Value Measurement and Payment Exploration: Two Core Dilemmas in Medical AI Commercialization

As various industries undergo corrections due to pressures from the economic cycle, the medical AI sector continues to maintain high-speed growth despite not yet achieving scalable profitability. The latest market research data shows that China’s medical AI solutions market totaled RMB 16.4 billion in 2024 and is projected to expand to RMB 35.3 billion by 2030, representing a CAGR of 13.63%.

The vast and growing market has not only attracted more entrepreneurs but also driven a large number of physicians to engage in scientific research and product development in AI. Current medical AI is no longer the product of a single discipline, but rather a deep integration of computer science, engineering, and medicine.

Focusing on 2025, the most significant changes in medical AI can be summarized in two key points:Breakthrough Evolution of Large Language ModelswithLarge-Scale Participation of Medical Institutions。

DeepSeek-R1, released by DeepSeek in early 2025, has brought significant momentum to the large language model (LLM) industry. Supported by innovative designs such as Parameter-Efficient Fine-Tuning (PEFT) and Mixture of Experts (MoE) architecture, DeepSeek has successfully lowered the entry barrier for LLMs, prompting hospital administrators to proactively deploy related infrastructure.

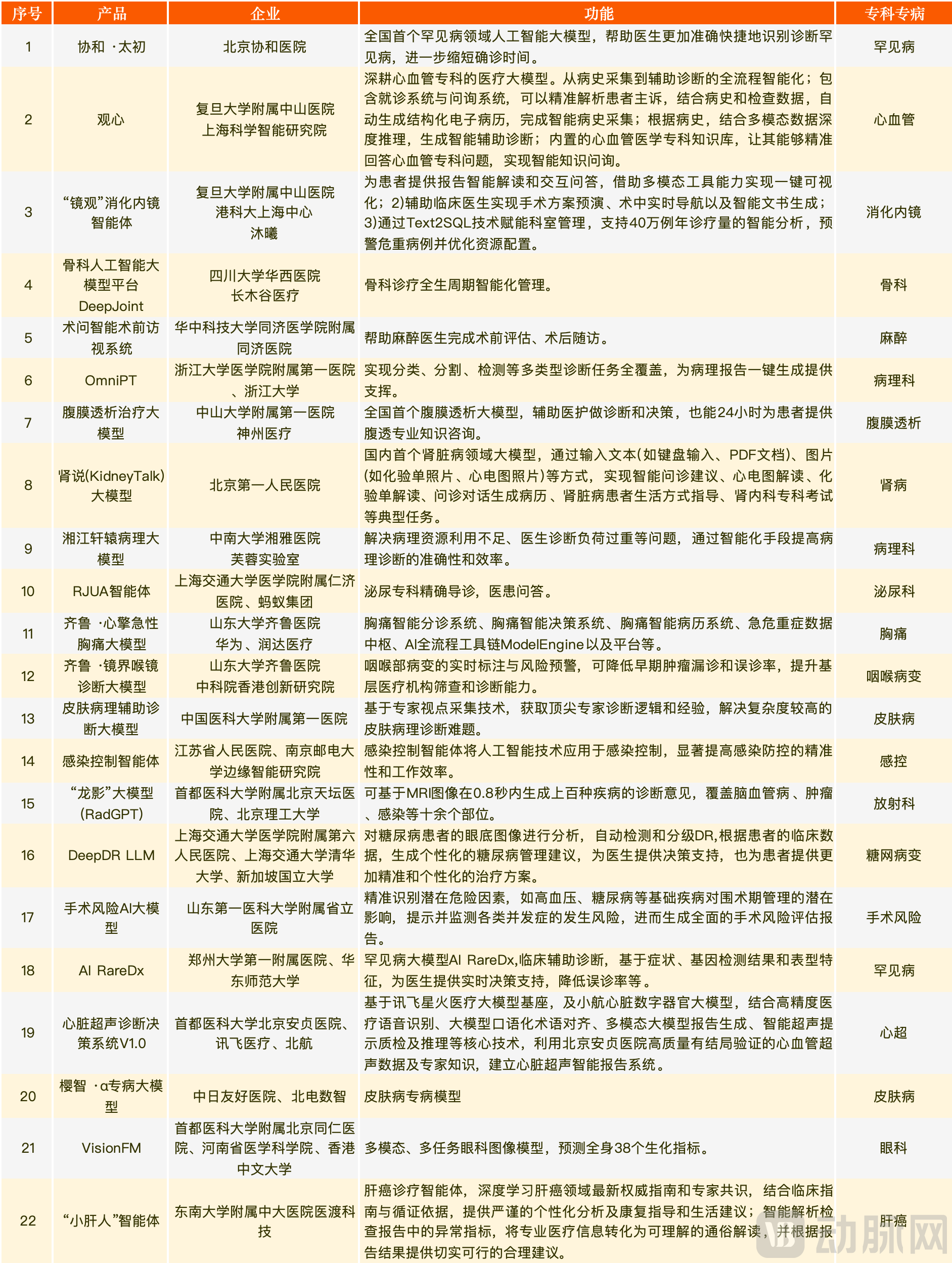

According to statistics from VBInsight: As of May 2025,All of the top 100 hospitals in China on third-party rankings have fully completed large language model deployment., 38 hospitals have furthered R&D on the basis of general-purpose models to create 55 vertical medical models tailored to their specific needs, including 22 specialty-specific models.

Meanwhile, physicians’ enthusiasm for hands-on use of large language models (LLMs) far exceeds that for traditional AI. When the Shenzhen Municipal Health Commission began restricting hospitals from independently procuring computing resources—opting instead for centralized procurement to prevent excessive purchases by individual hospitals and avoid waste—and hospitals were reluctant to allow patient data to leave their premises, some physicians still circumvented the policy on computing resource procurement by applying for research grants, persisting in leveraging LLMs for clinical research exploration.

Specialty Large Language Models Co-Developed by Hospitals in the First Half of 2025 (Source: Public Information)

It is worth noting that non-Transformer AI architectures are also being increasingly deeply integrated into clinical practice. Previously, their deployment was concentrated in departments such as medical technology and information technology, empowering processes including consultation, examination, and follow-up. In recent years, with the rise of surgical robots, a significant number of applications have begun to emerge in therapeutic scenarios.

Publicly available information indicates that surgical specialties, including thoracic surgery, neurosurgery, cardiology, and orthopedics, already have a wide array of AI-assisted therapeutic tools at their disposal. In this survey, over 90% of physicians who had used such AI systems provided positive feedback, confirming that AI can enhance surgical precision and significantly reduce the incidence of complications.

Panoramic View of AI Applications in Specific Healthcare Scenarios (Source: VBInsight)

Policy support is also being progressively strengthened. The “Measures for Optimizing Full-Lifecycle Regulatory Oversight to Support the Innovative Development of High-End Medical Devices (Draft for Public Comment)” has publicly solicited opinions on market access pathways for emerging technologies such as multi-disease AI and large language models, taking a pioneering step in setting a strategic direction for the development of large language models.

The "Implementation Opinions on Promoting and Standardizing the Development of 'AI + Healthcare' Applications" proposes 24 key directions for application development.By 2027, establish a set of high-quality datasets and trusted data spaces in the health sector, develop a series of vertical large models and intelligent agent applications for clinical specialties and specific diseases, and achieve widespread adoption across healthcare institutions of intelligent auxiliary tools for primary care diagnosis and treatment, intelligent decision support for clinical specialty and disease-specific diagnosis and treatment, and intelligent patient services., a number of national pilot bases for AI applications in the medical and health sector have been basically established, creating more high-value application scenarios and driving the high-quality development of the health industry. The introduction of these policies has further clarified the development path for medical AI.

Overall, medical AI is currently reaping the dividends of capital investment, supportive policies, and physician collaboration, which will provide sufficient momentum for its rapid development over the next three years at least. However, to translate these resources into a continuous stream of value, medical AI must further reduce R&D costs, resolve the “value divergence” associated with its adoption, and innovate in business models and payment mechanisms.

Despite the rapid development of AI through multi-party collaboration, AI devices/software that emerge as independent product forms have always struggled to break through in commercialization. Ultimately,The Value Generated by Medical AI Varies Across Different Deployment Environments, Making It Difficult for Hospitals to Accurately Calculate Benefits, to some extent, hindering the commercialization of medical AI.

Furthermore, the clinical benefits generated by AI applications may not necessarily translate into hospital value. In most cases,AI is deployed only when it aligns with the interests of administrators., and thus some intelligent applications serving doctors and patients may be overlooked during procurement.

Short-term: The interests of hospitals and physicians are largely misaligned

Considering Department Capacity (neutral stance, same below): When patient queues occur (primarily in the Radiology Department), optimizing a single step can theoretically improve overall efficiency, enabling physicians to treat more patients. In the absence of queues, the introduction of AI into the department will not change patient volume; while it alleviates physicians’ workload, the resulting gains in physician efficiency will not yield tangible benefits in the short term.

Consider Application Functionality (Reverse): Hospitals may procure AI for rating purposes, potentially overlooking factors such as application capability and interoperability, which are closely related to physicians' user experience.

Consider Autonomous Model Learning (Reverse): Hospitals aim for physicians to organize data generated during clinical care to enable in-house autonomous model learning. However, contributing their expertise to AI does not align with physicians’ short-term interests, and some physicians resist using their own data to train models.

Long Term: The Interests of Hospitals and Physicians Are Largely Aligned

Department Perspective (Consensus): Superior surgical quality will enhance the hospital’s reputation, attract more patients for treatment, and potentially improve both departmental performance and physicians’ income.

Scientific Research (Consensus): The time saved by AI enables physicians to engage in more scientific and educational activities, thereby enhancing their individual influence and the hospital’s overall research capabilities.

Autonomous Learning (Neutral): After learning physicians' habits, the model can provide personalized settings upon subsequent use by the same physician (particularly in surgical procedures), thereby enhancing both surgical efficacy and efficiency, which ultimately translates into improved departmental performance. However, for senior physicians, contributing their accumulated experience to AI capabilities without compensation enhances the department’s overall capacity but diminishes their individual competitive advantage, which is not aligned with their personal interests. Consequently, some physicians are reluctant to allow their data to be used for training AI models.

Cost Considerations (Inverse): The scaled adoption of AI may reduce hospitals' demand for physicians, leading to salary reductions or workforce downsizing.

Patient Perspective: Potential Misalignment of Interests Between Patients and Departments

Patient Experience (Consistency): AI can optimize treatment efficacy and surgical procedures, leading to better patient outcomes, increasing surplus under DRG-based payment systems, and thereby boosting income for physicians and departments.

Patient Payment (Reverse): While process optimization has reduced patients' treatment time and costs, it may have decreased departmental revenue due to changes in coding and reduced interdepartmental assistance.

As can be seen from the above analysis,In the short term following AI implementation, hospitals and physicians often have misaligned interests; short-term deployment benefits physicians but not hospitals., and the payback period is difficult to estimate. In the current economic climate, hospitals generally face tight cash flows, prompting managers to prioritize risk control and innovative technologies with short payback periods. Consequently, while they are willing to adopt AI solutions, they struggle to afford them.

As for long-term benefits, the actual survey results:From 2020 to 2021, hospitals that began deploying specialty-specific AI in clinical departments have already achieved a dual improvement in departmental efficiency and patient volume, with deep integration of AI applications into physicians’ diagnostic and treatment workflows.

However, the measurement of short-term and long-term benefits varies across different clinical departments, significantly influenced by factors such as macroeconomic policies, hospital infrastructure, management perspectives, the limitations of AI capabilities, and AI reimbursement mechanisms, thus necessitating independent evaluation. In this report, we will delve into departments including thoracic surgery, cardiology, neurosurgery, and radiation oncology to analyze AI applications and commercialization progress within specific clinical contexts, aiming to identify new approaches to resolving the challenges in the commercialization of medical AI.

As a department in a tertiary hospital with high patient volumes, significant clinical pressure, and intense workloads, thoracic surgery has an inherent demand for medical AI to improve departmental operational efficiency and diagnosis/treatment quality, while reducing redundant clinical tasks in physicians’ daily practice.

Meanwhile, data generated during thoracic surgery diagnosis and treatment is easily standardized. This is particularly true in pulmonary surgery, where lung imaging data from CT and DR scans are highly suitable for deep learning training, making it one of the earliest medical scenarios empowered by AI.

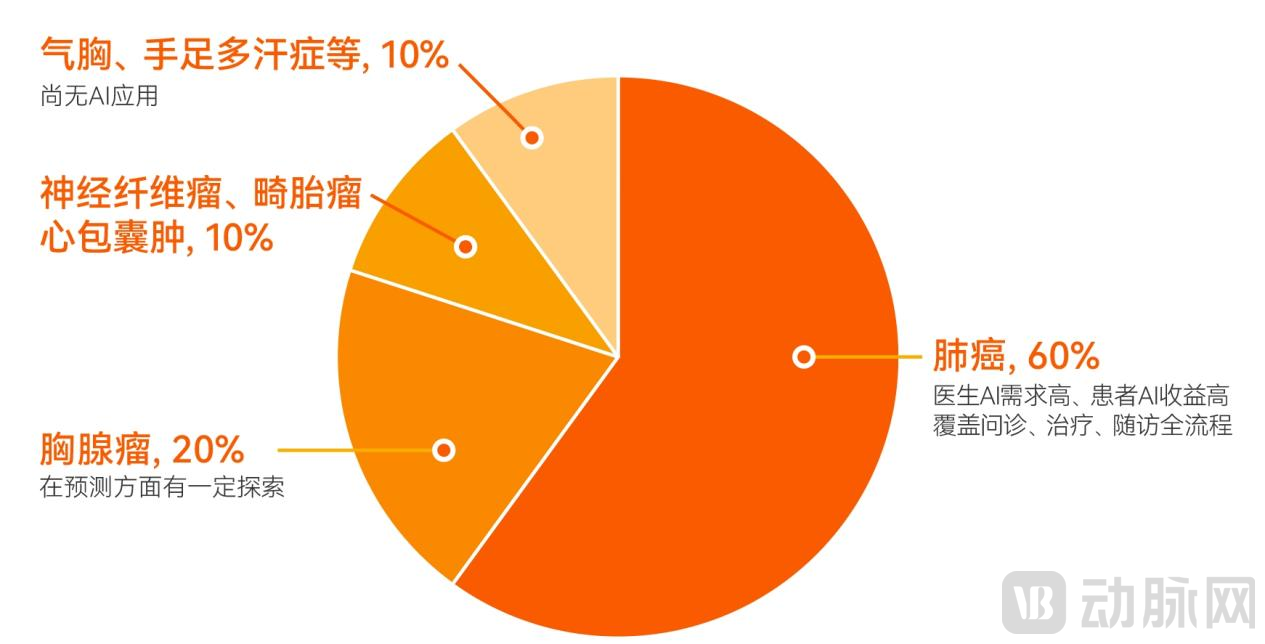

Outpatient Services in Thoracic Surgery and the Distribution of Artificial Intelligence (Source: Survey Interviews)

Surveys indicate that the most frequently used AI applications in thoracic surgery departments of tertiary hospitals in China are concentrated in auxiliary diagnosis, guided biopsy, surgical planning, and intraoperative navigation, with pulmonary surgery being the most mature area.

Diagnostic Phase,Based on human-machine comparative experiments using CT imaging samples with fewer than 100 slices, physicians required 5–10 minutes to independently identify pulmonary nodules, whereas the time consumed in a human-machine collaboration mode was 1.6–2.2 minutes. Theoretically, this reduces the time by 2.8–8.4 minutes, representing an efficiency improvement of 56%–84%.. As the number of CT slices increases, there is further room for growth in the efficiency improvement ratio.

Taking a Grade A tertiary hospital in Northeast China as an example, its thoracic surgeons previously had to manually review 60 sets of patient imaging studies from start to finish each day, resulting in slow interpretation speeds and a heightened risk of missed diagnoses. With AI empowerment, the system now flags an average of several cases requiring special attention daily (typically 5–6 at this hospital).Some physicians conduct detailed reviews of annotated images while briefly scanning non-annotated ones, improving overall diagnostic efficiency by approximately 73%. The system has been in operation for about four years; coupled with intraoperative AI empowerment, the department’s outpatient volume has increased by approximately 40%.。

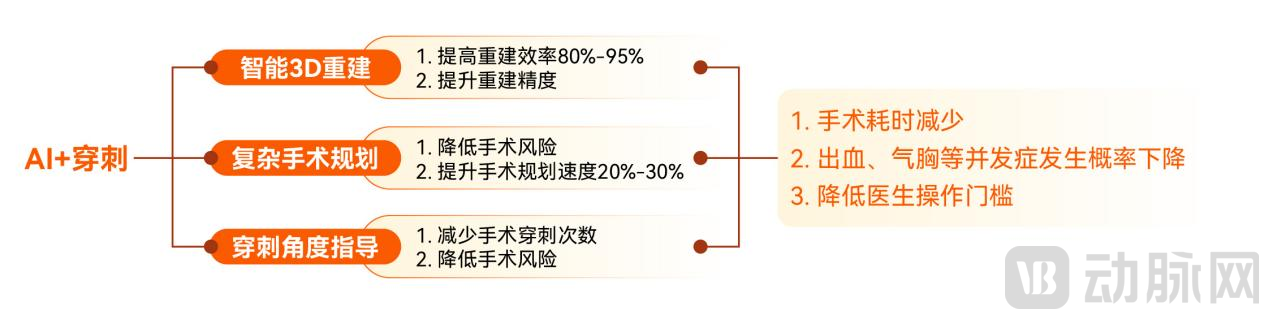

During the surgical phase, AI value creation is mainly reflected inComplex Surgical PlanningandPuncture Angle GuidanceIn complex surgical planning, junior surgeons are prone to errors when managing high-risk lesions (such as those adjacent to blood vessels). AI can optimize needle insertion paths, thereby reducing procedural risks. Regarding needle insertion angles, surgeons must accurately replicate the "virtual angles" from two-dimensional images within the three-dimensional human body, while also contending with dynamic interferences such as respiration and patient positioning. This makes it difficult to rapidly identify an effective insertion angle. AI can assist surgeons by providing real-time assessment of whether the needle insertion angle meets surgical requirements.

The Value of AI-Guided PunctureSource: Public information, research interviews

In AI-assisted needle biopsy, data from a Grade 3A hospital showed that the AI-enabled robotic group significantly outperformed the conventional manual biopsy group in terms of the success rate of localization with no more than two adjustments (76.5% vs. 25.0%), the mean number of needle adjustments (1.62 ± 1.71 vs. 4.39 ± 3.69), and the number of CT scans received by patients (5.47 ± 2.59 vs. 8.39 ± 4.69).

In the field of 3D reconstruction, after the First Affiliated Hospital of Harbin Medical University introduced AI to achieve precise segmentectomy,The 3-year survival rate of patients increased by approximately 20%, with a significant reduction in complications (refractory cough decreased by about 40%, pain decreased by about 20%, and overall complications decreased by about 30%).. In terms of length of stay, the hospital’s average length of stay decreased from 12 days before AI implementation to 5 days currently, representing an efficiency improvement of approximately 58.3%.

Theoretically, the commercial value of AI in thoracic surgery depends on the economic value it brings to the department. Currently, the performance of AI in thoracic surgery falls into three models: efficiency enhancement, quality improvement, and process optimization. Among these, efficiency enhancement primarily delivers value to the department, quality improvement primarily benefits patients, while process optimization provides value to physicians in some cases and to patients in others.

When the actual clinical care cost of a department is lower than the payment standard for its corresponding DRG group, the efficiency-enhancement model has a certain impact on the department’s revenue, but the magnitude of this impact is limited.This is because the improvement of departmental operational efficiency aligns with the core logic of the “wooden bucket theory,” where the upper limit of efficiency gains is determined by the weakest link. Even if consultation and surgical procedures achieve efficiency improvements exceeding 50%, factors such as prolonged preoperative examinations and unreasonable physician scheduling will still hinder the realization of overall efficiency gains.

The quality improvement model has a significant impact on enhancing patient value., the enhancement of departmental value is contingent upon specific circumstances. When departmental beds are at full capacity and the cost of diagnosis and treatment is below the payment standard for the corresponding DRG group, reducing the average length of stay can increase the department’s surplus from medical insurance payments. However, if there is bed availability, AI empowerment can only generate additional surplus by lowering the cost per case (by reducing complications and readmission rates); while valuable, its impact is relatively limited.

Compared with the first two models, the optimized process model often achieves higher comprehensive value (patient value + departmental value) due to its substantial patient value, but it may be detrimental to departmental performance evaluation under the DRG system.

Taking posterior mediastinal neurofibroma as an example, under the traditional pathway, thoracic surgeons would perform contrast-enhanced chest CT to clarify the tumor’s location, size, and its relationship with blood vessels (such as the aorta and azygos vein), the trachea, and the intervertebral foramina. However, if the tumor invades the intervertebral foramen, a chest MRI is additionally required, along with a risk assessment conducted in collaboration with neurosurgeons, resulting in a total patient cost of approximately 50,000 yuan.

Once AI-based 3D reconstruction technology matures, certain AI systems will be able to reconstruct critical nerves from CT images and directly assess the risk of resection. As neurosurgical involvement is no longer required, the total cost for patients decreases, and the diagnostic workflow is shortened. However, under the Diagnosis-Related Group (DRG) payment system, the traditional diagnostic and treatment pathway involves two surgical procedures, which can be reimbursed separately, whereas the new pathway involves only a single surgery, resulting in reduced reimbursement.

Under these circumstances, the new workflow benefits patients but is detrimental to departmental interests, making it difficult for the relevant AI solutions to realize their value in the short term and thereby diminishing their commercial viability to some extent. In the long run, however, these AI solutions still hold the potential for a qualitative leap in value, a possibility that will be closely tied to changes in DRG payment rules.

From the perspective of medical AI’s applications in both clinical specialties and clinical support services, it can deliver certain value; however, most of this value is insufficient to persuade payers to provide reimbursement. Therefore, in the near future, medical AI must continue to explore additional pathways for deeper integration into clinical practice, identifying application scenarios that more tangibly improve patient outcomes in diagnostic examinations and surgical interventions.

However, deeper exploration entails higher costs. To ensure the sustainable development of medical AI, the industry must identify more efficient R&D pathways and effectively control expenditures to develop more powerful AI solutions at lower costs. Furthermore, reducing costs can further influence pricing, thereby expanding sales opportunities across a broader range of medical scenarios.

Prior to 2023, “data governance” constituted a rigid cost in AI research and development, making it difficult to discuss “cost reduction” in this area. However, with the establishment of the National Data Bureau, data’s role as a “factor of production” has begun to take effect, marking the onset of transformative change.

At the current stage, the impact of “data” as a key factor on AI development is more direct and profound than that of computing power or algorithms. This impact depends not only on enterprises’ investment in this factor and the pace of data governance by enterprises, medical institutions, and research organizations, but also on the exploration of ethics related to healthcare data—specifically, how developers utilize healthcare data.

If data governance efficiency can be improved, the cost of producing high-quality datasets reduced, and high-quality data reused multiple times, both the application scope of the medical AI industry and the robustness of the algorithms themselves will see significant improvements.

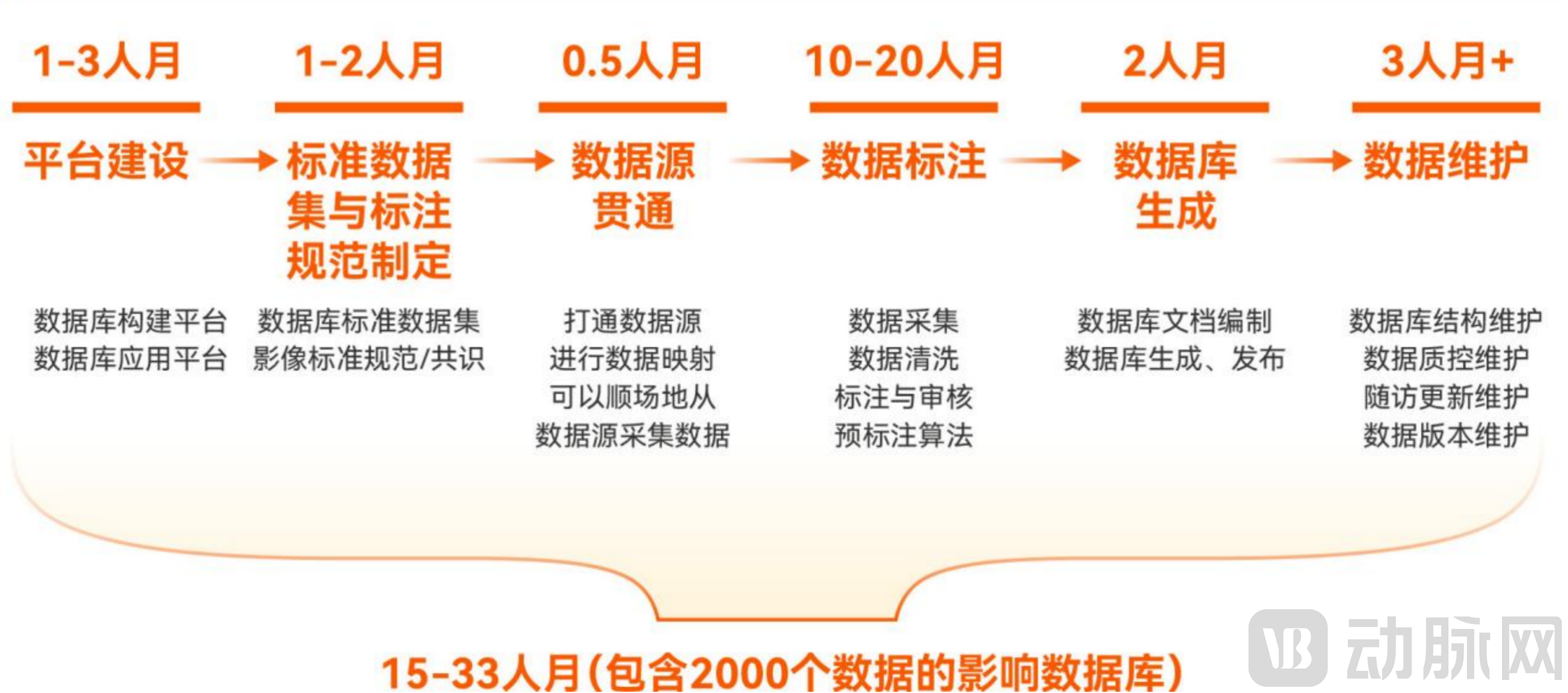

Challenges in Dataset Construction. Data sources: Research interviews, Neusoft Medical

In April 2020, the State Council issued the “Opinions on Building a More Complete System and Mechanism for Market-Based Allocation of Production Factors,” formally establishing data as the fifth major factor of production and explicitly proposing to “improve rules governing the circulation of data factors.” Following the establishment of the National Data Administration in 2023, the process of “data assetization” accelerated, marking the genuine commencement of exploration into medical and health data.

There are numerous pathways for data reuse centered on the capitalization of health data assets; this discussion focuses primarily on exchange-based trading and trusted data spaces.

On-Exchange Trading of Medical DataIt is a nationally equitable method for data circulation. The prerequisite for efficient data circulation lies in having abundant suppliers and sufficient demand. At present, demand is robust, but the supply of providers remains insufficient.

To transform raw data into tradable healthcare data assets, suppliers typically need to complete five stages: data collection, data governance, law firm assessment, asset establishment, and platform trading. Among these, data governance, law firm assessment, and asset establishment collectively constitute the production costs of data assets.

1. Data Cleaning Phase. Before establishing data assets, institutions need to define the content of the dataset, identify the raw data, and perform cleaning on the raw data. Taking imaging data assets as an example,The standard cost for a single chest CT scan at a tertiary hospital is approximately RMB 50–60 per scan. For a dataset comprising 1,000 patients, the corresponding data governance cost amounts to RMB 50,000–60,000.。

2. After completing data governance, the next step for the data provider is to engage a law firm to conduct a compliance assessment, ensuring that the source of the data assets meets legal requirements. Fee structures across law firms are similar; charges are unrelated to the content of the data and are based solely on volume and frequency.Generally, the fee for a single digital asset valuation ranges from 50,000 to 60,000 yuan.

3. Asset Ownership Confirmation: Data providers need to approach a data exchange to confirm asset ownership and obtain a data asset certificate for public disclosure and trading purposes. This step is less expensive than the previous ones; fees vary by exchange but are all capped at several thousand yuan.

The total cost across the three stages amounts to approximately RMB 100,000. For certain entities, particularly healthcare institutions, the cost of producing data assets may exceed the revenue generated from a single medical health data asset transaction, while also entailing data-related risks. Consequently, sales volume is constrained in the short term, leading to a scarcity in the supply of medical data assets.

Some IT department physicians at hospitals have stated that the current revenue generated from data trading is insufficient to justify the significant risks involved. Consequently, most hospitals remain in a wait-and-see mode, pending further development of the medical data trading market.

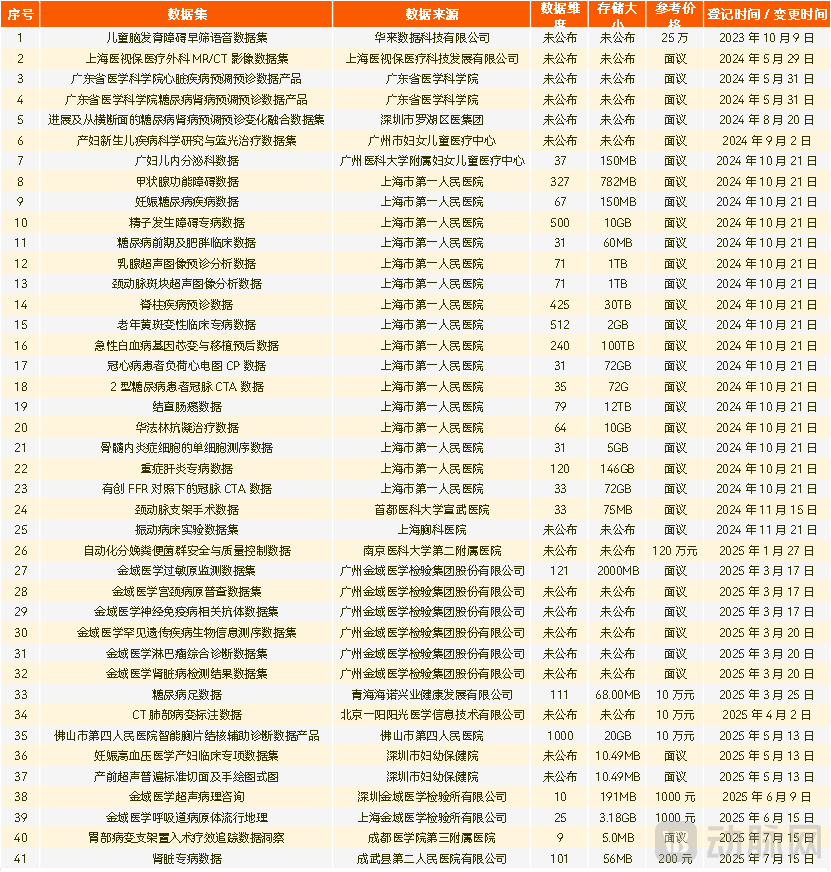

Selected Health Data Trading Assets Listed on Online Exchanges

(Source: Public information; statistics as of July 10, 2025; incomplete data)

Trusted Data SpaceIt is a data circulation and utilization infrastructure based on consensus rules, designed to connect multiple parties and achieve the sharing and joint use of data resources. Compared with technologies such as blockchain and privacy-preserving computation, its breakthrough lies inA Special Space with an Intrinsic Data-Sharing Trust Mechanism, to create a secure and trustworthy data circulation environment for different entities, industries, and regions, and to promote the orderly flow of data.

Specifically, trusted data spaces ensure “trustworthiness” throughout the entire process of data resource access, usage, and traceability. By implementing strict access authentication for participating entities, data, products and services, and technical components, they guarantee verifiable entity identities, data usability, and the safety and reliability of products and services within the space. Meanwhile, by leveraging digital contracts and usage control policies, they implement real-time management and control over all activities in the data circulation and usage process, effectively safeguarding the data rights and interests of all parties involved.

In the healthcare sector, the value of this technology lies in helpingHealthcare institutions, pharmaceutical companies, insurance providers, and research organizationsenabling all stakeholders to securely share various types of healthcare data, including patient diagnosis and treatment data and clinical research data, on the basis of adhering to common rules, thereby breaking down data silos and promoting the deep integration and utilization of medical data.

Trusted Data Space in the Medical Insurance Industry

(Data source: public information, Jiangsu Data Group)

Before the healthcare data trading market reaches scale, trusted data spaces can facilitate small-scale data transactions and promote data reuse among the entities responsible for building these spaces.

Overall, there have been active explorations and practices in the field of trusted data spaces, but overall development is still in its early stages. In particular, the integration of “large models + data spaces” remains limited in application cases due to high technical complexity and cost constraints. To truly promote the healthy development of trusted data spaces, it is necessary to establish unified technical roadmaps and standard systems, address the challenges of integrating large models with data space technologies, and advance the construction of a secure, efficient, and fair data circulation environment.

The above is an excerpt of the main content of the report. Scan the QR code to download the full report for free.

Report Table of Contents

Chapter 1: Medical AI, Trapped in Value Divergence

1.1 “Capital + Policy + Physicians” Triple Drive: Medical AI to Maintain Rapid Growth Over the Next Three Years

1.2 Deep-Rooted Value Divergence: The Difficulty in Balancing Patient Outcomes with Departmental Efficiency

Chapter 2: AI in Clinical Specialties: Significant Patient Benefits, with a Need to Explore Payer Models in Out-of-Hospital Settings

2.1 Thoracic Surgery: Originating in Diagnosis, Rooted in Treatment

2.2 Cardiology: Late Movers Take the Lead, Device Sales Open New Pathways for AI Commercialization

2.3 Orthopedics: Highly Compatible with Robotic Applications, Pioneering the Large-Scale Implementation of AI

2.4 Neurosurgery: Focused Treatment, AI Reshaping Precision Surgery

2.5 Department of Endocrinology: Revitalizing Chronic Disease Management and Empowering the Full Care Cycle to Unlock the Vast Value of Health Data

2.6 Commercialization of Clinical AI Departments Requires a Shift in Mindset

Chapter 3: Clinical AI Support: Mature Implementation Models for Medical Technologies Require Deep Integration of Information and Systems

3.1 Department of Medical Technology - Department of Radiology: The Most Comprehensively AI-Empowered Department

3.2 Medical Technology Department – Radiation Oncology: A Leap in Wisdom Toward Maximizing Efficacy and Minimizing Damage

3.3 Medical Technology Department – Pathology: Large Language Models May Redefine Pathological Capabilities

3.4 Department of Medical Technology – Clinical Laboratory: Multimodal Large Models Drive a Qualitative Leap in Efficiency

3.5 Management Support – Information Department: Integrating into the System, with Profitability Not as the Core Objective

3.6 Primary Healthcare: Shift in Commercialization Model, Transition from Policy-Driven to User-Driven

Chapter 4: Data Assetization: Unveiling the Path to Breakthroughs for Sustainable Growth in Medical AI

4.1 Intelligent Iteration of Medical Data Governance

4.2 Reuse of Medical Data

4.3 Challenges and Opportunities in the Context of Ethical Issues

Chapter 5 Corporate Case Studies