2025 Annual Innovation White Paper on Medical Devices and Supply Chain: Industrial Transformation Driven by Innovation, Global Expansion, and Payment Restructuring

In 2025, China’s medical device industry is demonstrating significant resilience in its recovery and a clear new trajectory for growth, following a period of profound adjustment and structural reshaping. Confronted with the substantial rigid demand driven by an increasingly aging population and the deepening landscape of global competition, the industry as a whole is moving towardValue InnovationandGlobalization Capabilitiesa high-quality development stage centered on . WithArtificial IntelligenceThe technological revolution, represented by these innovations, is deeply embedded in the entire process from diagnosis to treatment, becoming the most core variable driving industrial upgrading.

VBInsight has observed that the underlying logic of industry development has undergone a profound shift: first,The growth engine has completed its gear shift., the scale-driven dividends of traditional products are slowing down, while those with genuine clinical valueOriginal Innovative Productsare emerging in large volumes and rapidly scaling up, with technology-driven growth replacing channel-driven growth as the core engine. Secondly,The Industry Landscape Is Undergoing Strategic Reshaping, domestic mergers and acquisitions have accelerated the emergence of platform-based industry leaders, while deep cultivation of overseas markets has fostered the nascent formation of Chinese multinational corporations (MNCs) in the medical device sector that are breaking into international markets through original innovation. Third,Payment and MarketEnvironmentContinuous Optimization, while the volume-based procurement policy has become more rational and moderate as it expands its coverage, the robust growth of commercial health insurance has jointly created a more favorable space for value realization of high-value innovative medical devices.

To systematically analyze this evolutionary trajectory, the VBInsight team interviewed representatives from multiple frontline innovative enterprises. Drawing on their practical experiences and insights, this report provides an in-depth review of the key industry changes in 2025 across macroeconomic conditions, policy access, sector rotation, capital flows, and global expansion, while also offering a forward-looking perspective on future trends. We firmly believe that the medical device industry is a sector with long-term potential and substantial returns; only those who adhere to the essence of innovation and possess a deep understanding of both clinical needs and the global market can navigate economic cycles and lead the next wave of growth.

01-2025 Overview of Hot Topics in the Medical Device and Supply Chain Industry

Industry PanoramaAtlas: Industry Stabilizes, Advancing with Resilience

Since 2021, China’s medical device industry has gradually entered a phase of structural adjustment following growth fluctuations driven by the pandemic and centralized volume-based procurement. In 2025, despite phased challenges faced by certain sectors and enterprises, the industry as a whole has demonstrated strong resilience, with its market size continuing to expand.Despite the slowdown in growth, China remains the world’s second-largest single-country medical device market.Over the next five years, we expect the overall industry to maintain a single-digit compound annual growth rate, with the total market size of China’s medical device sector reaching RMB 570 billion by 2030.

Market Size Forecast of China's Medical Device Industry (in RMB 100 million, ex-factory price, tax-exclusive)

Data sources: IQVIA, public information, VBInsight

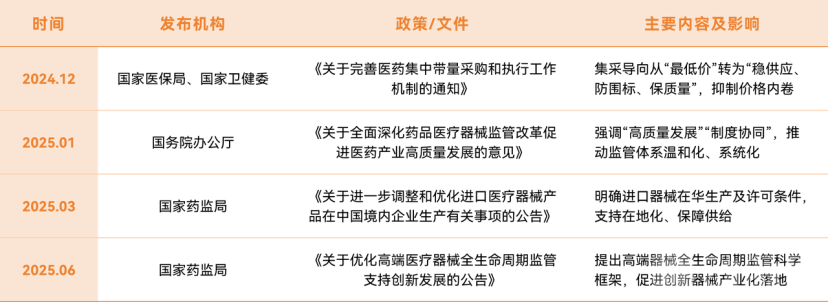

Policy Changes: The Main Tone Continues to Promote Innovation, Stabilize Supply, Improve Quality, and Reduce Ineffective Involution

In 2025, China’s regulatory and industrial policies for medical devices exhibited a trend of transitioning from “high-pressure regulation and price bargaining” to “institutionalized, tiered, and moderate support.” The national regulatory focus is gradually shifting from short-term competition driven by speed and low prices to“Clinical"Value, Quality Assurance, Stable Supply, and Innovation Promotion"the establishment of long-term mechanisms centered on this core. While curbing low-quality involution, the policy framework fosters a more rational and predictable industry environment by optimizing review pathways, encouraging localized production, adjusting centralized procurement mechanisms, and strengthening full-lifecycle regulatory oversight.

2025 Partial Medical Device Policies

Data source: Public information, VBInsight

Industry and Capital Markets: Reshaping and Recovery, with High-Tech Leading a New Cycle in Medical Device Investment

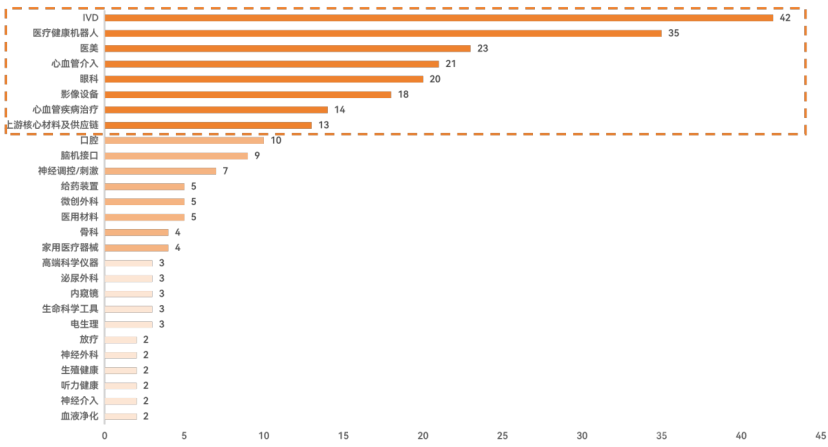

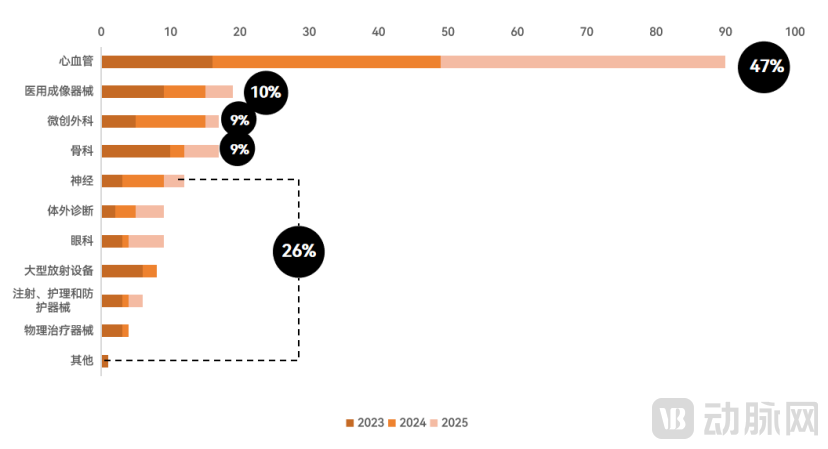

Primary Market Sees Moderate Recovery, with Investment Preference for "High-Tech" Sectors.Despite the overall cautious investment and financing environment, the medical device sector, characterized by clear clinical value and technological barriers, continues to demonstrate strong capital appeal. Financing data from 2025 shows that healthcare robotics, cardiovascular intervention, medical aesthetics, ophthalmology, and imaging equipment ranked as the top five sectors in terms of the number of financing deals, reflecting a trend of capital concentration in high-barrier fields. Among financing rounds exceeding RMB 100 million, high-value sectors such as medical robotics, brain-computer interfaces, ophthalmology, and medical aesthetics also performed prominently, further confirming this structural preference.

Number of Financing Events in Medical Device Sub-sectors from January to October 2025

Data source: Arterial Orange, public information

IPO Regulation Sends Positive Signals, Reshaping the Valuation Framework for Innovative Enterprises.In 2025, the initial public offerings (IPOs) of medical device companies sent multiple positive signals. First, the pace of IPO reviews accelerated; relevant sponsor representatives reported that their projects received approval documents within two weeks after passing the review meeting, marking a significant improvement in review efficiency compared to the previous timeline, which often spanned hundreds of days. Second, the fifth set of listing standards on the STAR Market was reinstated, and the first medical device company successfully passed the review under these standards. This development has bolstered the confidence of medical device firms with breakthrough innovative technologies but weak short-term profitability in their pursuit of listings in the secondary market.

M&A Logic Deepens, Driven by “Product Enhancement” and “Global Expansion” to Fuel Industry Consolidation.In 2025, M&A activity in the global medical device industry revealed a clear strategic landscape. The Chinese market sought breakthroughs amid stability, while the global market continued to witness intense competition as industry giants fortified their moats through targeted acquisitions. The underlying logic was highly consistent: leading companies pursued deep strategic synergies via M&A, aiming to leverage these transactions with maximum efficiency to address critical gaps, secure high-growth sectors, or reshape their industrial niches.

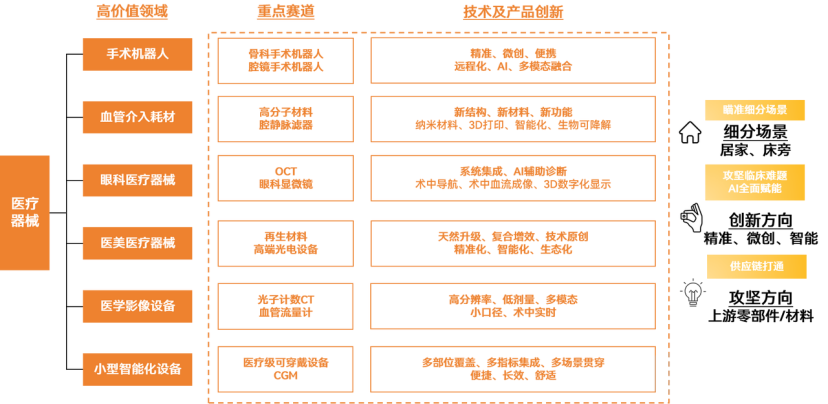

Overview of Key Product and Technological Innovations: Driven by Source Innovation

Overview of Key Product and Technological Innovations

Source: VBInsight

02-2025 Insights into the Most Valuable Fields and Product Competitiveness

Surgical Robot

Policy Acceleration and Demand Resonance Drive Industry Growth into an Accelerated Phase.As of 2025, surgical robots have become one of the fastest-growing segments in China’s high-end medical device industry, benefiting from some of the strongest policy support. According to public data from Mordor Intelligence, the global surgical robot market size is projected to exceed USD 13.6 billion in 2025, while the Chinese market surpassed RMB 10 billion in 2024 and continues to maintain a compound annual growth rate (CAGR) of over 14.8%. The industry widely recognizes that China is currently at a critical transition stage, shifting from “equipment importation” to “independent innovation and industrial commercialization.”

Orthopedic surgical robots represent a high-certainty growth sector driven by population aging.By the end of 2024, China’s population aged 60 and above reached 310 million (accounting for 22%), while those aged 65 and above numbered 220 million (accounting for 15.6%), marking the country’s formal entry into a moderately aging society. Meanwhile, there has been a rise in osteoarthritis cases among younger individuals due to improper exercise and trauma, leading to a trend toward younger patients undergoing joint replacement surgery. From a clinical perspective, surgical procedures covered by orthopedic surgical robots, such as joint replacements and spinal corrections, exhibit significant characteristics of rigid demand. Orthopedic surgical robots are gradually transitioning from “innovative equipment” to “standard configuration,” with their adoption expanding from top-tier Grade A tertiary hospitals to secondary and specialized medical institutions. As the health insurance payment system and volume-based procurement mechanisms continue to improve, the industry is entering a balanced phase characterized by “volume growth and price stability.”As of now, there are approximately 14 domestic manufacturers participating in market competition, among which about 12 have obtained NMPA marketing approval, while several other projects are in the R&D/clinical stages.Domestic manufacturers, represented by MicroPort MedBot, Tinavi, and Yuanhua Intelligence, have rapidly penetrated the secondary hospital and regional healthcare markets by leveraging more competitive pricing, localized services, and flexible market strategies. Although the installed base of domestic systems started later than that of imported brands, it is growing at a faster pace, with their market influence continuing to rise.

Orthopedic Surgeries Already Launched in ChinaRobotProduct Portfolio (as of November 2025)

Data source: VBInsight

A Wave of New Endoscopic Surgical Robots Hits the Market as Chinese Manufacturers Enter the Commercialization Harvest Period.Following the successive approvals of Weigao in 2021, and MicroPort Scientific Corporation and Suzhou Sizherui in 2022, multiple domestic companies obtained regulatory approval for their products in 2025, marking their formal entry into clinical use. Although current mainstream Chinese-made products predominantly feature integrated architectures, technological development is witnessing a breakthrough toward “modularization.” This approach involves introducing scalable robotic arm interfaces or replaceable end-effector modules within an integrated framework; notably, Ruilong Nuofu has already received approval for its modular surgical robot. Driven by policies such as the “Equipment Renewal” initiative, domestic sales of laparoscopic surgical robots exceeded 100 units by November 2025. The localization rate has increased significantly, with the market share of domestic brands nearing parity with that of imported brands.

Endoscopic Surgical Robots Approved in China

Data Source: Official Website of the National Medical Products Administration, VBInsight

Vascular Interventional Consumables

Driven by the dual forces of market demand and evolving concepts, domestically produced vascular interventional materials achieved key breakthroughs in 2025, making the leap from technological R&D to commercialization in multiple “chokepoint” areas.For instance, polyimide (PI) precision catheter materials, which had long been monopolized by foreign manufacturers, have made significant progress in processes such as thin-wall extrusion, wall thickness uniformity, and surface modification. These materials have successfully entered high-precision application fields including electrophysiology, coronary, and peripheral interventions, initially establishing the capacity for import substitution. In the field of drug-coated balloons (DCBs), domestically produced coating systems are upgrading from early simple physical adsorption to composite structures featuring an “adhesion layer–controlled release layer–surface functional layer.” By leveraging technologies such as micro/nanocarriers and wettability modulation, these systems significantly enhance drug transfer efficiency and local retention time, supporting the expansion of DCBs to more complex indications such as small vessels and bifurcation lesions. Meanwhile, in the area of biodegradable stents, which had previously cooled off, new-generation polylactic acid materials have achieved a better balance between degradation profiles and mechanical support through copolymerization modification, crystal structure regulation, and surface engineering. This has brought bioresorbable scaffolds (BRS) back into clinical and commercial focus, with products from multiple domestic companies entering critical stages of registration submission in 2025.

Evolution of Polymer Materials and Key Pathways to Localization in China

Data source: VBInsight

At the capital level,The Field of Polymer Materials for Vascular Intervention Continued to Attract Investment Attention in 2024–2025, financing has clearly concentrated on the “deep-water zone of domestic substitution” and “platform-type technologies.” Companies with independent R&D capabilities in high-end polyimide, PEEK modification, and coating technologies, such as Linsheng Polymers and Ruining Biology, have all completed hundred-million-yuan-level financing rounds in recent years.

2025 marks a pivotal turning point for the vena cava filter industry, as it transitions from a “niche high-end consumable” to a “large-scale routine consumable.”Driven by the combined effects of centralized procurement implementation, strengthened emphasis on retrievability, maturation of domestic supply chains, and improvement of supporting systems, the industry is forming a new landscape characterized by “domestic products as the mainstream, retrievable devices as the priority, and closed-loop services as the core.” According to the latest statistics on reported demand volumes from the 23-province alliance-led centralized procurement initiated by Heilongjiang Province in 2025 (by manufacturer), Bard Medical ranks first in the Chinese market with a 25.4% share, followed by Celsion in second place (17.8%), and LifeTech Scientific in third with a 17.3% share. The market share of overseas companies is gradually being eroded. Domestic brands are also transitioning from imitators to the main force of technological innovation.

Ophthalmic Medical Devices

In 2025, China's mid-to-high-end ophthalmic medical device market demonstrated robust growth momentum, driven by both policy support and technological innovation.On one hand, the policy environment, guided by the deepening of centralized procurement and a preference for domestic products, continues to improve, creating a more favorable competitive advantage for local enterprises. On the other hand, domestically produced medical devices have achieved a series of key breakthroughs, with multiple first-of-their-kind products receiving approval. Furthermore, domestic brands have made varying degrees of headway in market share across various product lines. Overall, the industry is moving towards technological upgrading, cost optimization, and self-reliance and controllability, while the market landscape is poised for profound transformation driven by the resonance between policy and market forces.

Hotspot Insights into Domestic Mid-to-High-End Ophthalmic Devices in 2025

Data Source: VBInsight

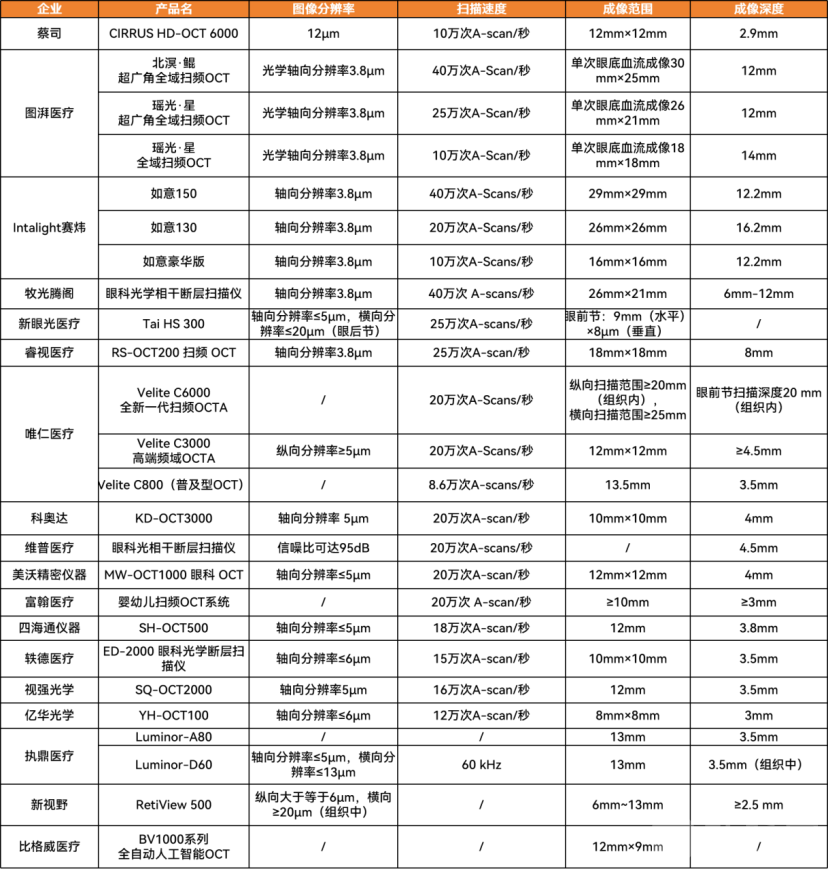

In 2025, China’s ophthalmic OCT market exhibited a multifaceted landscape characterized by certain demand, dominance by domestic manufacturers, technological advancement, and intensifying competition.The continuous release of clinical demand is the core driver propelling the development of the ophthalmic OCT market. Meanwhile, in surgical fields such as cataract and refractive surgery, OCT has become an indispensable tool for precise preoperative measurements and postoperative outcome assessment. Furthermore, driven by policies promoting the high-quality development of public hospitals, the renewal and upgrading of medical equipment, and the strengthening of primary healthcare service capabilities, medical institutions at all levels have significantly increased their willingness to equip themselves with ophthalmic OCT systems.

VigorousClinicalDemand has spurred the intensive launch of products.As of December 2025, a total of 34 ophthalmic OCT devices have received approval from the National Medical Products Administration (NMPA), with domestic brands dominating the market at 25 units. Notably, eight new domestic products were approved in 2025 alone, significantly surpassing previous years. An analysis of the technical specifications reveals that leading Chinese manufacturers have surpassed imported brands in core performance metrics such as scanning speed, imaging depth, and resolution, demonstrating robust product competitiveness.

Performance of Core Parameters of Ophthalmic OCT Devices

Source: VBInsight

Prior to 2025, the market share of domestically produced ophthalmic surgical microscopes in China was negligible, with the market firmly monopolized by international giants such as Zeiss.In 2025, the entrenched market landscape of ophthalmic surgical microscopes was disrupted for the first time.According to statistics from ZhaoCai Data Tong, imported brands accounted for over 89.68% of the total winning bid amount in the first three quarters of 2025. Tuopu Medical’s “Boyun” series of ophthalmic surgical microscopes ranked among the top ten in terms of winning bid amount, with a unit price of RMB 5.8 million, marking the first breakthrough for domestic brands in the high-end ophthalmic surgical microscope sector. This not only opens the door to the localization of ophthalmic surgical microscopes but also signifies that domestically produced equipment has entered the high-end price segment, with technical performance and brand value capable of meeting the stringent requirements of top-tier hospitals.

Inventory of Core Products in Ophthalmic Surgical Microscopes

Source: VBInsight

Medical Aesthetic Medical Devices

In 2025, the VBInsight team observed clear structural changes in the medical aesthetics device industry across three dimensions.:Domestic substitution has penetrated core sectors, innovative materials are emerging in volume, and high-end equipment has achieved key breakthroughs.These changes are underpinned by specific market dynamics and case studies, collectively outlining a new industry landscape characterized by greater standardization, innovation, and intensified core competition.

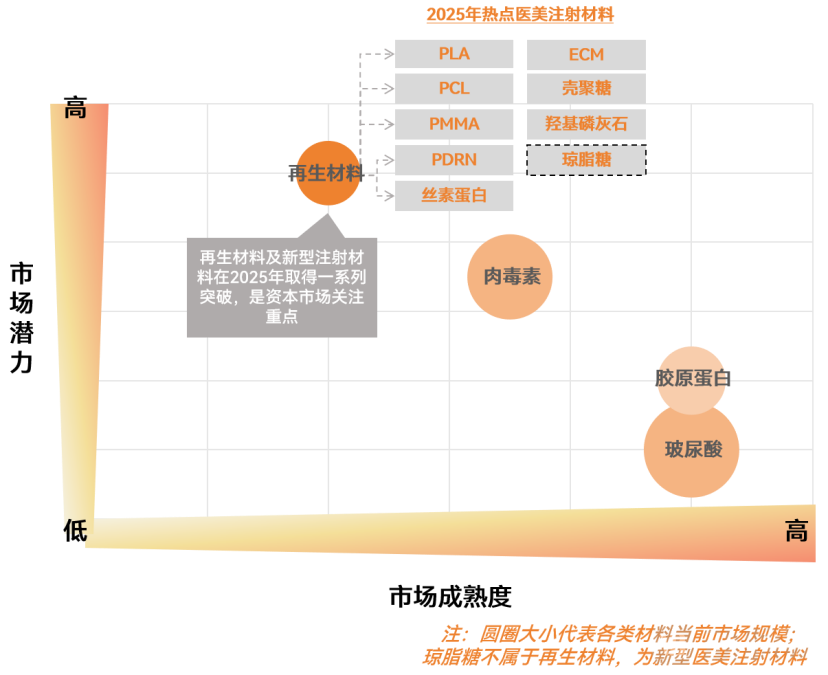

First, domestic substitution is evolving from “replacement” to “leadership,” with leading companies building significant advantages through their product portfolios and number of approvals.In the field of injectable fillers, the pathway for domestic substitution has been fully realized: from collagen products breaking the import monopoly to new materials represented by hydroxyapatite and agarose being the first to obtain Class III medical device certifications in 2025, Chinese brands have transitioned from followers to parallel competitors. Taking Bloomage Biotech as an example, as of May 2025, it held 13 Class III medical device approvals, 11 of which were for aesthetic injection products, a number that leads the industry. In the field of energy-based devices, domestic breakthroughs are even more landmark. For instance, the picosecond laser treatment system independently developed and manufactured by Keying Laser has successfully achieved localization and import substitution in this sector. Meanwhile, radiofrequency devices, hailed as the “gold standard for anti-aging,” and multiple models of domestic picosecond laser equipment have successively entered the market, indicating that the technological gap between Chinese-made devices and international brands in the mid-to-high-end market is rapidly narrowing.

Secondly, innovations in new materials, represented by recycled materials, are experiencing an “explosive” surge and have attracted significant attention from the capital markets.In 2025, industry hotspots moved beyond traditional hyaluronic acid and botulinum toxin, expanding into diverse biomaterials. Both hydroxyapatite and agarose received their first Class III medical device certifications this year, marking the transition from zero to one in compliant applications. Meanwhile, innovative ingredients such as ECM (extracellular matrix) and PDRN have attracted significant R&D resources from numerous companies. The capital market has also responded swiftly; for instance, Meibai Bio, a company specializing in ECM materials, completed an A++ round of financing amounting to tens of millions of yuan in April 2025, led by Cofoe Medical. These materials are not only used for injectable fillers but are also extending into adjacent fields such as functional skincare and wound repair, driving the industry trend of “integrating medical aesthetics with skincare.”

Classification and Selection of Injectable Materials in Medical Aesthetics in 2025Atlas

Data Source: Miot Data, VBInsight

Finally, driven by the triple forces of policy, capital, and technology, the optoelectronic equipment sector has achieved a critical leap, with its market potential continuing to be unleashed.In 2025, radiofrequency (RF) aesthetic devices were formally included under Class III medical device regulation. This move not only raised market entry barriers but also created opportunities for compliant leading domestic enterprises. At the technical level, Chinese-made equipment has achieved breakthroughs—either “from zero to one” or “from existing to excellent”—in the three mainstream energy-based modalities: ultrasound, radiofrequency, and laser. The capital market has responded positively to these developments. For instance, Nuoding Xianchi Medical, a startup focused on AI-driven ultrasound aesthetics and repair, announced in early October 2025 that it had completed a seed financing round of nearly RMB 10 million to support core product development and advance clinical trials. These advancements align with substantial market demand. Data shows that the market size of “light medical aesthetics,” characterized by non-invasive and minimally invasive procedures, grew from RMB 50.2 billion in 2018 to RMB 146 billion in 2023. This rapid growth has provided a solid foundation for innovation in upstream medical devices.

Hot Topics and Representative Companies in the Non-Surgical Medical Aesthetics Device Industry in 2025

Source: VBInsight

Medical Imaging Equipment

In 2025, driven by the national strategy of expanding and upgrading medical resources and advancing precision medicine, China’s high-end medical imaging equipment market exhibited a robust recovery and structural upgrading, characterized by the “dual-wheel drive” of demand escalation and technological innovation. The market demonstrated“Accelerated Localization,” “Release of High-End Demand,” and “Scenario-Based Product Innovation”Three Core Characteristics.

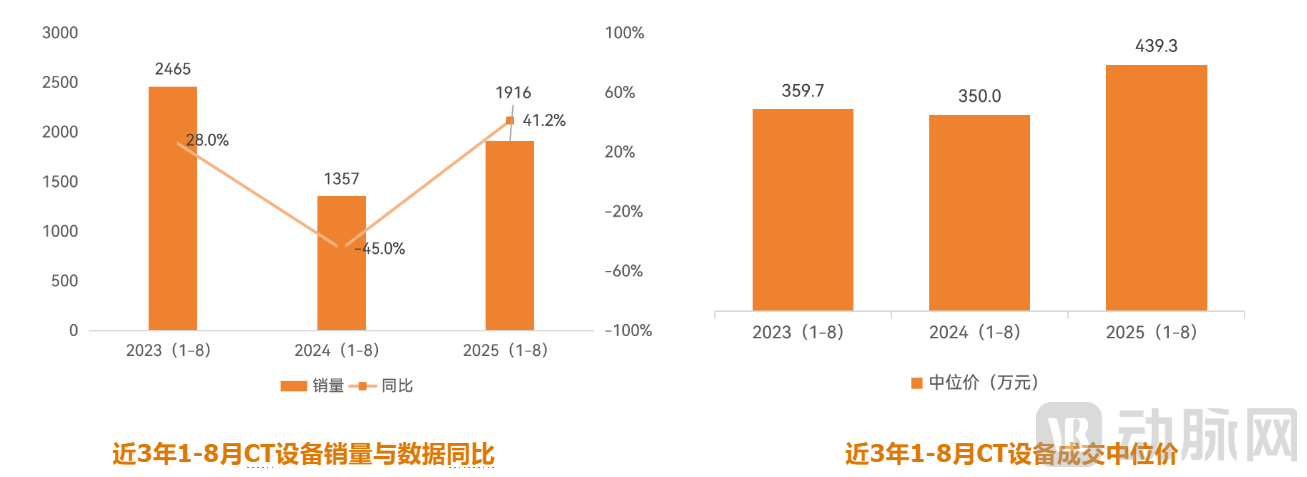

According to industry data,From January to August 2025, medical imaging became one of the fastest-growing segments in the medical device industry.Among them, the CT market led with a scale of approximately RMB 14.453 billion, accounting for nearly 30% of the overall medical imaging market, and its sales volume increased significantly by 41.19% year-on-year, demonstratingRising Volume and Pricea high-end dominated landscape with high brand concentration, where Siemens, United Imaging, and GE collectively monopolize over 70% of sales. Meanwhile, the localization process for ultrasound equipment has advanced significantly, with the domestic production rate rising to 46.40%, and year-on-year growth in sales revenue and volume reaching 24.71% and 42.30%, respectively. On the demand side, driven by the increasing need for early disease diagnosis and precise assessment, there is strong demand for high-end equipment such as high-field MRI, multi-slice CT, and PET-CT in tertiary hospitals, with technological development focusing onAI Empowerment andMultimodalFusion Imaging。

Data Sources: High-End Medical Device Institute Data Center, VBInsight

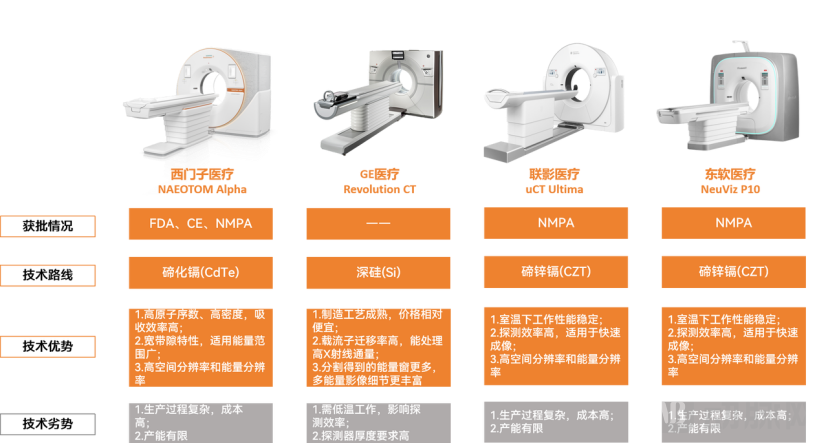

2025, hailed as the third revolution in CT technologyPhoton-Counting CT, is transitioning from concept to clinical commercialization, ushering in a new era of high-end medical imaging. Unlike conventional CT, it employs novel semiconductor detectors capable of individually counting and analyzing the energy of each X-ray photon, thereby achieving qualitative leaps in ultra-high spatial resolution, direct multi-energy spectral imaging, and lower radiation doses. This provides unprecedentedly precise information for early disease diagnosis. Industry forecasts predict that its domestic market will reach RMB 15.8 billion by 2030, accounting for 80% of the total CT market, indicating broad prospects.

Current Photon CountingCTRepresentative Product Technical Roadmap

Source: VBInsight

AI technologies, remote systems, and big data analytics are further expanding the application boundaries of ultrasound medicine.Among the many innovations, ultrasonic vascular flow meters based on transit-time blood flow measurement technology are becoming key tools for achieving real-time intraoperative quality assessment in precision surgeries such as cardiac surgery.This technology directly and objectively measures blood flow volume within 7–10 seconds by calculating the minute time difference between ultrasound propagation in the direction of and against the blood flow. Compared with traditional Doppler techniques, it offers significant advantages, including strong real-time performance, high measurement accuracy, and the ability to simultaneously assess vascular resistance.Its coreClinicalIts value lies in providing surgeons with immediate, quantitative decision-making support, significantly improving outcomes of coronary artery bypass grafting (CABG).Currently, this niche market is dominated by international manufacturers such as MediStim. Its VeriQ ultrasonic transit-time flowmeter holds the highest global market share, while the MiraQ™ system combines transit-time blood flow measurement technology with high-frequency ultrasound imaging technology to better assess anastomotic quality.。Domestic innovators are also emerging. Yuewei Medical’s transit-time flowmetry-based vascular flowmeter is currently undergoing registration, offering accuracy comparable to imported products at a lower cost. Furthermore, the company has achieved breakthroughs in the fabrication and signal processing technologies for small-diameter (<1 cm) vascular flow sensors based on transit-time flowmetry—a field that has been largely unexplored in China. This technology can be applied to microsurgical procedures such as coronary artery bypass grafting, organ transplantation, and intracranial bypass surgery.

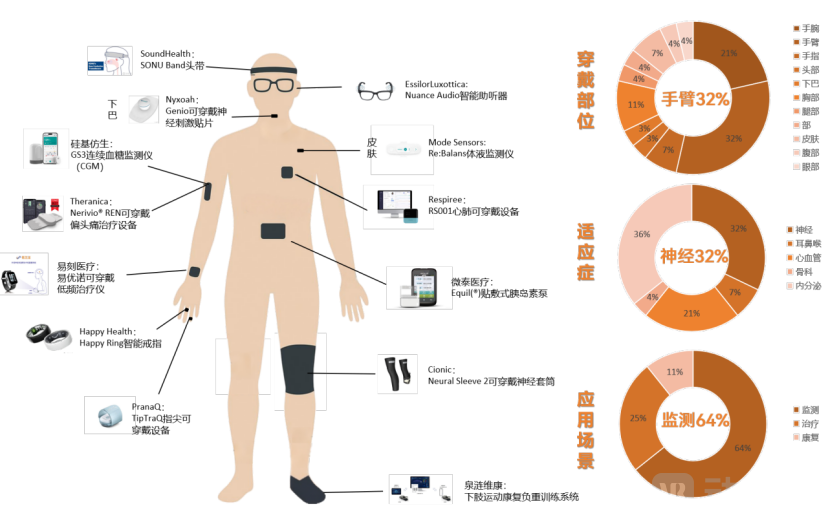

Small Intelligent Devices

Wearable Medical Devices:Monitoring data from VBInsight shows that in 2025 (as of November),A total of 28 models worldwideMedical GradeWearable medical devices (including CGMs) obtain regulatory approval or FDA Breakthrough Device designation. From the perspective of approved product developments and technological advancements, the deep integration of artificial intelligence (AI) and wearable devices has transitioned from a trend to industrialized practice, driving the evolution of medical health management from “passive monitoring” toward “proactive intervention” and “personalized management.”

From a statistical perspective, wearable medical devices have already shownMulti-site coverage, multi-indicator integration, and multi-scenario applicationsignificant features. Its application has expanded from daily monitoring of vital signs such as step count and sleep to comprehensive management of chronic diseases like diabetes and cardiovascular disease, achieving full-cycle health coverage from “health prevention” to “disease intervention.”

Cluster Analysis of Representative Wearable Products Approved in 2025

Data source: Public information, VBInsight

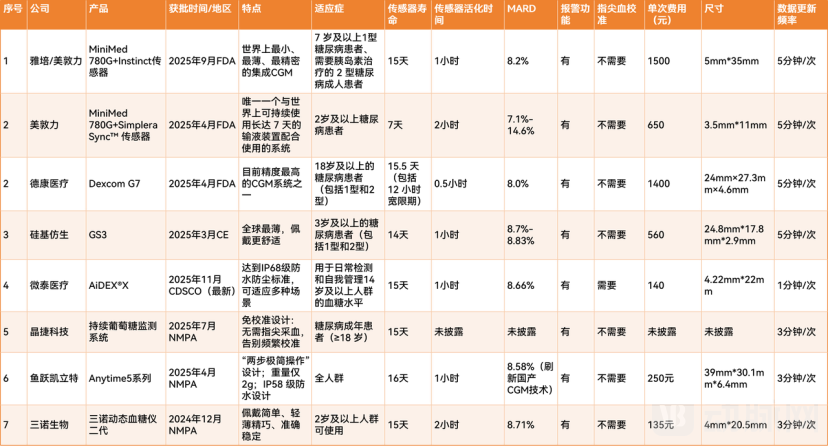

CGM:In 2025, global CGM giants continue to optimize their technologies, increase R&D investment, and launch new products.Chinese Enterprises’ Innovation Pace Significantly Accelerates, Shifting from “Following” to “Running Side by Side”. Leading domestic companies such as Sinocare, Yuwell Kailite, and Jingjie Technology have successively obtained NMPA registration certificates for their new products from late 2024 to early 2025. These new products have reached international standards in key performance indicators, including sensor lifespan (generally achieving 14–15 days) and MARD value (Mean Absolute Relative Difference, mostly optimized to below 9%).

Latest CGM Product Specifications from Leading Manufacturers in 2025

Note: MARD refers to the Mean Absolute Relative Difference. All product features listed are claims made by the manufacturers at the time.

Data Source: Public Information, VBInsight

03 Top 10 Predictions for the Medical Device and Supply Chain Industry in 2026

3.1 Demand Side

Trend 1: The importance of medical devices continues to strengthen, with the market size experiencing steady growth

The Medical Device Market Sees Steady Growth

Data Source: Public Information, VBInsight

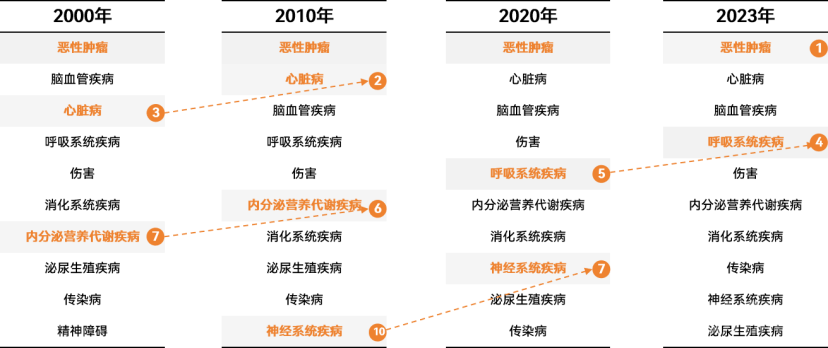

Trend 2: Deepening Population Aging Drives Structural High Growth Through Demand Shifts

Changes in the Ranking of the Top Ten Causes of Death in China, 2000–2023

Data source: National Health Commission

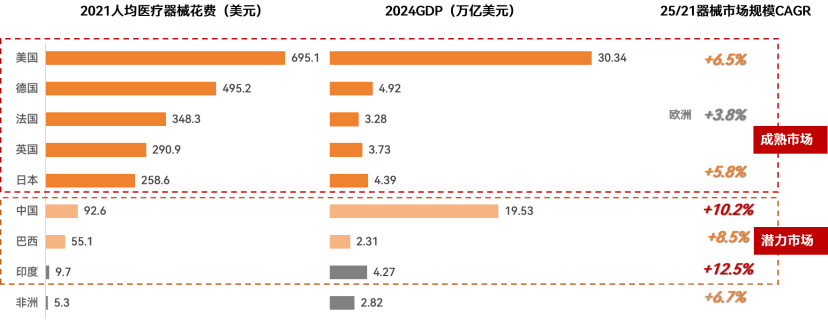

Trend 3: Continue to Deepen Overseas Engagement, Break Through Overseas Markets with Original Innovation

Global Distribution of the Medical Device Market

Data Sources: Public Information, IQVIA, VBInsight

3.2 Supply Side

Trend 4: Accelerated Industry Consolidation, with Platform-Oriented Leaders and the Emergence of Medical Device MNCs

Mergers and acquisitions integration has become a key pathway for platform-based strategic layout.Following Mindray Medical’s acquisition of a controlling stake in Huitai Medical and Sino Biopharmaceutical’s takeover of Haobo in 2024, the industry witnessed four more major M&A deals in 2025, indicating that leading enterprises are actively building diversified product portfolios through external expansion.Mergers and acquisitions have always been the core logic behind the growth of global medical device giants.Looking ahead to 2026, we anticipate that mergers and acquisitions in China’s medical device sector will continue to deepen, further strengthening the competitiveness of platform-based companies. In the near future, China is poised to produce multinational corporations (MNCs) in the medical device industry with global influence, potentially breaking into the top 50 ranks of global healthcare enterprises.

Trend 5: Accelerated Innovation—China’s Medical Device Industry Enters a Period of Mass Emergence of Original Achievements

Classification of Innovative Medical Devices Entering the Approval Process by the End of November, 2023–2025

Data Source: NMPA, VBInsight

Trend 6: AI Further Penetrates Diagnostic and Treatment Equipment, Becoming the Largest Structural Change on the Supply Side

AI Fully Penetrates Diagnostic and Treatment Equipment

Data Source: Public Information, VBInsight

Trend 7: Advancements in Foundational Technologies Drive a “Bottom-Up” Comprehensive Upgrade of the Medical Device Industry

Currently, China’s medical device industry is undergoing a profound paradigm shift in innovation. The focus of competition is rapidly shifting from whole-device integration and channel marketing to the core components that determine the upper limit of product performance, as well as advanced biomaterials that confer product differentiation and clinical value.In 2026, enterprises and investors who focus on companies possessing proprietary technologies in specific core components, or those with deep strategic layouts in particular material platforms coupled with a thorough understanding of clinical language, will be better positioned to capture the long-term dividends generated by the upward shift in the industrial value chain.

Trend 8: Upgrading the Global Expansion Model: From “Product Export” to “Ecosystem Export”

The overseas expansion strategies of Chinese medical device companies are undergoing a profound evolution, with the core shift moving from simple trade transactions to building an overseas ecosystem that encompasses localized operations and resilient supply chains.In 2026, global competition will enter a new phase, as companies transition from being “product providers” to “builders of localized ecosystems,” propelling the internationalization of China’s medical device industry toward greater maturity and sustainable growth.

3.3 Payment Side

Trend 9:Centralized ProcurementCoverage is expanding at an accelerating pace, albeit with moderated intensity, while pricing is becoming more rational.

In 2026, we anticipate that medical devicesCentralized Procurement"Full-domain" coverage will be further achieved, with the overall centralized procurement coverage rate for medical devices exceeding 50%, while price reductions will fully take into account corporate profitability levels.On the other hand, medical insurance reimbursement for innovative products (including AI) will be significantly higher than current levels. For enterprises, it is essential to actively explore incremental markets both domestically and internationally to offset the impact of declining prices in China; meanwhile, they should further increase R&D investment and focus on next-generation technologies.

Trend 10: Sustained Growth in Commercial Health Insurance, Structural Transformation of Payment Systems for Innovative Medical Devices

In the short term, with the first edition of the commercial health insurance catalog officially taking effect on January 1, 2026, the payment pathway for innovative medical devices will become as clear as that for innovative drugs.In the long term, the expansion of commercial health insurance will directly feed back into the R&D sector, creating a flywheel effect of “payment assurance – market returns – R&D investment.” For medical device companies, this means that the clinical value and innovative attributes of their products will not only be reflected through centralized procurement pricing but will also achieve more reasonable and sustainable value returns via diversified payment markets, ultimately driving the entire industry to climb up the higher end of the value chain.

Based on the white paper’s analysis of innovation logic across major high-value sectors and corporate implementation practices, this year’s edition highlights fifteen outstanding innovation case studies.

(The above is an excerpt from the key contents of the white paper. Scan the QR code below to access the full report.)

Table of Contents

Preface

Key Views and Conclusions

Chapter 1 Overview of Hot Topics in the Medical Device and Supply Chain Industry in 2025

1.1 Industry Panorama: Sector Stabilizes, Advancing with Resilience

1.2 Policy Changes: The Main Tone Continues to Promote Innovation, Stabilize Supply, Improve Quality, and Reduce Ineffective Cutthroat Competition

1.3 Industry and Capital Markets: Reshaping and Recovery, High-Tech Leading a New Cycle of Investment in Medical Devices

1.4 Overview of Key Product and Technological Innovations

Chapter 2: Insights into the Most Valuable Fields and Product Competitiveness in 2025

2.1 Surgical Robots

2.2 Vascular Interventional Consumables

2.3 Ophthalmic Medical Devices

2.4 Medical Aesthetic Devices

2.5 Medical Imaging Equipment

2.6 Small Intelligent Devices

Chapter 3: Top 10 Predictions for the Medical Device and Supply Chain Industry in 2026

3.1 Demand Side

3.2 Supply Side

3.3 Payment Side