Sarepta Therapeutics: Navigating Multi-Platform Innovation Amid Strategic Restructuring and Global Collaboration with Roche

Sarepta

Developer of Therapies for Rare Neuromuscular Diseases

Recently, Sarepta Therapeutics, a leading U.S. company in small nucleic acid therapeutics, offloaded its equity stake in Arrowhead Pharmaceuticals for $174 million. This move has drawn industry attention and is viewed as a strategic adjustment in its dual-track layout of RNA and gene therapies.

This transaction is not only a significant strategic divestiture case in the field of nucleic acid therapeutics this year, but also exposes the hidden predicament of this pharmaceutical company with a market capitalization exceeding $10 billion—Amid the Elevidys hepatotoxicity controversy and pressure from convertible bonds maturing in 2027 (including the $1 billion bond issued in 2022 and subsequent refinancing adjustments), Sarepta is adopting a “cutting off the arm to save the body” strategy to buy breathing room for its triple technology portfolio spanning RNA, AAV, and siRNA.

Previously, Sarepta faced significant turbulence. Patient deaths occurred in some clinical trials of its product Elevidys, prompting the FDA to restrict the eligible patient population and plunging Sarepta into a storm of public controversy. It was not until July this year that the FDA announced the reinstatement of certain uses for Elevidys.

From an industry perspective, nucleic acid and gene therapies stand at the intersection of hope and risk. According to Grand View Research, the market was valued at approximately $5.5 billion in 2023 and is projected to exceed $18 billion by 2030. Whether through RNA-mediated modulation of gene expression or adeno-associated virus (AAV)-based delivery of functional genes, these innovative therapies aim to intervene in diseases at their root causes, making cures increasingly attainable. However, this bridge connecting patients to health continues to face severe challenges, leaving practitioners and patients on an emotional rollercoaster marked by periods of stability interspersed with turbulence.

From an Obscure Player in a Niche Field to a Leader in Oligonucleotide Therapeutics: A 45-Year Leap

Sarepta’s story dates back to 1980, when the company was known as AntiVirals Inc. (AVI). In the early 21st century, it focused on RNA-based therapeutics (antisense oligonucleotide therapy), dedicating itself to a field that was not yet mainstream at the time.

Renamed Sarepta Therapeutics in 2012, the company marked a strategic shift toward rare diseases, thereby embarking on an innovative journey in small nucleic acid therapeutics. Since then, Sarepta has gradually grown into a representative U.S. enterprise in small nucleic acid therapy and established a leading position in the treatment of Duchenne Muscular Dystrophy (DMD).

To date, Sarepta has successfully developed and commercialized four drugs for the treatment of DMD.: Exondys 51 (eteplirsen), Vyondys 53 (golodirsen), Amondys 45 (casimersen), and Elevidys (delandistrogene moxeparvovec).

Among them, the first three therapies based on RNA exon-skipping technology were approved by the U.S. Food and Drug Administration (FDA) in 2016, 2019, and 2021, respectively, for DMD patients amenable to exon 51, exon 53, and exon 45 skipping; Elevidys received conditional FDA approval in 2023, becoming the first gene therapy for the treatment of ambulatory children aged 4–5 years with DMD.

Sarepta’s transformation has been driven by key leadership. Doug Ingram, who has served as CEO since 2017, previously worked at Allergan, a pharmaceutical company renowned for its medical aesthetics and neuroscience products. He brought a dual market- and clinical-oriented philosophy to Sarepta, steering the company’s strategy to align more closely with clinical needs.

Figure 1: CEO Doug Ingram

Meanwhile,Sarepta maintains its R&D investment through secondary market financing and strategic collaborations.In December 2019, Roche and Sarepta entered into a $2.85 billion collaboration to jointly develop Elevidys. Roche obtained the commercialization rights for Elevidys in regions outside the United States, while Sarepta was responsible for clinical development and manufacturing.

Table 1: Overview of Sarepta Therapeutics’ Financing and Investment (2010–2025)

Sarepta was listed on the NASDAQ in the late 1990s (stock ticker: SRPT). In 2024, Sarepta generated approximately $1.9 billion in revenue, representing a year-over-year increase of more than 50%. This growth was primarily driven by the commercial scale-up of multiple core marketed drugs. While RNA therapies remained the primary source of revenue, gene therapy is rapidly emerging as a new pillar of the business.

Today, Sarepta secures the “immediate returns” from RNA therapeutics while strategically positioning itself in frontier innovative assets such as gene therapy and siRNA, demonstrating unique endurance in balancing present gains with future growth.

Triple-Pronged Layout: Exon-Skipping Therapies, siRNA Platforms, and Gene Therapy

Unlike many biopharmaceutical companies that opt for a single technology,Sarepta adopts a multi-platform parallel strategy: leveraging RNA exon-skipping therapies as an early revenue source, making substantial investments in gene therapy, and expanding into siRNA through collaborations with biotech firms to amplify its competitive advantage in the oligonucleotide therapeutics sector.This structure provides Sarepta with a relatively robust balance in the high-risk R&D landscape of rare diseases.

1Editor's Pick: RNA Exon Skipping Therapy

RNA Exon Skipping Therapy is a type of antisense oligonucleotide (ASO) therapy. Its mechanism of action involves modulating gene splicing to enable cells to skip mutated exons, thereby producing partially functional proteins. This process is akin to skillfully bypassing erroneous chapters in the genetic codebook, allowing normal coding to proceed.

Sarepta has a portfolio of flagship products in this field. Its approved drugs, EXONDYS 51, VYONDYS 53, and AMONDYS 45, target different mutation types in patients with Duchenne muscular dystrophy (DMD). By modulating precursor messenger RNA (pre-mRNA), these therapies facilitate partial restoration of the reading frame of the dystrophin gene, thereby improving muscle function in patients. The application of these products has benefited thousands of patients to date, establishing a stable market presence.

2Silent Guardian: siRNA Platform

Within the technological spectrum of RNA therapeutics, small interfering RNA (siRNA) represents a class of double-stranded RNA molecules capable of precisely “silencing” target gene expression through the RNA interference (RNAi) mechanism. Unlike antisense oligonucleotides (ASOs), which block mRNA translation, siRNAs enter the intracellular RNA-induced silencing complex (RISC) and directly guide this complex to recognize and cleave aberrant mRNA, thereby inhibiting the synthesis of pathogenic proteins. This mechanism offers higher specificity and a longer duration of action, demonstrating significant potential in the treatment of neurological, metabolic, and rare genetic disorders.

Based on this, Sarepta has entered the field of siRNA technology development through a strategic collaboration with Arrowhead Pharmaceuticals, enabling precise silencing of abnormal gene expression and expanding intervention pathways beyond antisense oligonucleotides (ASOs). Sarepta has currently established a pipeline of multiple early-clinical or preclinical projects, including those for facioscapulohumeral muscular dystrophy (FSHD; SRP-1001), myotonic dystrophy type 1 (DM1; SRP-1003), spinocerebellar ataxia type 2 (SCA2; SRP-1004), and idiopathic pulmonary fibrosis (IPF; SRP-1002), covering the neurological and metabolic disease sectors to reserve a broader range of indications for the future.

3Gene Delivery Vehicle: AAV Gene Therapy

Elevidys (delandistrogene moxeparvovec) is Sarepta’s flagship product in the field of gene therapy (AAV vectors). Acting as a specialized gene delivery vehicle, it uses adeno-associated virus (AAV) to precisely deliver the micro-dystrophin gene into patients’ muscle cells, enabling these cells to resume production of the critical protein and thereby addressing the underlying pathology of Duchenne muscular dystrophy (DMD) at its source.

As the first FDA-approved gene therapy for Duchenne muscular dystrophy (DMD), Elevidys marks the true realization of gene therapy in the treatment of rare diseases. Clinical data indicate that Elevidys can improve motor function metrics (NSAA scores) in ambulatory patients; however, serious adverse events have been observed in some non-ambulatory patients, and its long-term efficacy and safety still require ongoing validation.

4Future Exploration: Gene Editing

In the more cutting-edge field of gene editing, Sarepta is pursuing a Duchenne muscular dystrophy program based on CRISPR/Cas9, which remains in the preclinical stage. Although this exploration is still in its early phases, it demonstrates that the company is not content with its existing platforms and strives to remain at the technological forefront of nucleic acid therapeutics.

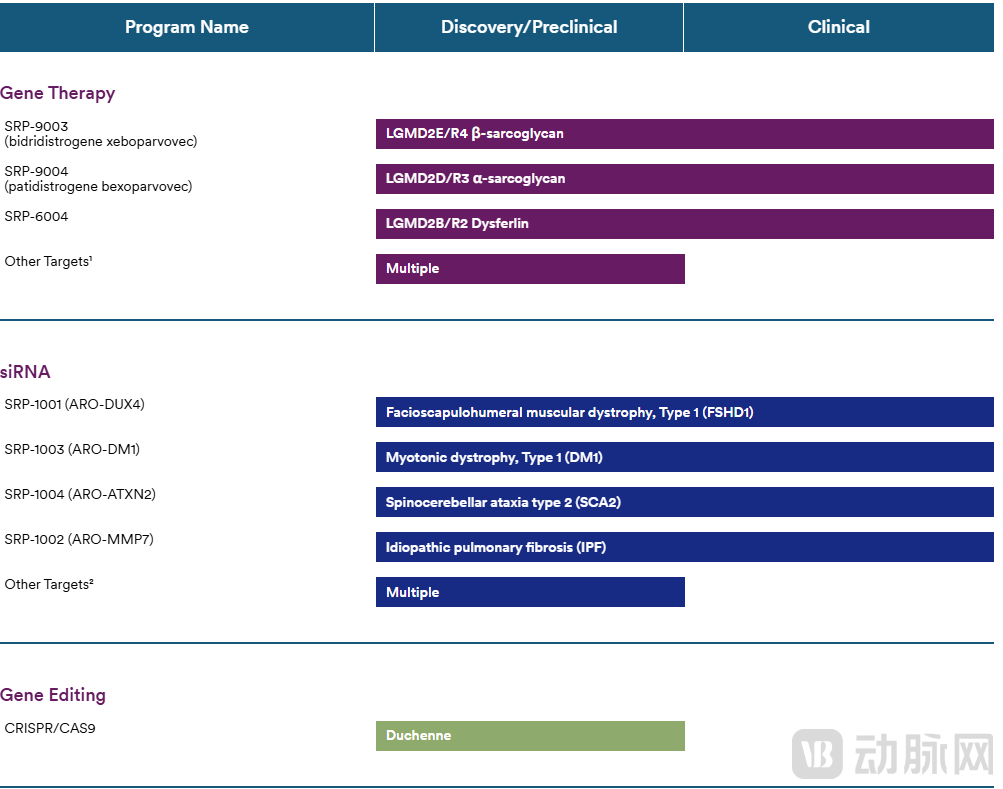

Overall,Sarepta currently has more than 40 R&D projects at various stages, covering three major technological platforms—RNA therapeutics, AAV gene therapy, and gene editing—as well as multiple therapeutic areas including neuromuscular disorders, the central nervous system, and cardiology., forming a panoramic layout that spans from cash flow support to innovation breakthroughs and long-term development.

Figure 2: Overview of Sarepta’s Pipeline Progress

From Corporate Narrative to Industry Microcosm: The Promise and Challenges of Gene Therapy

If the development of AAV gene therapy were plotted on a timeline, it would not be a smooth upward curve but rather a jagged line: each clinical breakthrough has been accompanied by renewed reflection on safety and accessibility.

In 2017, pharmaceutical giant Roche and its subsidiary Genentech partnered with Spark Therapeutics, a biotechnology company specializing in gene therapy, to secure the FDA’s first approval for an in vivo AAV therapy, Luxturna (AAV2, indicated for inherited retinal dystrophy caused by RPE65 mutations). This milestone marked the transition of “one-time in vivo gene delivery” from concept to reality. In 2019, Novartis’s Zolgensma (AAV9, for spinal muscular atrophy [SMA]) elevated AAV delivery to the forefront of neurological disease treatment. Subsequently, risks associated with high-dose administration—such as hepatotoxicity, immune-related reactions, and thrombotic microangiopathy (TMA) in rare cases—began to be systematically reviewed and closely monitored.

The back-and-forth between regulators and the company surrounding the approval of Elevidys and the subsequent investigation into safety incidents serves as a prism, clearly reflecting the complex industrial ecosystem in the development of AAV gene therapies.

In May 2023, after weighing the benefits of using micro-dystrophin levels as a surrogate endpoint, an external advisory panel voted 8–6 in favor of granting Elevidys accelerated approval. In June, the FDA formally granted accelerated approval to Elevidys for the treatment of ambulatory pediatric patients aged 4 to 5 years with confirmed DMD gene mutations. In August, Elevidys was launched commercially at a price of $3.2 million per dose, making it the second most expensive gene therapy product globally at the time, surpassed only by Novartis’s Zolgensma.

The therapeutic landscape of AAV has expanded from ophthalmology and neurodevelopmental disorders to the field of muscular dystrophy; these milestones are not isolated victories, but rather repeated demonstrations: The therapeutic potential of AAV is real. But so is the complex relationship between dose, immunity, and organ toxicity.

In October 2023, Sarepta’s DMD gene therapy Elevidys failed to meet the primary endpoint of NSAA in the Phase III EMBARK study (the gene therapy group showed a 2.6-point increase in NSAA score from baseline, compared with 1.9 points in the placebo group, which was not statistically significant), but it did meet the secondary endpoints. Despite the Phase III failure,Sarepta continues to submit supplemental efficacy data for its Biologics License Application (BLA) to the FDA, seeking to expand the indication for Elevidys to all patients with DMD gene mutations (covering all age groups).

The BLA approval process continued into 2025, with Sarepta becoming embroiled in a new safety dispute. Starting in late June, the FDA identified individual post-treatment death cases and initiated a review, prompting Sarepta and its international partner Roche to suspend shipments in certain markets. On July 28, the FDA recommended lifting the voluntary suspension for “ambulatory patients,” and the company announced the resumption of Elevidys supply to this patient population in the United States; however, the FDA’s risk assessment for patients with higher disease severity remains ongoing.

The underlying logic is that,“Stratified Dosing, Evidence-Based Expansion” is emerging as the new regulatory and clinical consensus for AAV therapies—prioritizing patient populations with more robust evidence of benefit, then cautiously extending to more complex patient groups under conditions that allow for monitoring and intervention.

From a financial perspective, this also reflects the balancing act required in high-risk sectors. In the second quarter of 2025, Sarepta generated $611 million in revenue, a year-on-year surge of 68%, yet this still lagged behind the growth rate of its R&D investment (R&D expenses reached $530 million in the first half of 2025). Meanwhile, Sarepta announced a layoff of 500 employees, expecting to save approximately $400 million annually, and raised $174 million in cash by selling its equity stake in Arrowhead to hedge against future milestone payments. Such moves are not short-sighted cash-outs but rather strategic maneuvers to create flexibility for addressing $1.2 billion in convertible bonds maturing in 2027.

These actions cannot be simply labeled as “conservative” or “aggressive.” Revisiting the current controversies surrounding Sarepta: safety is not a black-and-white true-or-false question, but rather a proposition that requires continuous quantification and passive/active management; the equity sale is not a matter of value judgment, but the result of the coupling between cash flow trajectories and clinical/regulatory timelines.

Sarepta chose to implement a series of deleveraging measures in 2025 and extend its technological roadmap from RNA and AAV to siRNA, precisely leveraging organizational and financial resilience to buy time for the accumulation of robust scientific evidence. In the short term, these are variables; in the long term, they are constants.

At the intersection of high risk and high value, Sarepta has answered part of the question “How can gene therapy move from science to reality?” through its own choices. Placing these two events within the long-term trajectory of AAV development reveals that they are more akin to “necessary interludes” in the maturation of this emerging technology.

What truly determines long-term value still hinges on three factors: the ability to more clearly define the dose–immunity–organ safety boundaries; the capacity to continuously accumulate sufficient evidence to support population expansion and label broadening; and the capability to mitigate commercial volatility to a controllable range through multi-platform synergy.