This decision stemmed from the need for continuous process improvements in the manufacturing of TIL therapy, which would require substantial investment. In light of future funding requirements and the financing environment, Turnstone was compelled to make this decision. Meanwhile, Turnstone’s Board of Directors is also exploring options to maximize shareholder value.

XOMA chose to act at this juncture, leveraging a Contingent Value Right (CVR) structure to secure rapid board approval from Turnstone and acquire the company for a total consideration of less than $8 million. Although its core pipeline is currently stalled due to cost constraints, it retains significant transactional potential and benefits from endorsement by multinational corporations (MNCs). This underpins XOMA’s willingness to make a low-cost strategic bet.

The transaction with Twist Bioscience demonstrates another aspect of XOMA’s “cunning” strategy. In this deal, valued at a total of $15 million, XOMA did not acquire any substantial product pipeline or services from Twist. Instead, it purchased the right to receive 50% of the milestone payments and sales-based royalties generated from existing collaborations between Twist’s antibody discovery platform and other pharmaceutical companies. XOMA is not entitled to upfront payments or other forms of income, and revenues from future new partnerships will remain solely with Twist.

Several aspects of this transaction are noteworthy. As early as its 2024 financial report, Twist Bioscience recorded an asset impairment charge of over $44 million for its antibody discovery division and achieved year-over-year revenue growth through expense control, while also stating that it would not abandon its antibody discovery platform. XOMA’s $15 million investment enabled Twist to recoup funds in advance, thereby strengthening its financial position. In return, XOMA acquired 50% of the future milestone and royalty rights from more than 60 early-stage projects in Twist’s existing portfolio, which involves collaborations with dozens of enterprise partners (at just $250,000 per project). This low-risk investment has enhanced XOMA’s capital deployment capabilities.

Overall, XOMA’s business model offers distinct advantages while carrying certain risks. By holding rights to a diverse portfolio of drug candidates across various stages and therapeutic areas, XOMA mitigates the risk associated with the failure of any single drug development program. Meanwhile, its counter-cyclical strategy enables the company to acquire promising pipelines at lower valuations, and its asset-light operating model allows it to avoid directly bearing the high costs and risks inherent in R&D.

On the other hand, XOMA’s revenue is entirely dependent on the R&D and commercialization capabilities of its partner pharmaceutical companies, while the value of its assets ultimately hinges on which drugs successfully reach the market and become “blockbusters,” introducing a degree of uncertainty. Particularly before a significant number of drugs gain regulatory approval, cash flow may be unstable, necessitating continuous financing to acquire new royalty interests.

XOMA Royalty resembles a “special asset disposal expert” and a “packaged investor in future revenue rights” within the biopharmaceutical sector. It does not pursue scientific “glamour,” but instead carves out its own profit margins amidst the industry’s high risks and uncertainties through shrewd financial engineering and risk control.

The financial data for the first half of 2025 undoubtedly affirms XOMA’s development model.

In H1 2025, XOMA’s total revenue reached approximately $29.6 million, representing a year-over-year increase of over 130%. Of this amount, $16 million was derived from commercialization-related sales royalties, while $13.6 million came from milestone payments. Meanwhile, XOMA’s R&D expenses totaled $1.4 million, with only $100,000 incurred in Q1 2025; the rise in expenses in Q2 was attributed to the management of acquired projects. Overall, these results align with its asset-light operational strategy.

XOMA stated that although milestone payments remain the primary revenue driver, commercial royalty income has increased quarter-over-quarter for two consecutive quarters. As more projects in its “pipeline pool” advance to the commercialization stage, royalty payments from sales are expected to continue rising in the second half of 2025, clarifying a path toward break-even even without milestone payments. Going forward, milestone payments will be used to cover acquisition costs, while commercial royalty income will become the company’s main source of profit.

Overall, XOMA aims to achieve a high degree of risk diversification by assembling a “patent licensing pool” comprising assets at various development stages, across different therapeutic areas, with diverse mechanisms of action, and from multiple licensors. Meanwhile, leveraging its professional expertise in legal affairs, deal structuring, buyer networks, valuation adjustment mechanisms (VAMs), compliance management, and patent continuity, the company has expanded into liquidation services. This enables it to provide rapid wind-down solutions for distressed biotech firms, thereby maximizing shareholder value while generating service-related revenue.

XOMA’s business model is also worth studying for China’s biotech industry. First, it has shifted from a “blockbuster bet” strategy to a “cash flow portfolio.” With XOMA’s patent reserve covering more than 120 pipeline assets, the failure of any single project would impact overall cash flow by less than 2%. Second, it facilitates the mutual conversion between “future milestones” and “current cash”; XOMA not only purchases future royalty rights but also sells them off in one-time transactions. Finally, transitioning from scientists to capital operators, a significant proportion of XOMA’s small workforce consists of legal, financial, and tax professionals.

No matter how you look at it, XOMA is an atypical biotech company. The insight it offers is not about how to develop a drug, but rather how to commercialize the various capabilities honed during corporate development. As financing windows narrow and valuations fall broadly below cash reserves, those who first learn to leverage these capabilities will have the opportunity to turn the capital winter into dividends from cyclical fluctuations. There are already several companies similar to XOMA in the U.S. market; when will such enterprises emerge in China?