After Stagnation, Huimin Insurance Finds New Payers

It’s insurance renewal season again.

Many long-time users have noticed that the buzz around Huiminbao (city-specific supplementary medical insurance) has significantly diminished this year compared to previous years, with the once-ubiquitous marketing campaigns and referrals from friends and family nowhere to be seen. Consequently, willingness to purchase Huiminbao has become markedly polarized. Healthy individuals show weak intent to renew their policies and may miss the enrollment window while hesitating, whereas individuals with pre-existing conditions demonstrate a strong willingness to enroll.

However, for the underwriters of Huiminbao (city-specific supplemental medical insurance), adverse selection—characterized by healthy individuals dropping coverage while those with pre-existing conditions enroll—is far from desirable. Behind this sudden chill, the once-sought-after Huiminbao has quietly embarked on a phase of market consolidation.

Gross Margin Cliff

Upon closer examination, the precipitous decline in the gross profit margin of Huiminbao (city-specific supplementary medical insurance) operations may have had the most direct impact. Faced with consecutive years of losses, this increasingly unprofitable business has become somewhat of a liability.

Looking back to around 2019, the unexpected surge in popularity of Huiminbao (city-specific inclusive commercial health insurance) sent shockwaves through both the commercial insurance sector and the innovative drug industry. Huiminbao, fully known as city-customized inclusive commercial health insurance, creatively demonstrated the feasibility of simultaneously addressing the differentiated needs of three distinct stakeholders: patients with pre-existing conditions, insurance companies, and pharmaceutical innovators.

For a time, Huiminbao initiatives—orchestrated by insurtech companies and integrating insurers with pharmaceutical firms—blossomed across various regions.At the height of its initial popularity, the gross profit margin for Huiminbao insurance products reached as high as 90%.Within the business landscape of insurtech companies, the primary payers for Huiminbao (city-specific supplementary medical insurance) services are insurance carriers and pharmaceutical companies. When dealing with insurance carriers, insurtech firms typically wield greater bargaining power, resulting in higher gross margins for their insurance service modules, whereas the gross margins for their pharmaceutical company service modules are relatively lower. According to the prospectuses of insurtech enterprises, the comprehensive gross margin for Huiminbao businesses has peaked at nearly 90%.

In this process, Huimin Bao has rapidly emerged as a hot investment track in the primary market. According to statistics from the VCBeat Orange Database, since 2021, over RMB 20 billion has flowed into several domestic innovative companies engaged in Huimin Bao-related businesses, with top-tier investors such as Sequoia China, Qiming Venture Partners, IDG Capital, and 5Y Capital among their backers. Since 2022, leading Huimin Bao innovators have sequentially initiated IPO filings.

Initially, the biggest selling point of Huiminbao (city-specific supplemental medical insurance) was to provide individuals with pre-existing specific conditions an opportunity to purchase commercial medical insurance. In the context of traditional commercial health insurance, these individuals are defined as non-standard risks and are often denied coverage. This means that through Huiminbao, pharmaceutical companies can compliantly reach end-users.

Since 2018, the pace of approval and market launch for new and specialty drugs has accelerated. While these medications have filled clinical gaps, their treatment costs often exceed the financial capacity of ordinary households due to a lack of medical insurance coverage. Huiminbao (city-specific supplementary medical insurance) offers an innovative payment solution for these high-priced new and specialty drugs.

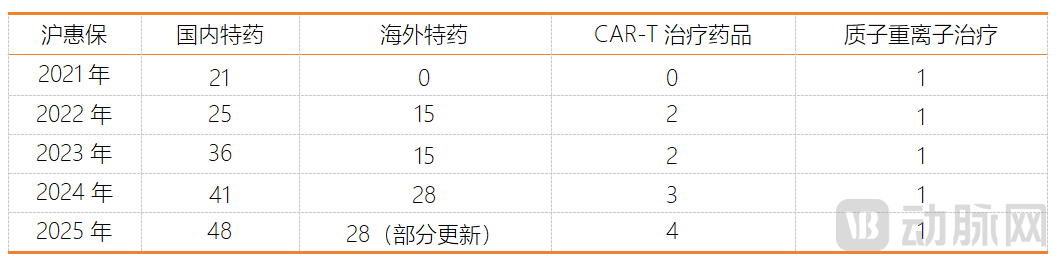

In Huiminbao (city-specific supplemental medical insurance), clauses covering expenses outside the basic medical insurance scheme are typically positioned as core benefits. Taking "Hu Hui Bao" in Shanghai, which has the largest number of insured participants in China, as an example, its coverage primarily focuses on out-of-pocket expenses not reimbursed by basic medical insurance. This includes benefits for specific inpatient out-of-pocket medical costs, domestic specific high-cost drugs, proton and heavy ion therapy, overseas special drugs, and CAR-T therapy drugs. Since its launch in April 2021, Hu Hui Bao has undergone multiple iterations of its coverage terms, with a key component being the regular update of the list of covered new and special drugs. In the 2025 version of Hu Hui Bao, the reimbursement scope already includes 48 domestic special drugs, 15 overseas special drugs, 4 CAR-T therapy drugs, and proton and heavy ion therapy.

However, constrained by the law of large numbers in insurance, Huimin Bao will not significantly boost the volume growth of the new specialty drug market.Coupled with the very limited medical resources that can be leveraged, Huiminbao’s bargaining power vis-à-vis pharmaceutical companies has further diminished. Meanwhile, as enrollment in Huiminbao plans shrinks year by year, insurers’ negotiating leverage is also waning. VCBeat has noted that,Since 2024, the comprehensive gross profit margin of the Huiminbao business for various insurtech companies has been compressed to around 50%.

Beneath the precipitous drop in gross profit margins, early-stage insurtech companies began to scale back their Huiminbao operations. The Huiminbao market consequently cooled down.

The Shift in Huiminbao

As previously mentioned, over the years, Huimin Bao (city-specific supplementary medical insurance) has experienced adverse selection, characterized by the exit of healthy individuals and the entry of those with pre-existing conditions. By analyzing hundreds of Huimin Bao products currently on sale or discontinued in China, VCBeat has found that the product logic of Huimin Bao is shifting. Retaining healthy individuals has replaced the race for new customer acquisition as a more critical consideration for insurers when designing these plans.

Internal Adjustments: Multiple Regions Revise Deductibles and Reimbursement Ratios for Huiminbao, Directing More Claim Funds Toward Healthy Individuals.

On the one hand, directly reduce deductibles and increase reimbursement ratios.Early Huiminbao policies often featured high deductibles, offering low or zero deductibles only for expenses related to drugs listed in the special drug catalog. For instance, the previous Beijing Puhui Health Insurance stipulated an annual deductible of RMB 18,000 for employees covered by basic medical insurance and RMB 22,000 for residents under basic medical insurance for out-of-pocket expenses within the scope of medical insurance coverage. The annual deductible for self-paid expenses outside the scope of medical insurance coverage was even higher, reaching RMB 20,000.

Among these, out-of-pocket expenses within the scope of basic medical insurance refer to the portion exceeding the reimbursement ratio for covered drugs, while self-paid expenses outside the scope refer to costs incurred for non-covered drugs. For healthy individuals, the likelihood of annual out-of-pocket expenses exceeding RMB 18,000 or self-paid expenses exceeding RMB 20,000 is very low. In other words, due to high deductibles, Huimin Bao (inclusive commercial health insurance) is not truly inclusive. In the 2026 product iterations, Beijing adjusted the deductible for Huimin Bao to RMB 15,000 in out-of-pocket expenses for healthy individuals, with a 25% reimbursement rate for the portion between RMB 15,000 and RMB 30,404, and an 80% reimbursement rate for amounts above RMB 30,404 after settlement through critical illness insurance. For self-paid expenses outside the scope of basic medical insurance, the deductible is set at RMB 5,000 for healthy individuals and RMB 15,000 for those with specified pre-existing conditions, provided they have been continuously insured for three years without any claims, thereby directly lowering the claim threshold for healthy individuals. In addition to Beijing, new versions of Huimin Bao in Shandong, Hunan, Hainan, and other regions have made similar adjustments.

On the other hand, simplify the rules for fee calculation.VCBeat has observed that in 2026, many regions have merged the deductibles for expenses covered and not covered by basic medical insurance into a single calculation. For instance, Hunan Yihuibao has adjusted its deductible structure from RMB 16,000 for inpatient expenses within the policy scope and RMB 15,000 for those outside the policy scope to a unified deductible of RMB 15,000 for all inpatient expenses, thereby consolidating two claim thresholds into one. Similarly, Chongqing Yukuaibao no longer distinguishes between expenses inside and outside the national medical insurance catalog, settling claims based on the total medical costs for hospitalization and special disease outpatient services. Notably, Hunan Huiqiongbao has introduced a dynamic deductible adjustment mechanism: for policyholders who did not file any claims in the previous year, the deductibles for both covered and non-covered responsibilities are reduced by RMB 1,000 each; conversely, for those who filed claims, the deductibles increase by RMB 1,000. This approach tilts the claims policy in favor of healthier individuals.

In addition, some Huiminbao plans have layered critical illness insurance features on top of medical insurance, providing enhanced protection for healthy individuals. For instance, the Zibo Qihui Bao stipulates that insured individuals who have purchased supplemental coverage will receive a one-time payment of RMB 10,000 to 20,000 upon their first diagnosis of malignant cancer during the policy period, with the specific amount varying by age group.

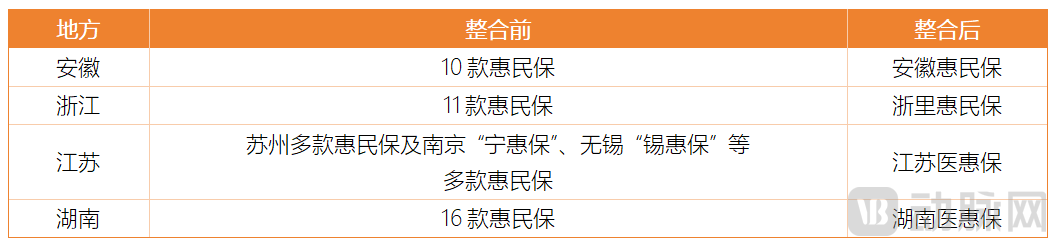

External Adjustments: The Land Grab for Local Supplemental Health Insurance Has Largely Concluded, with Cost Compression in Distribution Channels Becoming the Trend.Historically, policyholders often had to choose among multiple “Huimin Bao” (inclusive commercial health insurance) products. For instance, prior to consolidation, Suzhou had three such plans on the market, offering largely similar coverage. This homogenized competition undoubtedly increased insurers’ customer acquisition costs, which also explains why Huimin Bao campaigns were previously ubiquitous and why insurtech companies enjoyed high gross profit margins.

Since 2022, various regions have successively consolidated multiple “Huiminbao” (inclusive commercial health insurance) products into single provincial-level offerings. In 2022, Zhejiang Province issued policies aiming to achieve provincial-level pooling for the “Zhe Li Huimin Bao” by the end of 2024. Previously, each of Zhejiang’s 11 prefecture-level cities had its own Huiminbao product, with varying product names, funding mechanisms, and reimbursement rules. This fragmented market increased the operational costs of Huiminbao. The consolidated “Zhe Li Huimin Bao” established uniform coverage scopes and funding standards, and implemented a “provincial + municipal” reimbursement list system. Additionally, in Suzhou, the previously coexisting “Su Kang Bao” and “Su Hui Bao” were merged into a single product in 2023, and Jiangsu Province also launched the provincially pooled “Jiangsu Yihuibao No. 1.”

In September 2024, Hunan Yihuibao was launched. Meanwhile, 16 products, including Changsha Huiminbao and Hunan Aiminbao, were discontinued, consolidating the market into a single provincial-level product. Also in 2024, Anhui integrated all ten of its fragmented Huiminbao products into the provincially coordinated Anhui Huiminbao, aiming to expand the insured population and enhance overall risk resilience through provincial-level coordination.

Of course, many provinces and cities still have multiple “Huiminbao” (inclusive supplemental health insurance) products operating in parallel. For example, in Henan Province, the provincial-level Zhongyuan Inpatient Supplemental Medical Insurance coexists with city-level plans such as Zhengzhou Yihuibao, Pingdingshan Huihebao, and Jiaozuo Huiminbao. In Shandong Province, the upgraded Xinminbao operates alongside city-level products including Qilubao, Qihuibao, and Jihuibao. In Shenzhen, two city-level plans—Shenzhen Huiminbao and Pengchengbao—are offered concurrently.

Overall, if the inclusiveness of previous Huiminbao (city-specific supplemental medical insurance) products was primarily reflected in their low pricing, current Huiminbao offerings focus on providing coverage to a broader population.

New Capital Inflows

In the past two years, another trend in Huiminbao (inclusive commercial health insurance) has emerged: offering supplementary riders alongside the main policy terms or introducing upgraded versions beyond the basic product. VCBeat has observed that among these layered coverage options, adding outpatient internet medical insurance has become mainstream. According to incomplete statistics from VCBeat, Huiminbao programs in multiple regions, including Jiaozuo, Chongqing, Jiangsu Province, and Dezhou, have covered outpatient expenses at internet hospitals by stacking benefits or upgrading coverage. Meanwhile, Shaoxing and Xiamen have directly integrated their platforms with internet hospital services.

Under the newly added outpatient coverage for internet hospitals, insured individuals are generally required to log in to the official Huiminbao platform, complete an online consultation, and obtain an electronic prescription. Medications are provided by internet hospitals designated by the Huiminbao platform, with corresponding expenses directly reimbursed. Typically, internet outpatient insurance features a zero deductible, supports 24/7 online consultations, offers home delivery of medications, and enables direct payment and expedited claims settlement. Different Huiminbao plans stipulate varying terms regarding the annual total number of reimbursements, the maximum reimbursement amount per visit, and the reimbursement ratios for initial and subsequent claims.

Taking Chongqing Yu Kuai Bao as an example, after the insured opts for the additional Internet Hospital Outpatient Medical Insurance at a premium of CNY 30 per year, they become eligible for a monthly quota of CNY 600 for outpatient medical services at internet hospitals. During the policy period, the insured can access the consultation page via the Chongqing Yu Kuai Bao WeChat service account, complete medical consultations at designated internet hospitals, and purchase eligible medications based on prescriptions issued by internet physicians. Within the coverage limit, medication expenses can be directly reimbursed in a one-stop manner according to the agreed reimbursement ratio. Specifically, for Chongqing Yu Kuai Bao’s internet hospital outpatient services, the initial reimbursement rate is 90%, while subsequent reimbursements are covered at a rate of 70%.

VCBeat’s research reveals that the designated online hospitals for various local Huiminbao (inclusive commercial health insurance) schemes are primarily managed by platforms such as Heyi Health, Ruizhe Health, Taozi Health, and Ali Health. Among these, Heyi Health’s online hospital is designated by the largest number of Huiminbao plans, including Jiaozuo Huiminbao, Zhenjiang Huiminbao, and Dezhou Huiminbao.

It is worth noting that these internet hospital platforms are all backed by robust pharmaceutical retail systems. Heyi Health, established in 2015, is an online pharmaceutical enterprise providing end-to-end services spanning healthcare, pharmaceuticals, and insurance. Its parent company has received investments from top-tier institutions such as Sequoia China, Tencent Investment, and Source Code Capital. ZhiLu Pharmacy, a subsidiary of Heyi Health, operates multiple chain pharmacies across China. Another major internet hospital platform, Ruize Health, secured RMB 10 million in investment from Yaoshibang in 2024. The Zhejiang Provincial Internet Hospital Platform, integrated with Shaoxing Yuehuibao, was developed by AliHealth.

With the entry of new major investors holding substantial pharmaceutical distribution resources, Huiminbao (city-specific supplemental medical insurance) is gradually evolving from a single supplementary payment channel into a more comprehensive national health service platform. However, the extent to which the transformed Huiminbao can provide inclusive health coverage remains to be verified over time.