AI Adoption Takes Center Stage as Brain-Computer Interfaces Enter Clinical Trial Boom

In 2025, the digital health industry exhibited robust growth, driven by technological innovation and capital investment. Breakthroughs in two core areas—artificial intelligence and brain-computer interfaces—were particularly significant, injecting strong momentum into the sector’s development.

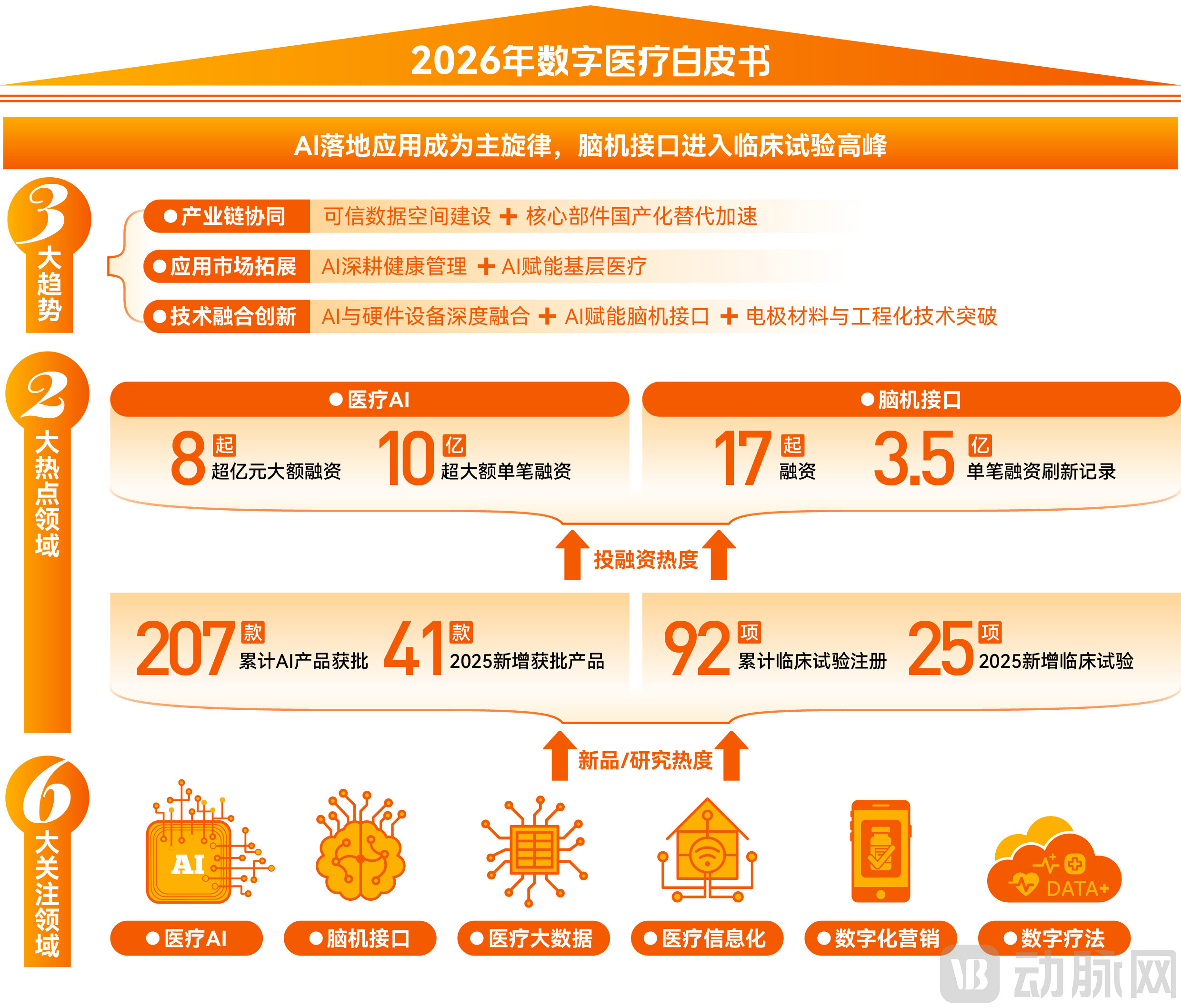

The integration of artificial intelligence and healthcare continues to deepen, becoming the core engine driving industry development.. As of 2025, a cumulative total of 207 AI-powered medical devices have received regulatory approval, accelerating the pace of technological implementation; capital market enthusiasm remains undiminished, with single financing rounds reaching the billion-yuan level, underscoring the industry’s development potential. At the application scenario level, artificial intelligence has successfully empowered key areas such as clinical trial optimization, personalized health management, insurance service innovation, and regional medical collaboration, achieving a leap from technological R&D to practical value.

The Brain-Computer Interface Field Simultaneously Enters a Period of Explosive Growth, with the Accelerated Advancement of Clinical Trials Becoming the Most Distinctive Industry Characteristic.In 2025, multiple clinical trial achievements secured international firsts and achieved global breakthroughs, continuously enhancing China’s international influence in this field. The capital sector also performed remarkably, with a single financing round of RMB 350 million setting a new industry record and providing solid support for technology translation. Notably, the deep integration of artificial intelligence and brain-computer interfaces has emerged as a new industry trend, opening up new possibilities for cross-sector convergence in digital healthcare.

This white paper, based on in-depth research and interviews with more than ten digital health innovators, leading investment firms, and seasoned industry experts, examines the current state of development across various segments of China’s digital health sector—including medical artificial intelligence and brain-computer interfaces—from the dual perspectives of industry dynamics and corporate practices. It provides a comprehensive analysis of the core characteristics and key breakthroughs that defined the industry in 2025, offers a forward-looking outlook on development trends for 2026, and aims to deliver valuable insights and guidance for industry stakeholders.

Key Views and Conclusions:

I. A Three-Dimensional Review of 2025’s Hotspots in the Digital Health Industry: Policy, Products, and Capital

1Policy Intensification: Emphasizing Practical Implementation, with Breakthroughs Achieved in Payment Mechanisms Across Multiple Sectors

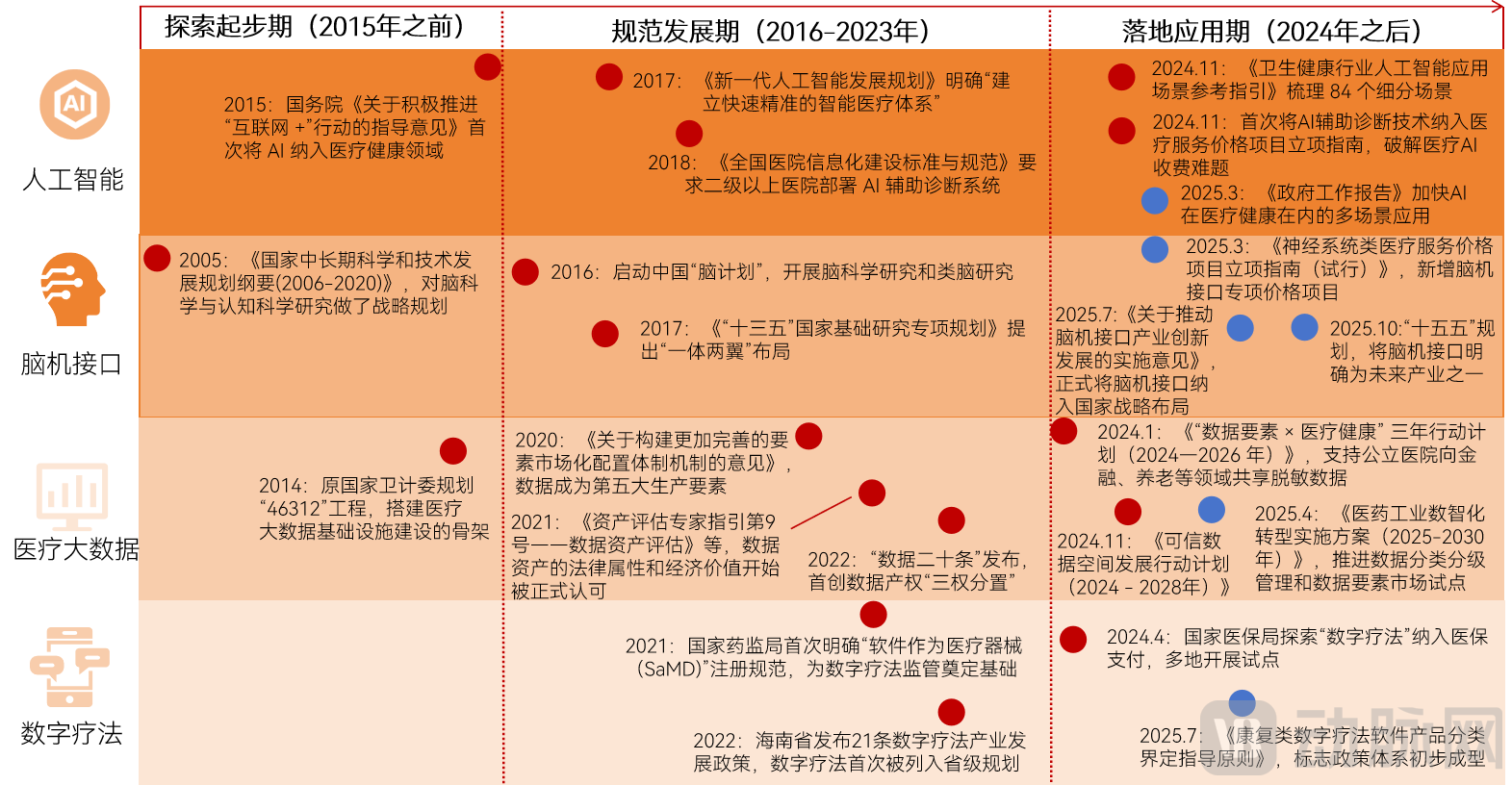

As a typical policy-driven industry, the development trajectory of digital healthcare is deeply coupled with national strategic planning. From the foundational construction of medical informatization to innovative internet-based healthcare models, and further to leapfrog advancements in the integration of digital healthcare technologies, China has consistently promoted iterative upgrades within the industry through systematic policy provision. Since 2025, government departments have successively introduced several landmark policies to actively foster the application and development of emerging technologies such as artificial intelligence and brain-computer interfaces in the medical field. By implementing multifaceted measures—including standard setting, industrial support, price management, and strengthened regulation—a comprehensive policy ecosystem has been established to facilitate the digital transformation and innovative development of the healthcare sector.

Key Policies in Various Subsectors of Digital Healthcare Over the Years (Blue Dots Indicate 2025 Policies)

Artificial Intelligence: Focusing on Application Scenarios with the Core Objective of Driving Practical Adoption.In August 2025, the State Council officially released the “Opinions on Deepening the Implementation of the ‘AI+’ Initiative,” marking China’s first special action program in the field of artificial intelligence. This milestone signifies a comprehensive shift in China’s AI development from the “technological breakthrough” phase to a new stage characterized by “scenario-based implementation, industrial empowerment, and universal benefit.” Notably, healthcare has been explicitly identified as one of the six key sectors for integrated AI application, with policy incentives becoming more targeted and actionable. A review of policies at both national and regional levels in 2025 reveals four distinct trends in China’s AI policy landscape: “application-driven, scenario-centric,” “regulatory innovation with encouragement for pioneering efforts,” “focus on primary healthcare and decentralization of AI capabilities,” and “whole-industry-chain collaboration for systematic implementation.”

Brain-Computer Interfaces: Listed as One of the “Six Major Future Industries,” with Independent Pricing Items Established for the First Time.A series of landmark “firsts” in national-level policies have been successively introduced, including the “first industry standard for brain-computer interface (BCI) medical devices” and the “first establishment of independent pricing items for BCI technology,” injecting strong momentum into the development of the BCI industry. The “Implementation Opinions on Promoting Innovative Development of the Brain-Computer Interface Industry” and the “Proposal of the Central Committee of the Communist Party of China on Formulating the 15th Five-Year Plan for National Economic and Social Development” have been released one after another, with brain-computer interfaces listed as one of the “six major future industries” prioritized for strategic layout. This marks a formal elevation of brain-computer interfaces from a frontier research field to the level of national industrial strategy, representing a significant leap forward in its industrial development positioning.

Medical Big Data: Interdepartmental Collaboration and Data Integration to Accelerate the Assetization of Healthcare Data.China’s data landscape has undergone a leapfrog evolution from being regarded merely as a “factor of production” to becoming recognized as an “asset.” The term “data assetization” has also become a high-frequency keyword in policy documents in recent years. In 2025, multiple policies in the field of medical big data were officially implemented, characterized by distinct features of “cross-departmental collaboration and data linkage,” directly addressing key pain points in the process of medical data assetization—from rights confirmation to valuation and circulation. From national top-level design to regional implementation practices, China’s policy framework for medical big data now covers the entire process of “compliant rights confirmation – value assessment – circulation and trading,” laying a solid institutional foundation for compliant data flow and value realization.

Healthcare Informatics: A Mature Policy Framework, with a Focus on Implementation and Detailed Refinement.After more than three decades of development, the healthcare informatization industry has achieved large-scale construction driven by policy tailwinds such as “Smart Healthcare” and “Internet + Healthcare.” It has now entered a plateau phase characterized by well-established infrastructure and a mature standards system. In 2025, no fundamental policy changes emerged; instead, the focus shifted toward cross-sector collaboration and the deepening of details within the existing policy framework.

Digital Marketing: Core constraints are concentrated in the two dimensions of compliance and data security.From a policy perspective, anti-corruption campaigns in the healthcare sector have promoted standardized pharmaceutical sales; professional guidelines for medical representatives have encouraged a return to the essence of academic promotion; and policies such as centralized volume-based procurement (VBP) and national reimbursement drug list (NRDL) negotiations have driven companies to reduce costs, improve efficiency, and optimize sales expenditure. These factors have all enhanced the importance of digital marketing to varying degrees. Furthermore, with the expansion of healthcare service pathways and the advancement of digital technologies, the necessity of digital marketing will continue to escalate. Currently, there are no specialized policy documents specifically addressing digital marketing in the healthcare sector. Industry development remains indirectly guided by cross-sectoral regulations and technical policies, with core constraints concentrated in the two dimensions of compliance and data security.

Digital Therapeutics: Clarifying Pricing Principles and Pathways to Address the Biggest Pain Point.In 2025, China’s first reimbursement policy for digital therapeutics and the first specialized regulatory policy targeting digital therapeutics were successively released, marking the industry’s transition from a chaotic phase of “unbridled growth” to a virtuous path of “standardized development.”

2Product Upgrades: Surge in AI Large Model Products, Brain-Computer Interface Technology on Par with International Standards

In 2025, various sub-sectors of digital healthcare achieved upgrades and iterations in product technology. It is worth noting that products/solutions in the field of digital therapeutics have matured, with no major iterative products or solutions emerging in 2025. Meanwhile, the medical informatics sector has seen an accelerated integration of AI into its products/solutions, resulting in significant overlap with the medical artificial intelligence sector. In light of these two factors, this report will not provide an in-depth analysis of these two fields.

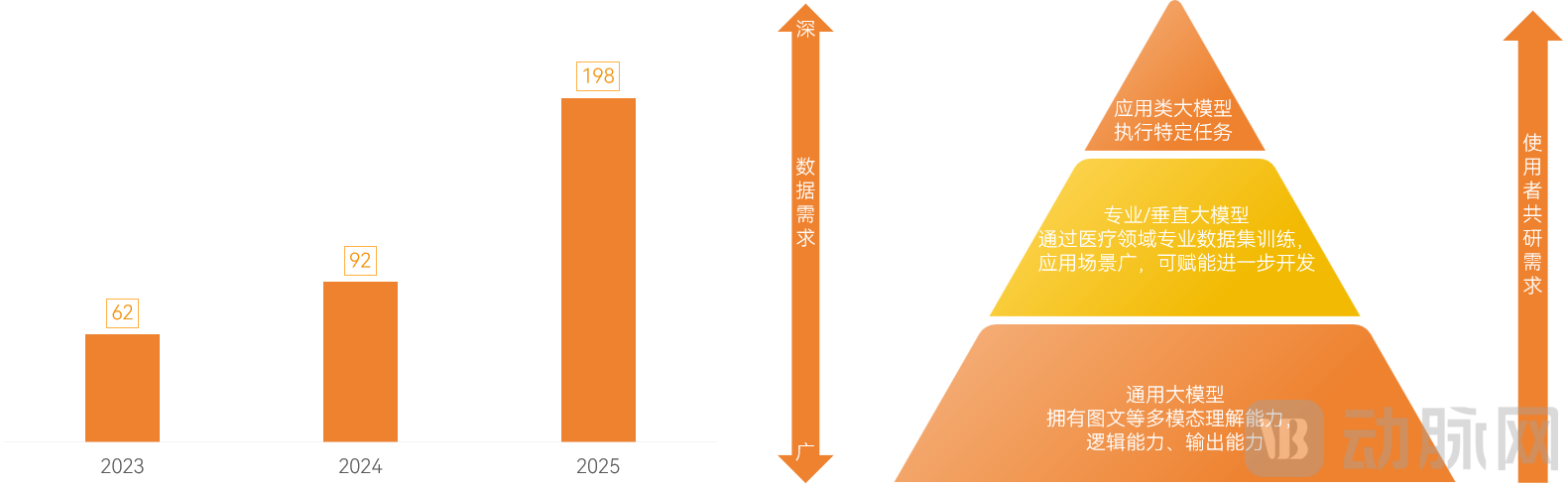

In 2025, large medical models experienced explosive growth, driving the development and deployment of AI applications across multiple dimensions, including performance, cost, and market adoption.In terms of performance, the two mainstream models are leveraging AI to enhance application performance and treating the model itself as a product. Next is pricing: reduced R&D costs, driven by DeepSeek and advancements in domestically produced chips, have granted AI applications more flexible and attractive pricing strategies. Finally, regarding the market, DeepSeek’s role in promoting market education should not be underestimated, beyond its improvements in performance and cost reduction. The entire society, including the medical community, has directly perceived the allure of large language models and their imaginative potential.

Number of Major Medical Large Language Models Released from 2023 to 2025 / Classification and Characteristics of Medical Large Language Models

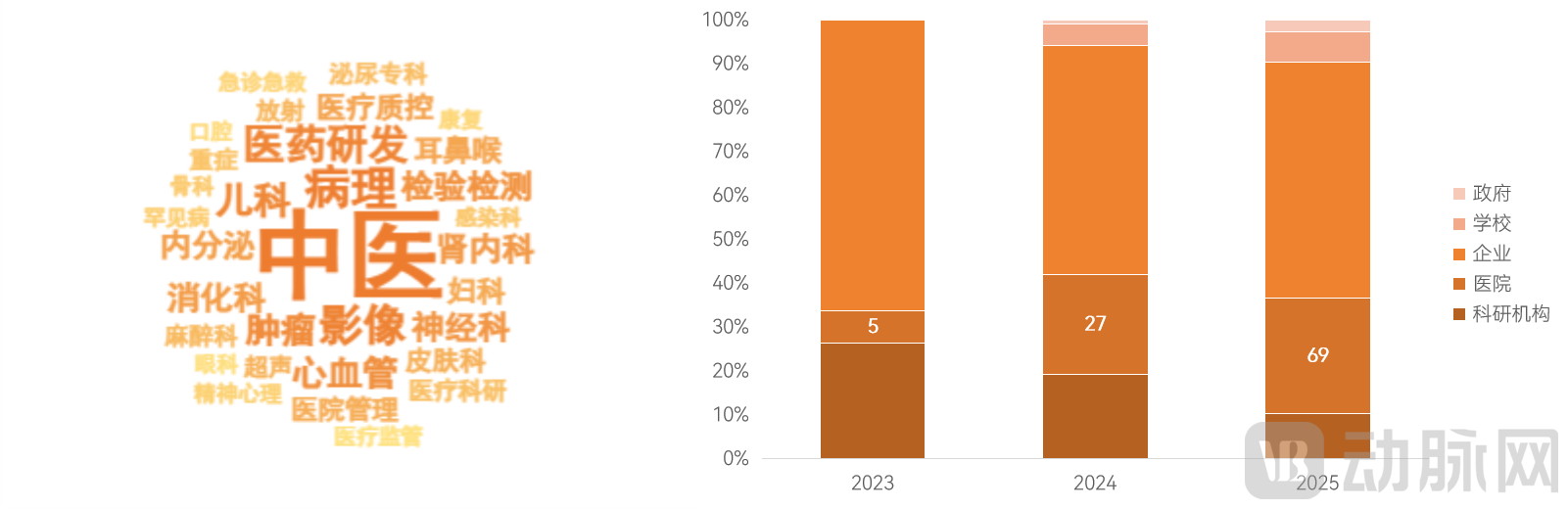

Medical agents derived from large language models are also showing a trend toward specialization in specific medical disciplines and diseases.VBInsight has identified nearly 160 vertical large language models (LLMs) and AI agents specialized in specific diseases and medical specialties through an analysis of publicly available data, revealing a trend of multidimensional expansion in application scenarios. Radiology is one of the most frequently applied areas. Shukun Technology’s “Shukun Multimodal Medical Health Large Model 3.0” deeply integrates multimodal data to provide physicians with an all-knowing, all-capable “digital doctor” assistant. In oncology applications, JD Health is actively exploring the development of LLMs tailored to multiple specialties and specific diseases. For instance, it has partnered with Peking University Cancer Hospital to create a specialized LLM for gastrointestinal diseases, covering esophageal cancer, gastric cancer, colorectal cancer, and other related conditions. Additionally, in collaboration with the First Affiliated Hospital of Guangzhou Medical University, JD Health has built a specialized LLM for respiratory diseases, supporting the diagnosis and treatment of lung cancer, chronic obstructive pulmonary disease (COPD), pneumonia, and other conditions.In the clinical laboratory, Roche Diagnostics’ AI large model-based handheld digital service solution, “Luo e Fu,” focuses on three areas—smart operations, project planning, and clinical empowerment—to achieve intelligent and lean management of the laboratory.These specialty-specific large language models not only achieve deep reasoning across all diseases, entire clinical workflows, and comprehensive factors within their respective specialties, but also integrate the full-service chain spanning “diagnosis–image interpretation–treatment,” thereby embedding AI empowerment into every critical link of disease prevention and control.

Healthcare institutions have become a crucial part of “AI manufacturing.”The breakthrough of large models has also attracted more hospital experts to participate in their joint research and development. According to incomplete statistics, the number and proportion of large models developed with hospital participation (including those independently developed by hospitals) have increased year by year, rising from 7% in 2023 to 26% in 2025. For exampleShenzhou Medical andThe First Affiliated Hospital of Sun Yat-sen University, Fujian Children's Hospital, Nanfang Hospital of Southern Medical University, and other leading medical institutionsThrough collaborative partnerships, joint research and development of specialized large language models (LLMs) and AI agents for specific diseases were conducted. In 2025, a total of 20 disease-specific LLMs were intensively launched, including the Peritoneal Dialysis LLM, the “Fuxing” AI LLM for Childhood and Adolescent Obesity, and the “Zhishen” LLM for Comprehensive Management of Chronic Kidney Disease. Additionally, Yidu Tech, in collaboration with Academician Teng Gaojun’s team, developed “Xiao Gan Ren,” an AI agent for the diagnosis and treatment of liver cancer. This agent deeply integrates evidence-based medicine systems and comprehensively consolidates guidelines from the National Health Commission, the China Anti-Cancer Association (CACA), as well as multi-sectoral standards and consensus on liver diseases, aiming to create an “AI Doctor” with expert-level diagnostic and therapeutic logic for hepatology. This collaborative co-development model has undoubtedly facilitated the deep integration of high-quality medical data, professional know-how, and technology, thereby creating higher-performance products that feed back into clinical practice and establish a virtuous cycle.

Word Cloud of Specialized Disease-Specific AI Agents / Proportion of Large Model R&D Participants, 2023–2025

As the review and approval system matures, industry registration and market access efficiency continue to improve, driving sustained high growth in the AI medical device sector.As of December 5, 2025, a total of 207 AI-based medical devices have obtained Class III medical device registration certificates; since the beginning of 2025, 41 new approvals have been granted, consistent with recent trends, marking the third consecutive year that annual approvals have exceeded 40.

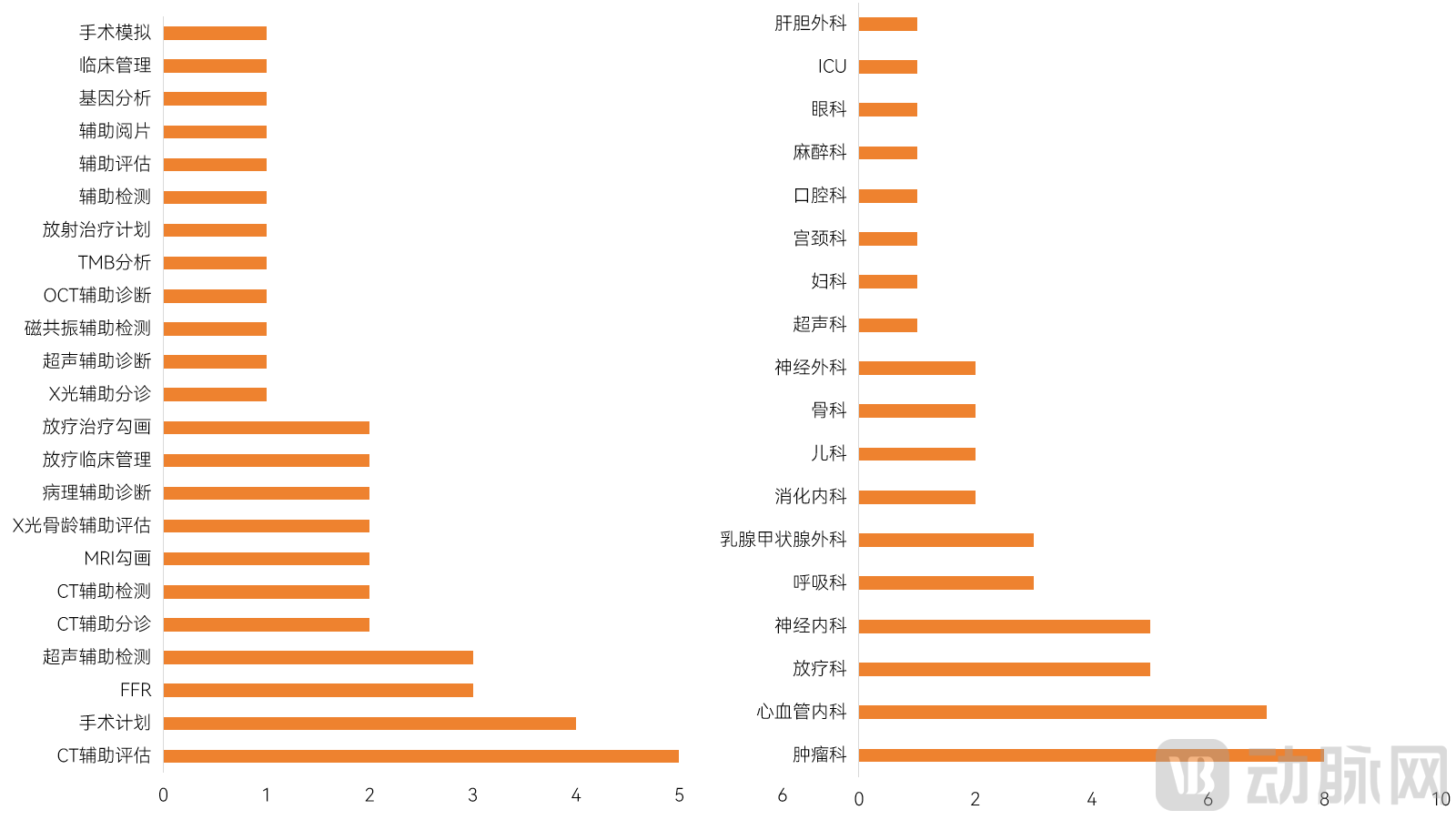

Product capabilities are progressively breaking through the constraints of single-link operations and expanding into diverse scenarios.Although AI for assisted diagnosis remains mainstream, diverse new scenarios such as radiotherapy planning, clinical management, and surgical planning/simulation, along with clinical management functionalities, are being rapidly implemented. The field is evolving from a sole focus on diagnosis to a dual emphasis on “diagnosis and treatment.” In terms of departmental distribution, AI-based medical devices are widely applied in oncology, cardiology, radiation oncology, and neurology. Taking oncology, the most concentrated area of application, as an example, indications mainly focus on prostate cancer and lung cancer, with core functionalities centered on assisted diagnosis and radiotherapy. For instance, Siemens Healthineers received approval in October for its AI-based software for assisted detection of prostate cancer in MRI images. This device, which employs deep learning technology, is used for the display, processing, measurement, and analysis of prostate MRI scans. It provides assisted detection of suspected prostatic adenocarcinoma lesions in untreated adult patients aged 40 years and older, thereby improving physicians’ image interpretation quality and reducing unnecessary biopsies in clinical practice.

Approval Status of Class III Medical Device Certificates for AI Products by Function and Department

As AI product performance improves, market acceptance and trust grow, and the commercialization environment becomes increasingly mature, AI is rapidly penetrating every aspect of the healthcare sector. We categorize these applications into five segments: drug R&D and manufacturing, in-hospital scenarios (including clinical and hospital-side operations), out-of-hospital health services, payment and distribution, and regional regulation. The “2025 Healthcare Artificial Intelligence Industry Research Report,” released by VBInsight at the end of 2025, provides an in-depth analysis of AI application and commercialization progress specifically within in-hospital scenarios. Therefore, this report focuses on the remaining AI application segments, analyzing the outstanding achievements and advancements in each subsector in 2025.

A Panoramic View of Artificial Intelligence Applications Across Healthcare Subsectors

AI Across the Entire Clinical Trial Process: The Leap from “Efficiency Tool” to “Value-Driven Tool”In 2025, companies are differentiating their services by expanding overseas and building international clinical trial capabilities, while gradually leveraging AI to differentiate their products. AI not only serves as an efficiency tool to shorten clinical trial timelines by enabling real-time risk assessment, but also helps improve success rates. For example, Yilin Cloud has integrated AI into its full product suite to create a digital management platform covering the entire clinical trial lifecycle. This platform facilitates a leap in efficiency and cost reduction, provides endpoint assessment solutions, monitors data quality and trial risks in real time, and supports key decision-making to dynamically enhance success rates and compliance.

AI organically integrates the entire ecosystem of out-of-hospital health services, with comprehensive health management as the core focus.In the realm of out-of-hospital health services, large-scale health management application scenarios have emerged as the absolute hotspot for AI implementation in 2025, a trend driven by the convergence of policy, technology, market dynamics, and demand. We are witnessing an increasing number of mature digital-intelligent health management solutions across the industry. Companies are actively developing their own large language models (LLMs) to create unique, personalized health management solutions, thereby strengthening their product moats and enhancing corporate competitiveness. For instance, CyberPilot has developed its proprietary medical LLM for disease risk assessment, building a full-cycle digital-intelligent health management platform that drives the industry’s transformation from “single-service” models to “ecosystem collaboration.” Ping An Good Doctor, leveraging its self-developed LLM “Ping An Yi Bo Tong,” has established a “7+N+1” medical AI product system, helping to improve access to high-quality medical resources. Yuanxin Technology has created the “Yuanquan Partner Agent Cluster,” which empowers pharmacies to significantly improve health management adherence, assists hospitals in enhancing quality and efficiency, and enables insurers to provide faster and more convenient insurance enrollment and claims services. Lejian Health, relying on the “Tianrui Qiyuan Medical LLM,” uses its platform as a carrier and AI as the core to coordinate high-quality medical and nursing resources nationwide, offering comprehensive digital-intelligent health service solutions that cover health check-ups, chronic disease management, and home care.

AI Empowers the Entire Insurance Service Process, Facilitating the Development of Diverse Insurance Products.Numerous processes in insurance, including sales, underwriting, and claims settlement, involve extensive data collection and analysis. However, this series of tasks—though tedious and labor-intensive—is characterized by clear standards and procedures, making it highly compatible with AI empowerment. Moreover, AI implementation in this field has already reached a high level of maturity. For instance, Qingsong Health, as part of its service ecosystem, has developed the AIcare large language model to empower the entire workflow of digital integrated insurance services, linking 58 insurance companies and offering a total of 294 insurance products. This approach not only applies AI across the full spectrum of digital integrated insurance services but also provides technological solutions to insurance partners to help improve quality and efficiency.

AI Facilitates the “Flow” of Medical Data, Promoting the Sustainable Development of Healthcare Artificial Intelligence.Current medical data faces the pain points of “siloed, low-quality, and heterogeneous” information. Among these issues, the cross-institutional data access rate is less than 15%, unstructured data accounts for more than 70%, and the data missing rate and error coding rate exceed 30%. Governing such data requires substantial repetitive workloads. Theoretically, specialized artificial intelligence can be constructed to address these challenges, and relevant applications have already been implemented in the industry. For instance, Neusoft Medical partnered with the Shenzhen Health Development Research and Data Management Center to build China’s first local government-led multimodal general data model for clinical diagnosis and treatment (SZ-CDM). This model achieved standardized integration of 34 business tables and 1,042 data fields, overcoming the challenge of cross-system data mapping.

Technological development has accelerated significantly, with breakthrough achievements made across all sub-sectors, propelling the overall standing to the forefront globally.In the invasive domain, Tii Medical has completed the world’s second prospective clinical trial of an invasive brain-computer interface (BCI), while NeuroXess has become the only invasive BCI company globally to master both real-time motor decoding and real-time Mandarin Chinese decoding technologies. In the semi-invasive domain, “Beinao No. 1” has achieved multiple human implants, setting a global benchmark in dimensions such as signal acquisition and core technologies; the launch of its Good Clinical Practice (GCP) multi-center clinical trial marks a step toward standardized validation. In the endovascular domain, the team from Nankai University has completed the world’s first trial assisting in the restoration of motor function in affected limbs. In the non-invasive domain, BCI companies represented by BrainCo are continuously expanding their product portfolios.

The industry is accelerating from the “technical validation” phase to the “clinical application” stage.The number of registered clinical trials for brain-computer interfaces (BCIs) has shown a significant upward trend in recent years. From January to October 2025, the registration volume already matched that of the entire year of 2024, with full-year figures poised to break records. This growth is reflected not only in quantity but also in the quality of translational outcomes: although 48% of the trials remain in early exploratory stages, the number of trials involving novel therapeutic technologies (including Phase I, II, and III) has increased from 14 (with only one reaching Phase III) before February 2024 to 20, indicating that the technology is progressively advancing toward clinical validation.

The industrial chain is accelerating the establishment of vehicles for the clinical translation of technologies.Driven by the dual forces of favorable policies and technological breakthroughs, China’s supporting industrial chain for brain-computer interfaces (BCIs) is rapidly taking shape. Milestones include the first clinical application of domestically produced BCI chips, the establishment of China’s first BCI medical insurance data research center, and the launch of the world’s first customized magnetic resonance imaging (MRI) platform for BCI interaction. Furthermore, in 2025, many regions proactively established specialized BCI research wards, providing a solid foundation for the clinical translation of these technologies. According to incomplete statistics, as of October, 41 BCI clinical research wards and centers had been established nationwide. The primary indications under investigation include motor impairments (such as limb disabilities, post-stroke motor deficits from cerebral hemorrhage, amyotrophic lateral sclerosis, and spinal cord injury), consciousness and cognitive disorders (including vegetative state and Alzheimer’s disease), and epilepsy and neurodevelopmental disorders (such as epilepsy, attention-deficit/hyperactivity disorder, autism spectrum disorder, language disorders, and sleep disorders).

Number of Brain-Computer Interface Research Wards Across China and Their Focus on Indications

Trusted Data Space Construction Is in Full Swing, with Cases Already Implemented in the Healthcare Sector.According to the VCBeat database, as of October 2025, there were 40 health data trading listings on online data exchanges in 2025, significantly surpassing the 24 recorded in 2024. Driven by the "Action Plan for the Development of Trusted Data Spaces (2024–2028)," data resources have achieved efficient and secure sharing and joint utilization. On July 16, 2025, the National Data Administration announced the first batch of pilot projects for the innovative development of trusted data spaces, with seven pilots from the healthcare industry making the list. Furthermore, companies such as Beijing Electronics Digital Intelligence, Digital China, and Neusoft Group officially launched healthcare trusted data space solutions in 2025, with implementation cases already in place. Neusoft Group’s "Medical Insurance Trusted Data Space" focuses on the coordinated development of medical insurance, pharmaceuticals, and healthcare services. It has been implemented in three typical scenarios: AI-based intelligent supervision of medical insurance funds, pharmaceutical retail and smart healthcare, and personal health intelligent management services, providing data-driven solutions for medical insurance payment reform and pharmaceutical industry innovation.

Accelerated Secondary Use of Medical Data Drives Deeper Value ExtractionIn China, the secondary use of hospital data has entered a phase of large-scale practice, presenting a differentiated development pattern dominated by basic applications and supplemented by research support.From a technical perspective, AI is no longer merely an auxiliary element. Vendors are actively adopting AI technologies, including large language models (LLMs), and deeply integrating them into the entire value chain, encompassing data governance, diagnostic and therapeutic services, and operational management. In terms of application scenarios, the depth of value extraction from medical big data continues to increase. Applications have expanded from single-module use within hospitals to a full-scenario closed loop covering operational optimization, precision clinical diagnosis and treatment, and out-of-hospital chronic disease management. Furthermore, this expansion extends into cross-industry domains such as pharmaceutical and medical device R&D and commercial insurance innovation. In August 2025, Deepwise Medical released the Deepwise TrioData X Multimodal Medical Data Large Model Capability Platform. Centered on the core mission of “reconstructing the value of medical data,” it creatively establishes a full-stack closed loop of “data governance – capability innovation – scenario implementation.” This platform transforms massive multi-source data into a high-quality, trustworthy data asset hub, empowering healthcare institutions at all levels across clinical care, scientific research, management, and AI innovation capabilities.

The Focus of Digital Marketing Shifts Toward “Patient Services.”Driven by developments in policy, patient awareness, and the market, digital marketing is shifting from a physician-centric model to a diversified “dual-centered” (physician and patient) or patient-centric model, with the overall marketing focus transitioning toward “patient services.”

Effective marketing content and health management services are scarce.In recent years, significant progress has been made with the support of artificial intelligence. Digital doctors and AI health managers, for example, have provided substantial assistance. Beyond directly reducing labor costs, these technologies have enhanced the standardization of health management services and established a stronger foundation for data collection and analysis.

3Capital Market Performance: AI-Plus-Healthcare Companies Queue for IPOs, Brain-Computer Interfaces See Surge in Popularity

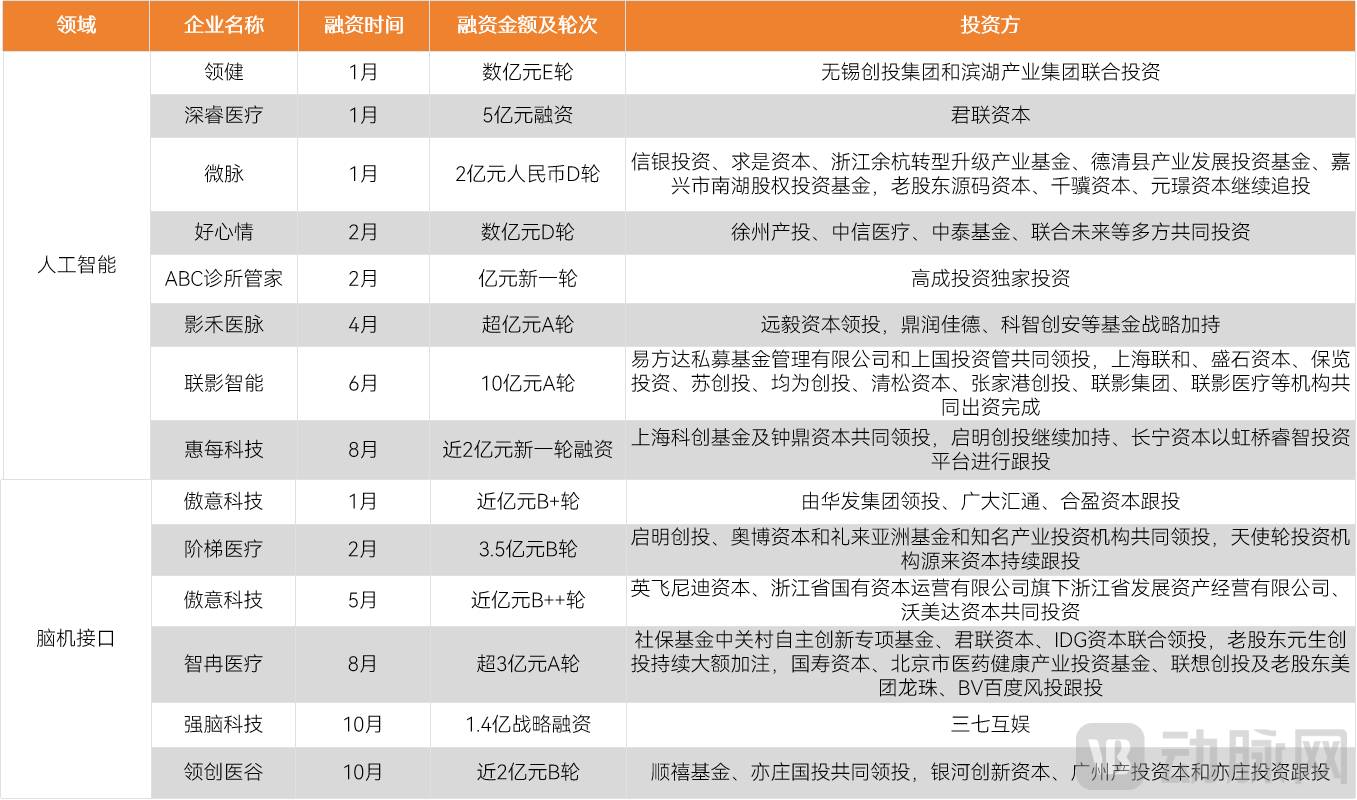

AI Healthcare Breaks Through Against the Trend, Continuously Shattering Financing Records and Becoming a Core Highlight in the Big Health Sector.Whether empowering health management, assisting in diagnosis and treatment/imaging analysis, or enhancing hospital administration, AI is demonstrating its value in driving technology-led innovation to address industry pain points.UIH AI completed a RMB 1 billion Series A financing round in June, marking not only a key breakthrough in its own development but also the largest single financing deal in the digital health sector within the research period.In 2025, the surge in financing activities within the brain-computer interface (BCI) sector underscored its heightened market momentum.Invasive and Non-Invasive Tracks Exhibit Divergent Development Trends. The invasive sector saw eight financing events, including three major deals worth hundreds of millions of yuan, with leading companies demonstrating significant fundraising scale and industry influence; the non-invasive sector recorded eleven financing events, predominantly at early stages, indicating that the industry remains in a phase of rapid growth.

Capital Events with Financing Amounts Exceeding 100 Million Yuan in 2025 (as of October 2025)

The Hong Kong Stock Exchange IPO Market Rebounds in 2025.From June to October, seven companies in the medical AI sector progressed from filing and updating their prospectuses to obtaining listing registrations, covering niche segments of the AI healthcare industry chain. This trend highlights the capital appeal of the AI healthcare track in the Hong Kong stock market and the surge in IPOs among healthcare enterprises driven by policy support.

The niche segment of medical insurance informatization achieved slight growth, driven by policy support.The policy mandate to achieve nationwide coverage of DRG/DIP payment methods by the end of 2025, coupled with the explosive growth phase of market-oriented healthcare insurance data elements, will directly drive the demand for upgrading hospital-side medical insurance settlement systems. A cohort of enterprises specializing in healthcare insurance informatization is poised to benefit from these developments.

Favorable Policies Drive Brain-Computer Interface Concept Stocks HigherSeveral listed companies have entered the brain-computer interface (BCI) sector through diverse pathways, including “independent R&D, provision of supporting equipment, equity investments, and strategic partnerships.” Among them, Chengyitong, Chuangxin Medical, and Xinwei Medical have emerged as the top performers in the sector, driven by clear progress in technology commercialization, with share price increases of 280%, 180%, and 172%, respectively.

Yice Medical Management and YiHui Technology Were Acquired in Succession, Indicating Reduced Demand for IT Systems at the Hospital EndThere are two primary reasons for this. First, there are no new mandatory policy requirements for smart hospital accreditation. Most hospitals that have already met the policy-mandated accreditation levels are shifting their focus from striving for higher-tier ratings to consolidating the gains achieved through existing accreditation. Specifically, they are further translating the enhancements in diagnostic and treatment capabilities and the optimization of patient services brought about by accreditation into tangible operational value for the hospital. Second, the comprehensive and deepened implementation of DRG/DIP payment reforms is driving a strategic shift in hospital operations from past “scale expansion” to “lean management,” resulting in a significant reduction in demand for non-core and non-essential informatization projects.

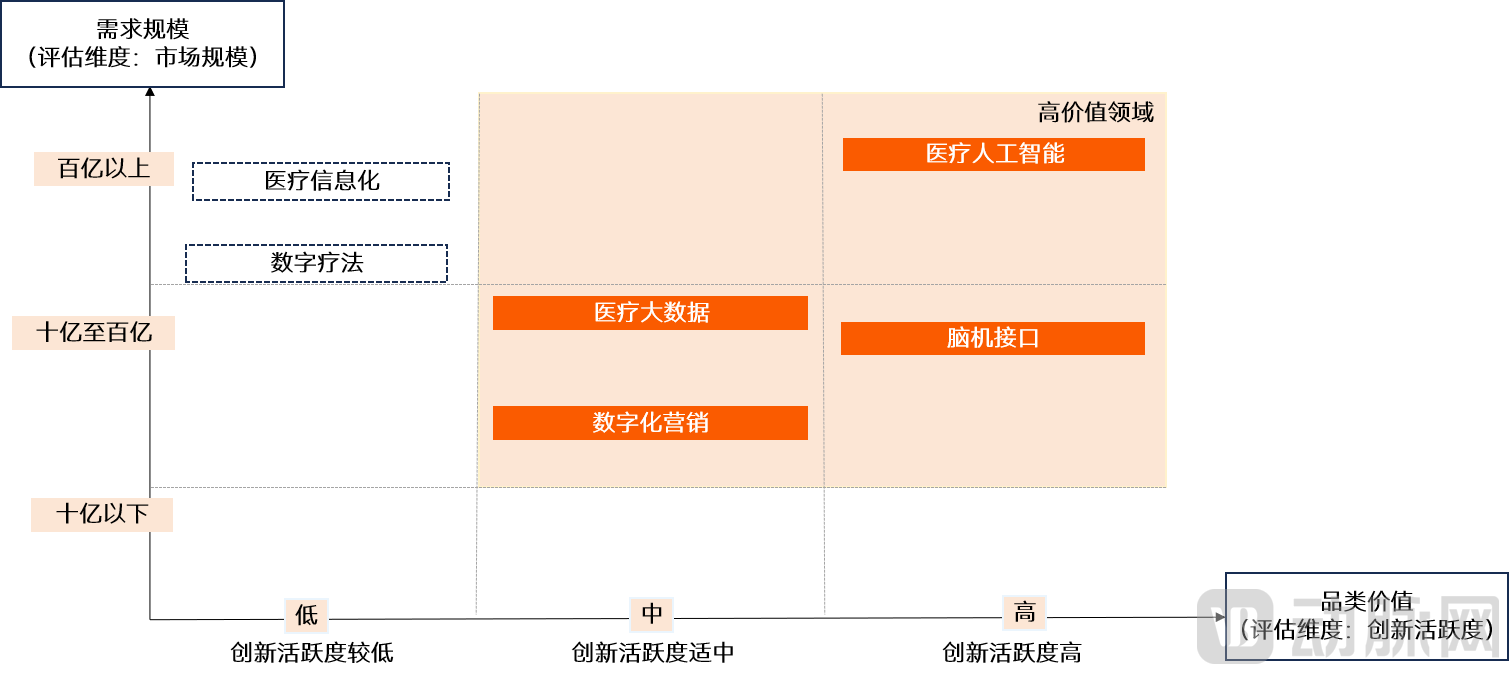

II. Insights into the Most Valuable Fields and Product Competitiveness in 2025

A surge of innovative products and solutions has emerged across all subsectors of the digital health industry. VBInsight, leveraging a dual-dimensional assessment based on demand scale and the innovation activity of products/solutions, has identifiedMedical AI, Brain-Computer Interfacestwo high-value sectors, and will conduct an in-depth analysis of the core competitiveness of innovative achievements in these fields.

2025 High-Value Areas in Digital Health

Based on the innovation logic analysis of high-value sectors and corporate practical initiatives outlined in the white paper, ten outstanding innovation case studies of the year have been selected. (The above is an excerpt from the main content of the white paper; to obtain the full report, please scan the QR code below.)

The following is the table of contents for this white paper:

Chapter 1: Overview of Hot Topics in the 2025 Digital Healthcare Industry

1.1 Policy Intensification: Emphasis on Practical Implementation, with Breakthroughs in Payment Mechanisms Across Multiple Sectors

1.2 Product Upgrades: Surge in AI Large Model Products, Brain-Computer Interface Technology on Par with International Standards

1.3 Capital Performance: AI+Healthcare Companies Queue for IPOs, Brain-Computer Interface Sector Sees Surge in Popularity

Chapter 2: Insights into the Most Valuable Fields and Product Competitiveness in 2025

2.1 Medical Artificial Intelligence

2.1.1 Overall Market Changes in 2025: AI Deeply Empowers Healthcare, Unlocking More High-Value Scenarios

2.1.2 Interpretation of AI-Driven Innovative Products: Accelerated Scenario Implementation and the Reconfiguration of Medical AI Application Value

2.2 Brain-Computer Interface

2.2.1 Overall Market Changes in 2025: China Achieves Consecutive Milestone Breakthroughs as US-China Competition Intensifies

2.2.2 Insights into the Competitiveness of Innovative Products: Chinese-Made Products Break Multiple International Records, with Promising Clinical Trial Trends

Chapter 3: Seven Predictions for the Digital Healthcare Industry in 2026

3.1 Technological Integration and Innovation: Breaking Through Core Bottlenecks to Build a New Paradigm for Intelligent Healthcare

3.2 Expansion of Application Markets: Deepening Penetration into Grassroots Scenarios to Unlock New Value in the Health Industry

3.3 Supply Chain Collaboration: Refining the Ecosystem Layout and Strengthening New Domestic Forces