Shandong Keyuan Pharma Announces Termination of $503 Million Acquisition of Hongjitang Pharmaceutical

On November 28, Shandong Keyuan Pharmaceutical issued an announcement terminating its major asset restructuring plan to acquire a 99.42% equity stake in Shandong Hongjitang for RMB 3.58 billion.The transaction, launched in October 2024, went through processes including trading suspension, disclosure of the preliminary plan, deliberation by the shareholders’ meeting, inquiries from the Shenzhen Stock Exchange, and clearance of antitrust review, but was ultimately terminated at a stage close to completion.

In this regard, Keyuan Pharmaceutical stated in its announcement that the termination of this transaction was a prudent decision made after comprehensive consideration of factors such as the overall market environment, and following full communication, careful analysis, and amicable negotiations with all relevant parties. There are no circumstances under which the Company or related parties need to bear liability for breach of contract. Currently, all business operations of Keyuan Pharmaceutical are proceeding normally. The termination of this transaction will not have a significant adverse impact on its existing production and operational activities, nor does it constitute any harm to the interests of the Company and its minority shareholders.

The restructuring report previously projected that revenue would increase by 276.34% following the acquisition.

Keyuan Pharmaceutical (Stock Code: 301281.SZ), established in 2004, is a leading enterprise in the niche segment of chemical active pharmaceutical ingredients (APIs) in China. The company specializes in the research and development, production, and sales of chemical APIs and their formulated preparations, with its product portfolio covering key therapeutic areas such as antidiabetic, anesthetic, cardiovascular, and psychiatric disorders. Its API products mainly include gliclazide, metformin hydrochloride, ropivacaine hydrochloride, and isosorbide mononitrate. Its chemical drug formulation products primarily include fluoxetine hydrochloride dispersible tablets, isosorbide mononitrate sustained-release tablets, and isosorbide mononitrate tablets. The company also engages in the business of certain intermediates, which are mainly exported to overseas markets.

Hongjitang is a time-honored Chinese brand established in 1907. In the television series *The Grand Mansion Gate*, the character Bai Jingqi, the young master of “Baicaoting,” establishes a pharmacy in Jinan. Bai Jingqi is based on Le Jingyu, the founder of Hongjitang, and the pharmacy he founded is Hongjitang. Hongjitang’s product portfolio covers proprietary Chinese medicines, formula granules, Chinese herbal decoction pieces, active pharmaceutical ingredients (APIs), donkey-hide gelatin (Ejiao), and health foods. Among these, products such as Guanxin Suhe Pills, Shihu Yeguang Pills, and Liuwei Dihuang Pills have received the National Silver Quality Award from China. Products including Houzheng Pills, Compound Xiling Jiedu Tablets, Chufengjing, Hailong Gejie Oral Liquid, Ying’er’an Tablets, and Yinqiao Jiedu Pills have been awarded ministerial- and provincial-level high-quality designations. Eight products—Xiao’er Xiaoshi Tablets, Jinming Tablets, Qianliexin Capsules, Hailong Gejie Oral Liquid, Kangjun Xiaoyan Tablets, Xiongdan Jiuxin Pills, Kangshuan Zaizao Pills, and Compound Xiling Jiedu Tablets—are listed as Nationally Protected Traditional Chinese Medicine Varieties.

From a conventional perspective, both companies operate within the pharmaceutical industry, with their businesses being coordinated and complementary. If this acquisition is successfully completed, it would constitute a “strong alliance” that “combines Chinese and Western strengths.” Specifically, this acquisition transaction has three positive impacts:

First, integrate high-quality proprietary Chinese medicine assets to build a comprehensive healthcare platform:Keyuan Pharmaceutical is a chemical drug enterprise, while Hongjitang is a traditional Chinese medicine (TCM) enterprise with strong brand advantages and sales channel resources. Upon completion of this transaction, Keyuan Pharmaceutical will be able to extend its core business into areas such as proprietary Chinese medicines, health products, and muscone, thereby facilitating the creation of a large-scale, highly reputable pharmaceutical and healthcare platform.

Secondly, enrich Keyuan Pharmaceutical’s product portfolio to enhance its risk resilience and market competitiveness:Keyuan Pharmaceutical’s main products include gliclazide, metformin hydrochloride, ropivacaine hydrochloride, and isosorbide mononitrate. While terminal demand for these products remains relatively stable, the scale and technological capabilities of potential industry entrants are continuously improving, which may lead existing companies to lower prices and expand production capacity, resulting in intense market competition. However, Hongjitang is a time-honored Chinese brand in traditional Chinese medicine (TCM). It holds 150 drug approval documents covering various therapeutic areas, including cardiovascular and cerebrovascular diseases, colds and inflammation, throat and oral conditions, digestive system disorders, and urinary system disorders. Among its portfolio are seven exclusive drug varieties, such as Jinming Tablets, Qianliexin Capsules, and Shexiang Xintongning Tablets, as well as two exclusive dosage forms, including Compound Xiling Jiedu Capsules. Its characteristic products, such as donkey-hide gelatin (Ejiao), Angong Niuhuang Wan, and muscone, have accumulated long-standing market recognition and a strong reputation. Through internal resource integration within the group, Keyuan Pharmaceutical can incorporate these exclusive products into its portfolio, thereby enhancing its risk resilience and market competitiveness.

Third, leverage industrial synergy advantages to enhance Keyuan Pharmaceutical's profitability and asset scale:Keyuan Pharmaceutical’s finished chemical drug business started relatively late, and its market recognition and sales channels need further strengthening. As a century-old brand, Hongjitang boasts extensive network coverage across retail pharmacies, pharmaceutical distribution, and hospitals, along with an experienced sales team that can further enhance Keyuan Pharmaceutical’s sales capabilities. Furthermore, as both companies operate in the pharmaceutical manufacturing industry, this transaction will enable synergistic complementarity in R&D, production, procurement, and daily management, facilitating centralized production and office operations as well as joint procurement to reduce operating costs.

According to the restructuring report released by Keyuan Pharmaceutical, it is projected that, excluding the funds raised through matching offerings, the company’s operating revenue will increase by 276.34% and the net profit attributable to shareholders of the parent company will rise by 177.86% in 2024 upon completion of the transaction. Why did this win-win acquisition fall through at the final stage? Is the truth really as stated: “Given certain changes in the overall market environment compared to the initial planning phase of this restructuring, and in order to safeguard the long-term interests of all shareholders”?

Three Factors Leading to the Failure of "Integrating Chinese and Western Medicine"

In fact, numerous factors lie behind the termination of this acquisition.

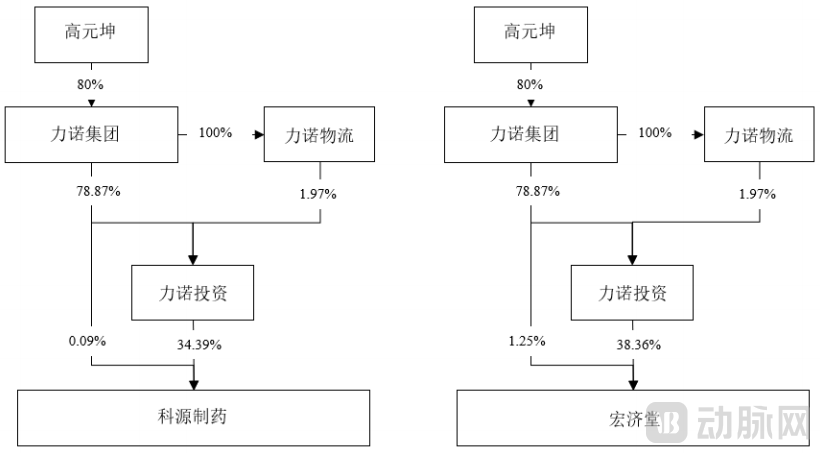

First, the regulatory authorities had repeatedly inquired about the necessity of the transaction and whether there was any benefit transfer.In fact, both Keyuan Pharmaceutical and Hongjitang are enterprises under the control of Gao Yuankun, the former richest man in Jinan and head of the “Linuo Group.” Furthermore, this merger and acquisition involves 38 related-party transaction counterparts, including Linuo Investment and Linuo Group. Although the company has adjusted the scale of supporting financing, the lock-up period, and performance compensation clauses, challenges such as the difficulty of coordinating multiple transaction parties and stringent compliance requirements for related-party transactions persist.

Keyuan Pharmaceutical’s Shareholding Structure, Hongjitang’s Shareholding Structure

Keyuan Pharmaceutical’s Shareholding Structure, Hongjitang’s Shareholding Structure

Second, Keyuan Pharmaceutical’s performance has declined; if this transaction is completed, its asset-liability ratio will increase significantly.In the first three quarters of this year, Keyuan Pharmaceutical witnessed a decline in both its operating revenue and net profit attributable to shareholders. Its third-quarter financial report revealed that the revenue for the first nine months amounted to approximately RMB 303 million, representing a year-on-year decrease of 8.52%; the net profit attributable to shareholders stood at approximately RMB 31.4707 million, marking a year-on-year drop of 20.69%. Should this transaction be successfully completed, Keyuan Pharmaceutical’s earnings per share (EPS) would decrease by 7.39%, its current ratio would decline by 69.04%, and its asset-liability ratio would increase by 28.55 percentage points.

Third, Hongjitang’s financial position is also unstable; its earnings volatility and high debt ratio may exacerbate the operational risks of Keyuan Pharmaceutical.Although Hongjitang holds over 150 drug approval numbers, its capacity utilization rate has declined significantly. In 2024, the capacity utilization rates for muscone, donkey-hide gelatin (Ejiao), and Angong Niuhuang Wan were 73.38%, 38.36%, and 72.81%, respectively, marking a substantial decrease from 108.47%, 106.8%, and 75.16% in 2023. Furthermore, between 2017 and 2019, its revenue fluctuated between RMB 467 million and RMB 515 million, while the gross profit margin declined annually from 74.5% to 57.29%, demonstrating a trend of “revenue growth without corresponding profit growth.” The company’s asset-liability ratio has consistently remained above the industry average; if integrated into Keyuan Pharmaceutical, it would significantly increase financial leverage and liquidity risk.

In summary, the termination of this acquisition, ostensibly attributed to the conventional rationale of “changes in market conditions,” is in essence the result of multiple factors, including volume-based procurement policies, regulatory policies, and corporate operational considerations.In fact, as early as 2019, the “Linuo Group” had planned to list Hongjitang and Keyuan Pharmaceutical on the A-share market through a backdoor listing, but the effort ultimately fell through. In 2021 and 2024, Hongjitang underwent IPO tutoring twice, only for both attempts to fizzle out. After these repeated setbacks, can Hongjitang “grow stronger with each challenge” and successfully enter the capital market with the joint support of companies within the Linuo Group and across its industry chain? Only time will tell.