Three sources of capital rush back to innovative drugs

A noteworthy signal is emerging: global innovative drug funding appears to be flowing back in rapidly.

Earlier this year, a well-known overseas pharmaceutical media outlet reported that after four consecutive years of decline, the biopharma sentiment index surged sharply heading into 2026. Predictions like this, however, emerge almost every year. The article surveyed nearly a thousand pharmaceutical professionals, some of whom are corporate executives, and their assessments of current and future business conditions, financing, financial health, and the regulatory environment were almost uniformly optimistic.

Of course, as usual, this survey failed to attract much attention. But judging from global capital flows in late March and early April, this optimism appears to have been validated.

Billions of Dollars Have Poured In

First, let's look at the data. After the global biopharma secondary market strengthened overall in 2025, it continued to trade at elevated levels with volatility in the first quarter of 2026, showing a trend of linked upward movement.

In the U.S. equity market, the pharmaceutical sector rebounded, led by giants such as Eli Lilly. As of the end of the first quarter, the S&P 500 Health Care Index recorded a cumulative increase of approximately 8% to 12%, with quarterly net capital inflows of approximately $4 billion. In Hong Kong and the STAR Market, the pharmaceutical sector experienced a staged rebound in March following a period of volatility, showing some correlation with the U.S. market. On March 10 and March 27, both markets saw significant increases in their pharmaceutical indices, with some single-day gains exceeding 5%. According to Wind data, total quarterly capital inflows for the two markets reached nearly 15 billion RMB. Since late March, the pharmaceutical indices in the U.S., Hong Kong, and the STAR Market have continued their upward trend.

Pharmaceutical stocks have seen frequent rebounds in recent years after a sharp decline from their 2021 highs, which is not surprising in itself. However, when combined with synchronized efforts from the industry and private equity funds, the picture becomes more interesting.

On one hand, a rare wave of concentrated M&A by MNCs has emerged. Since the beginning of 2026, MNCs have significantly accelerated their pace of acquisitions. Notably, in just two weeks from late March to early April, six MNCs completed eight acquisition deals, injecting nearly $50 billion into the innovative drug market. Among them, Gilead and Eli Lilly were the most active, each making three acquisitions, spending $12.65 billion and $9.9 billion respectively.

Partial MNC Acquisition Deals Since 2026. Data Source: VBData

Interestingly, in these transactions, MNCs generally offered substantial premiums to secure their chosen targets. For example, Biogen acquired Apellis at a premium as high as 140%, Gilead acquired Arcellx at a 79% premium, Servier acquired Day One at a 68% premium, and Eli Lilly acquired Ventyx at a 62% premium. Furthermore, in MSD's transaction with Terns, four buyers were simultaneously bidding, with MSD winning the deal by offering the highest price combined with more favorable transaction terms.

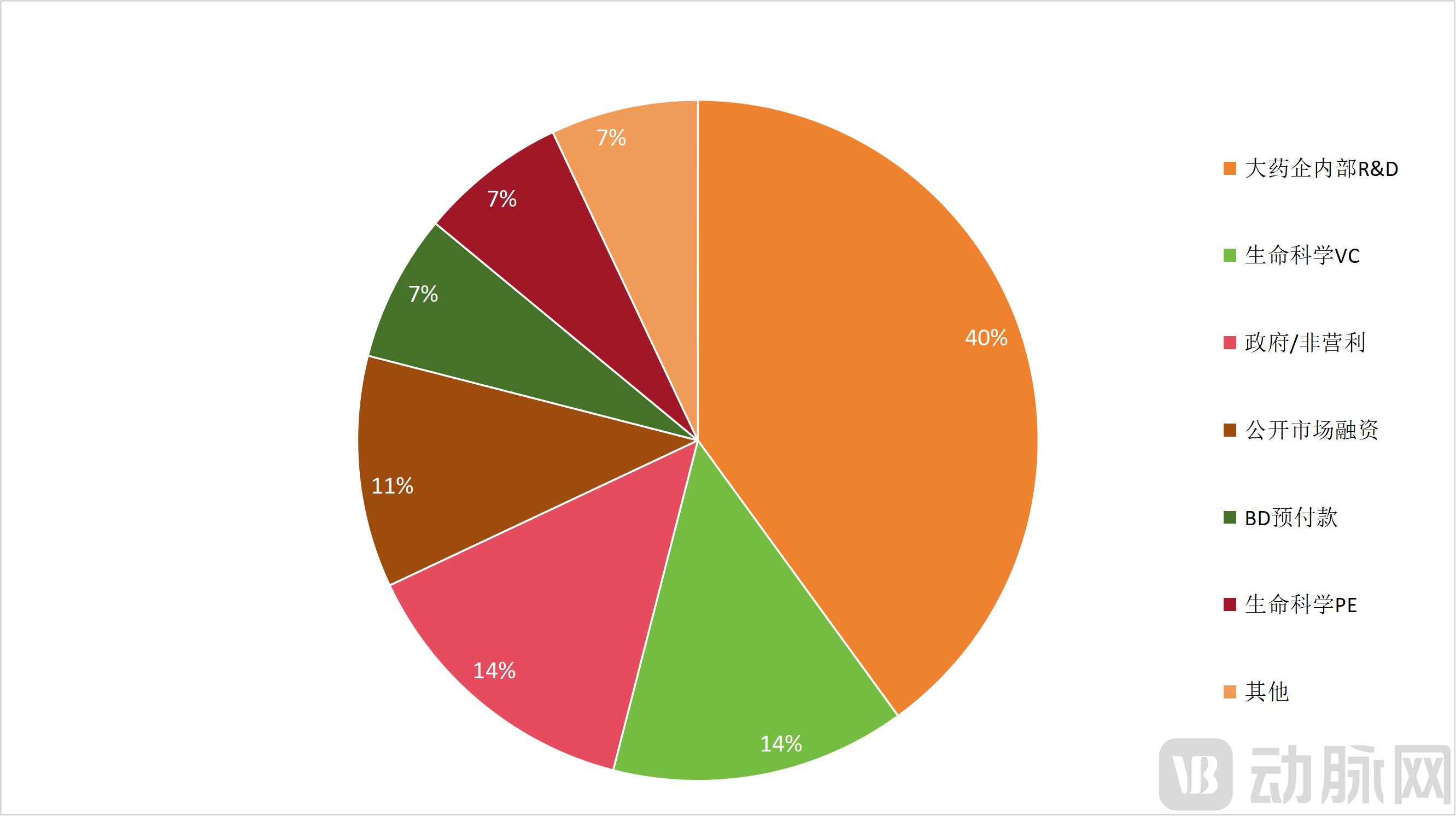

On the other hand, private equity funds have raised epic amounts of capital. At the end of March, Blackstone Group, one of the world's top 10 PE funds, announced that its Life Sciences VI Fund had completed fundraising of $6.3 billion, setting a record for the largest private fundraising in the history of the life sciences industry. This standalone event carries special significance at a time when global innovative drug funding is slowly recovering. In the innovative drug ecosystem, PE funds and VC funds work in synergy, serving as important external sources of capital for biotechs. According to the VBData, among the total global innovative drug financing in 2025, PE funds accounted for 7%, roughly equivalent to the total upfront payments from licensing deals. While not a large share, this contribution plays a critical role.

Global Innovative Drug Financing Structure in 2025. Data Source: VBData

Typically, PE funds step in during Phase II or Phase III clinical stages, helping biotech companies bridge the "last mile" from the lab to the clinic at the point when their capital pressure is greatest. Before blockbuster drugs such as Humira and Truvada were launched, mainstream PE funds like Royalty Pharma had entered the picture, investing hundreds of millions of dollars in exchange for billions of dollars in future royalty revenue.

Blackstone Life Sciences' record-breaking PE fundraise is not only an important milestone in the cyclical recovery but also a sign that mainstream LPs — including pension funds, sovereign wealth funds, and insurance funds — are regaining confidence in innovative drugs. For biotechs that were on the brink of failure before dawn, the return of PE funds is an even more encouraging signal than record-breaking licensing deals.

The Golden March and Silver April of Innovative Drugs

If we look only at the data level, capital from the stock market, industry, and private equity appears to be rushing back into innovative drugs with a vengeance. But once we move past the surface-level excitement to examine the underlying reasons, the situation is far less encouraging than it seems.

First, let's look at MNC acquisitions at the micro level. In reality, MNCs have simply accelerated their acquisition pace cyclically, rather than suddenly becoming more generous with their spending.

Looking at the short-term cycle within the year, it is customary for MNCs to complete asset transactions around major industry conference periods. The J.P. Morgan Healthcare Conference (JPM) in January, the American Association for Cancer Research Annual Meeting (AACR) in April, and the American Society of Clinical Oncology Annual Meeting (ASCO) in May are all key periods when biotechs showcase their innovative results and MNCs go on concentrated buying sprees, accounting for the majority of innovative drug asset transactions throughout the year. For example, during the JPM conference weeks in 2024 and 2025, innovative drug asset transaction values reached $8 billion and $20 billion respectively, equivalent to a full quarter of activity in the second half of the year. Johnson & Johnson's $14.6 billion acquisition of Intra-Cellular Therapies, for instance, occurred during the 2025 JPM conference week.

The recent wave of MNC acquisitions in late March and early April coincides with the period following the JPM conference and the lead-up to the AACR and ASCO conferences. In March and April of the past two years, MNCs also experienced small waves of acquisitions.

Data shows that during the 2024 AACR/ASCO conference period, eight acquisition deals with total values exceeding $1 billion were announced, marking the most active period of the year. Blockbuster deals such as Vertex's $4.9 billion acquisition of Alpine and Merck's $3 billion acquisition of EyeBio all occurred during this period. During the same period in 2025, innovative drug assets again saw a surge in both volume and pricing, with major deals such as Novartis's $1.7 billion acquisition of Regulus and BioNTech's $1.25 billion acquisition of CureVac. The stock prices of several biotechs also surged over a short period, with gains approaching 50% at one point. This year has been even more active than before. The JPM conference week in January unexpectedly saw a lull in asset transactions, but the underlying transaction logic has not changed, explaining the more concentrated wave of MNC acquisitions during this same period this year.

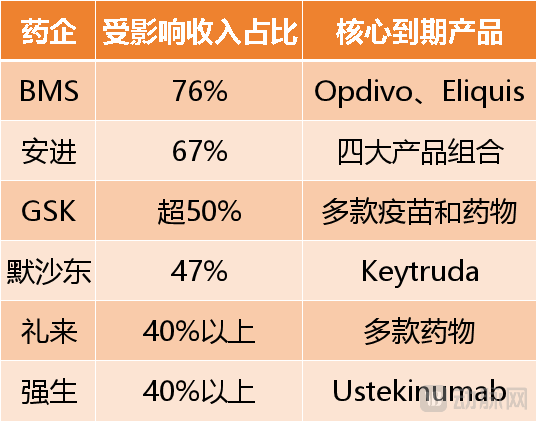

Looking at the long-term cycle across multiple years, the approaching patent expirations of blockbuster drugs have created an urgent need for MNCs to replenish their pipelines, objectively driving the sharp increase in innovative drug asset transactions since 2025. Typically, although MNCs often have a broad portfolio, their revenue during specific periods depends on one or more specific blockbuster drugs. For example, Humira for AbbVie in the early years, Opdivo for BMS today, and tirzepatide for Eli Lilly — the revenue generated by a single product determines the performance of the entire enterprise. The core logic behind this is the exclusive market period brought by the patent barriers of original innovative drugs. Patent expiration means losing market exclusivity.

According to incomplete statistics from VCBeat, between 2026 and 2028, the core patents of a large number of blockbuster drugs will expire, including BMS's Opdivo and MSD's Keytruda. The MNCs that have been actively transacting during this period — including BMS, GSK, Eli Lilly, and MSD — are all on this list. Take BMS as an example: the patents for Eliquis and Opdivo will both expire in 2028. These two drugs are BMS's revenue pillars, generating $13 billion and $9 billion in sales respectively in 2024. Once the patent barriers are lost, this revenue — accounting for 76% of BMS's total sales — will be sharply eroded by generic competition.

Some MNCs and Drugs Affected by the Patent Cliff. Data Source: Public Information Compilation

To address the patent cliff, MNCs have accelerated their acquisition pace since 2023, with multi-billion-dollar deals appearing frequently. For example, in December 2023, BMS acquired Karuna for $14 billion, securing the schizophrenia drug KarXT and entering the CNS space. Around the same time, AbbVie acquired ADC leader ImmunoGen for $10.1 billion, building a second growth engine beyond immunology. By 2026, even more MNCs have taken center stage with greater intensity. Eli Lilly, the most active dealmaker, derives nearly 50% of its revenue from metabolic drugs such as tirzepatide, dulaglutide, and empagliflozin, and is therefore forced to continuously search for a second growth curve to counter the impact of the patent cliff. In 2024, Lilly acquired Morphic Therapeutics for $3.2 billion to expand into immunology. Among its three acquisitions this year, the most notable is Centessa, which further expands Lilly's presence in CNS — a clear illustration of this strategy.

Looking at the broader capital landscape, the current recovery remains largely technical in nature. At present, both the secondary market and PE/VC funds are at historic lows. Since 2021, global capital markets have been mired in a prolonged downturn. Although several rebounds in recent years have somewhat boosted market sentiment, objectively speaking, the market is still at a low level. Take the A-share market as an example: from 2023 to the present, the P/E ratio of the pharmaceutical sector has fluctuated within the range of 25 to 27 times, consistently hovering around the 10th percentile of the past decade — meaning it is cheaper than 90% of the time in the last ten years. The U.S. market is similarly depressed. Based on the price of the SPDR S&P Biotech ETF (XBI), which fell from a high of $175 in 2021 to $66.66 in March 2026, the decline remains as steep as 62%.

The PE market is no different. Between 2022 and 2023, fundraising and investment activity in global life sciences PE funds slowed markedly. Leading life sciences PE funds, including Blackstone Life Sciences and Novo Holdings, saw significantly extended closing periods, with some taking 24 to 30 months to close, compared to the previous norm of 18 months. In 2022 and 2023, total investment by global life sciences PE funds plummeted from approximately $30 billion a year earlier to around $15 billion. It was only after 2024 that life sciences PE funds became active once again.

Will it Heat Up in China?

Regarding expectations for a bull market, the industry is most concerned about whether China will follow the trend. Setting aside the rebound in the secondary market — for which there are already signs in China — the key now lies in MNC acquisitions and PE funds.

On the MNC acquisition front, for a considerable period of time, MNCs will maintain a pipeline licensing deal relationship with Chinese biotechs rather than pursuing direct acquisitions. For MNCs, the cost-effectiveness of fully acquiring Chinese biotechs is relatively low. Apart from regulatory differences and geopolitical risks, such acquisitions would also involve the challenging work of integrating innovative drug ecosystems and reshaping corporate cultures both in China and internationally. The continued surge in licensing deals in recent years reflects MNCs' growing recognition of Chinese innovative drug assets. According to incomplete statistics from VCBeat, since 2024, there have been nearly 300 licensing deals between Chinese biotechs and MNCs, but fewer than five outright acquisitions in history — a truly rare occurrence.

One noteworthy point is that due to intensifying competition, MNCs have now pushed the average total transaction value for licensing Chinese biotech assets to more than double that of comparable transactions in other regions around the world. They would rather pay a premium for pipelines than sit down to discuss acquisitions. This suggests that MNC acquisitions will remain off the table as an exit pathway for Chinese biotechs.

Furthermore, even when dealing with overseas biotechs, although MNCs spend generously, they remain highly cautious. VCBeat has observed that in this year's transactions, MNCs have increasingly used Contingent Value Rights (CVRs). For example, in Eli Lilly's acquisition of Centessa, the approval of the OX2R drug was used as a contingent condition.

Part Includes MNC Acquisitions with CVR. Data Source: Collation of Public Information

Part Includes MNC Acquisitions with CVR. Data Source: Collation of Public Information

This is an additional clause in merger agreements. The buyer commits to paying an extra amount upon the achievement of specific milestones, such as drug approval or a clinical trial reaching a certain endpoint. If the milestone is not achieved, the CVR goes to zero, and the buyer does not have to pay. The essence of a CVR is to split the acquisition consideration into two parts: a certain portion paid upfront, and an uncertain portion paid conditionally based on outcomes. In acquisition transactions, the CVR is a classic risk transfer tool that buyers use to protect themselves amid uncertainty.

On the PE fund front. Historically, top global PE funds have rarely ventured into domestic biotech investments, and Blackstone, despite its record-breaking fundraise, has not made a single investment in this space. Therefore, the recovery and record-breaking performance of these PE funds have little impact on Chinese biotechs. However, as an investment model distinct from VC, China's domestic pharmaceutical PE funds have begun to emerge this year.

Since 2023, industrial funds have been established in cities such as Chengdu, Hangzhou, Suzhou, Beijing, Shanghai, and Shenzhen. Among these industrial funds, some carry management and investment logic reminiscent of PE funds.

For example, the Shanghai Biomedical M&A Fund, which completed its first closing in March 2025, was initiated by Shanghai Industrial Investment. Its LPs include social capital such as Shanghai Pharmaceuticals, Tofflon, and Junshi Biosciences. The fund focuses primarily on control acquisitions, integrating acquired companies into listed company systems and exiting after integration. In November 2025, the Shanghai Biomedical M&A Fund acquired a 21.9% stake in Kanghua Biological, becoming its controlling shareholder — a transaction that closely mirrors the practices of overseas PE funds. Although the scale of China's domestic pharmaceutical PE funds remains very small, the gradual recovery of the global life sciences PE fund market and the return of established LPs to the battlefield is undoubtedly good news for China's domestic pharmaceutical PE funds.

Overall, despite a stream of positive capital-related news from the stock market, industry, and PE side, spring has still not truly arrived for the innovative drug industry. This is especially true for China's domestic innovative drugs.