Domestic Oral Surgery Robots Dominate China's Market with No Imported Competitors

Yakebot

Developer and Manufacturer of Medical Robot Products

Lancet Robotics

Developer of Robotic Systems for Orthopedic Joint Replacement Surgery

As the wave of domestic substitution for high-end medical devices sweeps across various sub-sectors, the oral surgery robot industry presents a unique development pattern.

Since 2025, with the approval of dental surgical robots from Yakebot, Shenzhen Lancet Robot, and Remebot, there are currently 13 dental surgical robots (excluding standalone navigation systems) available in China, all of which are domestically produced. Chinese brands have not only achieved a monopoly in the domestic market but are also actively expanding overseas, aiming to secure a first-mover advantage in the global market.

Since 2025, China’s oral surgery robot industry has witnessed a peak in regulatory approvals, with new products from companies such as Yakebot, Shenzhen Lancet Robot, and Remebot successively receiving approval from the National Medical Products Administration (NMPA). To date, 13 oral surgery robots have been approved for market launch in China. Notably, Yakebot’s first oral surgery robot was approved as an innovative medical device in 2021, signifying that domestic products have gained regulatory recognition for their technological innovation.

Currently, the vast majority of oral surgical robots are indicated for dental implant surgery, with their primary advantages lying in high precision and minimally invasive techniques. Given the intricate and complex anatomy of the oral cavity, these robotic systems assist surgeons in achieving a clearer and more comprehensive visual field, enabling more precise positioning. They help minimize incision size, reduce pain and postoperative swelling, accelerate healing, and improve the long-term success rate of dental implants. Furthermore, they provide enhanced assistance to clinicians in performing precise implant procedures for complex cases, such as partial or complete edentulism and severe alveolar bone deficiency.

Approved Domestic Dental Surgical Robots (Excluding Single Navigation Systems), Source: National Medical Products Administration

Technical breakthroughs in domestically produced products are primarily reflected in two dimensions: first, the comprehensive localization of core components.Taking Lancet Robot as an example, its second-generation product, approved in 2025, has achieved domestic substitution of key components. This transition not only brings significant cost advantages, making the equipment more competitively priced, but also enhances supply chain controllability and the efficiency of technological iteration, laying the foundation for rapid response to market demands.

Second, functionality is expanding from single-purpose to multi-purpose.Early oral surgery robots were almost entirely focused on dental implant procedures, but as the technology has matured, leading companies have begun to break through the limitations of single indications. Yakebot’s new robot, approved in 2025, has expanded its indications to include endodontic surgeries, extraction of impacted teeth, autogenous tooth transplantation, and other fields.

Unlike the traditional landscape in other surgical robotics fields, such as laparoscopy and orthopedics, which has been characterized by “imported products gaining first-mover advantage, followed by gradual substitution with domestic alternatives,” the dental surgical robotics sector has exhibited a feature of “domestic dominance” since its inception. Currently, no imported products have entered the Chinese market.

Certainly, there are similar products in the global market, among which the most well-known is the Yomi dental surgical robot from Neocis, a U.S.-based company. It is the first and, to date, the only implant surgery robot approved by the FDA. Since its approval in 2016, the commercialization of Yomi has been primarily concentrated in the United States.

With multiple domestic products successively approved, there are currentlyMany devices have entered the commercialization phase, gradually entering the market by targeting leading public hospitals as a foothold; however, further breakthroughs are still needed in terms of both product functionality and commercialization pathways.

According to data from the China Government Procurement Network, the procurement volume of oral surgery robots has increased year by year since 2022, with transaction prices ranging from approximately RMB 1.8 million to RMB 3 million. Among them, public stomatological hospitals such as Peking University School of Stomatology, West China School of Stomatology of Sichuan University, Wuhan University School of Stomatology, and The Affiliated Stomatological Hospital of Sun Yat-sen University have introduced these products. Products from companies such as Yakebot, Remebot, and Dikai'er have achieved a high number of successful bids. Leading hospitals possess advantages in medical technology and financial strength, and can validate product application capabilities through robot-assisted treatment of complex cases; therefore, they have consistently been the key target for market expansion during the initial phase of innovative product introduction.

As one of the earliest enterprises to enter the commercialization stage, data released by Yakebot in July 2025 shows that its dental surgical robots have cumulatively completed over 10,000 clinical procedures. These products have been deployed in more than 300 public hospitals and over 50 private clinics across China.

The aforementioned data not only demonstrates the current scope of application for dental surgical robots but also, to a certain extent, reflects the differences in procurement willingness between public and private medical institutions. A review of the financial reports and other public information of numerous listed dental companies reveals scant mention of the application of dental surgical robots. Through industry exchanges, VCBeat has learned thatAs a “pillar” supporting dental implant services, private medical institutions have largely adopted a wait-and-see attitude toward dental surgical robots.

Overall,Despite significant progress in technological R&D and market expansion by domestically produced oral surgical robots, and the absence of competitive pressure from imported products, numerous challenges remain. The core issue lies in two prominent imbalances currently existing within the industry: the imbalance between physicians’ operational costs and clinical benefits, and the imbalance between capital investment in equipment and operational returns.

The first challenge is balancing the operational costs for physicians with clinical benefits.

Li Qiang, President of Dingzhi Dental and an expert in dental implantology, stated that due to significant variations in patients’ conditions, the intelligence and personalization capabilities of robotic planning remain insufficient. Therefore, physicians must be deeply involved in designing implantation protocols. When using robotic assistance for dental implants, preoperative data processing and path planning are time-consuming. “If overall surgical time is calculated from the start of preoperative planning, experienced surgeons can work even faster than robots. Currently, robotic technology has not yet matured to the point where it can universally enhance productivity.”

Following the comprehensive implementation of centralized procurement for dental implants, implant volumes at oral healthcare institutions have generally increased, with workflow and efficiency issues directly limiting the application of dental implant surgical robots.

In terms of clinical benefits, the core advantages of oral surgical robots lie in their precision and minimally invasive nature. However, compared with surgical robots used in laparoscopy, neurosurgery, and orthopedics, the critical necessity for these advantages is not as high. “Errors and incisions resulting from freehand implantation within a certain range do not significantly affect the success rate of the surgery,” stated Li Qiang.

Furthermore, concerns among doctors and patients regarding surgical safety have also affected the acceptance of dental implant robots. Robotic systems can detect and respond to minute movements in the patient’s oral cavity; if the patient’s position shifts, the robot adjusts accordingly to the new position, ensuring precise placement of the implant. When the patient’s movement exceeds a specific preset threshold, the system automatically activates an emergency stop mode to prevent surgical accidents. Nevertheless, many doctors remain concerned: unlike many other surgical procedures, dental implantation

The patient does not need to be under general anesthesia, as any movement may lead to uncertainty in the surgical condition.

Secondly, the mismatch between capital investment in equipment and operational output will directly affect the procurement willingness of medical institutions.

Li Qiang noted that RMB 2 million represents a significant expenditure for private dental practices, and the subsequent revenue generated by the equipment may fail to cover this cost. “With implant surgery robots or implant navigation systems, each tooth incurs over RMB 100 in costs for positioning consumables. Following the implementation of centralized volume-based procurement, prices for dental implants have dropped substantially, even entering a phase of intense price competition. Many patients are unwilling to pay a premium for advanced technology or minimally invasive procedures. Therefore, if institutions adopt these technologies for their own use, it means the more procedures they perform, the greater their losses will be.”

Furthermore, the lack of policy support is also one of the reasons for the commercialization difficulties of dental surgical robots. Of course, this is also because the charging codes for dental surgical robots have not been established in most regions, making it difficult for medical institutions to recover costs through compliant charges after introducing the equipment, which further suppresses market demand.

Overall, even in the absence of competition from imported products, domestically produced oral surgical robots must further optimize product functionalities—such as reducing overall surgical time, enhancing system fluency, and improving the surgeon’s operational experience—and continue to strengthen their commercialization strategies to better penetrate the domestic market.

According to Yao Xun, General Manager of Marketing at Lancet Robot, although the industry faces challenges, surgical robots remain a critical direction for the intelligent development of dental healthcare, offering irreplaceable value. Beyond further meeting clinical needs, they help alleviate the shortage of medical professionals and provide a standardized training platform for young dentists. The industry’s next major tasks include technological and functional iterations, as well as exploring diversified profit models.

Currently, the diversification of functional capabilities in dental surgical robots has become a major trend. The aforementioned expansion from implantology to endodontics and impacted tooth extraction represents just the beginning. Diverse surgical scenarios can enhance equipment utilization rates in healthcare institutions, thereby reducing per-unit procurement costs. Meanwhile, there is substantial room for intelligent advancement in the field of dentistry; surgical robots may offer more than just single-point solutions and could even evolve toward platform-based development in the future.

Regarding the profitability model, Yao Xun acknowledged that the industry is still actively exploring viable approaches. The pricing of consumables must strike a balance between patient affordability and corporate sustainability, while also necessitating innovation in after-sales service models. The industry consensus is to first increase equipment installation rates and gradually refine revenue streams.

Let’s examine Yomi’s commercialization path: Unlike traditional surgical robots that rely on large hospitals, Neocis has focused its promotion of Yomi on private dental clinics. A co-founder of Neocis once stated that this approach necessitates making expensive robotic technology more accessible and affordable.

Of course, the United States has a different dental healthcare service system, payment structure, and patient awareness, so Yomi’s commercialization path may not be fully applicable in China. Nevertheless, Yomi still offers valuable insights: for many private medical institutions, the high upfront procurement cost of dental surgical robots is a major barrier to their adoption. Therefore, to rapidly capture this significant market segment, it may be advisable to reduce initial procurement investments to increase installation rates, thereby laying the foundation for future profitability.

Notably, expanding into overseas markets has become a key strategic choice for Chinese manufacturers of dental surgical robots.

From the perspective of pricing structures, service prices for dental implants overseas are significantly higher than those in China, creating room for technology premiums.Li Qiang pointed out that dental implant fees in European and American markets are approximately 8–10 times higher than those in China. Patients are more willing to pay for technological innovation and surgical quality, and commercial insurance provides relatively high coverage for new technologies, making it easier for medical institutions to balance their return on investment. Furthermore, in many overseas markets, the volume of implant procedures is relatively lower, allowing physicians more ample time to adopt new products and technologies.

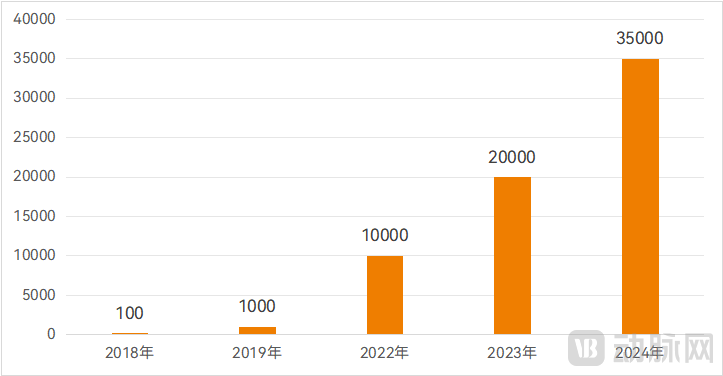

In terms of market acceptance, dental surgical robots represented by Yomi have already established a certain level of market recognition overseas.According to data released by Neocis, after selling its first Yomi device in 2017, the system assisted dentists in completing 1,000 implant surgeries by 2019. In the following years, the number of cases grew rapidly, reaching 35,000 by 2024. A review of the websites of some U.S. dental clinics also reveals that the Yomi robot has become a key highlight in promoting their service advantages.

Growth in the Number of Yomi Robot Application Cases. Data Source: Neocis Official Website

Yao Xun believes that,Compared with the domestic market, overseas markets offer a more mature development environment for dental surgical robots.In June 2025, Shenzhen Lancet Robot Co., Ltd. completed its Series A+ financing round. The funds will be utilized for the establishment of an industrialization base for domestically produced surgical robots across multiple departments, subsequent product R&D and iteration, and global commercial expansion. “While promoting products such as joint replacement surgical robots overseas, the company learned from distributors about the urgent demand for oral surgical robots in international markets. Driven by these distributors, our oral surgical robots have begun to be showcased in regions including South America.”

In July 2025, Yakebot’s dental implant robot obtained CE certification, becoming “the first known oral surgery robot to receive CE certification,” and officially embarked on its path to internationalization.

Looking at the current landscape, the oral surgery robot industry is still in its early stages of development. For companies, it is essential to consistently focus on the core needs of doctors and patients, use clinical pain points as the direction for technological iteration, and formulate flexible market strategies tailored to local conditions in both domestic and international markets.

In the global market, leading Chinese companies are nearly on par with U.S. firms such as Yomi, with no significant gap observed compared to other surgical robotics sectors. It remains to be seen whether domestically produced products can emerge as a global benchmark in oral surgery, akin to the da Vinci Surgical System—a prospect worth anticipating.

Note: The scope of this article covers oral surgery navigation and positioning systems equipped with robotic arms, excluding standalone navigation systems.