Domestic Innovators Disrupt China's Influenza Drug Market Amid Surge in New Entrants

Expectations of an Influenza Outbreak Drive a Surge in Biopharmaceutical Stocks.

The National Administration of Disease Control and Prevention stated at a press conference that the peak of the influenza epidemic in China is expected to occur from mid-to-late December to early January this autumn and winter. Meanwhile, according to data from the Chinese Center for Disease Control and Prevention, during the 44th week of 2025 (October 27–November 2), the positivity rate for influenza viruses among national outpatient and emergency visits for influenza-like illness was 17.5%, an increase of 6.4 percentage points compared with the previous week. Influenza activity has risen generally in southern provinces, while most northern provinces are also experiencing an upward trend. Since the onset of the autumn-winter season this year, influenza virus has surpassed rhinovirus, respiratory syncytial virus, and other pathogens to become the predominant cause of respiratory infectious diseases.

This news has sparked market attention and a surge in demand for influenza-related stocks. Te Yi Pharmaceutical hit the daily limit up for two consecutive days, while Bohui Innovation, Panlong Pharmaceutical, and Zhongsheng Pharmaceutical also successively hit the daily limit up. Meanwhile, Starry Pharmaceutical, Ha Sanlian, and Jinhua Co., Ltd. followed suit with notable gains.

Given the high correlation between influenza drug sales and flu outbreak cycles, the severity of flu outbreaks directly determines the sales performance of related medications. Over the past decade, oseltamivir has dominated the Chinese market, achieving a remarkable sales milestone of RMB 6.5 billion in 2019. Although its price declined due to centralized volume-based procurement, sales volume has continued to grow. Subsequently, Roche reignited a purchasing frenzy with baloxavir marboxil (Xofluza), marketed as a “miracle flu drug” for its single-dose regimen. Particularly during the 2024 flu season, market shortages occurred, and prices were speculated up from the original retail price of over RMB 200 to more than RMB 500.

However, the 2025 influenza market will no longer be a “duopoly” of oseltamivir and Xofluza.

In March, Masupiravir tablets (Yisuda), developed by Kerui Pharmaceutical, a subsidiary of Qingfeng Pharmaceutical Group, received market approval; in May, Onradivir tablets (Anruiwei), developed by Ruichuang Biotechnology, a subsidiary of Zhongsheng Pharmaceutical, were approved for launch; in July, Maseiloxavir tablets (Jikeshu), jointly developed by Jichuan Pharmaceutical and Zhengxiang Pharmaceutical, gained market approval; and in September, the marketing application for Madonosavir granules, co-developed by Simcere Pharmaceutical and Andikang Biotechnology, was formally accepted by China’s National Medical Products Administration (NMPA). Coupled with Jiankangyuan’s previously submitted marketing application for Marboxilvir, domestically produced innovative influenza drugs are experiencing a surge after prolonged accumulation. The year 2025 can be regarded as Year One for domestically produced innovative influenza medications in China.

On the other hand, Sunshine Guojian Pharmaceutical, which had previously secured a dominant share of the domestic market with its generic oseltamivir, lost its bid in the latest round of centralized procurement, further fueling volatility in an already unsettled landscape. The Chinese influenza market is poised for significant upheaval.

Oseltamivir dominated the domestic influenza drug market for the past decade, until the emergence of baloxavir.

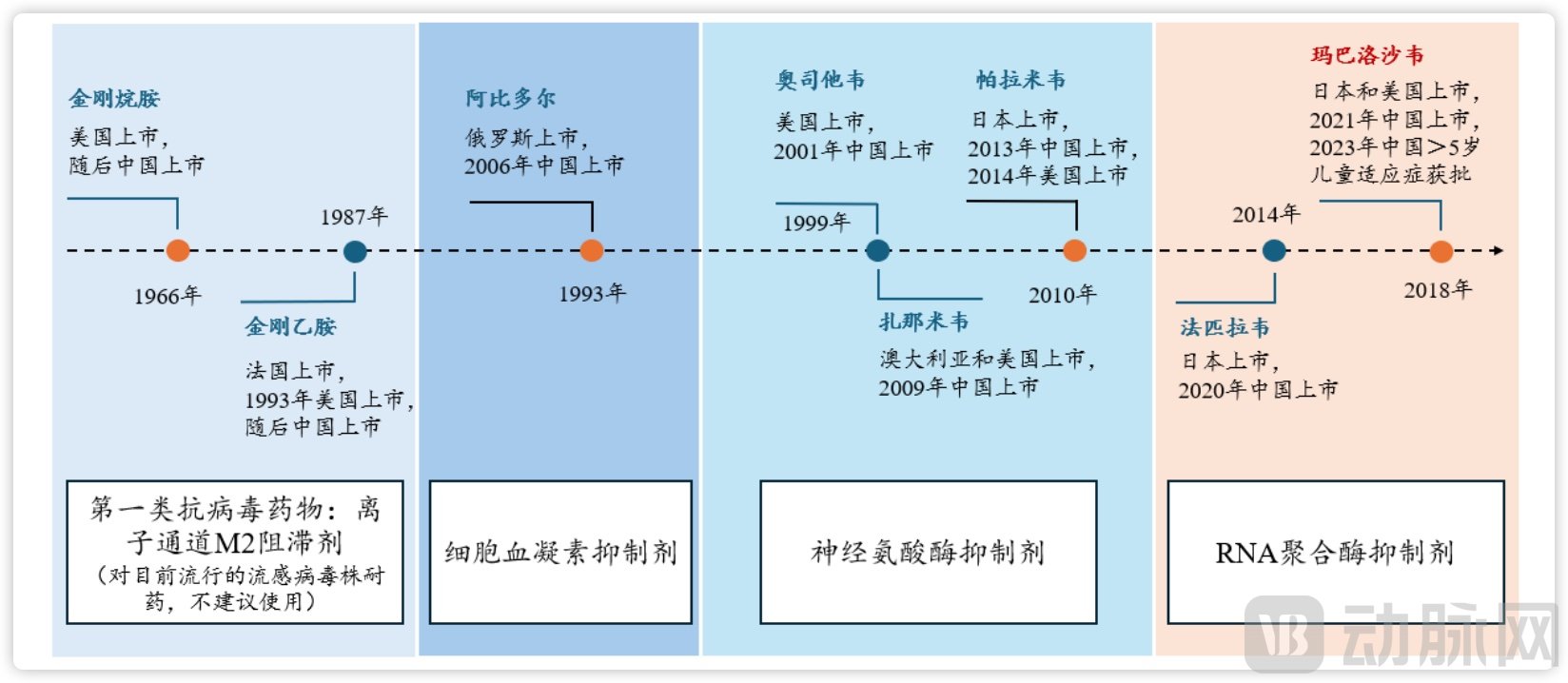

Anti-influenza antiviral drugs have undergone continuous updates and iterations in recent decades, evolving from the initial ion channel M2 blockers to the latest RNA polymerase inhibitors. This evolution reflects advancements in the mechanisms of action for influenza medications and represents an ongoing effort to combat drug resistance.

The “Diagnosis and Treatment Protocol for Influenza (2025 Edition)” indicates that the currently marketed drugs in China with activity against influenza viruses mainly include neuraminidase inhibitors (e.g., oseltamivir), RNA polymerase inhibitors (e.g., baloxavir, a PA-targeting agent), and hemagglutinin inhibitors.

The Iteration Process of Influenza Drugs, Source: Open Source Securities

Currently, the primary considerations for influenza medications are drug resistance and the time to symptom relief.

For example, since nearly all currently circulating seasonal influenza viruses are resistant to M2 ion channel inhibitors, these agents are no longer recommended for the clinical treatment of influenza. Meanwhile, with the widespread use of neuraminidase inhibitors (NAIs), some viral variants have begun to develop resistance, most commonly in the N1 subtype. For instance, among pediatric patients, the resistance rates for H1N1 and H3N2 are approximately 27%–37% and 3%–18%, respectively, whereas the resistance rate in adults is only about 1%.

Furthermore, viral escape mutants with reduced drug susceptibility have also been observed in patients treated with baloxavir. Studies indicate that these variants primarily involve I38T/M/F or E23K substitutions in the polymerase acidic (PA) protein. The detection rate of these variants is approximately 10% in adults and adolescents, whereas it can exceed 20% in pediatric trials. This suggests that pediatric patients face a higher risk of resistance when treated with baloxavir.

As can be seen, although oseltamivir and baloxavir marboxil dominate the domestic market, they are not without vulnerabilities, leaving ample room for latecomers to make breakthroughs.

Drug Resistance Becomes the Breakthrough Entry Point for Domestic Innovative Influenza Drugs.

Taking Mashulaxavir Tablets (Yisuda), developed by Qingfeng Pharmaceutical, as an example, it is similar to baloxavir marboxil (Xofluza). Both work by inhibiting the acidic protein (PA) subunit of the influenza virus RNA polymerase, rapidly blocking viral mRNA synthesis, thereby swiftly suppressing viral replication and enabling a single-dose treatment for the entire course.

Notably, in terms of resistance, no I38T mutations were detected in 365 influenza B virus samples collected from 191 patients during the previously conducted Phase 2 clinical trials. Thirty samples randomly selected for drug resistance testing using the viral plaque reduction assay showed no decrease in drug susceptibility. In the Phase 3 clinical trials, the rates of resistance-associated mutations to marboxil tablets against influenza A H1N1 and H3N2 subtype viruses were only 0.7% and 0.9%, respectively. No resistance mutations were detected in patients with influenza B, demonstrating its advantage in terms of low resistance potential.

Onradivir Tablets (Anruiwei), the world’s first novel anti-influenza A PB2 agent, was jointly developed by Guangzhou Laboratory, the First Affiliated Hospital of Guangzhou Medical University, the National Center for Respiratory Medicine, the National Clinical Research Center for Respiratory Diseases, and Guangdong Zhongsheng Ruichuang Biotechnology Co., Ltd.

PB2 is the first subunit of the viral RNA polymerase, a key enzyme for viral replication. Its primary function is to specifically bind to host capped mRNA. Subsequently, the second subunit, PA, performs endonucleolytic cleavage to capture the cap structure from the host mRNA and transfers it to the third subunit, PB1. Using viral RNA as a template, the complex transcribes viral mRNA, ultimately producing the proteins required by the virus.

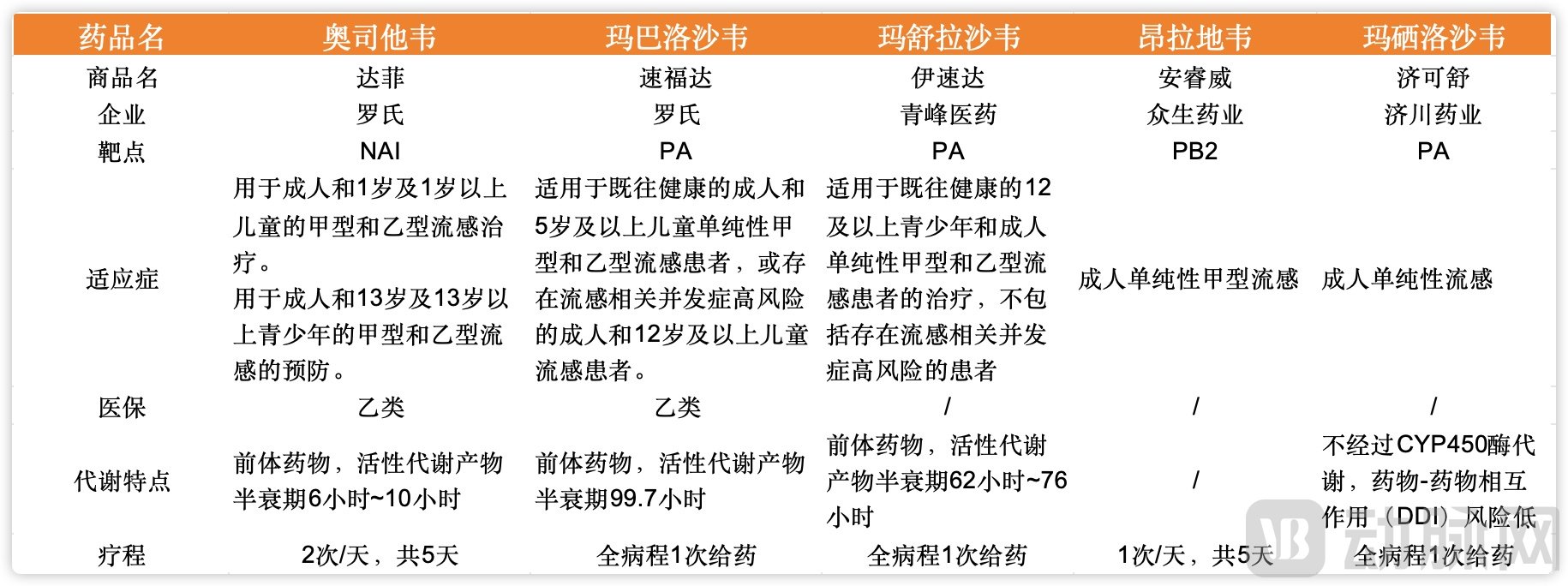

Comparison of the Characteristics of Multiple Influenza Drugs, Data Sourced from Minseng Pharma

The unique mechanism of onradivir lies in its ability to bind to PB2, the first subunit of the RNA polymerase complex, by acting as a cap structure analog. This binding prevents the RNA polymerase from interacting with host capped mRNA, thereby blocking subsequent protein synthesis via replication and transcription, and ultimately inhibiting viral replication. In other words, targeting PB2 can inhibit viral replication at an earlier stage compared to targeting PA, and there is no cross-resistance.

Previously, the Phase 2 and Phase 3 clinical data of onradivir were published in The Lancet and received peer-reviewed recognition. The studies highlighted that the drug interferes with the initial stages of viral transcription and replication through a “cap-snatching” mechanism, thereby demonstrating potent inhibitory activity against oseltamivir- and baloxavir-resistant strains. Furthermore, it is effective against avian influenza viruses, offering potential for combating zoonotic diseases.

In previous head-to-head Phase III clinical trials, Onradivir demonstrated multiple advantages. Zhongsheng Pharmaceutical also published detailed comparative data: the time to peak drug concentration was 0.5–2 hours for Onradivir versus 4 hours for baloxavir; regarding the proportion of reduction in duration across seven influenza symptoms, Onradivir showed a 39% reduction compared with placebo, whereas oseltamivir and baloxavir showed 33%; in terms of resistance rates, baloxavir had a rate of 9.7%, while Onradivir’s rate was only 1.6%.

Marboxil tablets, newly approved in July, are equally impressive. Phase III clinical trials demonstrated that the time to alleviation of influenza symptoms was significantly shorter in both marboxil dose groups compared with the placebo group. Meanwhile, the time to negativity for influenza virus RNA was 41.4 hours in the treatment groups, significantly lower than the 90.7 hours observed in the placebo group. In terms of onset of action, fever symptoms were significantly relieved within just 23.6 hours in the treatment groups, achieving defervescence within one day.

In terms of safety, as it is not metabolized by CYP450 enzymes, the risk of CYP450-mediated drug-drug interactions (DDIs) is reduced. The likelihood of interactions when used concomitantly with common medications for chronic diseases is low, providing a safe therapeutic option for patients with multiple comorbidities and polypharmacy. Regarding resistance, marboxil tablets demonstrated a resistance-associated mutation rate of only 1.8% in clinical trials. This characteristic underscores its long-term clinical value in the management of influenza.

It is evident that domestically developed novel influenza drugs have not pursued simple follow-on innovation; instead, they have focused on safety, efficacy, and drug resistance, charting a course driven by actual clinical needs.

The Evolution of China's Influenza Drug Market Over the Past Decade Is Worth Noting.

Although 2025 can be regarded as the inaugural year for domestically developed innovative influenza drugs in China, the subsequent commercialization challenges remain formidable. After all, the domestic influenza drug market has undergone profound transformations over the past decade, with particularly notable shifts in drug iterations (represented by oseltamivir and baloxavir marboxil), price fluctuations, and the evolving competitive landscape among enterprises. It is worthwhile to analyze the underlying causes driving these changes and the key factors influencing market choices.

Taking oseltamivir (Tamiflu) as an example, since its approval and launch in China in 2002, it has become the most widely used antiviral drug for the treatment and prevention of influenza. During the H5N1 avian influenza outbreak in 2005, it became the first-line choice for antiviral therapy, with a surge in orders straining production capacity. In this emergency situation, Roche successively granted domestic production rights to Shanghai Pharmaceuticals and HEC Pharm, but restricted their use to strategic reserves for epidemic prevention and control, prohibiting commercial sales. Against this backdrop, Shanghai Pharmaceuticals chose to halt production, while HEC Pharm persisted until the expiration of the original patent.

Leveraging years of accumulated manufacturing expertise, HEC Pharm became the first domestic company to have its relevant generic drug pass the Consistency Evaluation, marketed under the brand name “Kewei.” According to available data, driven by the persistent prevalence of influenza viruses and a rising number of flu cases in China from 2016 to 2019, HEC Pharm’s performance surged by 600% over those three years. In 2019, Kewei generated sales revenue of RMB 5.93 billion, accounting for approximately 95.4% of HEC Pharm’s total turnover that year. However, impacted by the 2022 volume-based procurement (VBP) program and shifts in market demand, HEC Pharm suffered significantly, reporting a loss of nearly RMB 1.5 billion that year. Subsequent sales have been highly volatile, and the company’s recent failure to win bids in the 11th national VBP round is expected to substantially erode its market share in the future.

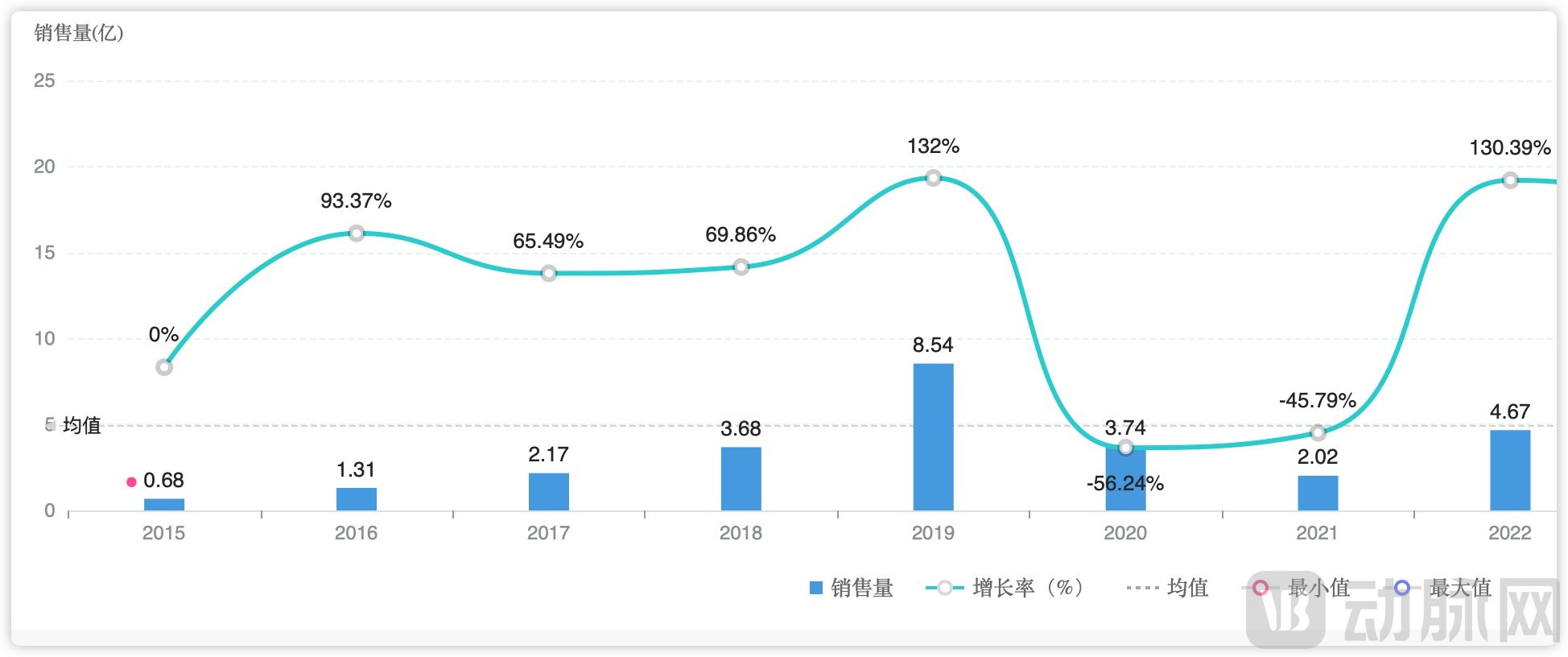

Domestic Hospital Sales of Oseltamivir, Source: MesoPharm

Data from MedSino’s in-hospital sales also reveal that domestic oseltamivir sales peaked in 2019 and have been on a steady decline since. During this period, the price of oseltamivir experienced significant fluctuations: it initially reached as high as RMB 300 per treatment course, dropped by approximately half to around RMB 150 during the generic drug era, further declined to the RMB 70 range amid intense market competition, and was ultimately driven down to approximately RMB 30 following the implementation of centralized volume-based procurement. It can be said that the cyclical nature of influenza outbreaks and policy interventions were the core factors determining the market trajectory of oseltamivir during this phase.

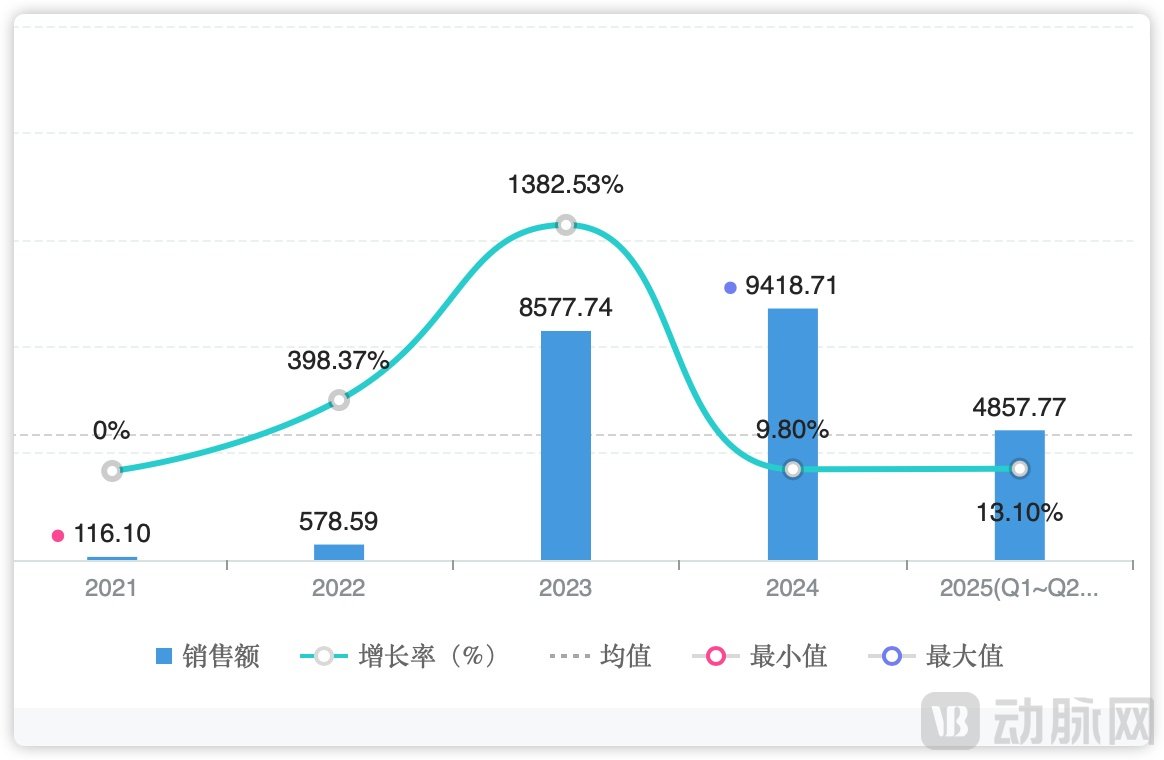

As prices declined, sales of oseltamivir subsequently showed signs of recovery. However, in 2021, Roche introduced baloxavir marboxil (Xofluza) to the Chinese market, where it successfully obtained regulatory approval. Leveraging its differentiated advantages—single-dose administration and significant symptom relief within 24 hours—the drug rapidly gained market traction. Its annual sales surged from RMB 300,000 in 2021 to RMB 700 million in 2024, with year-on-year growth rates reaching 759% in 2023 and 39% in 2024.

Xofluza Sales Surge Rapidly in Brick-and-Mortar Pharmacies, Image Source: Mordor Intelligence

Xofluza’s robust market growth has also been driven by its inclusion in the national medical insurance scheme. Eight months after approval, Xofluza was added to the National Reimbursement Drug List, with its price dropping from nearly RMB 500 to just over RMB 200. Meanwhile, in 2023, Roche expanded the indications for baloxavir marboxil to include pediatric influenza patients aged 5 to 12 years and obtained approval for a dry suspension formulation specifically developed for children. This formulation allows parents to administer precise doses based on their child’s body weight, while the strawberry flavor designed for children significantly improves the medication experience and enhances treatment adherence. Furthermore, Xofluza’s household prophylaxis regimen can effectively reduce the intra-household influenza infection rate from 54.45% to 6.93%, and shorten the duration of symptoms from 1.14 days to 0.11 days. These factors have all contributed to the rapid market acceptance of Xofluza.

According to the official website of the National Medical Products Administration (NMPA), two domestic companies, CSPC Pharmaceutical Group and Zhengzhou Taifeng Pharmaceutical, have already obtained production approvals for baloxavir marboxil tablets, while Zhejiang Puli Pharmaceutical and Shanghai Pharmaceuticals are currently under review for their production applications. Additionally, data from PharmCube indicates that there are 20 clinical trial records for baloxavir marboxil in China, involving companies such as Wellman Pharmaceutical, Mingrui Pharmaceutical, and Lamei Pharmaceutical. The development trajectory of oseltamivir appears to be repeating itself with baloxavir marboxil. However, this time, competition comes not only from generic drugs but also from domestically developed innovative drugs.

The ability to rapidly scale up sales volume during the window period is key to the success or failure of domestically produced new influenza drugs.

Given the annual seasonal epidemics of influenza A and B viruses, with influenza A also capable of causing global pandemics, the influenza therapeutic sector offers high certainty. Furthermore, as the structure and infection mechanisms of influenza viruses are relatively well understood, RNA polymerase inhibitors have become the mainstream direction in the development of small-molecule anti-influenza drugs. Compared with major disease areas such as oncology and autoimmune disorders, even companies with relatively limited financial and R&D capabilities can identify breakthrough opportunities. From another perspective, however, this market does not present sufficiently high barriers to entry; if a product fails to achieve rapid volume growth within a certain window period after approval and launch, it may face significant competition from later entrants.

Historically, market acceptance of a new drug depends not only on its efficacy but also on multiple factors, including market access, pricing, target population coverage, distribution channels, and production capacity.

First, regarding price: the selling prices of Yisuda, Anruiwei, and Jikeshu on e-commerce platforms all exceed 300 yuan. Currently, the terminal price of Xofluza is only around 220 yuan, while oseltamivir is even lower, with a per-course cost of merely about 30 yuan.

Of course, more importantly, the push from national medical insurance reimbursement is critical. Currently, both Yisuda and Anruiwei have passed the formal review for inclusion in the 2025 National Reimbursement Drug List (NRDL). Due to its later approval date, Jikeshu will have to wait until next year. In early November, the NRDL price negotiations concluded, with specific results expected to be announced in early December. If these products are ultimately included in the NRDL, it will further accelerate the reshaping of the market landscape. Based on product pricing and the price reduction seen when Xofluza was previously included in the NRDL (over 50%), the post-reimbursement prices of the two new drugs are expected to fall within the RMB 100 range, just below Xofluza’s RMB 220, thereby creating differentiated competition.

Next is the difference in population coverage. Within family units, children are a highly susceptible group for influenza. Pediatric patients not only experience longer disease courses and prolonged viral shedding but also easily trigger cluster infections in settings such as schools and classrooms. Therefore, children face a higher risk of influenza virus infection than adults and are a key target for prevention and control; consequently, the ability to cover the pediatric population is a major reference indicator for influenza medications. In terms of approved indications, apart from Qingfeng Pharmaceutical’s Yisuda, which covers adolescents aged 12 years and older, the other two new drugs are currently indicated only for adults.

Fortunately, several companies have recognized this. Qingfeng Pharmaceutical stated that it will continue to advance clinical studies of Yisuda in children, for influenza prevention, and among high-risk populations, while optimizing drug formulations to precisely meet the needs of different patients. Zhongsheng Pharmaceutical also revealed at an investor conference that Anruiwei had completed Phase II clinical trials for treating uncomplicated Influenza A in patients aged 2 to 17 years, achieving positive results in both efficacy and safety, and that the company will proceed with organizing Phase III clinical trials.

Finally, regarding distribution channels and production capacity, Qingfeng Pharmaceutical, Zhongsheng Pharmaceutical, and Jichuan Pharmaceutical are all established pharmaceutical companies with decades of history, boasting mature sales teams and distribution networks. Jichuan Pharmaceutical and Zhongsheng Pharmaceutical both started with traditional Chinese medicine (TCM) products; for instance, the former’s Pudilan Anti-inflammatory Oral Liquid and the latter’s Zhongsheng Pills and Naoshuantong Capsules are all supported by strong grassroots market penetration driven by their excellent sales teams.

Production capacity is also critically important. The initial shortage of the original oseltamivir brand and the rapid rise in market share of Dongyangguang Pharmaceutical’s Kewei were both driven largely by production capacity. In terms of business model, both Qingfeng Pharmaceutical and Zhongsheng Pharmaceutical possess the advantage of integrated API and finished dosage form manufacturing, enabling effective cost control and capacity management.

Overall, domestically developed innovative influenza drugs have taken a solid step forward. Although Roche looms ahead, numerous competitors flank both sides, and a host of oseltamivir generics trail behind, Chinese-made innovative drugs are currently bearing fruit across various fields.