Opportunities and Challenges in Novel Target Innovation for Oncology Drug Development

In the oncology drug market,First-in-Class DrugDemonstrating extraordinary commercial value. Taking programmed death receptor 1 and its ligand (PD-1/PD-L1) inhibitors as an example, since the approval of the first drug, pembrolizumab, in 2014, global sales of this class of drugs reached $55 billion in 2024, accounting for nearly one-fifth of the entire oncology drug market.

However,Nature Reviews Drug DiscoverAn analysis published on December 17, 2025, revealed that although first-in-class drugs accounted for only 31% of marketed oncology therapies, they generated 41% of market revenue, amounting to $119 billion. More notably, target novelty exhibited a significant stepwise decline across different stages of drug development, a trend that underscores the delicate balance between innovation and risk within the industry.

In oncology drug development,TargetIt refers to the specific molecular targets or biological pathways through which drugs exert their effects, typically key proteins that promote tumor growth, survival, or metastasis. First-in-class drugs refer to new molecules developed against a particular target for which no approved therapies currently exist in oncology indications.

The counterpart to first-in-class drugs isFollow-on Drug (also known as Me-too Drug), namely follow-on drugs developed against targets of already approved medications. The success of PD-1/PD-L1 inhibitors is a typical case demonstrating the value of first-in-class drugs: by blocking tumor cells’ suppression of the immune system, these agents reactivate the body’s own anti-tumor immune response, ushering in a new era of cancer immunotherapy.

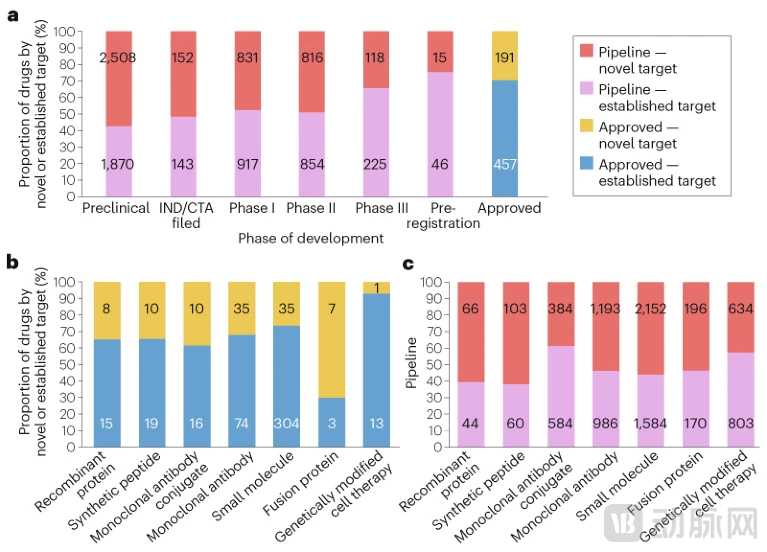

Figure: Trends in the Novelty of Oncology Drug Targets

(Source: Nature Reviews Drug Discovery)

The Selection of Target Novelty Is a Double-Edged Sword in Drug Development.

On the one hand, drugs developed against novel targets, if successfully launched, often yield significant market returns and competitive advantages, because theyAddresses unmet clinical needs that current therapies fail to satisfy.

On the other hand, new targets entail higher R&D risks:Lack of Clinical Validationbiological mechanisms may lead to suboptimal efficacy, and unknown safety issues may emerge in later-stage clinical trials. Therefore, pharmaceutical companies and investors often tend to adopt risk mitigation strategies when making decisions: either by usingMature drug modalities (e.g., small molecules, monoclonal antibodies)Developing new targets, either by usingEmerging Drug Modalities (e.g., Antibody-Drug Conjugates, Cell Therapies)Develop validated targets.

This study was conducted byJack Cuthbertson, Sakis Paliouras, and Tatiana KolesnikovaCompleted by three authors, based onGlobalData’s Drug Sales and Consensus Forecast Database and Drug R&D Pipeline Database, systematically analyzes oncology drugs approved since 2011 and candidate drugs currently in the R&D pipeline.

The study will define first-in-class molecules as those whose targets areOncology Indicationsmolecules for which no drugs have yet been approved (or were not approved at the time), with detailed categorical statistics by stage of drug development (preclinical, Phase I, Phase II, Phase III, pre-registration, and approved) and by drug modality (small molecules, monoclonal antibodies, antibody–drug conjugates, cell therapies, etc.). This analysis provides comprehensive and objective data support for understanding current trends in target innovation in oncology drug development.

The commercial advantages of first-in-class drugs are particularly evident in market data. In 2024, despite first-in-class drugsAccounts for onlyof the total number of marketed oncology drugs31%, but its global sales reached119 billionUSD, accounting for the revenue of the entire oncology drug market41%. This means that the average market performance of each first-in-class drugsignificantly superior toFollowing the drug, its unit doseHigher Revenue Contribution. This disproportionate commercial success stems fromFirst-in-Class DrugIt typically meets unmet clinical needs, secures approval for broader indications, and establishes stronger brand recognition and physician prescribing habits in the market.

However, there is a clear inverse relationship between target novelty and the stage of drug development. In the preclinical stage,First-in-Class Oncology Drugaccounted for the highest proportion, reaching57%, demonstrating a strong focus on innovative targets in early-stage R&D. This proportion begins to decline upon entry into the clinical trial phase:First-in-class drugs accounted for 48% in Phase I clinical trials and 49% in Phase II.The two are basically on par.

But byDuring the pivotal Phase III clinical trial stage, the proportion of first-in-class drugs plummeted to 34%.and further declines to 25% in the pre-registration phase. This stepwise decrease reflects the higher risk of failure faced by new-target drugs in late-stage clinical development—due to the lack of preclinically validated biological mechanisms and safety data, drugs targeting novel targets are more prone toPhase II and Phase IIIDevelopment was terminated in the trial due to insufficient efficacy or safety concerns.

Different drug modalities exhibit significant differences in target novelty. Among approved drugs, the proportion of first-in-class drugs ranges from 10% to 70% across different modalities. For the two most mature modalities—Small Molecule Drugs and Antibody Therapeutics(excluding antibody-drug conjugates, ADC)—26% and 32% of approved drugs belong to the first-in-class category, respectively.

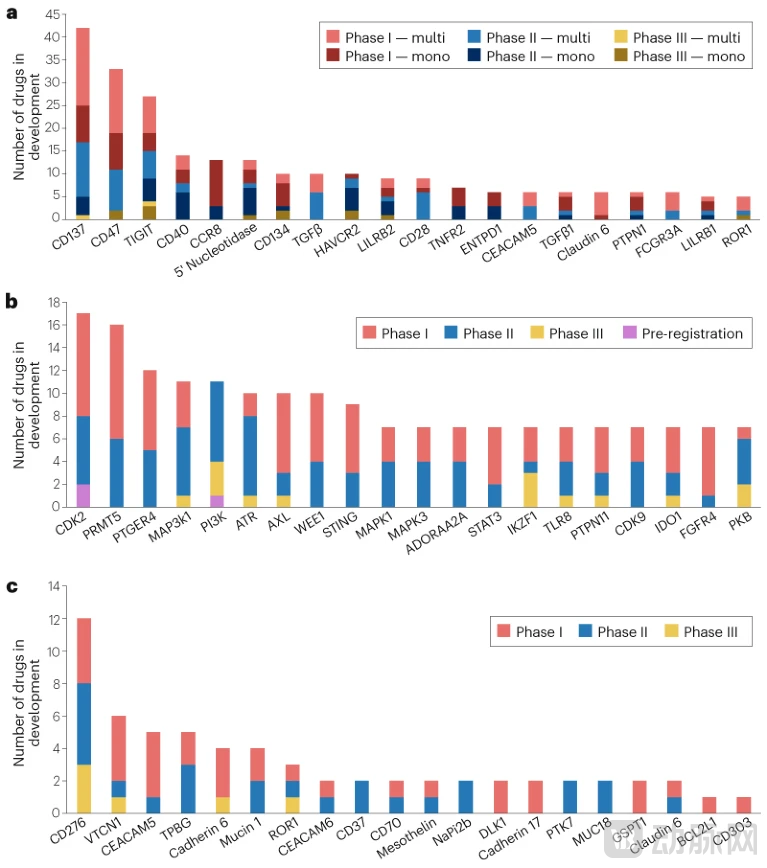

Figure: Popular Novel Oncology Targets for Major Treatment Modalities

(Source: Nature Reviews Drug Discovery)

At the two extremes areGenetically Modified Cell Therapy and Fusion Proteins:Only 10% of approved genetically modified cell therapies target novel indications, whereas up to 70% of approved fusion proteins are first-in-class drugs. In the R&D pipeline, including candidates in preclinical development, the proportion of novel targets across different modalities ranges from approximately 40% to 60%.

Notably, among candidate drugs in only two modalities—antibody-drug conjugates (ADCs) and genetically modified cell therapies—did the proportion developed against mature targets exceed that against novel targets.

The tendency of ADCs to target mature antigens is driven by strategic considerations. Developers typically choose to focus on already successfulMonoclonal Antibody (mAb)Building ADCs on the basis of established therapies and developing next-generation blockbusters by optimizing other components (such as the toxic payload) is a proven strategy. For example, targetingAntibody-drug conjugate (ADC) drugs targeting human epidermal growth factor receptor 2 (HER2): trastuzumab emtansine (brand name Kadcyla) and trastuzumab deruxtecan (brand name Enhertu)Building on the success of the groundbreaking monoclonal antibody trastuzumab (brand name Herceptin), treatment outcomes for patients with metastatic HER2-positive breast cancer have been further improved.

Competition for new targets began even before the approval of the first batch of drugs. The distribution of drug candidates developed against different novel targets is highly uneven, exhibiting a "clustering" phenomenon. Among antibody-based therapeutics, the most popular new target isCD137 (also known as 4-1BB), a co-stimulatory molecule expressed on the surface of activated immune cells. Currently, there are 42 antibody-based candidate drugs in Phase I to III clinical development, including 12 monoclonal antibodies and 30 multispecific antibodies (bispecific, trispecific, and tetraspecific molecules).

Bispecific AntibodyThe development has made it possible to jointly target two pathways, such as amivantamab, which simultaneously inhibits the Epidermal Growth Factor Receptor (EGFR) and MET, or talquetamab, a GPRC5D × CD3 bispecific antibody that brings tumor cells and T cells together.

For small-molecule drugs, the hottest new targets areCyclin-Dependent Kinase 2 (CDK2), there are 17 candidate drugs in the clinical pipeline. This reflects industry expectations that CDK2 inhibition may target solid tumors with CCNE1 gene amplification and address resistance to CDK4/6 inhibitors in breast cancer—a class for which three blockbuster drugs are currently on the market.

Although some new targets have candidate drugs in Phase III development and early candidates have failed in later-stage trials, they still attract a large number of Phase I candidates. For example, there are 22 candidate drugs targeting the innate immune checkpoint protein CD47 in Phase I trials; although more than half are novel bispecific antibodies, they may be more successful than their monoclonal antibody predecessors. Compared with other modalities, the number of antibody-drug conjugates (ADCs) developed against new targets is much smaller, reflecting the aforementioned strategy of developing ADCs against targets with existing monoclonal antibody drugs, such as HER2.

The main exception is forADC Development Targeting the Immune Checkpoint CD276 (Also Known as B7-H3)Currently, there are 12 candidate drugs, three of which are in Phase III trials. Although previous monoclonal antibodies targeting CD276 have failed, the therapeutic potential of this target in underserved patient populations with small cell lung cancer and other solid tumors has driven the development of these ADCs.

Although first-in-class drugs generate disproportionate revenue, the development of second- and third-in-class drugs still holds considerable commercial potential.Large Indication MarketsIt indeed supports the coexistence of multiple blockbuster drugs, providing ample room for follow-on strategies.

Some companies are also leveraging established targets through novel approaches, either by adopting new drug modalities to address these targets or by enhancing clinical efficacy or safety while using the same modality.Epidermal Growth Factor Receptor (EGFR)The development history of inhibitors is a typical case. AstraZeneca'sPioneering EGFR inhibitor gefitinib (trade name: Iressa)It was not commercially successful, with peak sales reaching only $400 million. Subsequently, Roche developedSecond-generation EGFR inhibitor erlotinib (trade name Tarceva)with peak sales exceeding $1.5 billion. AstraZeneca subsequently launched the third-generation EGFR inhibitor osimertinib (brand name Tagrisso), which has achieved global sales of over $6 billion. This case clearly demonstrates that even if a drug is not first-in-class, later entrants can still achieve greater market success through technological improvements and clinical optimization.

However, the race to develop first-in-class drugs can also lead to a string of failed investments. The collective failure of TIGIT inhibitors is a recent典型案例. In early 2025, there were5 TIGIT Inhibitor AssetsPhase III trials were conducted across multiple cancer indications, but all subsequently failed. Given the enormous costs associated with the clinical development of oncology drugs, these programs likely incurred expenditures in the billions of dollars.

This concentration of development efforts on a small number of high-priority new targets has resulted in substantial R&D capital investment with minimal returns, rather than being allocated to a broader portfolio of innovative, high-risk, high-reward projects. The contradiction between such resource concentration and the need for diversified innovation has become a critical issue that the industry must address.

Looking Ahead,Bispecific AntibodyThis may offer a new approach to balancing innovation and risk. By combining a well-established target with a novel one, bispecific antibodies can explore new therapeutic possibilities while leveraging validated mechanisms.

Moreover, developing previously failed targets using novel drug modalities has also shown promise.CD276The case of transitioning from monoclonal antibody failure to ADC resurgence demonstrates the feasibility of this strategy. However, what the industry needs more isOptimization of Resource Allocation——Rather than concentrating all capital on a few popular targets, investment should be diversified across a broader portfolio of high-risk projects with innovative potential. Only in this way can we truly drive sustained progress in oncology therapeutics, rather than falling into the trap of collective failure amid homogeneous competition.

For the pharmaceutical industry, these data reveal aKey Takeaways: AtStriking the Right Balance Between Pursuing Innovation and Managing RiskCrucial. While first-in-class drugs can yield higher returns, their development carries greater risks, requiring a more robust scientific foundation and more substantial financial support.

The follow-on strategy is not devoid of innovation; rather, it achieves this throughAchieving Business Value Through Incremental Improvement and Differentiated Competition, which is also a feasible and effective approach in large indication markets. The real challenge lies in how to avoid resource waste caused by blind bandwagoning, and how toAllocate R&D Investment Rationally Between Hot Targets and Innovative Exploration, and how toUnlocking New Value of Known Targets Through Novel Models and Combinations.

Although first-in-class drugs have delivered significant commercial returns, their development path is fraught with challenges.The high failure rate has led to a significant decline in the proportion of first-in-class drugs in late-stage clinical trials.Meanwhile, follow-on strategies can also achieve significant success through technological improvements and clinical optimization, as fully demonstrated by the three-generation evolution of EGFR inhibitors.

Industry NeedsBalancing the Enthusiasm for Chasing New Targets with Rational Risk Managementstrike a balance, avoiding the overconcentration of resources on a few popular targets, which could lead to collective failures such as those seen with TIGIT inhibitors. In the future, throughBispecific AntibodyIntegrating mature targets with innovative ones through new technologies, along with strategies to redevelop failed targets using novel approaches, may provide the industry with more diversified pathways for innovation. Rational resource allocation and differentiated competitive strategies will be key to driving continuous progress in cancer treatment.