2025 Annual Innovation White Paper on Medical Services: Deepening Payment Reform, Focus on Elderly and Pediatric Care, and Seven High-Value Segments Driving Transformation

VCBeat is committed to promoting competitive innovative products or solutions to the global market, driving Chinese innovation onto the world stage. In 2025, VCBeat continued its systematic research into hot and frontier sectors, producing the Annual Innovation White Paper Series for the Healthcare Industry, which includes the “2025 Annual Innovation White Paper on Medical Services,” the “2025 Annual Innovation White Paper on Medical Devices and Supply Chains,” the “2025 Annual Innovation White Paper on Innovative Drugs and Supply Chains,” and the “2025 Annual Innovation White Paper on Digital Health.” This series identifies Chinese innovative products or solutions that demonstrate both “product innovation” and “market performance,” providing multi-dimensional analyses of these selections. The “2025 Annual Innovation White Paper on Medical Services” is the first installment in the series; VCBeat will subsequently release the remaining three white papers to keep readers informed.

China’s healthcare services industry stands at a critical juncture of bottoming out and rebounding, as well as transformation and upgrading. It is gradually moving away from extensive growth models and entering a development phase centered on quality, efficiency, and value. In 2025, policies focused on elderly health, strengthening primary care capabilities, and optimizing payment systems. Although the capital market has generally slowed down, funds are rationally flowing into AI innovation and clearly policy-directed niche sectors. Meanwhile, companies are implementing explorations of large AI models and intensively laying out strategies in tracks such as weight management and instant retail of pharmaceuticals.

“2025 Annual White Paper on Innovation in Healthcare Services” systematically reviews the key highlights of 2025 from four dimensions: policy environment, industry scale, corporate developments, and capital perspectives. Its core objective is to recommend innovative solutions with core competitiveness and representativeness to the global market. By establishing an evaluation framework encompassing policy adaptability, demand inelasticity, business model resilience, and technological barriers, the white paper selects seven high-value sectors for analysis from numerous tracks: private ophthalmology, private reproductive health, private health screening, private dentistry, third-party sterile supply centers, “Internet + nursing services,” and instant pharmaceutical retail. It further provides case studies of representative high-value enterprises within these sectors, offering strategic insights for the market.

Key Insights and Conclusions:

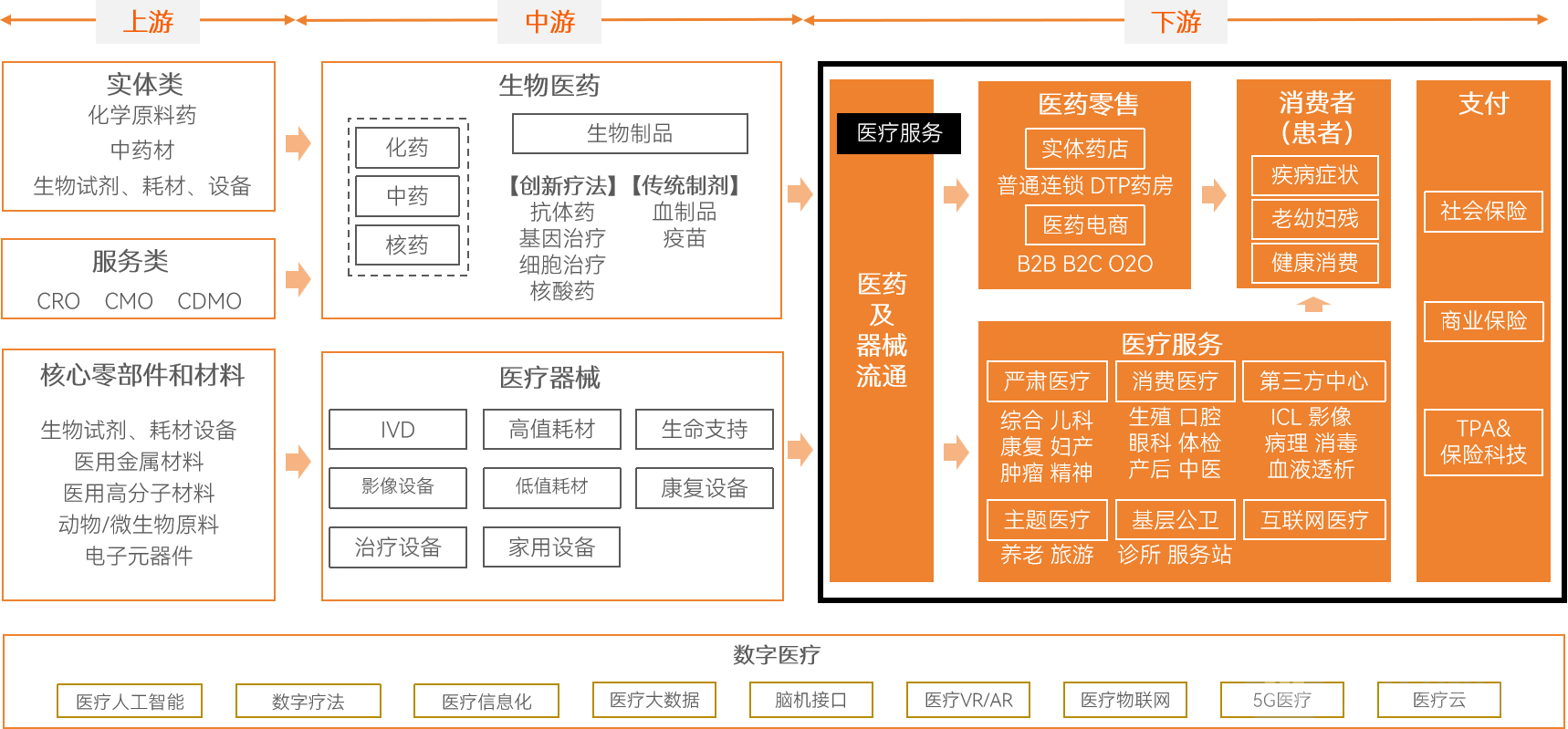

Medical Services Sector: A Panoramic View

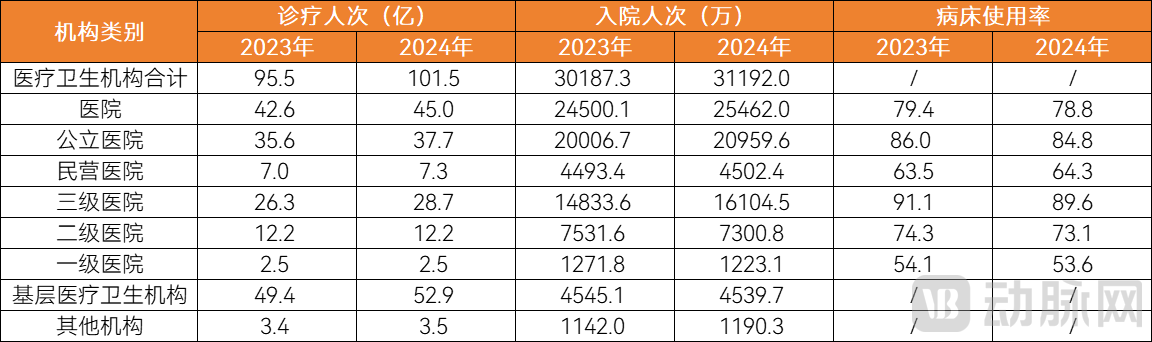

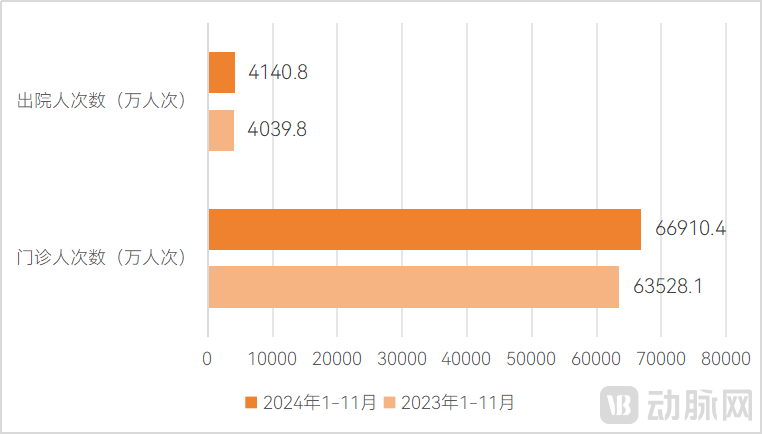

The supply side of healthcare services demonstrates a positive trend characterized by overall growth, structural optimization, and cost containment.In 2024, the total number of outpatient and emergency visits at medical and health institutions across China reached 10.15 billion, an increase of 600 million from the previous year; hospital admissions totaled 311.92 million, an increase of 10.047 million from the previous year. Significant progress was made in tiered diagnosis and treatment, with primary and secondary hospitals and grassroots medical and health institutions accounting for 6.76 billion visits, representing 66.6% of the total. Among these, township health centers, community health service centers (stations), and village clinics recorded 3.98 billion visits, an increase of 230 million from the previous year.

2024 Healthcare Service Supply Overview

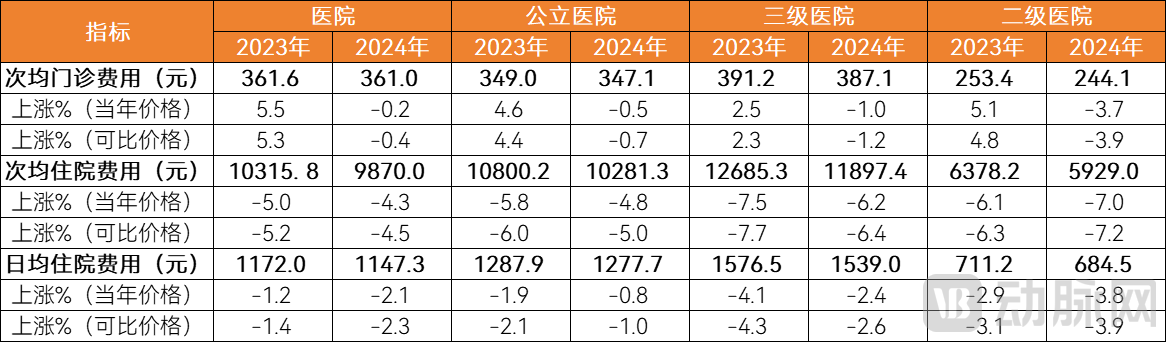

As service volume steadily increased, medical expenses were effectively controlled; the average per-visit outpatient and inpatient costs at tertiary and secondary public hospitals both showed a downward trend when calculated at comparable prices.

Changes in Hospital Outpatient and Inpatient Costs in 2024

It is evident that China’s healthcare service system is evolving toward diversified supply, efficient operations, and multi-tiered coverage. The continuous improvement in the volume and efficiency of healthcare service delivery has established a solid payment foundation for the stable operation of both basic medical insurance and commercial health insurance. Against this backdrop, the healthcare services sector witnessed significant changes in 2025 across four key dimensions: policy orientation, industry scale, business innovation, and capital dynamics.

Policy: Major Breakthroughs in Commercial Insurance Coverage for Innovative Drugs and Drug Price Governance

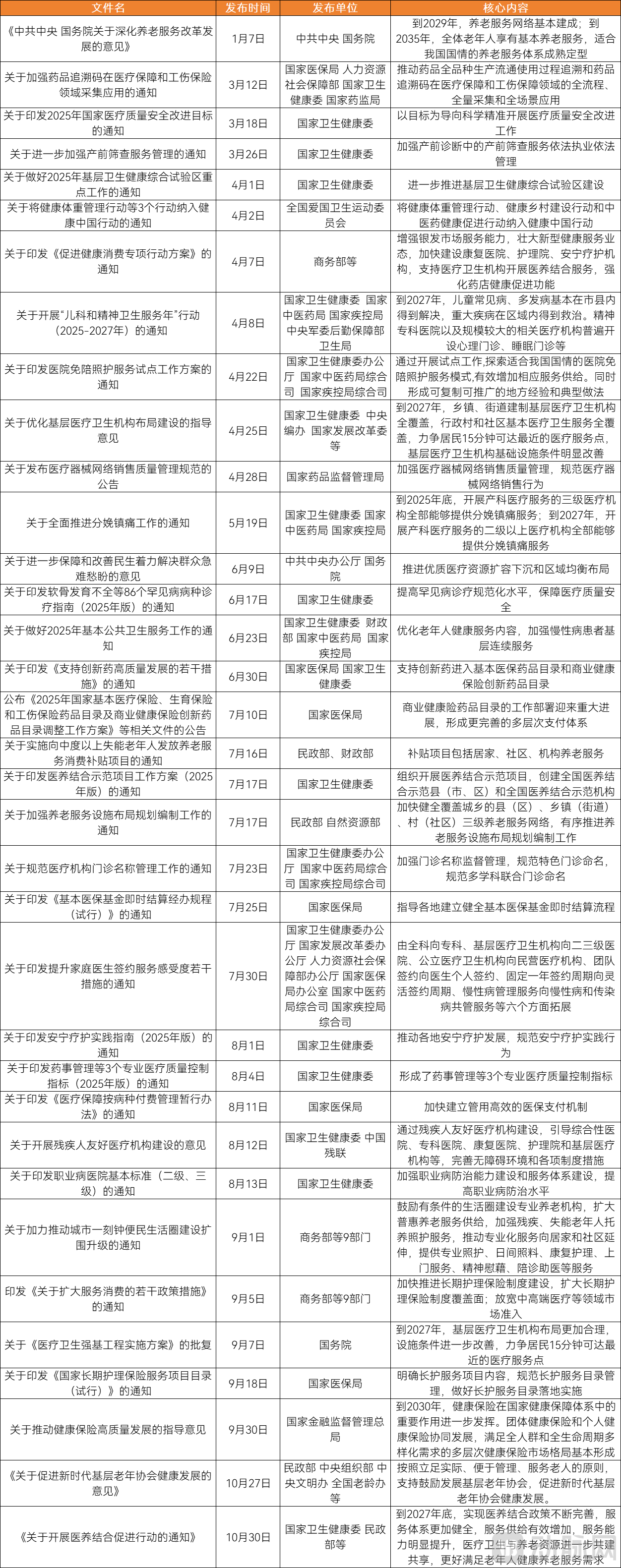

2025 marks the concluding year of China’s 14th Five-Year Plan, during which the state has intensively rolled out initiatives in medical services. VBInsight has reviewed the industry-related policies issued in 2025 and found that key policy focuses include health services for the elderly, strengthening primary healthcare capacity, health management, drug price governance, and improvement of the payment system.

National-Level Key Policies Released by the Medical Services Sector in 2025

Elderly Care Services Welcome Top-Level Institutional Design.The “Opinions of the Central Committee of the Communist Party of China and the State Council on Deepening the Reform and Development of Elderly Care Services,” released in January, is China’s first programmatic policy document issued under the joint auspices of the CPC Central Committee and the State Council to provide a systematic institutional framework for elderly care services. It has established clear development directions and market opportunities for related industries, including “Internet + nursing services,” integrated medical and elderly care institutions, longevity clinics, and elderly care finance.

Commercial insurance and public medical insurance further achieve functional complementarity.In August, the National Healthcare Security Administration publicly released the list of drugs that passed the preliminary formal review for inclusion in the 2025 National Basic Medical Insurance, Maternity Insurance, and Work-Related Injury Insurance Drug Catalog, as well as the Commercial Health Insurance Innovative Drug Catalog. Five CAR-T therapies not covered by basic medical insurance, along with multiple drugs for rare diseases and high-end tumor immunotherapies, are expected to be included in this Commercial Health Insurance Innovative Drug Catalog.

Drug price governance is evolving toward nationwide price linkage, horizontal and vertical drug price comparisons, and nationwide coordination of centralized procurement prices.In May, the release of the “Consensus on Drug Listing on Provincial Pharmaceutical Procurement Platforms” marked a new phase in drug price governance, transitioning from regional and fragmented approaches to nationwide coordination with unified rules. As of September 30, 2025, 14 provinces across China had officially issued drug listing rules, while 30 provinces had released draft versions of their new listing rules for public comment.

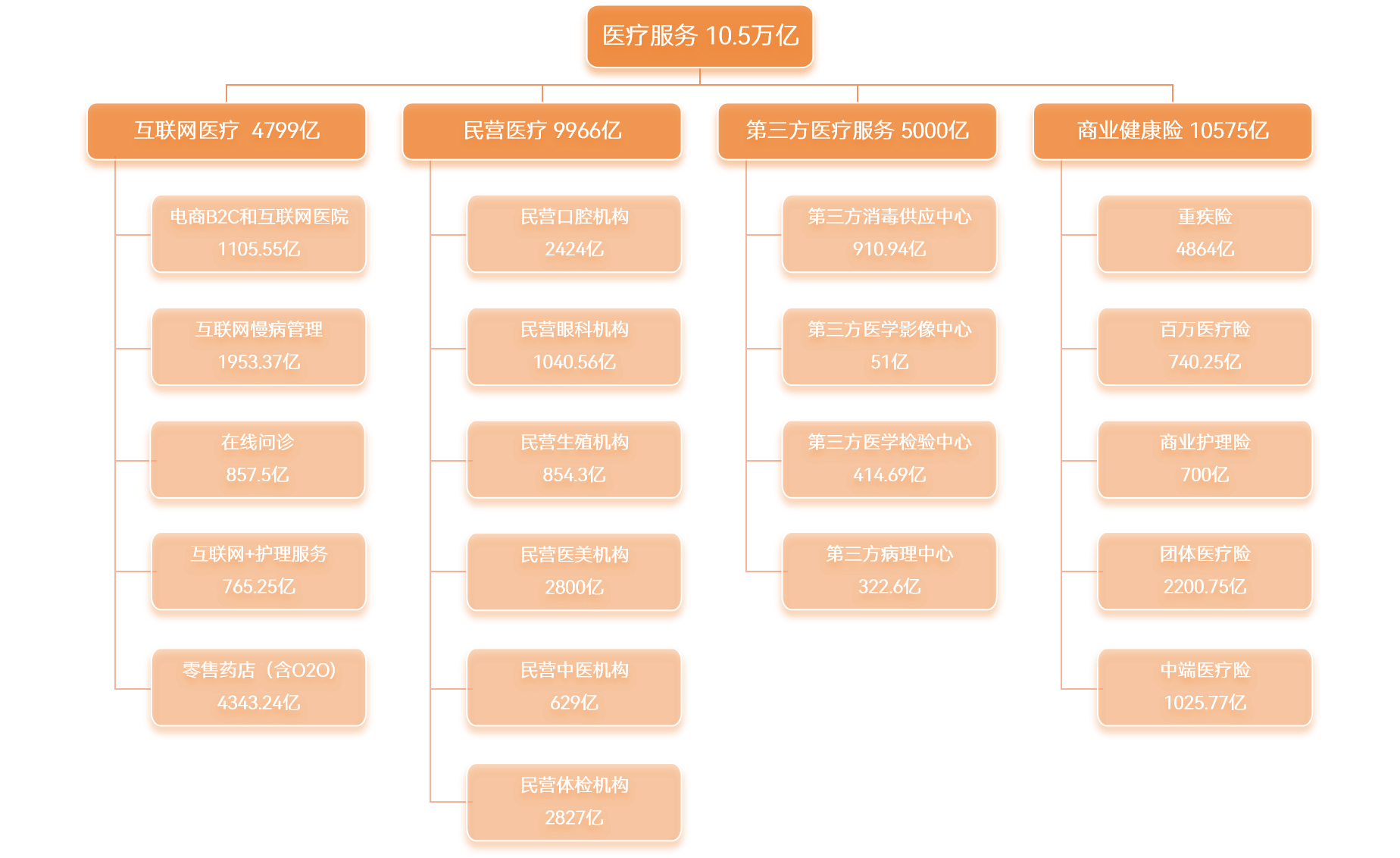

Massive Market Foundation, Industry Scale Exceeds 10 Trillion

China’s total healthcare service market is projected to reach RMB 10.5 trillion in 2025. This substantial scale results from the continuous upgrading of residents’ health demands coupled with supply-side structural reforms.

Statistics on the Market Size of Medical Services and Its Key Sub-sectors in 2025

Corporate Business and Product Updates: Digital Intelligence, Specialization, and Expansion of Business Boundaries Are the Main Themes

Internet Healthcare: Frequent Moves in Weight Loss, Large Language Models, and Other Sectors

The internet healthcare industry is steadily advancing through continuous exploration. The sector is witnessing a trend of multi-dimensional, deepening transformation: the service closed-loop integrating pharmaceuticals, medical testing, and insurance is becoming increasingly mature; large language model technology is further empowering every stage of diagnosis and treatment; and the online-offline integrated model is being continuously refined, with rapid growth in home-based services such as at-home testing and nursing care.

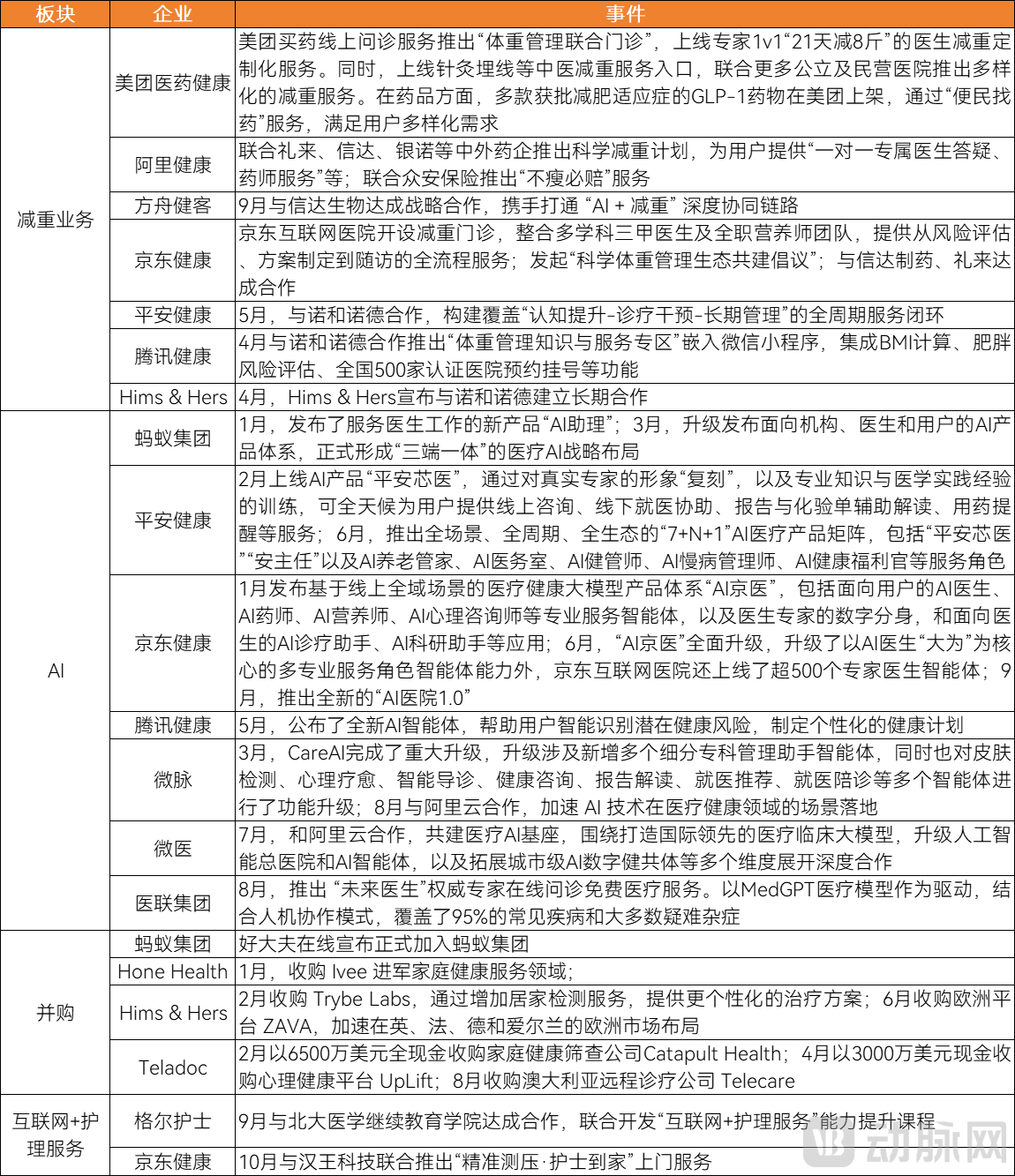

In 2025, the focal points of the internet healthcare industry included weight-loss services represented by GLP-1 drugs, in-depth application of large medical AI models, strategic mergers and acquisitions between domestic and international enterprises, and “Internet + nursing services.”

Hotspot Insights for Leading Internet Healthcare Enterprises in 2025

Among them,Weight-loss services are the hottest growth driver in internet healthcare in 2025.Major players such as Meituan Medicine & Health, Ping An Good Doctor, JD Health, and AliHealth are intensively expanding into the weight management sector. Pharmaceutical companies like Novo Nordisk and Innovent Biologics have also established online channels as key marketing platforms and primary touchpoints for reaching users in the weight loss drug market. The surge in weight management services is driven not only by the market opportunities presented by GLP-1 receptor agonist therapies but also reflects the public’s urgent demand for professionalized, effective, and trustworthy health management services.

Furthermore, in 2025, leading enterprises increased their investment in “Internet + Nursing Services” to pursue specialized development. In September, Geer Nurse’s “Internet + Nursing Services” platform jointly developed and pioneered the launch of a competency enhancement course for “Internet + Nursing Services” in collaboration with the School of Continuing Education at Peking University Health Science Center, addressing the industry’s shortfall in specialized theoretical training. To date, Geer Nurse’s “Internet + Nursing Services” platform has served over 2 million postoperative patients.

Private Healthcare: Prioritizing AI Development and Enhancing Quality of Care

Private healthcare has seen continuous growth in scale and market penetration in recent years. Data shows that in 2024, private hospitals accounted for 31.0% of hospital beds, while their outpatient visits and inpatient admissions represented 16.3% and 17.7% of the total hospital figures, respectively. By the end of 2024, the total number of hospitals nationwide had increased to 38,710, with private hospitals comprising over 60% of this total. Both the number of institutions and service capacity have maintained steady growth, and the scope of services has expanded from treating common diseases to various specialized fields, forming a service network complementary to the public healthcare system.

Changes in the Service Volume of Private Hospitals in Recent Years

Industry trends in 2025 clearly reflect that enterprises’ strategic focus has shifted toward refined operations, deepening specialized capabilities, and differentiated services.Institutions have intensively deployed and adjusted their strategies across dimensions such as digital-intelligent transformation, professional capability building, and market expansion.

Multiple companies are accelerating their digital and intelligent transformation to enhance internal operational efficiency and external service capabilities. For instance, in 2025, Meiwei Dental iterated its self-developed Weixiaomei Medical Cloud Intelligent Platform by integrating large language model capabilities. This upgrade refined AI-powered applications for auxiliary diagnosis, treatment plan design, and patient services, while also developing AI-driven risk control and management tools for human resources, finance, and assets, thereby establishing a comprehensive AI application system covering all scenarios of its dental chain operations.

In terms of service quality and the establishment of professional barriers, the company is committed to in-depth development. Regarding the expansion of service scope, aligning with the trends of the longevity era, Ping An Health (Testing) Center has leveraged its precise insight into customer needs and top-tier medical service capabilities to establish “Longevity Medicine Centers” across 11 cities in China. By providing health management services, it aims to shorten the period of living with disease and enhance the quality of life in later years, thereby achieving a complete closed loop of “screening, diagnosis, management, treatment, and rehabilitation” in specialized discipline construction.

In terms of medical service quality, enhancing clinical care standards is particularly crucial in the highly competitive optometry and ophthalmology industry. Historically, this sector has been skewed toward consumerism, prioritizing marketing over medical expertise. Beitong Pediatric Ophthalmology has established a chain of 10 outpatient clinics in Shanghai. In 2025, Beitong conducted a thorough review of its clinical cases from previous years and collaborated with upstream brand partners. By leveraging large-scale data and AI analytics, the company developed more specific and feasible in-hospital standardized pathways for the prevention, healthcare, diagnosis, and treatment of eye conditions in children and adolescents.

Some leading institutions have accelerated their international expansion. Dr. Zhang Qiang is comprehensively laying out its presence in the U.S. market, with the first CHIVA center currently under construction; Gushengtang has announced the full acquisition of Singapore’s Dazhongtang, planning to expand its clinic network in Singapore to 30 locations by the end of 2026.

Furthermore, prudent chain expansion continues based on a mature operational model. Mumuhua Reproductive Health has established a proven single-clinic model for reproductive medicine outpatient services, having opened 22 reproductive clinics and one tertiary hospital specializing in assisted reproductive technology. Building upon its national chain presence across 9 provinces and 15 cities, it launched the Xi’an No. 2 Hospital (Zhonglou Branch) in 2025 and is preparing to open the Zhuhai branch soon. Mengying Eye Care operates over 90 ophthalmology clinics in 13 provinces, including Jiangsu, Zhejiang, Guangdong, Hubei, Shandong, Henan, and Anhui. In 2025, it continues to establish and launch new ophthalmology clinics in multiple cities, such as Zhengzhou (Henan), Quanzhou (Fujian), Dongguan (Guangdong), Weinan (Shaanxi), Qufu (Shandong), and Changshu (Jiangsu).

Third-Party Medical Services: Chain Expansion and Overseas Exploration

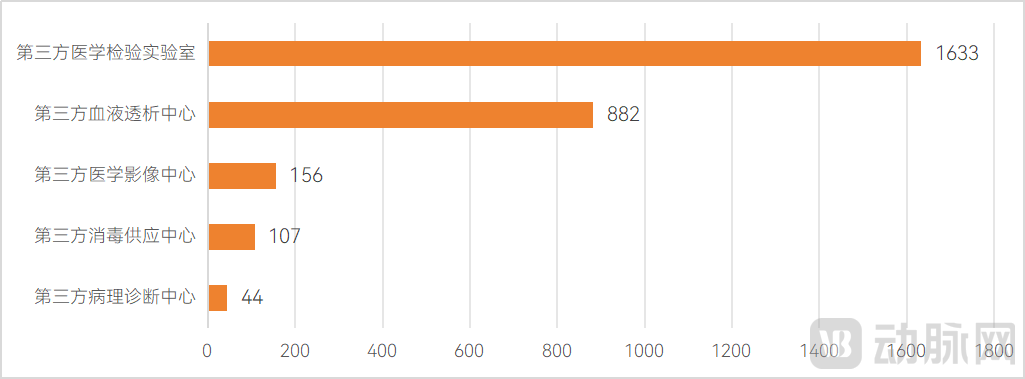

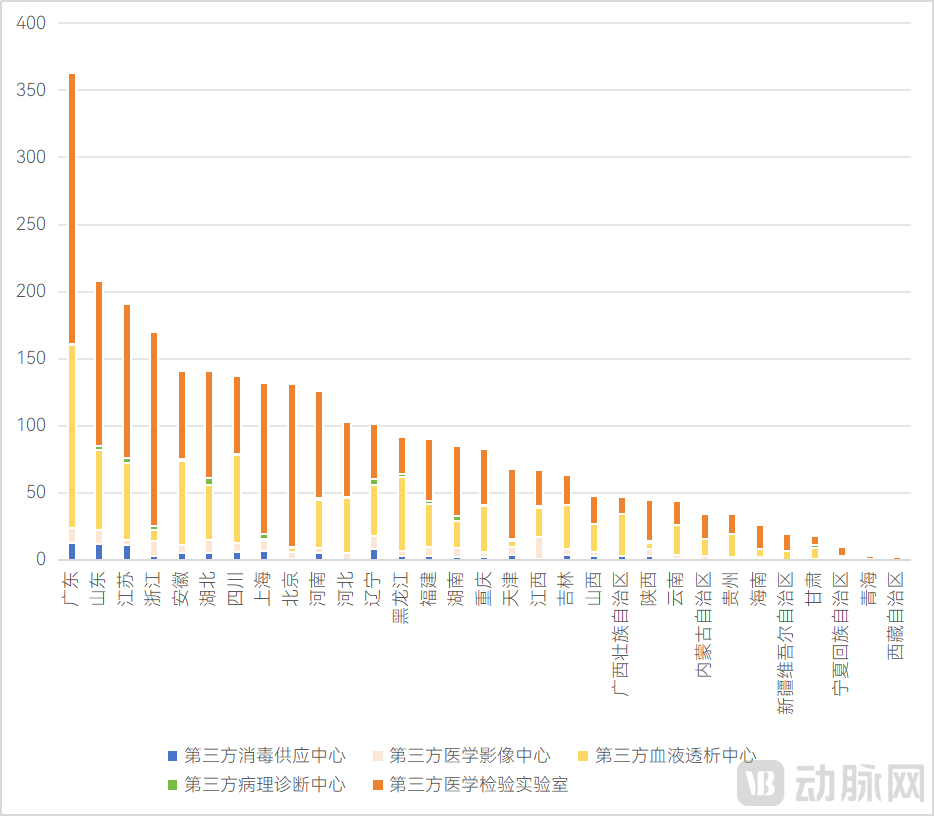

According to VBInsight statistics, as of November 2025, the total number of third-party medical service centers in China has approached 3,000, with relatively concentrated distribution in terms of type and region. In terms of institutional types, third-party medical testing laboratories are the most numerous, reaching 1,633; third-party hemodialysis centers follow closely behind, with 882 facilities.

Number of Third-Party Medical Service Centers in China

Geographic Distribution of Third-Party Medical Service Centers in China

In 2025, China’s third-party medical services market exhibited two major trends amid its continued deepening development: first, achieving rapid chain replication through standardization to enhance market penetration and operational efficiency; second, actively expanding business boundaries to identify new growth curves.

In terms of business expansion, leading enterprises are pursuing vertical integration along the industry chain and exploring cross-sector opportunities. A representative case is Jienuo Medical, which has begun providing industrial sterilization services to medical device manufacturers, successfully extending its client base from healthcare institutions to the industrial sector. In 2025, Jienuo Medical’s Hubei Sterilization Service Supply Center project was signed and established in Junshan New City.

A more groundbreaking expansion of boundaries is evident in its overseas exploration. Due to significant differences in healthcare systems, policies, regulations, and technical standards across countries, the barrier to entry for third-party medical service providers going global is extremely high. In May, Yimai Yangguang partnered with Medical Thinking Health to officially establish the “Yimai–Medical Thinking Health Technology Alliance” and jointly build a dual-engine supply chain platform featuring “centralized procurement + global distribution,” thereby undertaking medical imaging services for multiple private healthcare institutions, including Medical Thinking Health, in Hong Kong and Macao.

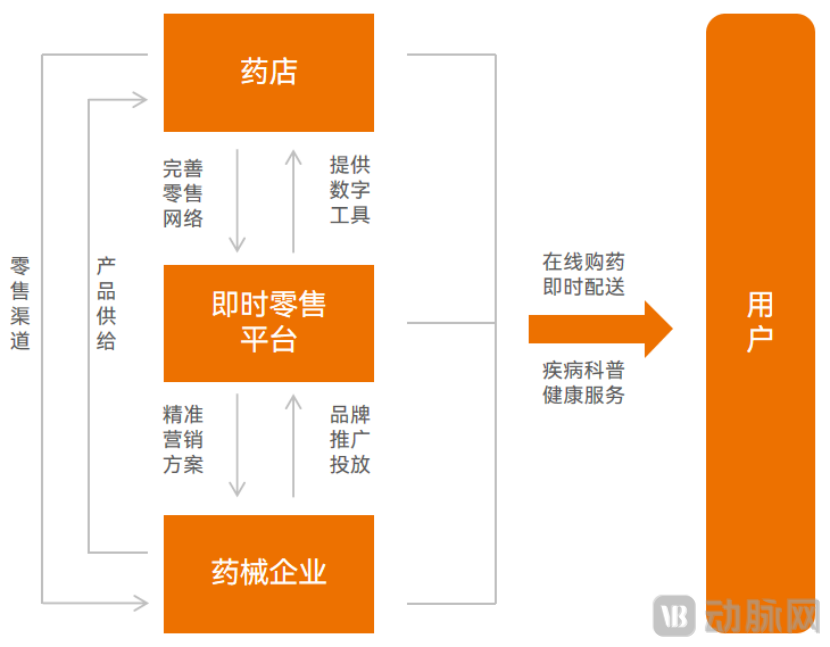

Pharmaceutical Retail: Instant Retail Gains Momentum as Social Media Platforms Enter the Fray

The growth of the instant retail market for pharmaceuticals has been recognized as a clear trend. In 2025, industry enthusiasm intensified, with various platforms uniformly increasing their allocation of traffic resources and deepening the closed-loop service model for instant pharmaceutical retail. For example, Meituan Medicine and Health has integrated its home-delivery and in-store services to establish a one-stop health service ecosystem encompassing “testing, pharmaceuticals, medical care, hospitals, and wellness.” Content-based social platforms such as Douyin and Kuaishou have also actively entered the market.

The rapid development of the emerging sector of instant retail for pharmaceuticals is driven, on one hand, by shifts in consumer behavior. Traditional e-commerce fails to meet the incremental demand triggered by specific life scenarios; for instance, instant retail has become the preferred choice for the younger generation in situations such as sudden nighttime illnesses or when leaving home is inconvenient.

On the other hand, against the backdrop of increasingly stringent healthcare cost-containment policies, the in-hospital market has been squeezed by volume-based procurement (VBP), making the out-of-hospital market a lifeline for pharmaceutical companies. As the most efficient and fastest-growing channel within the out-of-hospital sector, on-demand pharmaceutical retail has become key to driving performance growth and achieving brand premium for pharmaceutical enterprises.

Pharmacies are also facing pressure to transform. Although the number of retail pharmacies across China has reached 700,000, most stores are underperforming financially, prompting pharmacies to view instant retail as a key direction for transformation. The gradual opening of online medication purchasing channels through medical insurance in many regions across China has further boosted the development of instant retail in the pharmaceutical sector.

Market data fully corroborates the robust growth of instant retail in the pharmaceutical sector.According to the latest forecast data from Menet, the sales volume of instant retail in pharmacies reached 48.7 billion yuan in 2024, a year-on-year increase of 31.3% compared with 2023.In terms of the platform landscape, the “Blue Paper on the Development of Instant Retail in the Pharmaceutical Industry” released by Sinohealth shows that Meituan accounted for over 70% of the O2O online-to-offline pharmacy market share by the end of 2024.

To date, the collaboration models between platforms, pharmaceutical companies, and pharmacies have evolved beyond simple supply and advertising relationships into a new stage characterized by multi-party win-win outcomes and joint market development. The level of synergy among the three parties has reached an unprecedented depth, giving rise to various innovative forms of cooperation.For instance, the platform collaborates with pharmaceutical companies and pharmacies to build a joint supply chain, thereby enhancing supply chain efficiency. Additionally, through its flagship store model, the platform helps pharmaceutical and medical device enterprises strengthen their brand influence, addressing the challenge in traditional marketing where brands struggle to reach end users directly.

For another example, the platform captures patients’ true needs through data insights, delivers precise patient education, and even anticipates shifts in demand, thereby providing decision support for pharmaceutical companies’ warehousing, allocation, and supply strategies. Leveraging the platform’s precise user insights, it also helps pharmaceutical companies develop products that better meet the demands of instant retail scenarios. Meituan Medicine has seen the emergence of multiple new small-pack products tailored to immediate and emergency-use scenarios, such as the customized “Compound E-Jiao Syrup (6-sachet pack)” co-launched with Dong-E-E-Jiao, and small-pack hangover-relief products jointly introduced with By-Health’s Jian An Shi brand.

Collaboration Models Among Platforms, Pharmaceutical and Medical Device Companies, and Pharmacies as Key Participants in Instant Retail

Notably, social media platforms represented by Douyin and Kuaishou are becoming significant players in the instant retail pharmaceutical sector. In April 2025, Douyin Instant Retail announced the opening of a self-onboarding channel for pharmacies offering one-hour delivery services. In August, the Kuaishou app added an independent “Food Delivery” entry point under its homepage “Group Buying” section. Although initial product offerings were primarily sourced from third-party partners such as Meituan, this move has laid the foundation for future integration of local pharmacy resources and expansion into the instant retail pharmaceutical market.

Traditional competition has centered on delivery speed, product variety, pricing, and closed-loop services. The entry of social media platforms has elevated content reach and user attention to new competitive factors, prompting platforms to prioritize the construction of content ecosystems while strengthening their service capabilities. Pharmaceutical and medical device companies can also leverage the content-driven nature of social platforms for more precise brand education and product promotion, further enhancing the richness of the industry ecosystem and the diversity of competition.

Pharmacies: Medical Aesthetics and TCM Clinics Are Directions for Exploration

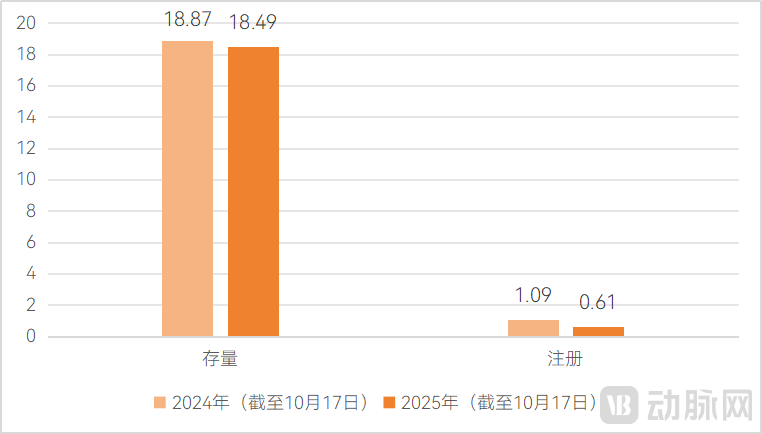

In 2025, the number of pharmacies across China continued to shrink. By the end of the first three quarters, six major pharmacy chains—Yixintang, Yifeng Pharmacy, Laobaixing Pharmacy, Dashenlin Pharmaceutical Group, Jianzhijia, and Shuyu Pingmin—had cumulatively closed 1,927 stores. Data from Qichacha also showed that the total number of pharmacy-related enterprises in China was 506,400. As of October 17, there were 184,900 existing pharmacy-related enterprises, a year-on-year decrease of 2.03%. In 2025, only 6,100 new pharmacy-related enterprises were registered, representing a year-on-year decline of 78.51%.

Changes in the Number of Pharmacies Across China in 2025 (Unit: 10,000)

The model of pharmacies relying on medical insurance is also shaking, with many regions witnessing a wave of pharmacies withdrawing from the medical insurance program. According to incomplete statistics, the number of pharmacies voluntarily terminating their participation in 2025 has exceeded one thousand.

VBInsight observed that in 2025, pharmacies deepened their investment in and reliance on instant retail of pharmaceuticals, which has become a significant growth engine for the pharmacy sector.

Medical aesthetics and traditional Chinese medicine (TCM) clinic services have also become a direction for pharmacies to explore new growth opportunities.In particular, the layout of medical aesthetics has evolved from simple sales of Class II/III medical device products to an integrated model combining “products + services + technology.”

Health Insurance: Mid-Tier Medical Insurance and Accelerated Innovation in Insurance for Individuals with Pre-Existing Conditions

In 2025, the commercial health insurance market accelerated product innovation. According to data from the Insurance Association of China, as of October 16, a total of 1,080 new health insurance products were launched during the year. Against the backdrop of slowing growth in critical illness insurance and intensifying competition in the million-yuan medical insurance sector, the market has exhibited three key directions for innovation:Expanded Coverage, Rise of Mid-Tier Medical Insurance, andExploration of Insurance for Individuals with Pre-existing Conditions。

The expansion of coverage is breaking through the boundaries of traditional medical insurance, extending from in-hospital treatment to whole-disease management. In 2025, health insurance products launched by companies such as Ping An Health Insurance and ZhongAn Insurance generally fully opened up coverage for externally purchased drugs and medical devices, no longer limited to specific lists. Meanwhile, out-of-hospital services such as home nursing and rehabilitation therapy have also been included in the scope of coverage.

The Rise of Mid-End Medical Insurance: Filling the Gap Between Basic Medical Insurance and High-End Medical Care as a Key Strategy for Industry GrowthAs the low-cost insurance market becomes increasingly saturated and new policyholders for critical illness insurance continue to decline, mid-end medical insurance has emerged to fill the market gap between basic medical insurance and high-end medical care, representing a significant industry effort to unlock growth potential. In 2025, companies such as Cigna & CMB, New China Life Insurance, and MSH China launched mid-end medical insurance products. These products emphasize medical experience and service quality, covering premium medical resources including VIP wards, special-needs medical services, special-needs outpatient and inpatient care, and international departments of public hospitals. They are also bundled with value-added services such as green-channel access, specialist appointments, outpatient scheduling, postoperative care, and home nursing services.

Shifting from “Insuring the Healthy” to “Safeguarding Health for All,” Insurance for Individuals with Pre-existing Conditions Emerges as a Strong Contender. The population of individuals with pre-existing conditions continues to grow steadily, creating an urgent need to unlock their insurance demand. In 2025, insurers explored innovations in developing insurance products for this segment. For instance, Taikang Online launched its first commercial medical insurance product tailored for patients with diffuse large B-cell lymphoma (DLBCL), named “Hao Xiao Bao · Songqing Guardian,” which covers the world’s first bispecific antibody therapy and CAR-T cell therapy. Additionally, Shuidi Bao partnered with Junlong Life Insurance to introduce the long-term critical illness insurance product “Popeye,” expanding coverage to include 19 conditions traditionally excluded from underwriting, such as TI-RADS 4a thyroid nodules and HBeAg-positive chronic hepatitis B (“big three positive” hepatitis B).

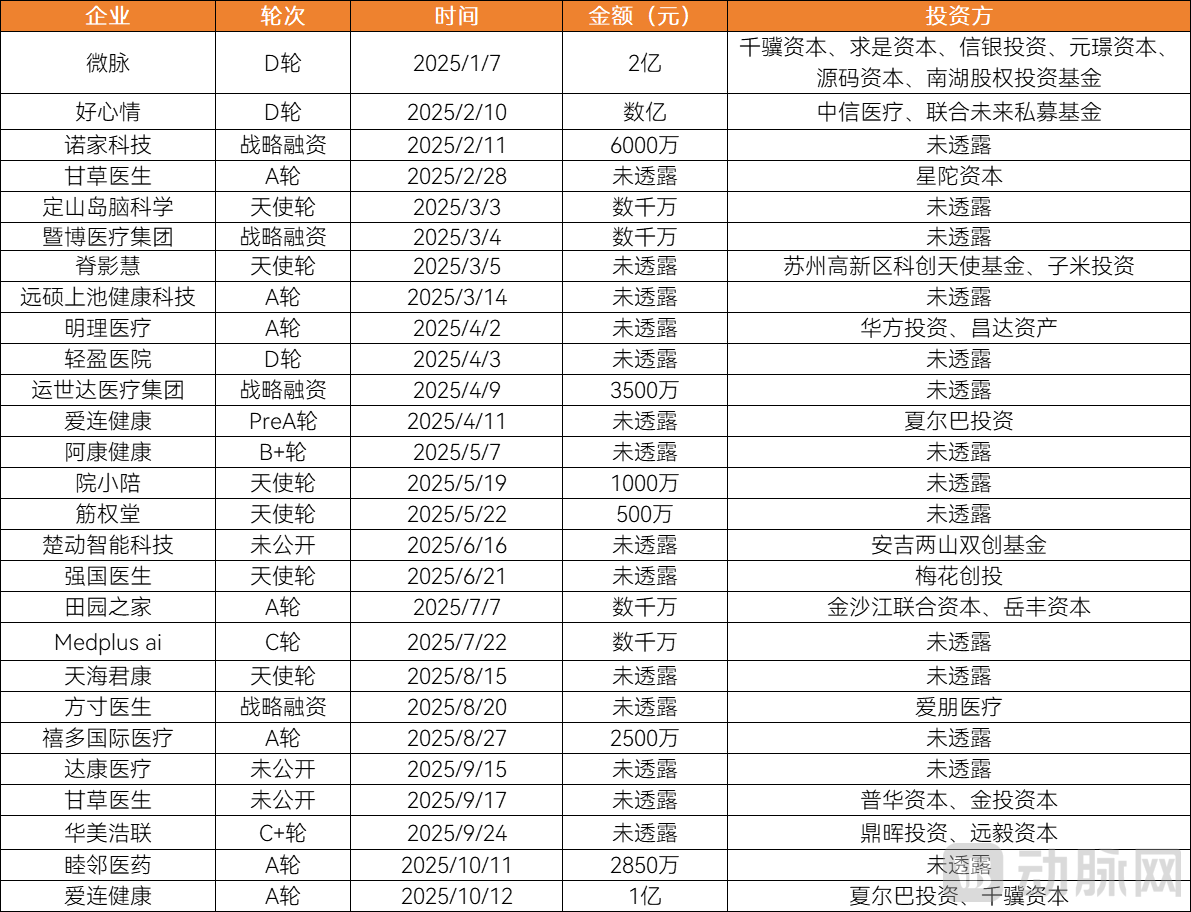

Capital Markets: More Rational Financing, IPOs Show Signs of Recovery

As of mid-October, there were 123 financing deals in the global healthcare services market in 2025. Of these, the Chinese market accounted for 27 deals, with a total financing amount of RMB 814 million, representing approximately 3.8% of the total number of financing events (700 deals) in China’s healthcare sector for the full year. The overseas market was more active, with 96 financing deals totaling USD 6.617 billion, accounting for 8.5% of the total number of financing events (1,132 deals) in the overseas healthcare market for the full year.

2025 Financing Landscape of China's Domestic Healthcare Services Market

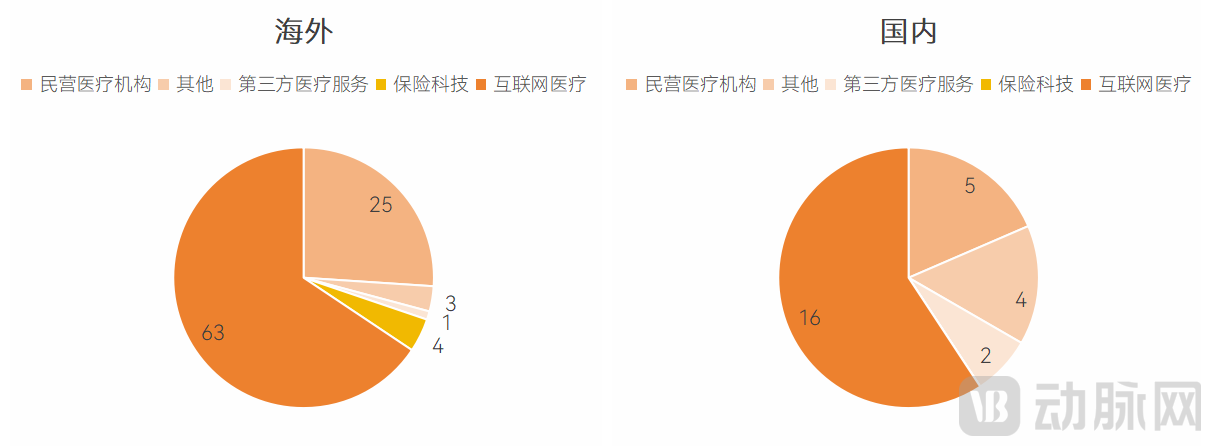

Distribution of Healthcare Service Financing by Sub-sector in 2025

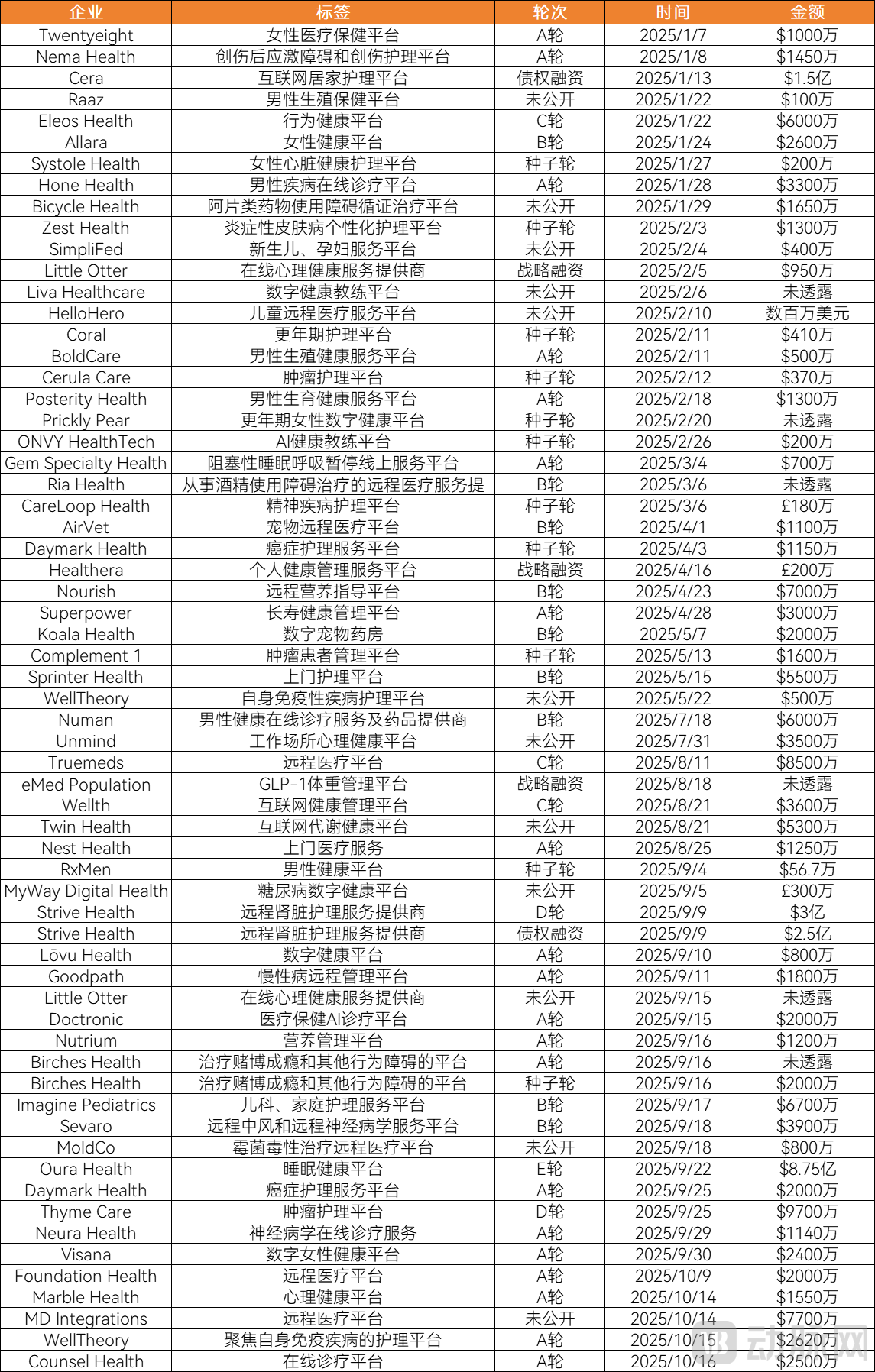

In the domestic internet healthcare sector, capital has shown a preference for health management, home-based care, and traditional Chinese medicine. Overseas markets have demonstrated stronger specialization characteristics, with the specialized nursing sector completing 51 financing rounds. Among these, women’s health platforms secured seven deals, men’s health platforms six, while mental health platforms and oncology care platforms each completed five. Furthermore, numerous highly vertical platforms have garnered favor from overseas investors, such as eMed Population Health, which focuses on weight management; Ria Health, which provides treatment for alcohol use disorder; and Gem Specialty Health, which specializes in obstructive sleep apnea.

Overseas Internet Healthcare Sector Financing Trends

In the field of private medical institutions, five financing deals in the domestic market were distributed across five niche sectors: dentistry, traditional Chinese medicine (TCM), assisted reproduction, mental health, and elderly care. Overseas private medical institutions recorded a total of 25 financing deals, predominantly among clinics, with a significant trend toward specialization. Companies secured funding across a broad spectrum of specialties, ranging from women’s health, orthopedics, and rehabilitation to intravenous therapy, pediatrics, ophthalmology, gynecology, and even Alzheimer’s disease care.

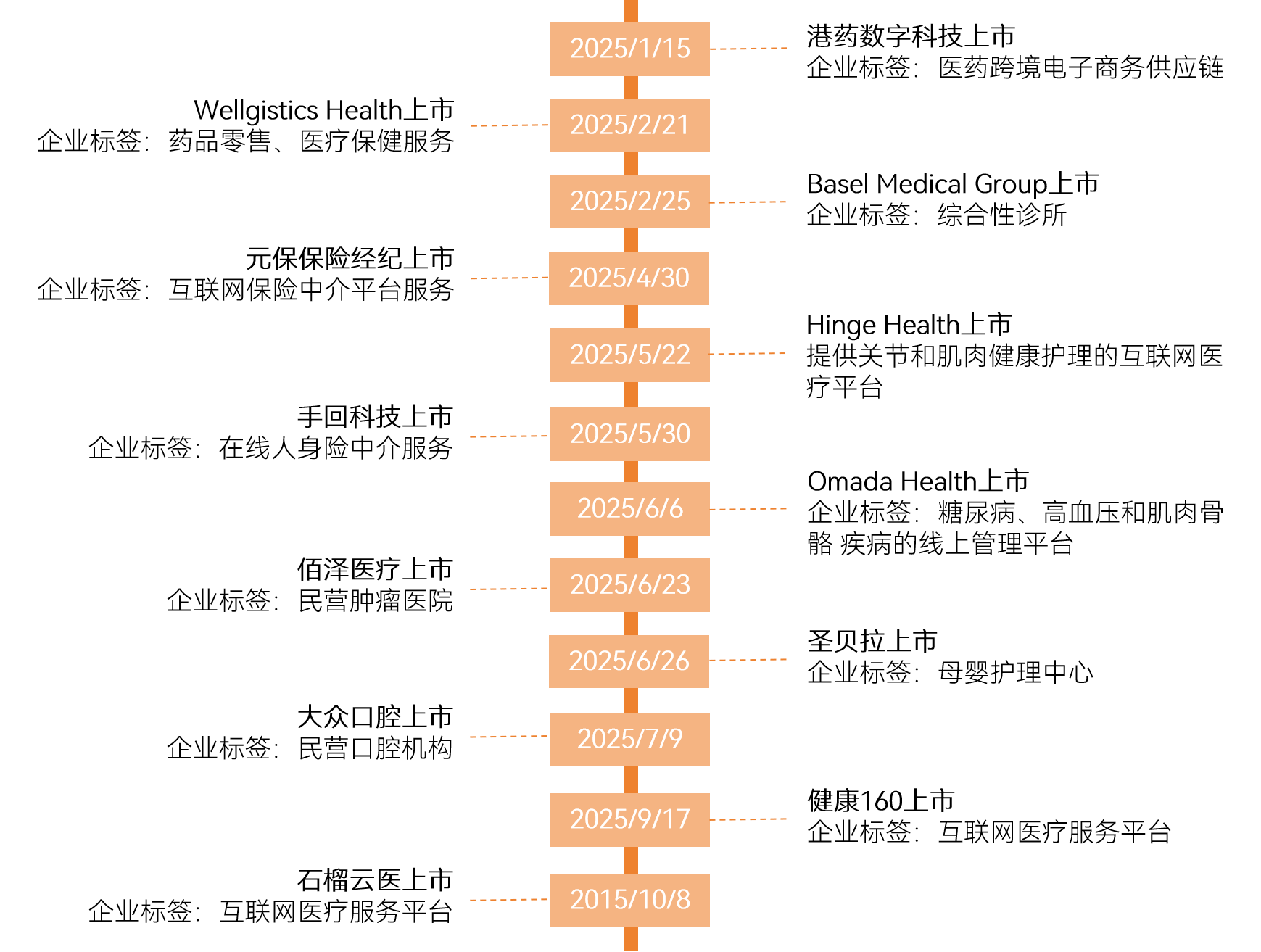

In 2025, the IPO segment for healthcare services showed signs of recovery. As of October 2025, a total of eight companies in China had successfully gone public, covering sectors such as internet healthcare, insurtech, private oncology hospitals, cross-border pharmaceuticals, private dental clinics, and maternal and child care centers. Overseas, four healthcare service companies entered the capital markets, including two internet healthcare firms. Compared with 2024, the number of newly listed companies both domestically and internationally increased, sending a positive signal to the market that the industry as a whole is rebounding.

Newly Listed Companies in the 2025 Healthcare Services Market

The healthcare services market is vast and diverse, with significant variations in development across its various segments. Some areas are experiencing accelerated growth driven by rising demand and technological innovation, while others face pressure due to intensifying market competition and challenges to their profitability models.

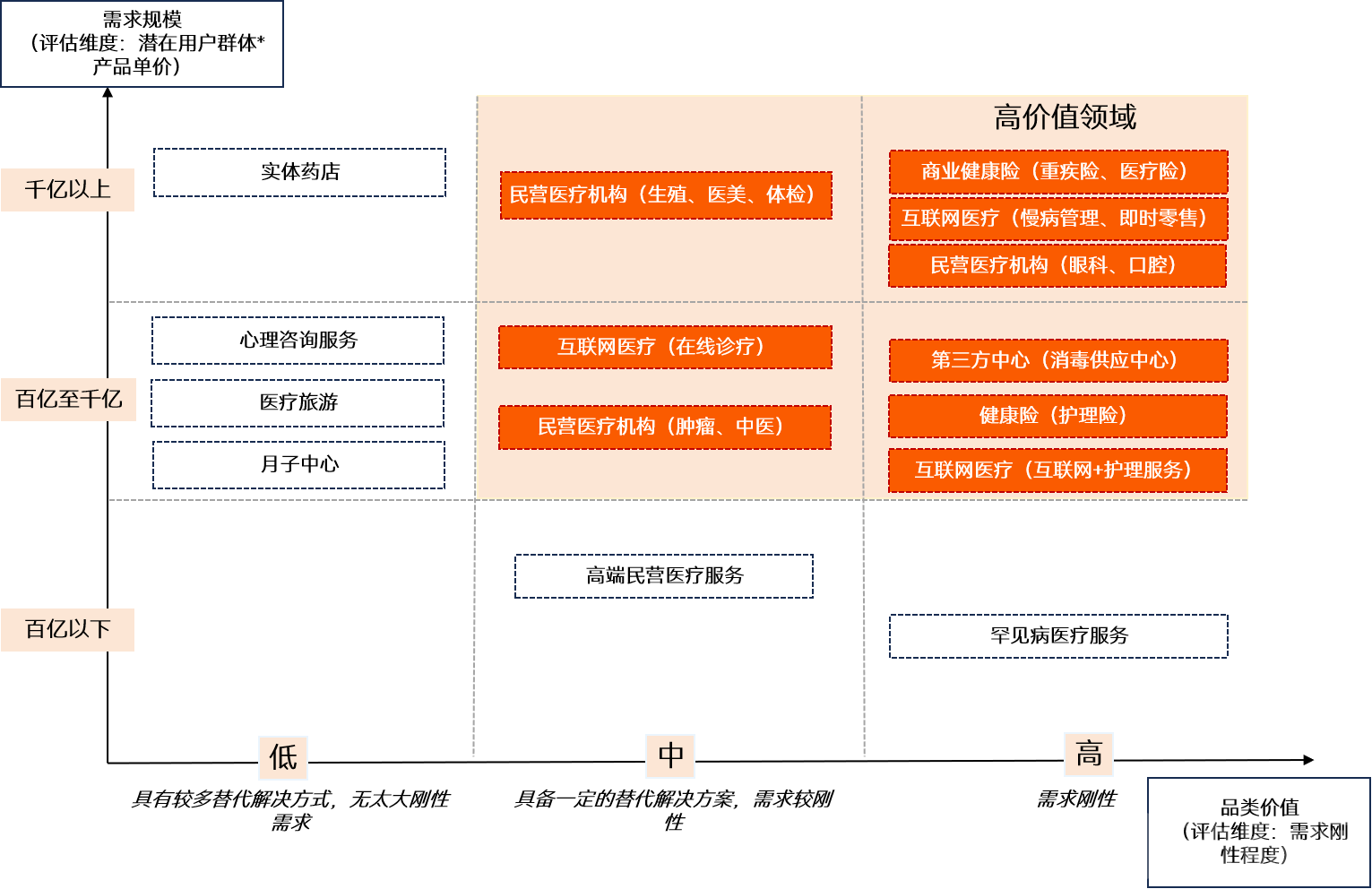

In this context, identifying high-value segments with substantial market size and inelastic demand from the myriad of specialized fields is of significant importance to investors and entrepreneurs. VBInsight attempts to evaluate the value of healthcare service sub-sectors from two perspectives: “market size” and “demand inelasticity.” The study finds that pharmaceutical instant retail and “Internet + nursing services” within the internet healthcare sector; ophthalmology, reproductive health, medical check-ups, and dentistry within the private healthcare sector; and sterile supply centers within the third-party medical services sector exhibited typical characteristics of high-value segments in 2025.

Selection Criteria for High-Value Subsectors in Healthcare Services

Based on the analysis of innovation logic and corporate practices across various high-value sectors presented in the white paper, ten outstanding innovation case studies of the year have been selected. (The above is an excerpt from the main content of the white paper; scan the QR code below to access the full report.)

The following is the report table of contents:

Chapter 1: Overview of Hot Topics in the Medical Services Industry in 2025

1.1 Policy: Major Breakthroughs in Commercial Insurance Coverage for Innovative Drugs and Drug Price Governance

1.2 Vast Market Foundation, Industry Scale Exceeds 10 Trillion

1.3 Corporate Business and Product Dynamics: Digital Intelligence, Specialization, and Expansion of Business Boundaries Are the Main Themes

1.4 Capital Markets: More Rational Financing, IPO Market Shows Signs of Recovery

Chapter 2: Insights into the Most Valuable Fields and Product Competitiveness in 2025

2.1 Private Healthcare: Ophthalmology, Reproductive Medicine, Dentistry, and Health Checkups Are in a Phase of Rapid Growth

2.1.1 Private Ophthalmic Institutions: Transformation Under Pressure—Optometry, M&A, and High-End Technologies as Key Breakthroughs

2.1.2 Innovation in Clinical Practice and Business Models for Private Reproductive Health Institutions in the Era of Medical Insurance Coverage

2.13 Private Health Checkups: Intensified Competition as Leading Enterprises Enter a New Phase of Full-Life-Cycle Health Management

2.1.4 Private Dental Care: Anchoring in AI and Talent System Development Amid Short-Term Pain and Long-Term Opportunities

2.2 Third-Party Medical Services: A Hundred-Billion-Yuan Market in Sterile Supply, with Untapped Potential

2.3 Internet Healthcare: Driven by Policy and Demand, with Prominent Value in “Internet + Nursing Services” and Instant Retail Scenarios

2.3.1 The High-Value Logic of “Internet+ Nursing Services”: Policy Support, Clear Demand, and Multi-Party Win-Win

2.3.2 On-Demand Retail of Pharmaceuticals: A Key Growth Market Evolving from a Retail Channel into a Health Services Ecosystem

Chapter 3: Top 10 Predictions for the Healthcare Services Industry in 2026

3.1 Market and Operational Trends

3.2 Service and Product Trends

3.3 Capital Trends: From Broad Spraying to Focused Investment