BiBette Pharma Surges 174% on Sci-Tech Innovation Board Debut with First-in-Class Drug BEBT-908

BeBetter Med

Innovative Drug Developer

Today, BeBetter Med Inc. (hereinafter referred to as “BeBetter”) was officially listed on the STAR Market of the Shanghai Stock Exchange, with the stock code 688759, has successfully listed on the forefront of the capital market, becoming another biotechnology enterprise centered on innovative small-molecule drugs and holding “First-in-Class” technological barriers.The stock opened today at RMB 48.90 per share, a significant increase of 174.91% from its issue price of RMB 17.78 per share. As of press time, the share price stood at RMB 30.70, representing a gain of 72.67%, with a total market capitalization reaching RMB 13.816 billion.

According to the issuance announcement,The company is issuing 90 million shares in this offering at an issue price of RMB 17.78 per share, raising approximately RMB 1.599 billion in total proceeds.; The raised funds will be primarily directed towards new drug R&D projects, the Qingyuan R&D Center, and the construction of a formulation industrialization base, as well as supplementing working capital, thereby further strengthening the company’s end-to-end capabilities from early-stage drug discovery to commercial-scale production. Notably, the net proceeds from this fundraising, after deducting issuance expenses, amount to approximately RMB 1.49 billion, whereas the company’s originally planned fundraising scale was approximately RMB 2 billion. Consequently, the final amount raised represents a reduction of approximately RMB 500 million compared to the initial requirement (calculated on a net basis).

Looking back on its listing journey, BeBetter Med’s path to going public began on June 29, 2022, when the Shanghai Stock Exchange formally accepted its application for listing on the STAR Market. The company successfully passed the Listing Committee review on January 11, 2023, and submitted its registration application on June 10 of the same year. It finally received the approval notice for registration effectiveness on August 7, 2025, and completed its stock exchange listing today, with the entire process spanning nearly three years.

Notably,Its critical push for listing coincided with the policy window of “prudently restoring the Fifth Set of Standards for the STAR Market” following the implementation of the CSRC’s “Eight Measures for the STAR Market” in 2025.With its core products entering the commercialization stage and multiple pipelines advancing in parallel, it has become a typical case of an innovative pharmaceutical company accessing capital under this standard.

High-Intensity R&D + Launch of First-in-Class New Drug: Solidifying the Foundation for IPO

Founded in 2012, BeBetter Med is a biopharmaceutical company driven by translational medicine and the R&D of original innovative drugs. Its founding team, with backgrounds in translational medicine and drug development, has long been committed to mechanistic innovation and the development of precise targets, focusing on addressing unmet clinical needs in the field of major diseases.

The company's R&D portfolio covers three major therapeutic areas: oncology, autoimmune diseases, and metabolic disorders., primarily including lymphoma, breast cancer, lung cancer, psoriasis, diabetes complicated with non-alcoholic steatohepatitis (NASH), and obesity, all of which represent therapeutic areas with substantial unmet clinical needs and vast market potential.

As an R&D-driven enterprise with innovation at its core, BeBetter Med maintains a high level of investment in research and development.From 2022 to 2024, the company’s cumulative R&D expenses exceeded RMB 440 million, with an R&D expense ratio as high as 92% in 2022. As of June 2025, BeBetter Med has obtained 32 granted global invention patents. The core team is led by Professor Qian Changgeng, a distinguished expert under the “National Major Talent Program,” who brings nearly 40 years of experience in drug development and has been deeply involved in the R&D of four First-in-Class drugs approved by the U.S. Food and Drug Administration (FDA).

The company'sCore Product BEBT-908, a First-in-Class Dual HDAC/PI3Kα Small-Molecule Inhibitor for the Treatment of Relapsed or Refractory Diffuse Large B-Cell Lymphoma (r/r DLBCL).The drug received conditional marketing approval from the National Medical Products Administration (NMPA) on June 30, 2025, becoming the first-in-class innovative drug with its mechanism of action. Phase II clinical data showed that BEBT-908 achieved an overall response rate (ORR) of 54.6%, with a median overall survival (OS) of 8.8 months, significantly superior to previous chemotherapy regimens (median OS approximately 4.0–4.7 months). In patients who had previously failed CAR-T (chimeric antigen receptor T-cell therapy) or bispecific antibody treatment, the ORR remained above 67%, demonstrating clinical potential. The project was supported by the National Science and Technology Major Project during the “13th Five-Year Plan” period and received Breakthrough Therapy Designation.

11 Class I New Drugs + 2 Drugs Awaiting Launch to Drive Long-Term Performance Growth

With the successful launch of BEBT-908, BeBetter Med’s innovative pipeline has begun to serve as the primary engine for future growth. According to the prospectus, as of the signing date,The Company has only one product, BEBT-908, approved for marketing, with multiple other pipeline candidates in the reserve stage.; Currently, a R&D matrix covering 11 Class 1 new drug candidates and 19 indications has been established, with a cumulative total of 33 clinical trial approvals obtained. One pivotal Phase II, one Phase III, seven Phase II, and eight Phase I clinical trials are being conducted simultaneously, with core R&D efforts focused on oncology and immune diseases.

Overview of BeBetter Med's Pipeline in Development

Among them, BEBT-209 is in Phase III clinical trials, and BEBT-109 has been approved to initiate Phase III clinical trials; both are expected to receive marketing approval in 2027.

BEBT-209 is a CDK4/6 inhibitor indicated for the treatment of advanced breast cancer. According to Frost & Sullivan, the market size of breast cancer drugs in China reached RMB 59.5 billion in 2023 and is projected to rise to RMB 110.4 billion by 2030, making this therapeutic area one of the largest by revenue within China’s oncology drug market.

BEBT-109 is a pan-mutant EGFR inhibitor for the treatment of EGFR mutation-positive non-small cell lung cancer (NSCLC). According to Frost & Sullivan, the market size of targeted therapies for NSCLC in China reached RMB 62.1 billion in 2023 and is projected to climb to RMB 159.8 billion by 2030.

Furthermore,BEBT-908’s dual-targeting profile and broad-spectrum antitumor activity confer potential for synergistic development with other anticancer agents., for example, in combination with BEBT-209 for HR+/HER2- advanced breast cancer, or in combination with BEBT-109 for patients who have experienced disease progression after treatment with third-generation EGFR-TKIs. Currently, these related combination therapies are all in Phase Ib/II clinical trials, with market launch expected in 2027.

In the field of metabolic diseases, BeBetter Med’s key project BEBT-809 (a GPR75 inhibitor) also possesses first-in-class potential.This drug targets G protein-coupled receptor 75 (GPR75) to regulate energy metabolism and lipolysis, thereby achieving the mechanism of “fat reduction with muscle preservation.” Compared with the widely used glucagon-like peptide-1 (GLP-1) class of drugs, BEBT-809 is expected to avoid the common side effect of muscle loss associated with the latter and provide an alternative treatment option for individuals intolerant to GLP-1 therapies. The drug is currently in the preclinical stage.

It is worth noting that the company expects BEBT-908 to be the only investigational product capable of commercialization before 2027, which means that its short-term performance will still rely primarily on the market performance of this drug. The clinical progress and commercial translation of other pipelines will directly affect the certainty of the company's medium- and long-term growth.

From a technical layout perspective, BeBetter Med is positioning itself for the next phase of growth through a dual-track strategy combining its siRNA (small interfering RNA) drug platform with innovative targets in metabolic diseases.The company has established an integrated small nucleic acid drug R&D platform with global intellectual property rights., covering multiple aspects including the design and screening of siRNA drugs, chemical modification, in vitro and in vivo efficacy evaluation, as well as pharmacokinetics and safety assessment systems. We have successfully established a GalNA-siRNA conjugate delivery system (GSOC and GDOC) targeting the liver, and a peptide-siRNA conjugate (POC) delivery system targeting various organs such as the kidney and central nervous system (CNS), to address the issues of poor stability, low tissue penetration, and insufficient targeting associated with traditional siRNA therapeutics.

Overall, BeBetter Med’s R&D portfolio is expanding from a sole focus on oncology to the cutting-edge intersection of immunology and metabolic diseases.Establish a development model of “short-term performance supported by BEBT-908 and long-term growth driven by platform expansion”。

Tapping into the Lymphoma Market’s 17.3% High Growth: Single-Product Dependence Becomes a Test

BeBetter Med focuses on diffuse large B-cell lymphoma (DLBCL), a subfield within hematologic malignancies characterized by a large patient population and significant unmet clinical needs, all set against the backdrop of the rapidly expanding global and Chinese oncology drug markets.

From an industry-wide perspective, according to data from Frost & Sullivan,The global market size of anti-tumor drugs reached $228.9 billion in 2023 and is projected to increase to $419.8 billion by 2030.; China's anti-tumor drug market was valued at RMB 241.6 billion in 2023 and is expected to exceed RMB 548.4 billion by 2030, with a compound annual growth rate (CAGR) of 12.4%. The lymphoma treatment sector, which includes diffuse large B-cell lymphoma (DLBCL), has shown particularly outstanding performance—according to Frost & Sullivan data,In 2023, the market size of lymphoma treatment drugs in China was approximately RMB 19.1 billion, and it is expected to reach RMB 58.3 billion by 2030, with a compound annual growth rate (CAGR) of 17.3%., with improvements in treatment modalities and prolonged patient survival, demand for related drugs continues to grow, indicating significant market growth potential.

In terms of the treatment landscape, seven therapies have been approved in China for third-line or later treatment of relapsed/refractory diffuse large B-cell lymphoma (r/r DLBCL), including CAR-T cell therapies, bispecific antibodies, and small-molecule drugs.There are significant cost differences among various therapies: CAR-T therapy costs approximately RMB 1.2 million per course, bispecific antibody drugs cost around RMB 476,000 per course, while the annual treatment cost for selinexor tablets has dropped to approximately RMB 120,000 after being included in the National Reimbursement Drug List (NRDL). BeBetter Med’s BEBT-908 has not yet been included in the NRDL; its initial launch price is expected to be lower than that of CAR-T therapy and bispecific antibody drugs. The company has established an industrialized supply chain system with WuXi AppTec and Guangdong Singhoon, and plans to promote the inclusion of this drug in the national medical insurance and local supplementary insurance schemes to enhance accessibility and reduce the financial burden on patients.

However, market competition persists. The objective response rate (ORR) of some marketed drugs exceeds 68%, whereas Phase II clinical data for BEBT-908 show an ORR of 54.6%, indicating a certain gap in efficacy.

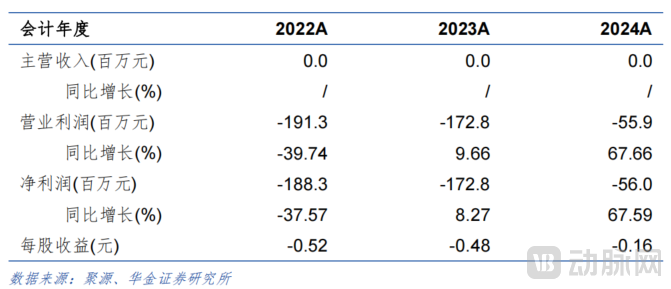

According to financial report data, BeBetter Med did not generate any main business revenue from 2022 to 2024., with net losses attributable to shareholders of the parent company amounting to approximately RMB 188 million, RMB 173 million, and RMB 56 million, respectively. The loss narrowed significantly year by year, and earnings per share improved from -RMB 0.52 in 2022 to -RMB 0.16 in 2024.

BeBetter Med's Revenue and Profit Performance Over the Past Three Years

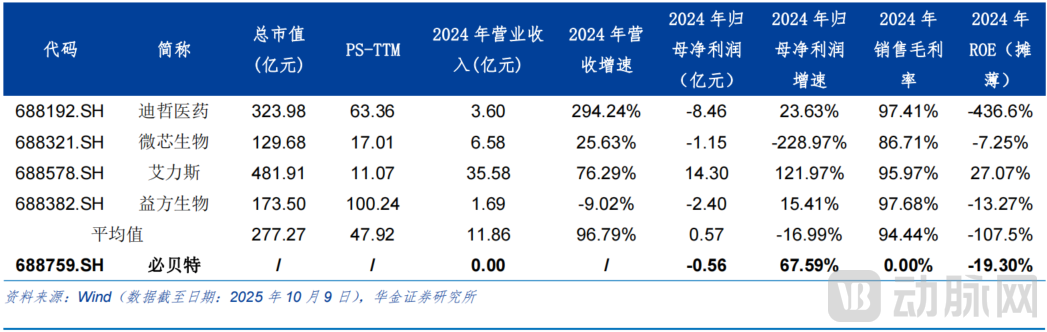

Compared with early-stage innovative drug companies such as Dizal Pharmaceutical and Chipscreen Biosciences, BeBetter Med currently has only one approved product, BEBT-908, with its commercialization still in the initial stage and no revenue generated yet. Therefore, the core of its valuation lies in the expected realization of its “First-in-Class technological barriers and the potential of its subsequent pipeline.” If the commercial ramp-up of BEBT-908 proceeds smoothly and the pipeline portfolio advances steadily, the company is poised to secure a capital premium driven by its mechanistic innovation and team execution capabilities.

Comparison of Indicators Among Listed Companies in the Same Industry

Overall, BeBetter Med’s IPO is not only a significant milestone in its entry into the capital markets but also provides a case study for observing the pricing and valuation models of early-stage innovative pharmaceutical companies. In the short term, attention should be focused on the sales ramp-up of BEBT-908 and progress in its inclusion in the National Reimbursement Drug List (NRDL). In the medium term, focus should be placed on the R&D and commercialization pace of its pipeline portfolio. In the long term, it is essential to assess whether the company can establish a solid foothold in the hematologic malignancy treatment landscape through technological innovation and cost accessibility, thereby supporting the sustainability of its valuation.Post-listing, the commercialization progress of BEBT-908, key data from its subsequent pipeline, and R&D investment alongside capital utilization efficiency will become key metrics closely monitored by investors.