InxMed Limited aims for IPO again, holding China's only phase III FAK inhibitor

InxMed

Tumor New Drug Developer

On April 21, InxMed Limited has once again submitted an application for listing on the Main Board of the Hong Kong Stock Exchange, with CITIC Securities and CCB International as joint sponsors.

InxMed has chosen a path different from most Biotech companies — instead of crowding into popular targets, it focuses on the "post-resistance" market. Its Core product Ifebemtinib (IN10018), a highly selective FAK inhibitor,is currently the only product in its domestic sector to have entered Phase III clinical trials.

Only one step away from commercialization, can InxMed leverage the capital market to complete this "final push"?

1HKEX 18A Warms Up, Differentiated Targets Gain Attention

In 2025, a total of 16 unprofitable Biotech companies in the Hong Kong stock market went public through Chapter 18A, raising over 13.7 billion Hong Kong dollars in total, accounting for 47.06% of the sector's total fundraising amount, becoming the main force of financing. Compared with only four companies going public under this rule in the same period of 2024, the growth was significant.

But in the recovery, the differentiation is also obvious. Investors are no longer buying into "stories" but are paying more attention to clinical progress, track scarcity, and clarity of commercialization pathways. InxMed happens to be at the intersection of these elements.

Since its establishment, InxMed has consistently focused on the unmet clinical need of tumor drug resistance. Its core strategy is clearly defined as "using FAK inhibitors as the cornerstone to build a dual-driven pipeline of combination therapies and ADCs." As a typical target under Chapter 18A, InxMed has yet to achieve commercial revenue. Its core value lies in the clinical progress of its pipeline and the rarity of its niche — the key product, Ifebemtinib, is the only highly selective FAK inhibitor in China to have entered Phase III clinical trials.

The validation from the capital market has already taken place. Prior to filing, InxMed had completed six rounds of financing, accumulating approximately 929 million RMB in total. Investors included SDIC Capital, Fosun Health Capital (under Fosun), I-Bridge, and others. Among these, the Series C financing round completed in August 2025 was particularly crucial — with an inflow of about 33.7 million USD, the company's post-money valuation was set at 306 million USD, becoming the core valuation anchor for this IPO.

According to the use of proceeds disclosed in the prospectus, the funds will be used for the Phase III clinical trial and NDA submission of Ifebemtinib, as well as for the development of early pipelines, commercialization preparation, and daily operations. This arrangement clearly points to one goal: to accelerate the market launch of the core product.

2FAK Inhibitor, a "Blue Ocean" Validated by Verastem

InxMed's core confidence stems from the precise judgment of the track — focusing on FAK inhibitors, directly addressing the core clinical pain point of tumor drug resistance. This track is on the verge of a boom, with enormous market potential.

In the field of cancer treatment, drug resistance is the primary challenge that limits therapeutic efficacy. Particularly in highly prevalent cancers such as ovarian cancer, non-small cell lung cancer (NSCLC), and colorectal cancer (CRC), the issue of resistance to traditional chemotherapy and targeted therapy is prominent, creating an urgent clinical need.

FAK (Focal Adhesion Kinase), as a non-receptor tyrosine kinase, is a regulatory hub in the tumor microenvironment. It not only regulates tumor cell proliferation and migration but also participates in angiogenesis and immune suppression, making it a key breakthrough point for tumor drug resistance. Inhibiting FAK activity can simultaneously achieve three major effects: improving the tumor microenvironment, enhancing drug penetration, and increasing tumor cell sensitivity, making it an ideal cornerstone for combination therapy.

In May 2025, Verastem Oncology's Defactinib was approved by the FDA for marketing, becoming the world's first selective FAK inhibitor. This is not only a milestone in the field but also validates the clinical value of FAK inhibitors.

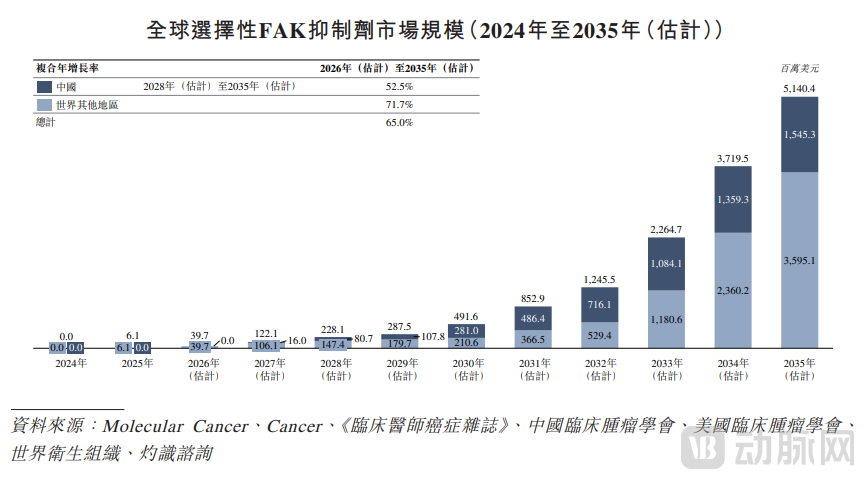

How large is the track space? According to the prospectus and industry data forecasts, the global selective FAK inhibitor market will reach 5.14 billion US dollars in 2035, with a compound annual growth rate of 65.0% from 2026 to 2035. The growth rate in the Chinese market is even more significant, with an expected compound annual growth rate of 52.5% during the same period, reaching 1.545 billion US dollars in scale by 2035.

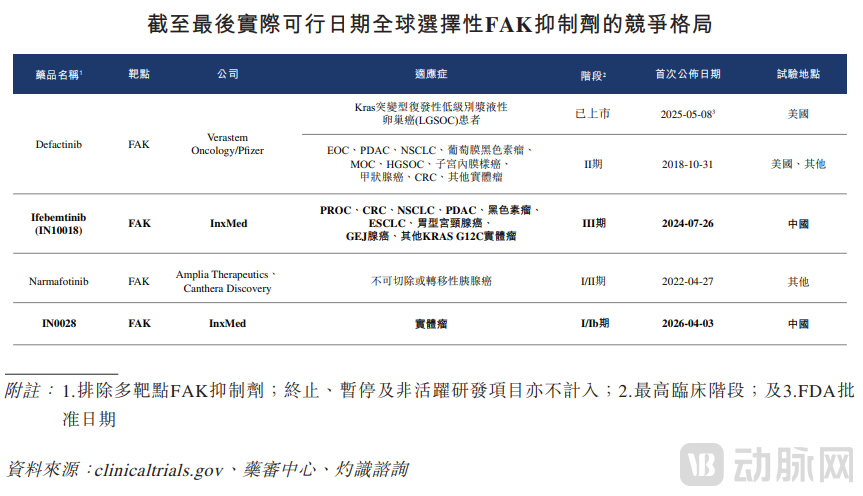

More importantly, this track is still a "blue ocean" at present. Globally, only four selective products are in clinical development, among which only Defactinib has been approved for marketing. In China, InxMed's Ifebemtinib is the only product that has entered Phase III clinical trials, leading domestic pharmaceutical companies such as BeOne Medicines and Hengrui by at least 2-3 years.

InxMed has a clear differentiation strategy: focusing only on combination therapies, not single-agent treatments. This approach sets it apart from other companies' "single-agent plus combination" layouts, avoiding the limitation of single-agent efficacy while building a unique competitive barrier.

3Core Product in Phase III Clinical Trials, Three Breakthrough Therapy Designations

The track logic is established, and the next thing to look at is: Where has InxMed's product reached?

Ifebemtinib (IN10018) is the core asset of InxMed and a benchmark product in China's FAK inhibitor field. It has received three Breakthrough Therapy Designations from the NMPA and one Fast Track designation from the FDA.

This highly selective oral small-molecule FAK inhibitor was acquired global rights from Boehringer Ingelheim in 2017 and has been independently advanced in clinical development by InxMed. Its core value lies in specifically inhibiting FAK kinase activity to improve the tumor microenvironment, enhance drug penetration, increase tumor cell sensitivity to combination therapies, and ultimately achieve synergistic anti-cancer effects.

In terms of clinical progress, the indication for platinum-resistant ovarian cancer is closest to commercialization, with Phase III clinical trials currently underway. An NDA is expected to be submitted in the second half of 2026 — if all goes well, it will become China's first marketed FAK inhibitor. In addition, the company has a broad layout in KRAS mutation-related cancers (such as non-small cell lung cancer and colorectal cancer), with multiple indications in Phase II/III. Key data will be read out from the second half of 2026 to 2027, representing an even larger market potential.

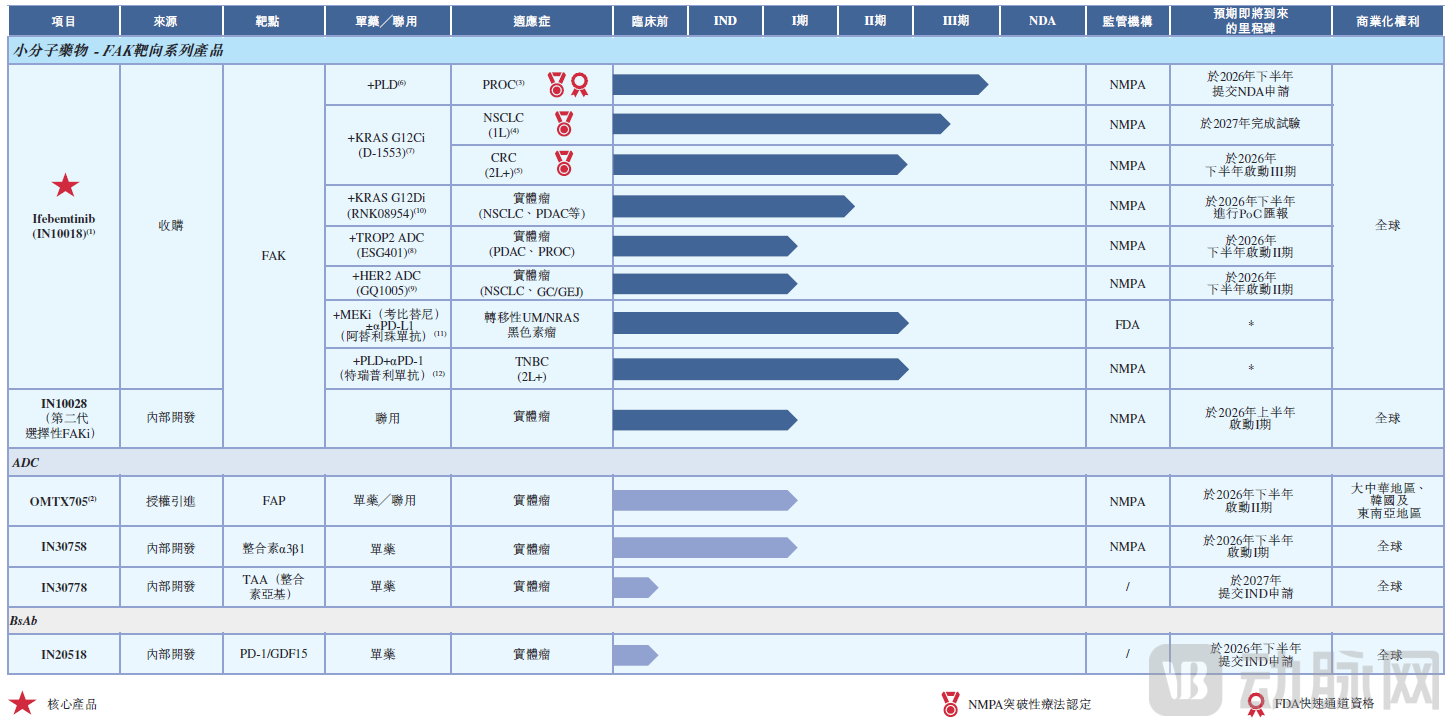

Core Products and Pipeline

To reduce reliance on a single product, InxMed has also built a diversified pipeline around tumor resistance: the Phase I clinical trial of the second-generation FAK inhibitor IN10028 has been initiated as an early strategic move; three ADC products cover different solid tumors, among which OMTX705 is the most advanced, having entered Phase II; InxMed expects to submit an IND application for the bispecific antibody IN20518 (PD-1/GDF15) in the second half of 2026, with its differentiation lying in simultaneously fighting tumors and improving cancer cachexia.

Overall, Ifebemtinib is InxMed's core asset at present, while other pipelines represent extensions and defensive strategies across different mechanistic dimensions. Every investment aims at the same goal—occupying as many ecological niches as possible in addressing the vast and complex clinical issue of tumor drug resistance.

4Financial Stability: Stable R&D Investment, Backed by Star Shareholders

As a non-profitable Biotech, InxMed exhibits a research-driven and continuously investing feature, relying on multiple rounds of financing and institutional endorsements to provide assurance for clinical advancement and pipeline expansion.

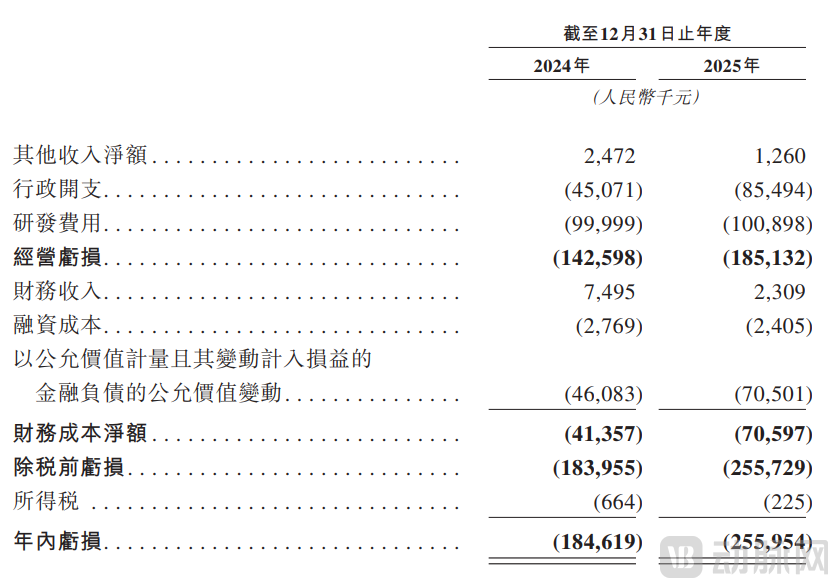

According to the prospectus, the company's R&D expenses were RMB 100 million in 2024 and RMB 101 million in 2025, remaining largely stable and reflecting the strategic orientation of "R&D first." Net losses for the same periods were RMB 185 million and RMB 256 million, respectively, with an accumulated loss of RMB 441 million. The widening of the loss was mainly attributable to changes in the fair value of preferred shares, rather than a deterioration in operating performance.

As of the end of 2025, InxMed's cash and equivalents amount to 210 million RMB. The prospectus disclosed that the existing cash can cover at least 125% of the funding needs for the next 12 months, which means there is no short-term liquidity pressure, the cash reserve is sufficient, and the sustainability of funds is strong.

In terms of liability structure, the net liability of RMB 981 million recorded on the books mainly stems from financial liabilities arising from preferred share financing, rather than operating liabilities, and does not affect daily operating cash flow. InxMed's bank borrowings are only RMB 64 million, and trade payables are RMB 46 million, indicating that current liabilities are manageable and short-term solvency is strong.

In terms of shareholder structure, the acting-in-concert parties (Wang Zaiqi, Cao Fei, etc.) hold 26.51%, making them the single largest shareholder group. Core institutional shareholders include: SDIC Capital (10.51%), Fosun Health Capital (8.97%), and I-Bridge (8.66%). This combination of "professional healthcare funds + industrial capital" provides the company with financial support and also reserves space for future commercial collaborations and strategic integration.

5The Next Step for InxMed: A Late-Stage Biotech Breakthrough

InxMed's IPO journey is not only its own capital challenge but also reflects the development trend of China's innovative drug industry — late-stage clinical trials + niche market presence are becoming the core competitiveness of unprofitable Biotechs, while pipeline diversification + combination therapies are key to navigating cycles.

With the boom of the FAK inhibitor sector, InxMed's combination with KRAS inhibitors, ADC, and other therapies is expected to solve the challenge of tumor drug resistance, offering new options for patients while opening up broader market opportunities for innovative pharmaceutical companies.

If Ifebemtinib can successfully submit its NDA and gain approval for market launch in the second half of 2026, it will become China's first marketed FAK inhibitor, filling the gap in domestic drug resistance treatment for tumors. At that time, according to the prospectus forecast, its peak annual sales are expected to reach 2-3 billion RMB.

For the Hong Kong Stock Exchange's 18A sector, the addition of InxMed will also inject new vitality, becoming a valuation benchmark in the field of tumor drug resistance and providing a reference for more late-stage clinical biotech companies seeking an IPO path.

In the future, as clinical data continues to be collected and pipelines expand, InxMed is expected to secure a significant position in the global FAK inhibitor field, transitioning from research-driven development to commercial profitability. InxMed's next steps are worth watching closely.