2025 Annual Innovation White Paper on Innovative Drugs and Supply Chain: Accelerated Polarization and Industry Return to Platform and Product Value

If one word were to summarize China’s innovative drugs in 2025, it would be “divergence.”This divergence is reflected in capital allocation: investors are no longer paying for “stories,” but are instead flocking to companies with core technology platforms, clear clinical value, and global potential. In terms of policy orientation, regulators are no longer solely pursuing speed, but are building a comprehensive, precision support system spanning the entire lifecycle from early-stage R&D to downstream payment mechanisms. The divergence is also evident in corporate fortunes: a cohort of companies with substantial hard-core capabilities is emerging, with their innovative achievements gaining recognition and collaboration from multinational pharmaceutical firms, while players lacking differentiated competitiveness face market exit.

As a frontier observer and deep participant in China’s healthcare ecosystem, VCBeat has perceived that the core logic of China’s innovative drug industry has fundamentally shifted amid the interplay of divergence and regression.A new era defined by product strength, platform capabilities, and global operational excellence is rapidly approaching.Amidst transformation, identifying true value and determining future directions have become shared challenges across the industry. To address this, VCBeat, leveraging its years of in-depth tracking and insights into the sector, is committed to releasing the “2025 Annual Innovation White Paper on Innovative Drugs and Supply Chains,” which is grounded in the present and oriented toward the future.

The core purpose of this white paper extends beyond mere documentation and description. We aspire to assume the roles of “value discoverer” and “ecosystem connector,” aiming to systematically identify, curate, and recommend to the global market those Chinese innovative products, technology platforms, and solutions that have demonstrated genuine competitiveness amidst the tide of market differentiation.

Key Viewpoints:

In terms of policy guidance, we systematically reviewed over 300 national and local policies issued from January to October 2025, with a particular focus on the nearly 100 technical guidelines released by the National Medical Products Administration (NMPA). We found that the policy environment hasFrom the early principled advocacy of “encouraging innovation” to a new stage of systematic and precise guidance on “how to innovate.”This provides a fertile institutional ground for projects with original innovation capabilities.

Regarding capital centrality, we conducted an in-depth analysis of nearly 300 financing rounds and over 200 business development (BD) transactions. The data clearly reveals that the narrative logic of capital has fundamentally shifted.Although total financing in the primary market has become more cautious, capital is highly concentrated on mid-to-late stage projects from Series B onwards.as well as frontier technological fields such as antibody-drug conjugates (ADCs), bispecific antibodies, cell and gene therapy (CGT), and AI-driven drug discovery. Meanwhile, companies going public in the secondary market must demonstrate solid clinical progress and commercialization prospects to gain recognition.The value of overseas licensing-out deals for China’s innovative drugs hit a record high in 2025, with transaction models expanding from single-product licensing to deeper collaborations such as platform technology licensing and the establishment of joint ventures (NewCos).

In terms of pipeline competitiveness, we conducted an in-depth analysis of the clinical pipeline progress of over one hundred companies. 2025 marks a pivotal year for the concentrated realization of both clinical and commercial value of innovative drugs in China. Domestically developed ADCs and bispecific antibodies have successively received marketing approval and showcased globally leading clinical data at top-tier international academic conferences such as ASCO. Small-molecule drugs have achieved breakthroughs against “undruggable” targets like KRAS G12C, while significant advances have also been made in cell therapies (CAR-T, TIL) and nucleic acid therapeutics. Underpinning these breakthroughs is the capability leap of Chinese enterprises from follower innovation to source innovation, and from technology importation to systematic exportation.

Chapter 1: Overview of Hot Topics in the Innovative Drug and Supply Chain Industries in 2025

1China’s Innovative Drug Policy System Enters a New Phase of Systematic Guidance, Achieving Full-Cycle Integration and Precision Support

Currently, China’s innovative drug industry has entered a critical phase of transition from “follow-on innovation” to “source innovation.” As the industry gradually matures, policy orientation has shifted from early efforts to accelerate review and approval processes and encourage imports toward systematically building a full-lifecycle support framework. This aims to foster an industrial ecosystem characterized by high quality, genuine innovation, and rapid accessibility. Since 2025, relevant policies have further demonstrated systematic, precise, and forward-looking features, covering key stages such as R&D, clinical trials, review and approval, market access, and reimbursement, thereby forming a synergistic policy force to drive industrial upgrading.

Trends in China’s Innovative Drug Policies (2015–2025)

Trends in China’s Innovative Drug Policies (2015–2025)

Data sources: public information, VBInsight

From January to October 2025, the National Medical Products Administration (NMPA) and its Center for Drug Evaluation (CDE) served as the core forces in policy formulation. Working in coordination with multi-sectoral agencies such as the National Healthcare Security Administration and the National Health Commission, they jointly guided the industry to focus on clinical value and high-quality development. During this period, more than 300 policies related to innovative drugs and supply chains were issued at both national and local levels. The pace of policy releases exhibited a pattern of “building momentum mid-year and surging in autumn,” with 13 important documents issued in October alone, marking the highest policy density in recent years.

Key Policy Terms for Innovative Drugs and Supply Chains in China in 2025

Key Policy Terms for Innovative Drugs and Supply Chains in China in 2025

Source: VBInsight

Policies now cover the entire lifecycle of pharmaceuticals.The Center for Drug Evaluation (CDE) alone has issued more than 80 technical guidelines, providing clear guidance across all stages from early-stage research and development and clinical trial design to post-marketing surveillance. Policy priorities are clearly directed toward patient-centricity, addressing unmet clinical needs, and enhancing the efficiency and quality of drug development, thereby systematically building a healthy ecosystem that encourages genuine innovation, accelerates the market entry of high-quality medicines, and ensures patient access.

2The Return to Value in Industry and Capital Markets: Capital Concentrates on “Certainty” and “Globalization”

In 2025, primary market investment and financing in the innovative drug and supply chain sectors showed a recovery compared to 2024. This financing trend further indicates that industry competition has entered a more intense phase, with capital rationally concentrating on leading enterprises that possess core technologies, clear clinical value, and well-defined commercialization pathways, thereby accelerating their journey toward IPOs and commercial launch.

BD deals for innovative drugs in China remain robust, with both the number of transactions and the value per deal on the rise; in particular, early-stage clinical assets have become hot commodities for global expansion. On one hand, Chinese biotech companies seek to maximize market capitalization management through BD activities; on the other, multinational corporations (MNCs) are increasingly recognizing the value of Chinese assets and pursuing mega-deals to bolster their R&D pipelines. Meanwhile, BD transaction models are becoming increasingly diversified. In addition to license-in/out agreements and the highly watched NewCo model, they now also include equity transactions and deeper strategic collaborations.

Investment and Financing: Overall Slowdown, with Capital Concentrating in Late-Stage Projects and Frontier Technologies

The cooling trend in primary market investment and financing has slowed, with the average funding amount rebounding against the tide to 2022 levels. According to incomplete statistics from VBInsight, the total financing amount in China’s innovative drug and supply chain sectors from January to October 2025 reached USD 3.914 billion, representing a slight decrease compared to the same period in 2024, and accounting for over 60% of the full-year 2023 total (USD 6.159 billion). As more financing deals are disclosed in November and December, this gap is expected to narrow further.

Total Financing Amount and Number of Financing Events in China’s Innovative Drug and Supply Chain Sectors, 2015–2025

Total Financing Amount and Number of Financing Events in China’s Innovative Drug and Supply Chain Sectors, 2015–2025

Source: VBInsight

IPO: Hong Kong-listed innovative drugs lead the recovery, with technology platform companies emerging as new forces in listings

The number of IPOs in the innovative drug and supply chain sectors from January to October 2025 saw a significant increase compared to the same period in 2024, which was relatively sluggish. According to incomplete statistics from VBInsight, there were 19 IPOs in the innovative drug and supply chain fields from January to October 2025. With more companies in these sectors going public in November and December, the cumulative number of IPOs is expected to match the level of 2023.

Number of IPOs for Innovative Drugs and Supply Chains in China from January to October 2025

Number of IPOs for Innovative Drugs and Supply Chains in China from January to October 2025

Source: VBInsight

Notably, 25 years after its listing on the A-share market, Hengrui Medicine, the “elder statesman” of China’s pharmaceutical industry, successfully listed on the Hong Kong Stock Exchange. It became the largest IPO in the Hong Kong healthcare sector over the past five years, raising more than HK$9.7 billion, with its shares closing 25% higher on the first day of trading. In addition to Hengrui Medicine, HybriBio, GenFleet Therapeutics, and Beite Pharmaceuticals each raised over US$200 million (i.e., more than RMB 1 billion) in their public offerings.

From the perspective of sector composition, the Hong Kong-listed innovative drug sector is forming a complete industrial ecosystem. It includes industry leaders such as Hengrui Medicine, platform-based companies focusing on cutting-edge technologies like Duality Biologics, and supply chain service providers such as Tide Pharmaceutical. This diversified landscape signifies that China’s pharmaceutical innovation system is maturing, expanding from standalone drug R&D to coordinated development across the entire industry chain.

M&A: MNCs Snap Up Cutting-Edge Technologies, While Domestic Leaders Focus on Supply Chain Completion and Efficiency Enhancement

From January to October 2025, there were over 87 mergers and acquisitions (M&A) transactions globally in the innovative drug and supply chain sectors. In China, the domestic pharmaceutical M&A market was less active compared to 2024. While the number of deals and transaction volumes lagged behind those involving global giants, the market exhibited distinct characteristics of internal consolidation and strategic strengthening. The primary participants were listed companies (such as Jiuzhitang, Qianjin Pharmaceutical, Shanghai RAAS, and Sansure Biotech) and large pharmaceutical enterprises, aiming to optimize their product pipelines, expand production capacity, or enter new therapeutic areas.

Overview of M&A Activities in China’s Pharmaceutical Sector from January to October 2025

Source: VBInsight

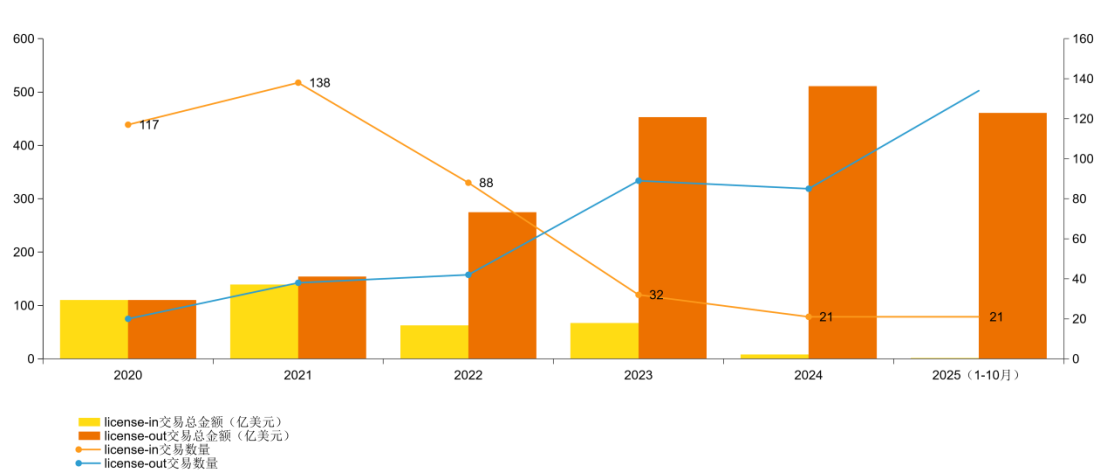

BD: Sustained Momentum as Innovative Drug Globalization Advances from “Single-Point Breakthroughs” to a New Phase of “Systematic Output”

Chinese companies are beginning to sell their R&D capabilities, rather than just R&D outcomes.While 2024 saw a substantial number of deals, most were limited to single-product licenses. In 2025, however, buyers demonstrated a greater willingness to pay a premium for platforms with sustained output capabilities. This shift reflects multinational pharmaceutical companies’ recognition of the systematic innovation capabilities in China; they are acquiring not only current pipelines but also future options. Meanwhile, the ceiling on deal values for Chinese innovative drugs was broken through in 2025, highlighting the value of platform and technology licensing.

Overview of License-in and License-out Deals for Innovative Drugs in China, 2020–2025

Overview of License-in and License-out Deals for Innovative Drugs in China, 2020–2025

Data Source: MedPeer, VBInsight

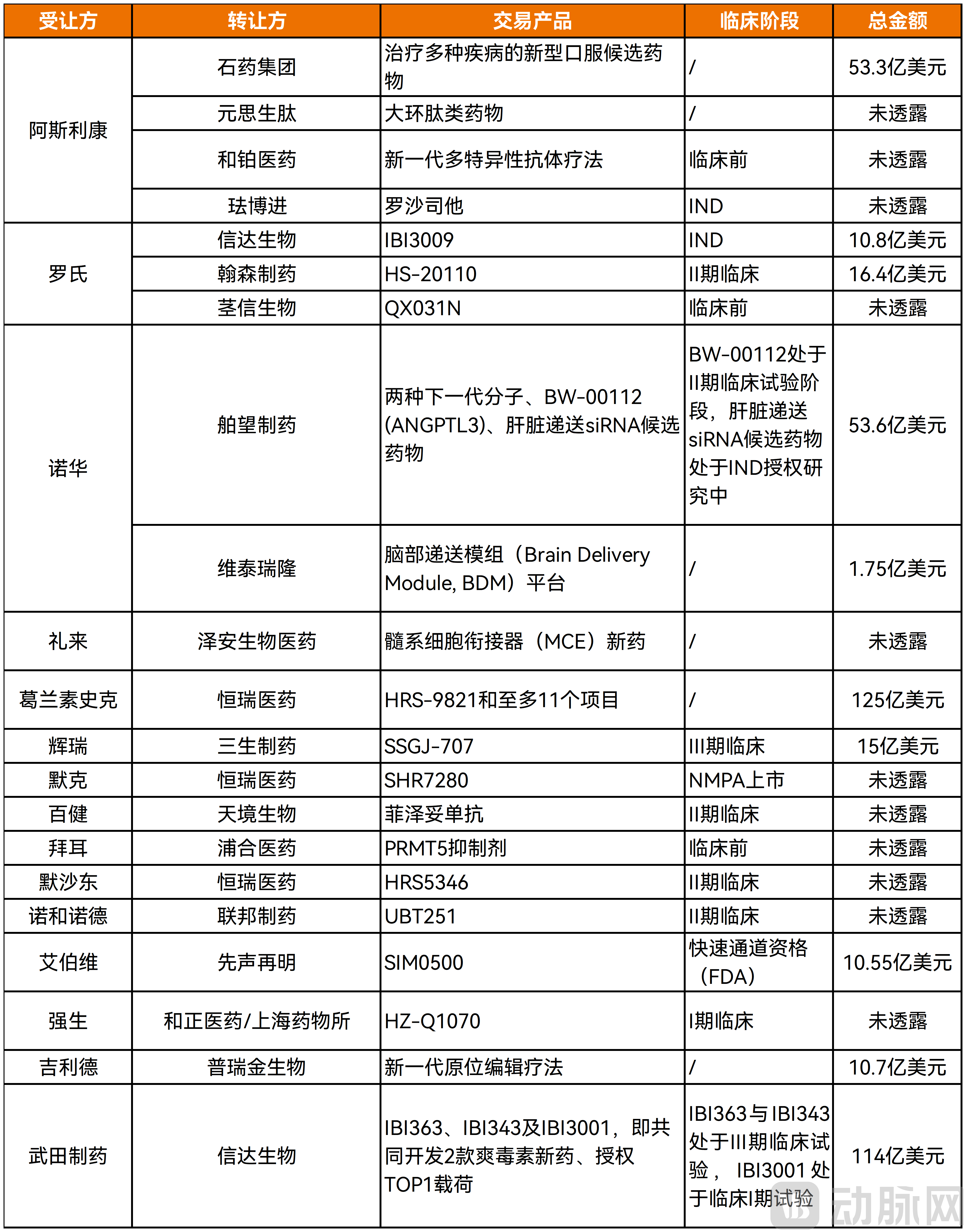

From the perspective of licensees, global pharmaceutical giants such as GSK, Novartis, AstraZeneca, Merck & Co., Eli Lilly, and Gilead have been exceptionally active, forming the main force in licensing Chinese innovative assets and underscoring the global competitiveness and appeal of China’s R&D achievements.

Overview of MNCs’ Moves in Innovative Drugs and the Supply Chain from January to October 2025

Data Source: VBInsight, MedPartner

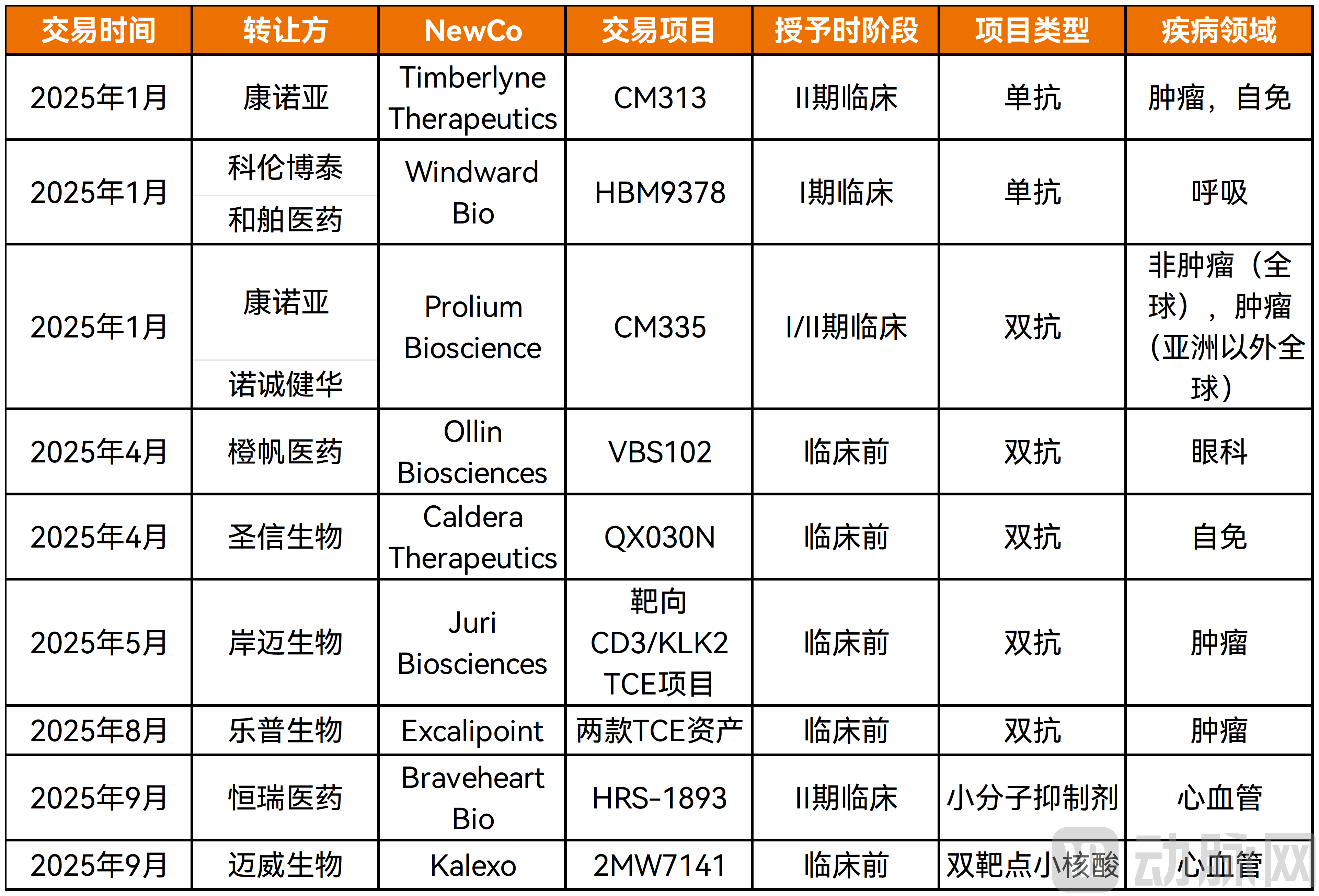

In 2025, NewCos are poised to transition from sporadic exploration in 2024 to scaled-up application, emerging as the second mainstream pathway for global expansion after traditional license-out deals. Furthermore, the asset types of NewCos have expanded from late-stage clinical candidates to early-stage technology platforms, with per-project valuations generally ranging between $200 million and $800 million.

As of October 30, 2025, NewCo model transactions in China’s innovative drug and supply chain sectors were more active than during the same period in 2024, with five publicly disclosed NewCo deals in the first half of the year alone, nearly matching the six transactions recorded for the entire year of 2024.

Public Newco Deals in Innovative Drugs and Supply Chain, January–October 2025

Data Source: PharmaCube, VBInsight

3Overview of Key Product and Technological Innovations

Major Stages in the Development of Innovative Drugs in China

Major Stages in the Development of Innovative Drugs in China

Source: VBInsight

Chapter 2: Insights into the Most Valuable Fields and Product Competitiveness in 2025

2.1 Rapid Technological Iteration and Differentiated Strategic Layouts Highlight China’s Growing International Influence in ADCs

From an industrial positioning perspective, China’s ADC sector has gradually transitioned from the early stage of “technology following” to a parallel-running phase characterized by “independent innovation + international competition.”Achieved synchronized global development in traditional target areas such as HER2 and Trop2, established differentiated competitive advantages in emerging targets like Claudin 18.2 and B7-H3, with clinical data for certain products reaching globally leading standards, thereby providing core support for the high-quality development of China’s innovative pharmaceutical industry.

As of October 2025, there are 21 ADC drugs marketed globally, among which 5 products were developed or independently approved by Chinese companies. Notably, 3 of these were launched in 2025 alone, compared to just 1 in 2021. Over the past five years, domestically produced ADCs have evolved from filling market gaps to helping define industry standards. The global ADC landscape has been systematically reshaped by Chinese contributions, with a solid industrial foundation now firmly established.

Overview of Marketed ADC Products as of October 2025

Overview of Marketed ADC Products as of October 2025

Data source: PharmaCube, public information

2.2 Accelerated Global Expansion of Domestically Produced Bispecific Antibodies, with Clearly Differentiated Specialized Technical Pathways

In 2025, the global bispecific antibody (BsAb) drug market underwent a qualitative transformation. The market size reached $13 billion in the first three quarters, representing a year-on-year increase of 33%, and is projected to surpass the $17 billion mark for the full year. Furthermore, thanks to the issuance of the National Reimbursement Drug List for Basic Medical Insurance, Maternity Insurance, and Work-Related Injury Insurance (2025 Edition) and the inaugural Commercial Health Insurance Innovative Drug Catalogue (2025 Edition), bispecific antibodies were officially included. This inclusion marks the transition of bispecific antibody drugs from a technical concept to a commercial pillar.

The core driver behind the market explosion is technological breakthrough.The core breakthrough of bispecific antibodies lies in their unique mechanism of action. Compared with traditional monoclonal antibodies, bispecific antibodies can simultaneously target two different signaling pathways, achieving a synergistic therapeutic effect. This “1+1>2” therapeutic paradigm has demonstrated significant advantages across multiple therapeutic areas.

2.3 Existing Pain Points Spawn New Opportunities, with Universal CAR-T and In Vivo CAR-T Advancing in Tandem

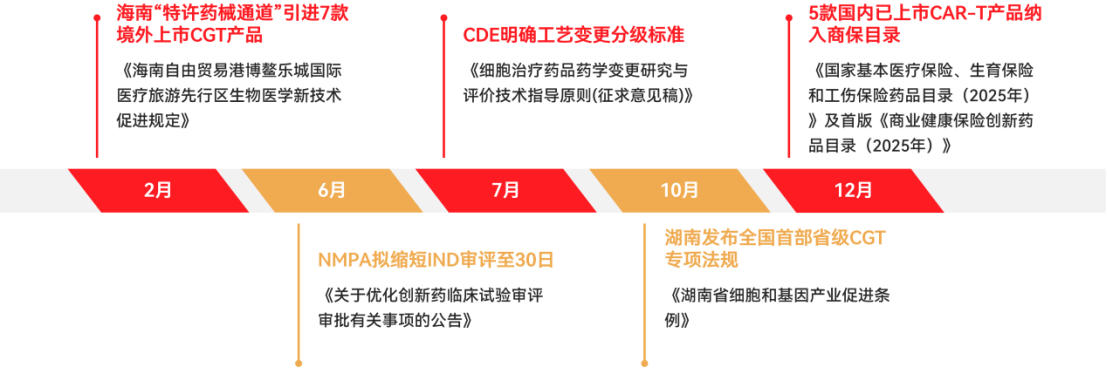

In 2025, regulatory oversight of China’s cell and gene therapy (CGT) industry continued to tighten and become more standardized. In the first half of 2025, the National Medical Products Administration (NMPA) intensively rolled out a series of more targeted regulatory policies to ensure the safety and efficacy of CGT products, particularly chimeric antigen receptor T-cell (CAR-T) therapies.These policies cover the entire process from clinical trials to commercial-scale manufacturing, aiming to promote standardized industry development and prevent unregulated growth.

Key Policies Related to Cell Therapy in China in 2025

Key Policies Related to Cell Therapy in China in 2025

Data source: public information

However, despite the approval and market launch of multiple CAR-T products, the commercialization of CAR-T therapy faces significant challenges due to treatment costs generally exceeding one million yuan and limited current insurance coverage. Patients not only have to wait several weeks but also confront high costs amounting to hundreds of thousands of dollars, as well as additional risks associated with chemotherapy-induced myeloablation.

Universal CAR-T (allogeneic CAR-T) is a breakthrough solution for the current exorbitantly priced cell and gene therapies.The primary reason for the high cost of CAR-T therapy lies in its predominantly personalized nature, which makes it difficult to reduce the price of related products. Universal CAR-T therapies mainly face two challenges: GvHD (graft-versus-host disease) and HvG (host-versus-graft reaction). Furthermore, if their efficacy is insufficient, universal CAR-T therapies characterized by “low cost and low efficacy” remain a suboptimal choice.

Chinese research institutions have made significant progress in emerging technological fields such as iPSC-derived cell therapies, driving a rapid increase in the number of clinical trials for universal CAR-T products in 2025. In 2025, more than 20 companies in China have established pipelines for universal CAR-T therapies, with nearly 20 candidates already entering the clinical validation phase.

Overseas companies such as Interius, Umoja, and Kelonia are exploring in vivo CAR-T therapies, which also highlight the “off-the-shelf” feature in an attempt to break through the pain points of traditional CAR-T.The competition in the field of in vivo CAR-T is essentially a race in delivery technology,Multiple domestic companies have established their presence in this field. Currently, most pipelines remain in the preclinical stage, with relatively limited clinical data available. Successfully transitioning from preclinical research to clinical development and improving development efficiency have become critical challenges.

2.4 Process Optimization + Efficacy Validation: Domestically Produced TIL Therapy Begins to Overtake on the Curve

Over the past two years,China’s TIL (Tumor-Infiltrating Lymphocytes) sector is witnessing a rare “explosive” catch-up:From nine publicly disclosed pipelines in 2023 to nearly twenty by 2025, the number of Investigational New Drug (IND) applications accepted rose from 10 to 15, with 10 clinical trial approvals secured, covering more than ten types of solid tumors including melanoma, cervical cancer, liver cancer, lung cancer, and pancreatic cancer. This “China speed” is driven by the convergence of three forces: technology, policy, and capital.

In terms of technological iteration, with process innovations and the introduction of automation technologies, cancer patients no longer need to wait nearly a month for TIL therapy specifically prepared for them; meanwhile, increased production yields and optimized cost control lay the foundation for subsequent price reductions and large-scale adoption of TIL therapy.

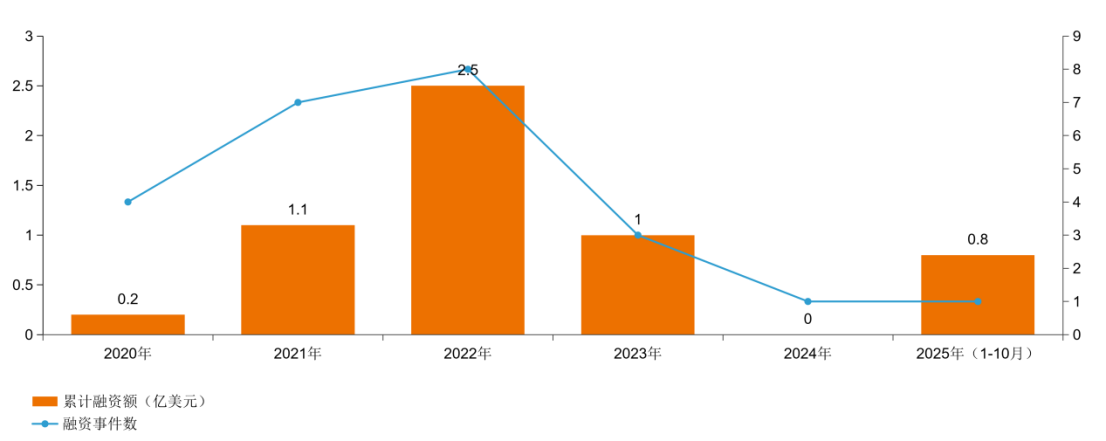

According to data from VBInsight, the total financing raised by domestic TIL therapy companies in China exceeded RMB 2 billion between 2023 and 2024, despite the unfavorable conditions in the primary market. This period saw numerous large-scale funding rounds exceeding RMB 100 million each, with investor sentiment shifting from cautious observation to aggressive participation. Furthermore, these companies are gradually transitioning from the startup phase to the growth stage, and moving toward maturity.

Overview of Financing in China's TIL Sector from 2020 to 2025

Overview of Financing in China's TIL Sector from 2020 to 2025

Source: VBInsight

In terms of policy, in December 2024, the Chinese Association of Medical Biotechnology officially released the first “Group Standard for the Preparation and Quality Control of TIL Products” (hereinafter referred to as the “Group Standard”). Endorsed by the National Medical Products Administration (NMPA) and academician teams, this standard incorporated culture duration, release criteria, and dose calculation into industry consensus for the first time. In the same year, the Center for Drug Evaluation (CDE) included TIL therapy in its “Breakthrough Therapy” list, shortening the review timeline and allowing multiple companies to submit rolling applications based on Phase I clinical data, thereby significantly accelerating clinical translation.In 2026, China is expected to welcome the first domestically produced TIL therapy product to market.

2.5 China’s CXO Industry Driven by BD: Breaking Through via “Integrated Solutions” or “Niche Specialization”

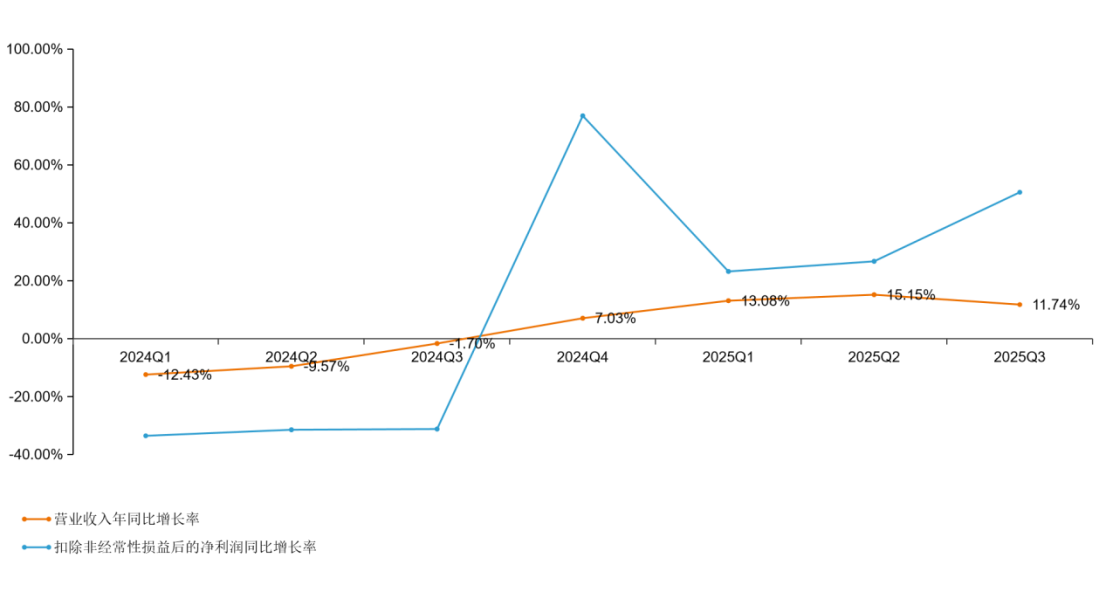

2025,The primary and secondary markets for China's CXO industry present distinct landscapes.From January to October 2025, there were a total of 39 financing deals in China’s CXO sector, with cumulative funding exceeding $340 million. This figure has continued to decline since 2021, aligning with the financing trends for innovative drugs in China.

Some CXO companies in the secondary market, especially the leading enterprises, have seen a significant recovery in their fundamentals.

In fact, by early 2024–2025, many companies had already shown a clear trend of recovery. Among them, TopAlliance Biosciences’ audited full-year results for the year ended December 31, 2024, revealed that the company’s performance exceeded expectations, with annual revenue surpassing RMB 1 billion, representing a 41% year-on-year increase. Product sales revenue grew by 39% year on year, while CDMO/CMO business revenue increased by 47% year on year.

Revenue and Net Profit Growth Rates in the CXO Sector, Q1 2024–Q3 2025

Revenue and Net Profit Growth Rates in the CXO Sector, Q1 2024–Q3 2025

Data Source: Soochow Securities

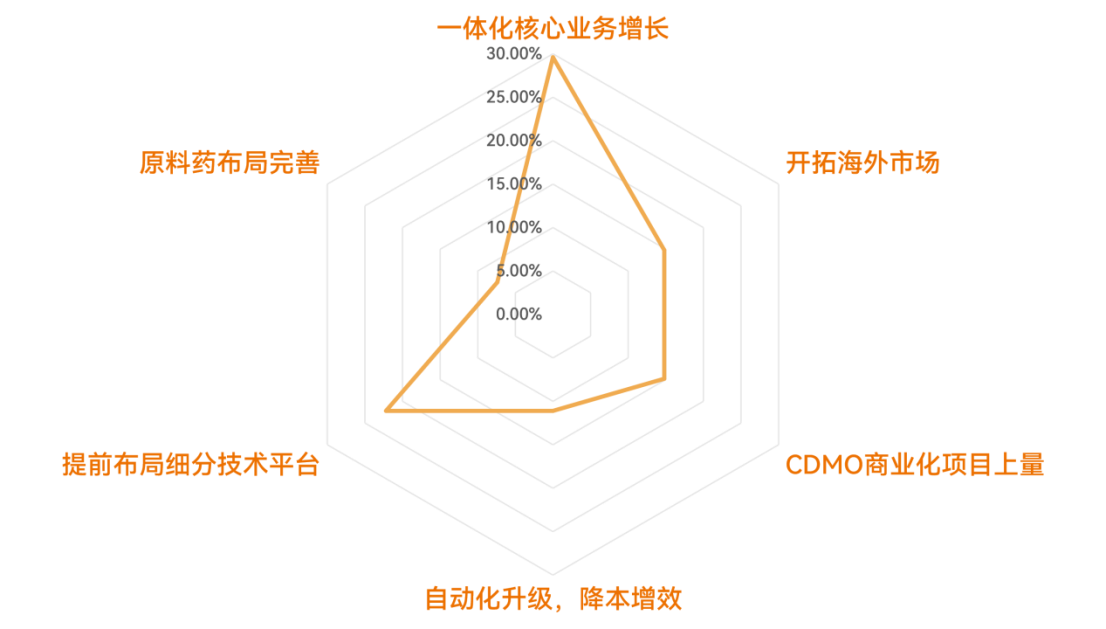

The “Matthew Effect” among industry leaders is becoming evident. During the industry downturn, leading enterprises are not only weathering the storm but also expanding their market share against the trend, leveraging their “integrated, end-to-end” platform advantages, robust cash flow, and global brand credibility. The exit or contraction of small and medium-sized competitors has, in turn, ceded market space to these leaders. On a more granular level, the recovery in the secondary market is not evenly distributed; rather, it is marked by divergence. For instance,If they do not pursue an “integrated” path, CXO companies equipped with leading technology platforms and deeply embedded in cutting-edge therapeutic areas will be better positioned to sustain revenue growth by leveraging their forward-looking strategies and differentiated advantages.

Reasons for the Performance Growth of Listed CXO Companies

Reasons for the Performance Growth of Listed CXO Companies

Data Source: Annual Reports of Listed Companies

2.6 Multiple IPOs Propel Small-Molecule Innovative Drugs into the Harvest Phase, with Weight Loss as a Key Growth Engine

In 2025, China’s small-molecule sector demonstrated a structural recovery and significant quality improvement, driven by breakthroughs in technology platforms, enhanced clinical translation efficiency, and the development of global capabilities, following fluctuations in the capital cycle. Although the overall financing environment has become more prudent, capital is accelerating its concentration toward enterprises with clear clinical value, differentiated technology platforms, and late-stage commercialization potential. Frontier areas such as weight management and autoimmune diseases have become the focus of global capital pursuit. With intensive realization of clinical pipelines and the market launch of multiple first-in-class products, China’s small-molecule innovation is advancing into a new phase of “defining standards.”

2.7 Over 100 Domestic Companies Enter the AI Drug Discovery Space, with Application Implementation Entering the Phase of Value Realization

Against the backdrop of accelerating paradigm shifts in global biomedical innovation, the deep integration of artificial intelligence with drug development has moved beyond the scope of mere auxiliary tools,Rather, it is gradually evolving into the core infrastructure that reshapes industry logic and reconstructs the value chain.In 2025, total financing in China’s AI-driven drug discovery sector experienced a phased correction, yet breakthroughs in technological platforms and global export capabilities reached new heights. Leading enterprises achieved platform-level licensing that spans from “molecular design” to “end-to-end R&D systems,” propelling the industry’s transition from technology validation to value realization.

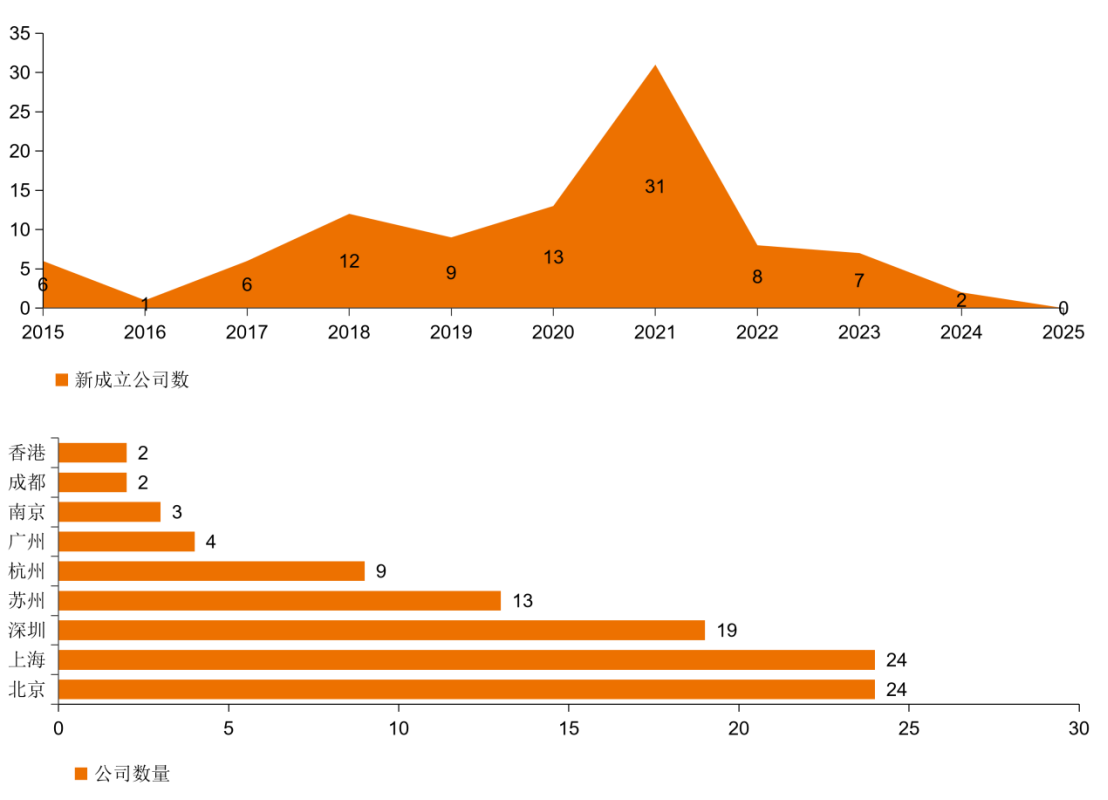

China’s AI-driven drug discovery sector has developed a vibrant ecosystem of over 100 active companies. These enterprises can be categorized by business model into CRO service providers, companies with self-developed pipelines, and software platform vendors, although the boundaries between these categories are increasingly blurred, reflecting a trend toward the integration of services, pipelines, and platforms. The Beijing-Tianjin-Hebei, Yangtze River Delta, and Pearl River Delta clusters account for more than 85% of these companies, demonstrating a pronounced agglomeration effect, while the number of new company formations has remained stable in recent years.

Newly Established AI Drug Discovery Companies in China and Their Geographic Distribution

Newly Established AI Drug Discovery Companies in China and Their Geographic Distribution

Source: Public information; chart by VBInsight

Chapter 3: Four Major Trend Predictions for the Innovative Drug and Supply Chain Industry in 2026

As the innovative drug sector undergoes a profound value reassessment amid market adjustments in 2025, the industry is entering a “post-BD era” characterized by product strength as its core, globalization as its benchmark, and platform-based capabilities as its barrier. The fundamental logic driving industrial growth is shifting: from value discovery reliant on single transactions to building sustainable competitive advantages through scientific innovation depth, clinical execution efficiency, and commercialization realization capabilities. In 2026, the industry will accelerate its divergence, with only those enterprises possessing the following core capabilities able to navigate the cycle and lead the future.

3.1 Iteration of Technological Paradigms: Frontier Technologies Transition from “Proof of Concept” to “Realization of Clinical and Commercial Value”

In 2026, technological iterations in core areas such as antibody-drug conjugates (ADCs), cell therapies, small molecules, and bispecific antibodies will no longer be confined to laboratories or early-stage clinical trials. Instead, they will enter a deep phase of industrialization, clearly oriented toward addressing unmet clinical needs, enhancing accessibility, and boosting commercial value. Technological leadership will directly translate into market influence and pricing power in transactions.

Overview of Technological Trends

Overview of Technological Trends

Data Source: Chart by VBInsight

3.2 Elevating the Competitive Dimension: From “Single-Point Breakthroughs” to “Systematic Global Capabilities”

In 2026, the competitive arena for Chinese innovative pharmaceutical companies will undoubtedly expand to a global scale. Success will no longer be defined solely by domestic market launch or out-licensing of individual products, but rather by building end-to-end operational capabilities spanning R&D, regulatory registration, manufacturing, and commercialization.

3.3 Divergence in Industry Structure: Platform Leaders and Specialty Technology Companies Jointly Build a New Ecosystem

Under the dual pressures of value regression and global competition, China’s innovative drug industry in 2026 will exhibit a landscape characterized by the coexistence of high concentration and deep segmentation, with an intensifying Matthew effect.

3.4 Payment System Reform: Commercial Insurance Formularies Guide Innovative Drugs from “Optional” to “Essential”

The release of the 2025 “Catalogue of Innovative Drugs for Commercial Health Insurance” marks a landmark event in the development of China’s multi-tiered medical security system. It represents not merely the addition of a new payment channel, but a systematic restructuring of market access and reimbursement mechanisms for high-value innovative therapies. In 2026, the impact of this policy will transition from framework establishment to substantive implementation, driving the innovative drug market toward a new ecosystem powered by the synergy between basic medical insurance and commercial health insurance, and reshaping pharmaceutical companies’ pricing, market access, and commercial strategies.

Based on the white paper’s analysis of innovation logic across major high-value sectors and corporate implementation practices, this year’s edition highlights the Top Ten Outstanding Innovation Cases.

(The above is an excerpt from the main content of the white paper. To obtain the full report, please scan the QR code below.)

Table of Contents:

Chapter 1: Overview of Hot Topics in the Innovative Drug and Supply Chain Industries in 2025

1.1 China’s Innovative Drug Policy System Enters a New Phase of Systematic Guidance, Achieving Full-Cycle Integration and Precision Support

1.2 Value Reversion in Industry and Capital Markets: Capital Concentrating on "Certainty" and "Globalization"

1.3 Overview of Key Products and Technological Innovations

Chapter 2: Insights into the Most Valuable Fields and Product Competitiveness in 2025

2.1 Rapid Technological Iteration and Differentiated Strategic Layouts Highlight China’s Growing International Influence in ADCs

2.2 Accelerated Global Expansion of Chinese-Made Bispecific Antibodies, with Clearly Differentiated Technical Pathways

2.3 Existing Pain Points Spawn New Opportunities, with Universal CAR-T and In Vivo CAR-T Advancing in Tandem

2.4 Process Optimization + Efficacy Validation: Domestically Produced TIL Therapy Begins to Overtake on the Curve

2.5BD-Driven Domestic CXO: Breaking Through with “Integrated” or “Small and Beautiful” Models

2.6 Multiple IPOs Propel Small-Molecule Innovative Drugs into the Harvest Phase, with Weight Loss as a Key Growth Engine

2.7 Over 100 Chinese Companies Enter AI Drug Discovery, with Applications Entering the Phase of Value Realization

Chapter 3: Four Major Trend Predictions for the Innovative Drug and Supply Chain Industry in 2026

3.1 Iteration of Technological Paradigms: Frontier Technologies Move from "Proof of Concept" to "Realization of Clinical and Commercial Value"

3.2 Elevating the Competitive Dimension: From "Point Breakthroughs" to a Contest of "Systematic Global Capabilities"

3.3 Industry Landscape Divergence: Platform Leaders and Specialized Technology Companies Jointly Build a New Ecosystem

3.4 Payment System Reform: Commercial Insurance Formularies Guide Innovative Drugs from "Optional" to "Essential"