Alkermes to Acquire Avadel Pharmaceuticals in $2.1 Billion Deal to Expand Sleep Medicine Portfolio

Alkermes

Innovative Drug Developer

On October 22, 2025, Alkermes plc (hereinafter referred to as “Alkermes”), headquartered in Ireland, announced the acquisition of biopharmaceutical company Avadel Pharmaceuticals plc (hereinafter referred to as “Avadel”) for up to $2.1 billion.The transaction involves not only a cash acquisition at $18.50 per share but also a Contingent Value Right (CVR): Alkermes will pay an additional $1.50 per share if Avadel’s flagship drug, Lumryz, receives approval from the U.S. Food and Drug Administration (FDA) for the treatment of Idiopathic Hypersomnia (IH) in adults by the end of 2028.TheThe transaction is expected to be completed in the first quarter of 2026.

Avadel: Once-Daily Bedtime Dosing Breaks Through in Narcolepsy Treatment, with Lumryz as the Core Asset of the Acquisition

As the target company in this acquisition, Avadel has upheld “Transforming medicines to transform lives” as its core mission since its inception. With years of deep expertise in the treatment of narcolepsy, the company has built a unique competitive advantage through its differentiated pipeline.

From the perspective of corporate fundamentals, Avadel’s financial performance and product competitiveness have shown a steady upward trend in recent years.According to the company’s financial report, Avadel’s performance in the second quarter of 2025 exceeded expectations, with earnings per share (EPS) reaching $0.10 and marking its first-ever net profit. Since its launch in 2023, Lumryz, the company’s core product, had been adopted by approximately 3,100 patients as of June 30, 2025. Starting from July 2023, new patient uptake has shown a significant advantage over competing products that require twice-nightly dosing. Net revenue contribution from Lumryz is projected to reach $265–275 million in 2025.

In the capital markets, Avadel has also gained institutional recognition: According to The Financial Times, H.C. Wainwright raised its target price for the stock from $24 to $36 in 2025, while UBS also increased its target price from $13 to $20, citing Lumryz’s sales performance, which underscores market confidence in the product’s value.

Avadel has become the focus of acquisition interest primarily due to its pipeline asset highly relevant to the treatment of narcolepsy—the already commercialized Lumryz therapy.As the first FDA-approved, once-daily bedtime treatment for narcolepsy, Lumryz breaks through the limitations of traditional therapies.Traditional medications for narcolepsy often require patients to take multiple doses each night, which not only reduces medication adherence but may also impair sleep quality due to nighttime awakenings. In contrast, Lumryz utilizes an extended-release sodium oxybate formulation technology to provide sustained efficacy throughout the night with a single dose, thereby improving daytime wakefulness while minimizing disruption to nocturnal sleep.

Alkermes: Deepening its Commitment to Neuroscience and Accelerating Expansion in the Somnolence Sector through M&A

In contrast to Avadel’s specialization in narcolepsy treatment, Alkermes is a global biopharmaceutical company with core competencies in neuroscience. Since its inception, the company has leveraged its extensive expertise in psychiatric and neurological disorders to launch multiple commercialized therapies, including Vivitrol for alcohol and opioid dependence, Aristada for schizophrenia, and Lybalvi for schizophrenia and bipolar disorder. With 2024 sales reaching $1.56 billion, Alkermes has established a strong brand presence in the neuropsychiatric therapeutic area.

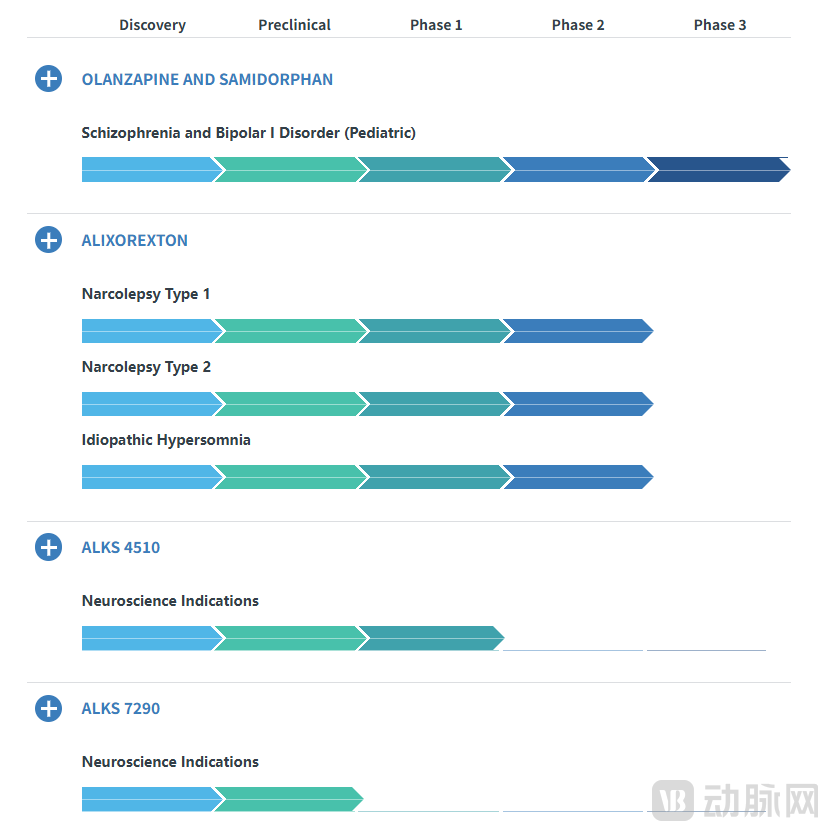

In terms of its R&D pipeline, Alkermes also focuses on areas with high unmet needs.Alixorexton, an oral orexin-2 receptor agonist under development, is currently in Phase II clinical trials and is intended for the treatment of Type 1 narcolepsy, Type 2 narcolepsy, and idiopathic hypersomnia. Additionally, the pipeline includes ALKS 4510, which is in Phase I clinical trials, and ALKS 7290, which is in the preclinical stage; both are orexin-2 receptor agonists, forming a tiered R&D portfolio targeting central nervous system disorders.

Overview of Alkermes' Pipeline in Development

In terms of strategic layout, Alkermes has recently signaled its intent to deepen its neuroscience pipeline through key personnel appointments and R&D incentive mechanisms.On September 12, 2025, the company announced the appointment of Joshua Reed as Chief Financial Officer (CFO), effective September 15, to strengthen its financial control and capital operations capabilities.

Meanwhile, Alkermes maintains its “Alkermes Pathways Research Awards®” program, supporting neuroscience research related to psychiatric disorders, bipolar disorder, and sleep/circadian disturbances through grants for early-career investigators (with a cap of $100,000 per project). These initiatives reflect the company’s continued investment in organizational and R&D incentives, while the acquisition of Avadel can be seen as a strategic move to further extend its expertise in neuroscience into the field of sleep disorder treatments.

Short-Term Cash Flow Fixes, Long-Term Combination Therapy Strategies: Hidden Challenges in the Sleep Market Layout

While this acquisition appears logical on the surface, it actually reflects Alkermes’ multifaceted considerations regarding R&D cycles, synergistic strategic alignment, and capital strategy.

First, from the perspective of the R&D and commercialization cycle, Alkermes’ self-developed orexin-2 agonist Alixorexton is still in the mid-to-late stages of clinical development (Phase 2 to Phase 3), and it will take time before commercialization; whereas Avadel’s Lumryz has already been approved in the field of narcolepsy and is generating revenue. Through this acquisition, Alkermes can quickly enter the sleep medicine sector, gaining a mature asset and sustainable cash flow, thereby significantly shortening the R&D return cycle and reducing market uncertainty.

Secondly, from the perspective of products and mechanisms, the core assets of the two companies are not simply overlapping but present potential for synergy.Industry analysis indicates that Lumryz® primarily affects nighttime sleep by modulating the gamma-hydroxybutyrate (GHB) pathway, whereas Alixorexton enhances daytime wakefulness by activating orexin-2 receptors. The two agents are complementary within the “nighttime sleep–daytime wakefulness” circadian regulation axis, paving the way for future research into combination therapy. This approach not only optimizes therapeutic efficacy but also enables sharing of patient populations, physician education initiatives, and market channels. This implies that the acquisition does not involve asset overlap; rather, it may serve as a starting point for developing combination therapies and achieving pipeline synergies.

From a market perspective, although sleep disorders and narcolepsy fall within the realm of rare diseases, they have witnessed significant growth in recent years. With improved patient identification rates and innovations in novel dosage forms, the industry is emerging as a high-value sector attracting substantial capital investment.For example, Harmony Biosciences and Bioprojet entered into an exclusive license agreement in 2024 to jointly develop TPM-1116, a highly selective oral orexin-2 receptor agonist; Jazz Pharmaceuticals previously acquired global rights to DSP-0187 from Sumitomo Pharma, a potent, highly selective oral orexin-2 receptor agonist indicated for the treatment of narcolepsy, idiopathic hypersomnia, and other sleep disorders; Avadel itself introduced valiloxybate, a novel once-nightly oxybate formulation, through a licensing agreement with XWPharma.

However, integration challenges and external risks cannot be overlooked.Alkermes needs to deeply integrate Avadel’s organizational structure, compliance framework, and supply chain, while properly addressing patent litigation related to its products. From an external perspective, regulatory uncertainty persists, centering on the approval prospects for Lumryz in the new indication of idiopathic hypersomnia (IH). Meanwhile, competitive pressure from drugs with novel mechanisms of action is intensifying; for instance, orexin receptor agonists developed by companies such as Takeda and Centessa have entered late-stage clinical trials, and their oral convenience poses a potential risk of market share diversion from Lumryz. Furthermore, investors are concerned about the vision-related adverse events (such as blurred vision) already specified in Lumryz’s drug label, which may affect patients’ long-term medication adherence and cap the product’s market penetration.

Overall, this acquisition represents both Alkermes’ proactive strategy to accelerate its entry into the sleep medicine market and optimize its product portfolio, as well as a high-stakes balancing act among regulatory compliance, integration, and competition. If the company can make steady progress by capitalizing on trends such as regulatory easing, improved patient identification, and the parallel advancement of precision medicine, Alkermes may well transition from a “long-term value-oriented enterprise” to a “multi-asset neuroscience platform company.” As innovation in rare diseases enters the deep waters of industrialization, this may precisely reflect the true strategic intent of industry giants—Anchored by Deterministic Assets, Betting on the Next High-Barrier Cycle.