Why are medical companies rushing "North" as 33 pass in Q1?

Recently, AIM Vaccine, a leading vaccine company in the Hong Kong stock market, announced that it has formally applied for A-share listing on the Beijing Stock Exchange. If the process goes smoothly, AIM Vaccine will become the first stock to return from the Hong Kong Stock Exchange to the Beijing Stock Exchange.

In fact, this is not a seemingly "reasonable" decision: on the one hand, the mainstream trend in the current market is for A-share companies to go public in Hong Kong, while there are very few cases of returning from the Hong Kong stock market to the A-share market. So far, there have been less than 10 disclosed successful cases; on the other hand, it depends on the choice of trading market. According to publicly available information, Hong Kong-listed companies returning to the A-share market mainly focus on the main board and the STAR Market, such as BeOne Medicines, Junshi Biosciences, and CanSinoBIO, etc., all of which chose the STAR Market for their "return to A", while the Beijing Stock Exchange has been almost "ignored".

Therefore, this reverse selection by AIM Vaccine has also drawn significant market attention to the Beijing Stock Exchange (BSE). However, a closer look reveals that the BSE has now become a new battleground for medical companies rushing to go public.

Figure 1. Medical Enterprises Successfully Listed in Q1 2026

Figure 1. Medical Enterprises Successfully Listed in Q1 2026

According to publicly available information, in the first quarter of 2026, 10 companies in China's medical field have successfully gone public, of which 4 were listed on the Beijing Stock Exchange, namely Excellent Medical, AND, Hisern Medical, and Promisemed Medical. The number of listings is on par with the hot Hong Kong stock market. Additionally, regarding companies in the queue for listing, the Beijing Stock Exchange currently has 16 healthcare listings under review. Although the number is smaller than that of the Hong Kong stock market, it still ranks first in A-shares, and the recent upward trend is obvious.

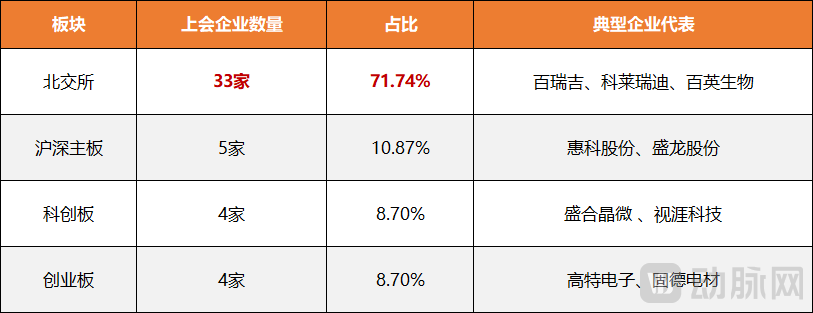

Figure 2.2026: Number of Listings on Major Trading Sectors of A-Share Market in Q1

Figure 2.2026: Number of Listings on Major Trading Sectors of A-Share Market in Q1

If we zoom out to look at the entire industry, the Beijing Stock Exchange (BSE) stands out remarkably. In 2025, the BSE accepted listing applications from 176 companies, a staggering 167% increase from 66 in 2024, surpassing the combined total of 124 from the other boards of the Shanghai and Shenzhen stock exchanges. Entering the first quarter of 2026, the three major exchanges in Shanghai, Shenzhen, and Beijing welcomed 46 companies for their initial public offering hearings. Among them, the Beijing Stock Exchange tops the list with 33 companies that attended IPO hearings, accounting for a whopping 71.74%, becoming the absolute main force in IPO reviews in the first quarter. As of March 20, 2026, the number of existing listed companies on the Beijing Stock Exchange has officially broken through the 300 mark, and has, without a doubt, become the most dynamic growth pole in China's IPO market.

Thus, a key question is rapidly fermenting in the industry: Why has the Beijing Stock Exchange risen so strongly? Why are healthcare companies choosing to flock northward now? What capital logic and changes in IPO trends does this reveal?

Why Are Medical Companies Collectively "Switching Lanes" to the Beijing Stock Exchange?

On November 15, 2021, the Beijing Stock Exchange (BSE) officially opened for trading, primarily targeting a group of "specialized, refined, distinctive, and innovative" enterprises. On the opening day, the BSE "welcomed" 81 listed companies at once, with 71 being companies transferred from the Select Layer of the National Equities Exchange and Quotations (NEEQ), and the other 10 being new stocks directly listed on the BSE. As a key coverage area, medical companies accounted for 10 of the first batch of listed companies on the BSE, including Tri-Prime Gene, Northland Biotech, and Senxuan Pharmaceutical.

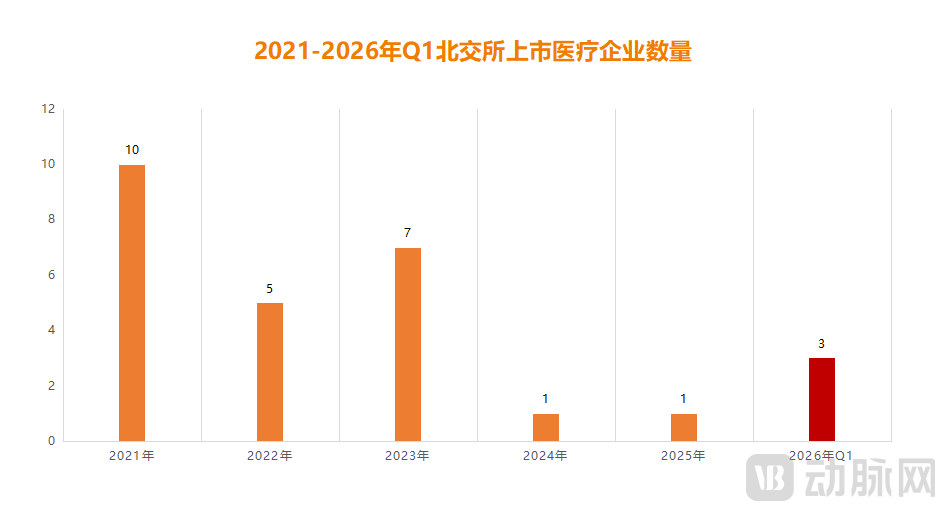

Figure 3. Number of Medical Enterprises Listed on the Beijing Stock Exchange (Q1 2021-2026)

Figure 3. Number of Medical Enterprises Listed on the Beijing Stock Exchange (Q1 2021-2026)

In the following years, medical stocks on the Beijing Stock Exchange (BSE) gradually dropped from their peak to the bottom, following the industry's development trend. In 2022 and 2023, the BSE welcomed a total of 12 listed medical enterprises, showing extremely high market expansion. However, entering 2024 and 2025, the situation took a sharp downturn. For two consecutive years, there was only one listed company each year on the Beijing Stock Exchange, namely Chemsyn Pharm in 2024 and Dynamiker Biotechnology in 2025.

Figure 4. Current Status of Medical Enterprises in the Queue for Listing Review on the Beijing Stock Exchange (Data Source: Official Website of the Exchange)

Figure 4. Current Status of Medical Enterprises in the Queue for Listing Review on the Beijing Stock Exchange (Data Source: Official Website of the Exchange)

Finally, in 2026, this situation saw a reversal. In just the first quarter of the year, four medical companies went public, twice the total number of the past two years. Additionally, there are currently 16 medical enterprises in the pipeline awaiting review. At the current review speed and pace of the Beijing Stock Exchange, all of them are expected to complete the listing process within this year.

So, what triggered this change? To answer this question, we must work backward based on the listing demands of medical enterprises.

The first point is the success rate of going public. In fact, a significant reason for the boom in Hong Kong stocks is that "18A" allows a group of unprofitable biotech companies to go public. Although the Beijing Stock Exchange mainly targets profitable healthcare enterprises, in recent years, with the restart of the fifth set of standards on the STAR Market, it has also been gradually relaxing the listing restrictions for unprofitable companies. It has started to focus on and support a group of innovative healthcare enterprises with core technologies and outstanding growth potential.

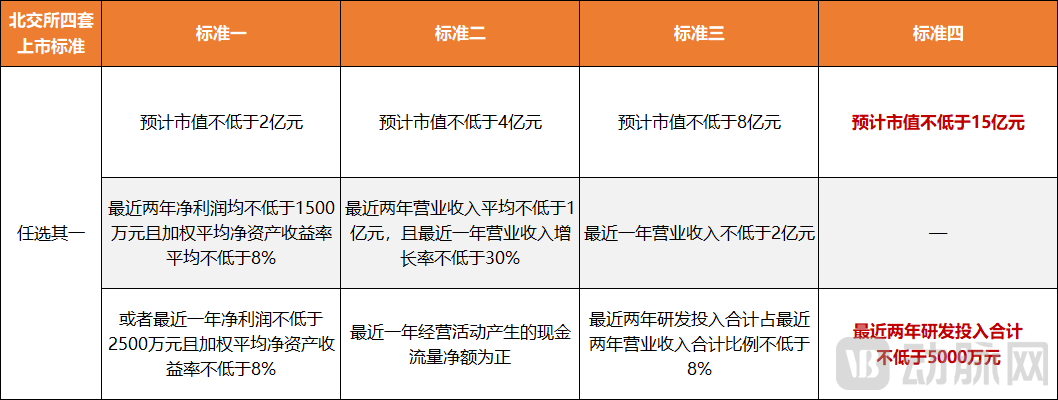

Figure 5. The "Four Sets" of Listing Standards of the Beijing Stock Exchange

Figure 5. The "Four Sets" of Listing Standards of the Beijing Stock Exchange

Take Health Guard, which successfully listed on the Beijing Stock Exchange in August 2025, as an example. Due to its products not being fully commercialized, it has been operating at a long-term loss, and even incurred losses exceeding RMB 100 million within the six months prior to listing. However, it still met the fourth set of listing standards of the Beijing Stock Exchange, namely, "an estimated market value of no less than RMB 1.5 billion, with combined R&D investment in the last two years of no less than RMB 50 million." This enabled Health Guard to become the first innovative enterprise to list on the Beijing Stock Exchange using "Standard Four." It is reported that among the nearly 300 listed companies currently on the Beijing Stock Exchange, only five companies adopted the third or fourth set of standards, three of which are biopharmaceutical companies, namely Health Guard, Northland Biotech, and Sunho Pharmaceutical.

In addition to easing restrictions, the review efficiency of the Beijing Stock Exchange (BSE) is also increasing significantly. In March alone, 12 companies passed the review meeting at the BSE, setting a new high for the number of companies reviewed in a single month since its establishment. Specifically in the medical field, the fastest review to date is for Hisern Medical, which has just been listed. It took only 162 days from acceptance to approval, setting a record for the fastest review this year. This is largely due to the "Direct Link Mechanism" launched by the BSE, which involves centralized management of the entire chain of review, supervision, and service work for directly linked companies within the BSE and the National Equities Exchange and Quotations (NEEQ). This mechanism supports directly linked companies in swiftly completing their issuance and listing processes after being listed for one year, significantly reducing the time cost of going public and substantially lowering listing expenses.

Secondly, the valuation and liquidity of the exchange itself need to be considered. In contrast to Hong Kong stocks, the A-share market represented by the Beijing Stock Exchange is mainly driven by both "institutions and retail investors," which usually results in higher valuation levels and liquidity for A-share listed companies. According to the latest data, A-share valuation is usually 20% to 40% higher than that of Hong Kong stocks, while in terms of liquidity, the average daily turnover rate of A-shares is typically three to five times that of Hong Kong stocks. Taking Biocytogen, which landed on the STAR Market from the Hong Kong stock market in December 2025, as an example, its A-share price has risen more than twice the issue price and is over 90% higher than its Hong Kong stock price.

This is actually very important. On the one hand, a high valuation means that more funds can be raised at the same level of profitability, providing sufficient "ammunition" for subsequent R&D investment and commercialization processes. On the other hand, good market liquidity can also provide a smooth market environment for corporate refinancing, merger and acquisition integration, and orderly exit of early investors, promoting further growth. Therefore, for a group of medical companies that have not yet turned a profit or are at a critical stage of R&D, choosing a market with better valuation and liquidity can not only effectively solve survival issues but also seize the initiative in fierce industry competition.

The last point is the "additional effect" after listing. Taking the Hong Kong stock market as an example, the reason many medical enterprises are willing to choose it as their listing destination is not only because it allows unprofitable companies to go public, but also because it can serve as a crucial springboard for accessing overseas markets. It can help medical enterprises expand international operations, enhance global brand influence, and leverage Hong Kong's position as an international financial center to connect with global capital.

Unlike Hong Kong stocks, A-shares represented by the Beijing Stock Exchange focus on deep cultivation of the local market. Therefore, they can not only help listed medical enterprises integrate upstream and downstream resources, enhancing collaboration efficiency with local medical institutions, supply chains, and research platforms, thereby forming stronger industrial chain synergies, but also allow them to benefit from various policy incentives. In addition to gaining easier access to targeted support such as local government industrial funds, tax preferences, and R&D subsidies, A-share listed medical enterprises also enjoy numerous advantages in terms of regulatory approval. These include the priority review channel for innovative medical devices, dynamic adjustment and alignment with the national medical insurance catalog, and green channel policies for online procurement of drugs and consumables by listed companies in some regions. All of these can accelerate the market transformation process of products from research and development to clinical application.

This shows that the current collective "northward movement" of medical enterprises is actually the result of multiple factors working together. As the influence of the Beijing Stock Exchange grows, it is becoming an important listing ground for China's medical innovation enterprises and is gradually reshaping the entire medical IPO landscape.

Who is "Going North"?

Currently, the Beijing Stock Exchange (BSE) remains dominated by medical device companies. For instance, the four healthcare companies that successfully listed this year all belong to the device sector. Additionally, among the 16 healthcare companies currently in the BSE's pipeline for review, over 60% are from the device field, maintaining a dominant position.

A further analysis shows that these medical device companies targeting the Beijing Stock Exchange are mainly concentrated in sectors such as high-value consumables represented by orthopedic implants and vascular intervention, medical imaging and equipment, in vitro diagnostics, as well as rehabilitation and home medical devices. Focusing on imaging equipment as an example, typical representatives include ChenGuang Medical, NovelBeam, and Klarity.

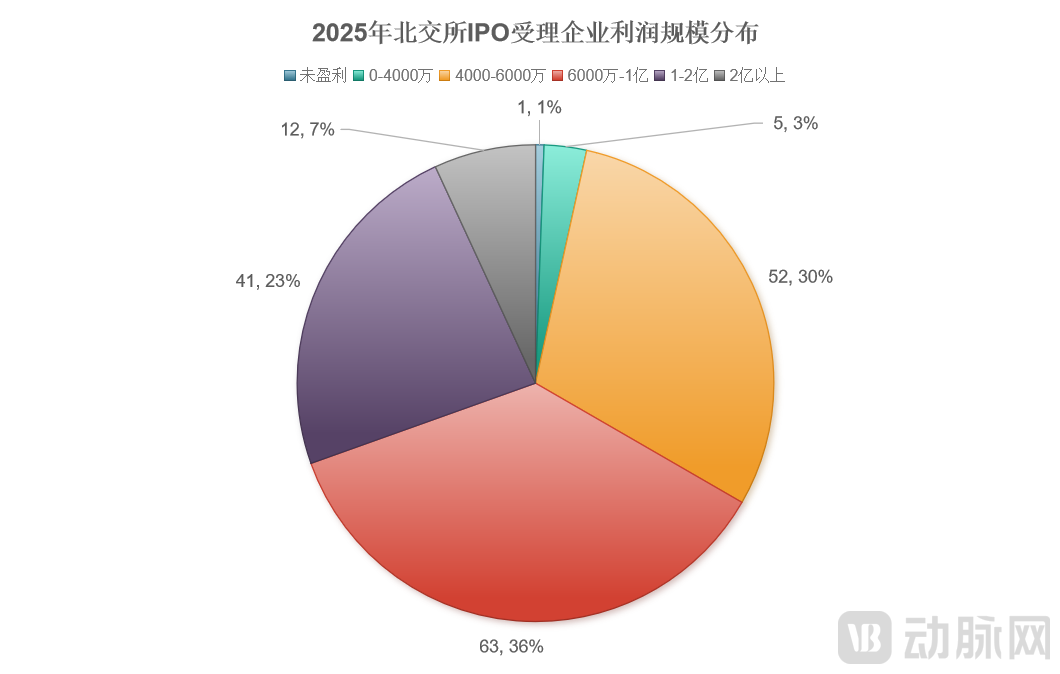

Figure 6. Profit Scale of Companies Accepted by the Beijing Stock Exchange in 2025 (Data Source: Annual Reports of Companies)

Figure 6. Profit Scale of Companies Accepted by the Beijing Stock Exchange in 2025 (Data Source: Annual Reports of Companies)

The formation of this situation certainly has its reasons. First, in terms of listing thresholds, although both the Hong Kong Stock Exchange and the Beijing Stock Exchange allow unprofitable medical companies to go public, in actual implementation, the Beijing Stock Exchange remains relatively strict. It typically exercises extreme caution when reviewing the "commercialization cycle" and "market potential." Compared to innovative drugs, medical device companies generally have shorter R&D cycles and more controllable market risks, making it easier for them to achieve profitability and meet the Beijing Stock Exchange's rigid requirements for net profit. According to the latest statistical data, in 2025, the 300 listed companies on the Beijing Stock Exchange achieved an average net profit of RMB 43.3248 million, with an overall profitability rate as high as 83.39%. In stark contrast, more than 80% of the companies in the Hong Kong Stock Exchange's 18A sector were in a loss-making state.

Secondly, considering the actual needs of listed companies, unlike most innovative pharmaceutical enterprises, medical device companies, after completing the construction of their main product lines and obtaining the necessary certifications, generally require around RMB 200 million to RMB 500 million in capital at each stage, which can precisely support their new product R&D, market promotion, and capacity expansion for the next two to three years. As everyone knows, the initial public offering (IPO) financing amount on the Beijing Stock Exchange is relatively small, with most fundraising amounts concentrated in the range of RMB 200 million to RMB 500 million. However, this precisely meets the demand. Additionally, a smaller financing amount also means less equity dilution, often allowing medical device companies to retain more autonomy and control after going public.

The last point is related to the "resources" behind the exchange. In fact, most innovative pharmaceutical companies strive to list on the Hong Kong Stock Exchange mainly because they value the advantages of its international platform, which can support pharmaceutical companies in business development (BD), overseas clinical development, and global financing. Medical device companies also have the need to expand overseas, but the majority of their business models at this stage still rely more on the domestic supply chain. The Beijing Stock Exchange is closer to the localized industry and has a relatively stable valuation system, making it a more preferred listing path for many medical device companies.

So, how did they perform after going public?

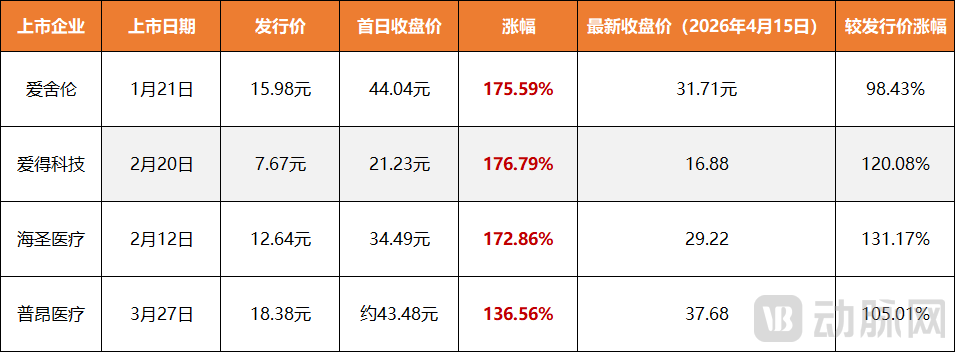

Still taking the four medical device companies that have gone public this year as examples, all of them experienced significant increases on their first trading day, with an average increase of over 165%. Among them, AND demonstrated the strongest momentum, surging 225.95% at the opening and reaching a maximum increase of 238.98%. By the end of the first trading day, the increase remained as high as 176.79%.

Figure 7.2026: Valuation Changes of Four Medical Companies Listed on the Beijing Stock Exchange

Figure 7.2026: Valuation Changes of Four Medical Companies Listed on the Beijing Stock Exchange

This is not a fleeting phenomenon. Currently, the share prices of four listed companies have increased by more than 100% compared to their issue prices. Taking Excellent Medical, the earliest listed company, as an example, its share price closed at 31.71 RMB on April 14, 2026, marking a 98.4% increase from its issue price of 15.98 RMB. This indicates that the four listed companies have successfully transitioned in value from the primary market to the secondary market and secured substantial cash flow support.

In addition, at the product operation level, the four listed companies have also made substantial strategic progress. For instance, AND launched a strategic investment in robotic-assisted systems for orthopedic surgeries within three months of its IPO, while Excellent Medical raised funds through a private placement to expand its high-end rehabilitation and nursing product line. This shows that the Beijing Stock Exchange not only provides an IPO channel for medical enterprises but also helps companies achieve technological upgrades and industrial chain expansion through capital tools.

Of course, everything has its pros and cons, and the Beijing Stock Exchange also has its own limitations. For example, the small initial public offering (IPO) financing amount mentioned earlier is one aspect, while another aspect includes strict regulatory standards and ongoing financial pressure. In this regard, a senior insider stated, "'Returning to A-share' means that enterprises will have to bear higher compliance costs, face stricter performance expectations, and more intense market competition. In addition, a large number of medical enterprises are concentrated in the Beijing Stock Exchange for listing, which may also lead to liquidity dilution in certain sectors, and high valuation targets are susceptible to market sentiment.”

Therefore, some medical enterprises are reluctant to switch to the Beijing Stock Exchange (BSE) even after multiple setbacks in the Hong Kong stock market. Take, for example, an innovative pharmaceutical company that faced obstacles in its Hong Kong IPO. Despite having multiple anti-tumor drug candidates in its R&D pipeline, it ultimately chose to remain in the Hong Kong market due to the BSE's substantive requirements for commercialization prospects and profitability. Another case is a medical device company that, despite being profitable, still has significant demand for external financing. The relatively lower fundraising amount available on the BSE clearly fell short of expectations, forcing the company to persist with the Hong Kong market. Additionally, some medical enterprises are concerned about the procedural complexity and time costs involved in moving from the Hong Kong market back to the A-share market ("returning to A"). This further diminishes their willingness to shift to the BSE.

Therefore, every trading market has its pros and cons. How to choose? It still needs to be comprehensively judged based on the development stage, current core needs, and future strategic goals of the medical enterprise.

Going Public is Not the End, but a New Beginning

After experiencing the capital winter in 2023 and 2024, the entire medical IPO market in China rapidly recovered in 2025. Thirty-seven medical enterprises went public throughout the year, more than double the number in 2024. Entering 2026, this momentum continues and becomes even hotter . In just the first quarter of this year, there have already been 10 listed medical companies, an increase of 233.33% compared to the same period in 2025.

This is undoubtedly a positive signal, but it must also be recognized that going public is only a phased victory, representing that medical enterprises have obtained the "ticket" to enter the capital market. Whether they can gain continuous recognition in the secondary market and truly realize value in commercialization, avoiding falling into the curse of "peak at listing," is the core issue that medical enterprises need to face going forward.

Therefore, medical enterprises, when going public, are no longer pursuing simple capital operations and short-term wealth creation, but rather focusing more on deep-seated value and demand. For instance, the current trend of medical enterprises flocking "northward" vividly illustrates this shift. Essentially, it reflects companies' rational decisions based on their development stage, market strategy, and valuation recovery needs, marking a significant shift from "financing for survival" to "value creation."

Figure 8. Representative Cases of "A+H" Medical Enterprises

Figure 8. Representative Cases of "A+H" Medical Enterprises

Besides, more medical enterprises are also embarking on an "A+H" dual capital platform layout. In the past, it was common for A-share medical companies to be listed on the Hong Kong stock market. Currently, there are as many as 20 successful cases, including typical representatives such as Fosun Pharma, Hengrui Medicine, Tigermed, and Shanghai Pharmaceuticals. According to previous data statistics from VCBeat, there are currently more than 10 A-share medical companies launching efforts to be listed on the Hong Kong Stock Exchange, indicating that this scale of listings will continue to expand.

In the past two years, some Hong Kong-listed medical companies have also been returning to China's A-share market. For instance, the recent vaccine leader AIM Vaccine, followed by Duality Biologics which is accelerating its "return to A-shares," and Biocytogen, which has successfully landed on the STAR Market. These companies have all taken a crucial step in moving from Hong Kong's "18A" to diversified A-share listing channels, showing strong expectations for policy dividends in China's capital market, valuation recovery potential, and improved liquidity.

In response, a seasoned expert who has long focused on the secondary market commented, "As the positioning of the two trading markets becomes clearer, and as the connectivity mechanism between them continues to improve and deepen in integration, the 'A+H' dual capital platform structure will inevitably become a new strategic choice for domestic medical enterprises on the listing front. Moreover, the differentiated goal of 'listing in Hong Kong, amplifying value in A-shares' will translate into an increasingly smooth capital pathway."

What can be clearly observed is that within the IPO window of the entire medical sector, the industry is accelerating its transformation toward a "value-driven" model. Both medical enterprises and investors are no longer chasing short-term gains but are beginning to focus more on the long-term value creation and sustainable development potential of companies.