United Imaging Rises to Second Place in China's Radiotherapy Market with Innovative Product Portfolio and Strategic Expansion

United Imaging

High-end Medical Device Developer

Over the past two years, domestically produced radiotherapy equipment has accelerated its market deployment, continuously capturing market share from imported products.

Among them, United Imaging, as an imaging giant, has also achieved remarkable results in the radiotherapy market. According to its 2024 annual report, United Imaging’s market share of radiotherapy equipment increased by nearly 8% year-on-year, ranking third in the industry and significantly narrowing the gap with the second-place competitor. However, data from multiple third-party research reports indicate that in 2024, United Imaging’s market share in the domestic medical linear accelerator segment (a major category within radiotherapy equipment)Surpassing international giant Varian to rank second。Medical linear accelerators constitute the core segment of the radiotherapy equipment market, accounting for over 90% of its total market share.Other radiotherapy equipment also includes medical light ion therapy systems, medical X-ray therapy devices, gamma beam teletherapy machines, brachytherapy afterloading devices, and radioactive seed implantation therapy systems.

According to United Imaging's financial report for the first half of 2025, its combined market share in medical imaging and radiotherapy equipment increased by 3.4% year-on-year,Market Share in China Rises to Second in the Industry. Although this data does not break down the market share of radiotherapy equipment separately, according to a report by Yi Gong Yan Xi She, United Imaging’s radiotherapy equipment business generated RMB 242 million in revenue in the first half of 2025, with its market share in China increasing by nearly 18 percentage points year-on-year, ranking second in the industry.

It is not only United Imaging; other domestic radiotherapy equipment manufacturers are also making concerted efforts to jointly promote the localization of radiotherapy equipment. Taking medical linear accelerators as an example, according to statistics from 5iRT:From 2020 to 2024, the market share of imported medical linear accelerators decreased from 88.7% to 68.69%, while that of domestic brands increased from 11.3% to 31.32%.。

(Market Share of Imported and Domestic Brands in China's Radiotherapy Equipment Market, 2020–2024)

The market share of domestic brands has risen rapidly, primarily because domestically produced medical linear accelerators have been successively approved and commercialized. For instance, Suzhou Lina Tech Medical Technology Co., Ltd.’s first medical electron linear accelerator was approved for market launch in 2021 and achieved commercial sales in 2022; SHINVA MEDICAL INSTRUMENT CO.,LTD.’s market share of medical linear accelerators increased from 2.82% in 2020 to 3.92% in 2024, peaking at 6.04% during this period.

In addition, the approval and market launch of domestically produced medical linear accelerators have also compelled imported products to continue reducing their prices.. Since 2020, the National Medical Products Administration (NMPA) has approved approximately 26 domestically produced medical linear accelerators, accounting for 52% of the total number of approvals. With the approval and application of domestic products, imported medical linear accelerators are no longer maintaining the high prices seen during their period of monopoly. From 2020 to 2024, the average winning bid price for imported brand medical linear accelerators decreased from RMB 27.35 million to RMB 26.01 million, showing a steady downward trend; meanwhile, the average winning bid price for domestic brands increased from RMB 18.35 million to RMB 20.35 million, indicating that domestic high-end radiotherapy equipment has achieved significant breakthroughs.

Nowadays, China's radiotherapy equipment market has transitioned from the first stage of import monopoly to the second stage, characterized by the accelerated adoption of domestically produced radiotherapy equipment and their direct competition with imported devices. In this new phase, how have domestically produced radiotherapy devices gradually captured market share? What new progress have Chinese radiotherapy enterprises made?

Domestic Radiotherapy Equipment Has Risen.

Taking United Imaging as an example, its independently developed world’s first integrated CT-linear accelerator was approved in 2018, and another conventional linear accelerator was approved in 2020. Since commercialization, the revenue from United Imaging’s radiotherapy equipment business has rapidly grown from RMB 9.0458 million in 2019 to RMB 318 million in 2024, with a compound annual growth rate (CAGR) of 104.37%. Its market share in China’s newly added linear accelerator market also increased from 7.34% in 2020 to 28.43% in 2024, surpassing Varian’s 24.51% share in 2024 to rank second in the industry.

(United Imaging's Radiotherapy Business Revenue and Its Linear Accelerator Market Share in China's New Installations)

2019–2024: In just six years, United Imaging rose from a market newcomer to the industry’s second-largest player. How did it achieve this?

First, breakthroughs in core technologies.United Imaging began its R&D layout for radiotherapy equipment in 2013. With support from the Ministry of Science and Technology, the National Development and Reform Commission/Shanghai Municipal Development and Reform Commission, and the Shanghai Municipal Science and Technology Commission, among other departments, it has taken the lead in undertaking multiple national and provincial-level R&D projects, such as “Precision Volumetric Modulated Arc Therapy Technology and Applications,” “Development and Industrialization of Internationally Advanced Medical Imaging and Radiotherapy Equipment,” “Clinical Trial Verification Project for CT Image-Guided Linear Accelerators,” and “Clinical Trial Research on Intelligent Contouring Workstations for Radiation Oncologists.”

Driven by strong policy support and massive R&D funding, United Imaging has gradually mastered core technologies in the field of radiotherapy, including accelerator tube technology, precise dose control systems, dynamic multileaf collimator (MLC) systems, integrated CT imaging technology, high-precision treatment couches with automatic deformation compensation technology, Monte Carlo dose calculation algorithms, and treatment planning optimization algorithms, securing a series of patents.

As of now, United Imaging has fully mastered the full-chain core technologies in the field of radiotherapy equipment, ranging from key core components such as accelerator tubes, multi-leaf collimators, and all-solid-state high-voltage modulators to radiotherapy software systems.

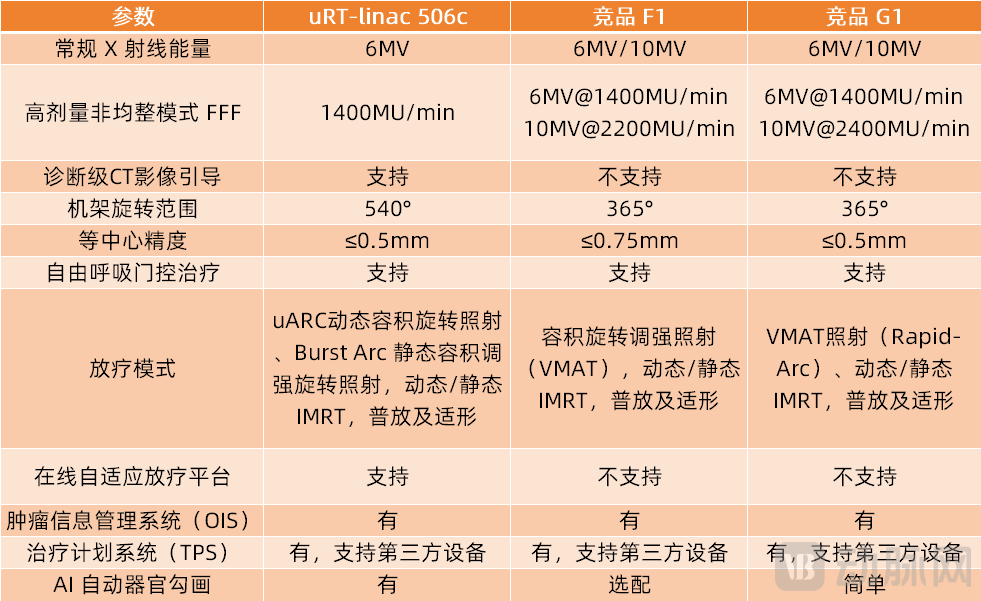

Secondly, the product offers differentiated advantages over imported equipment.During the product R&D phase, United Imaging recognized the gap between itself and the “big three” companies that dominate the global radiotherapy equipment market. In response, it chose a different path, leveraging its diversified strengths in imaging products to achieve breakthroughs in both products and technology through its proprietary CT-guided radiotherapy system. Under this strategy, United Imaging launched the world’s first integrated CT-guided linear accelerator, the uRT-linac 506c.

Compared to imported linear accelerators, this product integrates a diagnostic-grade CT with the accelerator. It is equipped not only with software technologies such as automatic contouring, automatic planning, and automatic quality control, but also provides a rapid workflow including online simulation, plan creation, and image guidance. In contrast to imported devices that do not support diagnostic-grade CT image guidance, this product enables physicians to customize treatment plans based on tumor pathology, significantly enhancing both radiotherapy efficacy and operational efficiency.

Meanwhile, in terms of technical specifications, United Imaging’s uRT-linac 506c linear accelerator is comparable to imported equipment and even surpasses it in certain metrics. For instance, the 6 MV photon energy of the uRT-linac 506c meets the requirements of most clinical scenarios; its gantry rotation range exceeds the 365 degrees offered by overseas competitors, reaching 540 degrees, thereby facilitating easier treatment of unilateral lesions; and its isocenter accuracy aligns with the latest products from multinational giants, achieving a precision of ≤0.5 mm, which is superior to the ≤0.75 mm precision of other products, thus ensuring greater accuracy during treatment.

(Comparison of Parameters between United Imaging’s uRT-linac 506c and Imported Products; Data Source: United Imaging’s Prospectus)

In addition to the uRT-linac 506c, United Imaging launched innovative products in 2024, including the uLinac HalosTx ring gantry linear accelerator, the single-photon large-bore CT linear accelerator uLinac EternaTx, and the new ultra-large-bore uCT 610 Sim, which integrates diagnostic CT scanning, radiotherapy simulation and localization, and image-guided interventional puncture procedures.

Among these, the uLinac HalosTx integrates a diagnostic-grade large-bore CT with a ring-shaped accelerator architecture. By combining a 4 RPM gantry rotation speed, a high dose rate of 1200 MU/min, and an MLC leaf speed of 6.5 cm/s, it achieves synergistic optimization of dose modulation precision and treatment efficiency, improving treatment efficiency by 50% compared to conventional equipment.

Driven by its pioneering design, superior performance, and clinical efficacy, United Imaging’s medical linear accelerator rapidly gained market recognition following its launch, with installations completed at numerous top-tier hospitals across China.

Ultimately, it was a victory of market strategy.For a long time, radiotherapy equipment has been primarily procured by Grade A tertiary hospitals in first-tier cities. These hospitals have relatively ample budgets and impose higher requirements on product quality, brand reputation, and performance. In response, United Imaging previously achieved breakthroughs in the high-end medical imaging equipment market through an “aiming high” strategy, earning consistent recognition from top-tier hospitals across China and building a strong reputation and brand image. By 2020, United Imaging’s products had already been installed in nearly 900 hospitals, with all of the top 10 medical institutions in China among its clients, and 49 out of the top 50 medical institutions also being its customers.

United Imaging has continued to refine its product portfolio in the field of radiation therapy. By 2024, its offerings had expanded to include simulation and localization systems, radiotherapy equipment, and radiotherapy software, making it one of the few suppliers in the industry to provide a comprehensive, closed-loop solution for radiation therapy.

Leveraging the reputation and brand established through its high-end imaging equipment, United Imaging has successfully entered China’s high-end radiotherapy equipment market by capitalizing on the performance advantages of its pioneering products and its product portfolio.。

Additionally, a major factor behind the significant surge in United Imaging’s market share is its breakthrough in lower-tier markets.In the past, radiotherapy equipment was primarily procured by Grade A tertiary hospitals in first-tier cities. However, since the implementation of the tiered diagnosis and treatment policy, the state has increased support for the county-level medical market. For instance, the "Work Plan for Enhancing the Comprehensive Capabilities of County Hospitals under the 'Thousand Counties Project' (2021–2025)," issued by the National Health Commission in 2021, explicitly stated that by 2025, at least 1,000 county hospitals nationwide should reach the service capacity level of tertiary hospitals. In August 2023, the National Health Commission released the "Equipment Configuration Standards for County-Level General Hospitals," which stipulated requirements for the types and quantities of equipment in county hospitals. Taking the radiology department of a hospital with 400–599 beds as an example, it is required to be equipped with one CT simulator and one set of radiotherapy treatment planning system software. Against this backdrop, procurement demand for radiotherapy equipment among county-level medical institutions continues to grow.

In contrast to multinational giants that focus on first-tier cities, United Imaging strategically anticipated the opportunities in lower-tier markets and made bold decisions.: Seizing industry trends in tiered diagnosis and treatment, primary healthcare development, and the domestic substitution of medical equipment, we have strengthened a three-dimensional marketing network by continuously establishing marketing service centers across China. Through market strategies such as “building distribution channels and strengthening primary care,” we meet policy requirements like the “Thousand Counties Project” and close-knit county-level medical communities, thereby promoting the decentralization of high-quality medical resources. By partnering with high-quality distributors and leveraging their regional penetration capabilities and rapid response times, we expand the breadth and depth of product coverage to drive sales growth. Furthermore, we have developed a mature after-sales service system that provides installation, repair, and maintenance services for our full range of high-end products, addressing the diverse needs of different customer segments.

Differing from the demands of Grade A tertiary hospitals in first-tier cities,County-level HospitalsWhen procuring medical linear accelerators, budgetary considerations are taken into account; rather than blindly pursuing high-end equipment, the focus is onMore inclined to enhance cost-effectiveness. United Imaging's conventional linear accelerator system, the uRT-linac 306, meets clinical needs while offering significant cost and pricing advantages, earning it strong market favor.

According to data from the High-End Medical Device Institute, the median winning bid price for United Imaging’s linear accelerators in the first three quarters of 2025 was RMB 22.684 million, lower than Elekta’s RMB 25.4 million, Varian’s RMB 24.8 million, and Accuray’s RMB 40 million. In comparison, United Imaging’s linear accelerator products offer a greater cost-performance advantage.

Beyond this, United Imaging has also proposed solutions to address issues such as the shortage of specialized professionals in county-level markets. By leveraging technologies like artificial intelligence, United Imaging has equipped its radiotherapy devices with intelligent features—including precise disease analysis, personalized treatment planning, and intelligent target volume delineation. These enhancements elevate the intelligence level of radiotherapy equipment, reduce operational complexity, improve the efficiency and quality of medical services, and alleviate the strain on medical resources.

By the end of 2024, United Imaging’s radiotherapy ecosystem network had covered more than 150 core medical institutions across China, successfully entering 70% of the leading national-level specialized cancer hospitals. With over 1.1 million precise radiotherapy treatments completed, the clinical value of its intelligent radiotherapy solutions has been validated, and related technological achievements have resulted in more than 90 high-level academic papers.

In addition, United Imaging has initiated a series of specialized alliances for high-quality development in collaboration with top-tier hospitals and experts, promoting talent cultivation and support for lower-tier hospitals. For instance, the Radiotherapy High-Quality Development Alliance, jointly launched by United Imaging, the Chinese Society of Clinical Oncology (CSCO) Radiation Oncology Branch, Fudan University Shanghai Cancer Center, and Sun Yat-sen University Cancer Center, will leverage multi-center collaboration to co-develop new radiotherapy products and facilitate talent training at the grassroots level.

It is perhaps United Imaging’s investment in the county-level market and its cost-performance advantage that have enabled its linear accelerators to win bids at numerous county-level medical institutions. According to incomplete statistics, as of December 10, 2025, United Imaging’s medical linear accelerators had won bids at 12 county-level hospitals, including Dengfeng City People’s Hospital, Chongzhou City People’s Hospital, and Suining County People’s Hospital, accounting for approximately 38.7% of its total successful bids this year.

(United Imaging Linear Accelerator 2025 Bid Winning Status, Incomplete Statistics)

In retrospect, United Imaging’s bold strategic foresight and its initiatives to penetrate lower-tier markets have yielded substantial returns. From 2020 to 2024, the proportion of radiotherapy equipment procurement by county-level hospitals in China rose from 22.25% to 30.48% of total procurement spending, outpacing the overall growth rate of hospital procurement nationwide. The rapid expansion of the county-level market has laid a solid foundation for the strong revenue growth of United Imaging’s radiotherapy equipment business.

In addition to the three major factors mentioned above, policy support is a key driver behind United Imaging’s rapid market penetration. For instance, multiple government departments jointly issued policies such as the “2024 High-End Medical Equipment Promotion and Application Project” and the “2025 High-End Medical Equipment Promotion and Application Project,” which support domestic radiotherapy equipment manufacturers—including United Imaging, SHINVA, Neusoft, Xi’an Dayi, and CNNC Anke—to accelerate innovation in high-end products and promote large-scale application of new technologies, new products, and new scenarios.

Beyond United Imaging, other domestic radiotherapy equipment manufacturers are also advancing along the paths of high-end development, intelligentization, and localization, while enhancing their competitiveness and capturing market share through new strategies.。

First, the number of approved domestically produced linear accelerators has surpassed that of imported ones. Domestic companies such as Neusoft Medical, Rui'er Medical, SHINVA MEDICAL INSTRUMENT CO.,LTD., Zhongneng Medical Accelerator, Huaming Putai, CNNC Accuray, Huachuang Medical, CAS Super Precision, Xi'an Dayi, Linico Medicine, Haibo Technology, Suzhou Lina Tech Medical Technology Co.,Ltd., and Daji Kangming have all launched linear accelerators.

As of the end of February 2025, the National Medical Products Administration (NMPA) had approved approximately 50 medical linear accelerators, including 15 imported products and 35 domestically produced ones, with domestic products accounting for about 70% of the total. Excluding localized products from Elekta and Varian, there were 26 approved medical linear accelerators from Chinese brands, representing 52% of the total.

Second, the accelerated market entry of domestically produced radiotherapy equipment has intensified competition in China's radiotherapy device market, forcing imported radiotherapy equipment manufacturers to lower prices to enhance competitiveness. The average winning bid price for imported medical linear accelerators has decreased from RMB 27.35 million in 2020 to RMB 26.01 million in 2024. In contrast, the average winning bid price for domestic brands has risen from RMB 18.35 million to RMB 20.35 million. With intensifying market competition and growing recognition of domestic brands, imported radiotherapy equipment is expected to see further price reductions.

Third, the commercialization of domestically produced radiotherapy equipment is accelerating. Following the intensive approval of domestic radiotherapy devices such as medical linear accelerators in the past two years, Chinese enterprises have gradually initiated their commercialization efforts. To date, companies including United Imaging Accuray (Zhongke Ankerui), SHINVA MEDICAL INSTRUMENT CO.,LTD., Lina Tech Medical (Leitai Medical), Xi’an Dayi, and Real Medical have all achieved commercial installations.

Meanwhile,Domestic EnterprisesPositiveAccelerate commercialization through medical-enterprise collaborations, and enhance brand influence via procedural innovations and landmark studies.For instance, Dayi Group signed a strategic cooperation agreement with West China Hospital of Sichuan University to jointly establish the “Joint R&D Center for Innovative Precision Radiotherapy.” The two parties focused on precision diagnosis and treatment of tumors, integrating artificial intelligence with real-world data to co-create the “West China Surgical Approach.” Meanwhile, Real Medical completed the clinical installation of its innovative product, the Real Knife, marking a critical step in the commercialization of domestically produced radiotherapy equipment.

Fourth, domestic companies have successfully conquered the field of radiotherapyUltra-High-EndProduct。In the field of radiation therapy, proton/heavy-ion radiotherapy systems are internationally recognized as cutting-edge technologies, offering clinical advantages such as high cure rates, superior precision, broad indications, and minimal side effects. Compared with conventional X-ray therapy, proton/heavy-ion therapy reduces the relative risk of severe side effects within 90 days post-treatment by two-thirds.

To date, only a handful of countries, including China, Germany, Belgium, the United States, and Japan, have mastered proton/heavy ion technology. Among them, three major players—IBA, Varian, and Hitachi—account for nearly 80% of the global market share. However, Chinese enterprises have achieved technological breakthroughs. For instance, in July 2025, Guoke Ion received a RMB 1 billion investment from Suzhou High-Tech Zone to establish the East China headquarters and R&D center for heavy ion medical equipment, thereby promoting the localization of high-end radiotherapy devices. Meanwhile, Maisheng Medical launched China’s first miniaturized, integrated single-room proton therapy system at the end of 2024.

Robotic radiosurgery systems are also at the forefront of radiation therapy technology. In this regard, Baiyang Pharmaceutical announced the commissioning and production launch of its high-end manufacturing industrialization base, which will produce the ZAP-X Mars Rover robotic radiosurgery system, a globally leading device for precise radiotherapy of brain tumors.

Furthermore, Chinese enterprises are also at the forefront globally in the field of Boron Neutron Capture Therapy (BNCT). For instance, the BNCT system HyBorSys, developed by Huaborg Neutron, has successfully completed medical device registration testing and entered the clinical trial phase. It is expected to commence Phase I clinical trials in early 2026 and begin enrolling patients in early 2028.

Boron Neutron Capture Therapy is a cutting-edge cancer treatment modality. Its principle involves the precise delivery of specific boron-containing drugs to cancer cells, followed by irradiation with a neutron beam to achieve targeted tumor destruction. The "micro-explosion" range of this therapy is confined to less than 10 micrometers, significantly sparing surrounding healthy tissues and demonstrating exceptional therapeutic precision and safety.

With the collective acceleration of domestically produced high-end radiotherapy equipment and the trend toward import substitution, the existing landscape of China’s high-end radiotherapy market is expected to undergo a new round of restructuring and reshuffling. During this period, domestically produced high-end radiotherapy equipment will become a significant force disrupting the market.

References:

"Analysis of the Domestic Accelerator Market (2020-2024)" — 5iRT

“Analysis of National Bid-Winning Data for Linear Accelerators in the First Three Quarters of 2025: Average Year-on-Year Growth Reached 48%” — High-End Medical Device Institute Data Center