127 Healthcare Companies in IPO Pipeline: Is 2026 Set to Be a Banner Year for Medical Listings?

In 2025, the long-silent medical IPO market finally ushered in a long-awaited surge of activity.A total of 37 medical companies went public throughout the year, a figure twice as high as that in 2024.。

Figure 1. Eight medical companies listed in 2026 (data as of the end of February)

Figure 1. Eight medical companies listed in 2026 (data as of the end of February)

As we enter 2026, this fervor continues to persist.In just the first two months of the year, eight companies in China’s healthcare sector have successfully gone public., namely Ribobio, Kingmed Medical, and Zhuozheng Medical listed on the Hong Kong Stock Exchange; Aishelun, Aide Technology, and Haisheng Medical listed on the Beijing Stock Exchange; Northcore Life Sciences listed on the STAR Market; and Newbridge Biologics, which successfully went public. Notably, all eight healthcare companies saw significant gains on their first day of trading, with an average increase of over 100%, demonstrating the capital market’s continued optimism and strong confidence in the healthcare innovation sector.

Beyond the public listing arena, the queue of healthcare companies awaiting regulatory review is unprecedented in scale. It is reported that,In January 2026, 31 healthcare companies filed or updated their prospectuses, reaching a staggering average of one per day and breaking the single-month record set during the peak of the 2021 bull market.. But this is just the tip of the iceberg; according to incomplete statistics from VCBeat,As of February 2026, a total of 127 healthcare companies are queued for listing on the Hong Kong and A-share markets, hitting a record high.。

Does this mean that a wave of IPOs focused on the healthcare sector is imminent in 2026?

Profile of Companies in the IPO Queue: Half Struggling for Survival, Half Scaling Up

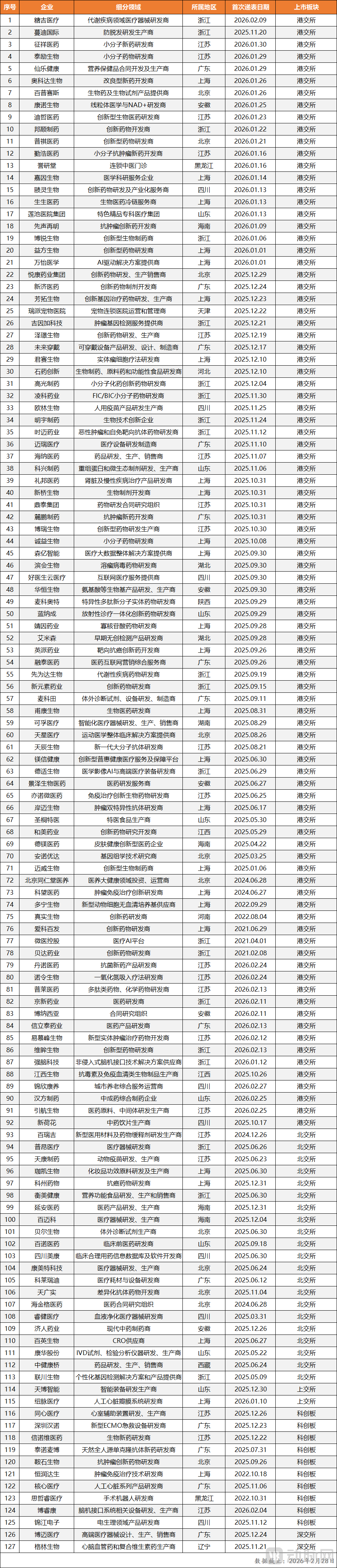

It is reported that among the 127 medical companies awaiting IPO review, 92 are listed on the Hong Kong Stock Exchange, while a total of 35 are listed on mainland China’s A-share market, distributed across the Beijing Stock Exchange, Shanghai Stock Exchange, Shenzhen Stock Exchange, and the STAR Market.

Figure 2. Distribution of 127 Queuing Companies by Sub-sector

Figure 2. Distribution of 127 Queuing Companies by Sub-sector

Drilling down further into specific sub-sectors, among the 127 companies, 83 are pharmaceutical firms, with innovative drug companies accounting for as high as 80% of this group. There are 28 medical device companies, primarily distributed across sub-segments such as in vitro diagnostics (IVD), interventional medicine, medical imaging, brain-computer interfaces, and consumables. The remaining 16 companies are spread across four major fields: artificial intelligence (AI), internet healthcare, consumer healthcare, and foods for special medical purposes (FSMP) and nutritional supplements.

Different stock market choices and different niche sectors naturally entail vastly different IPO valuation logics and capital narratives. In this regard, VCBeat has categorized them into three groups:

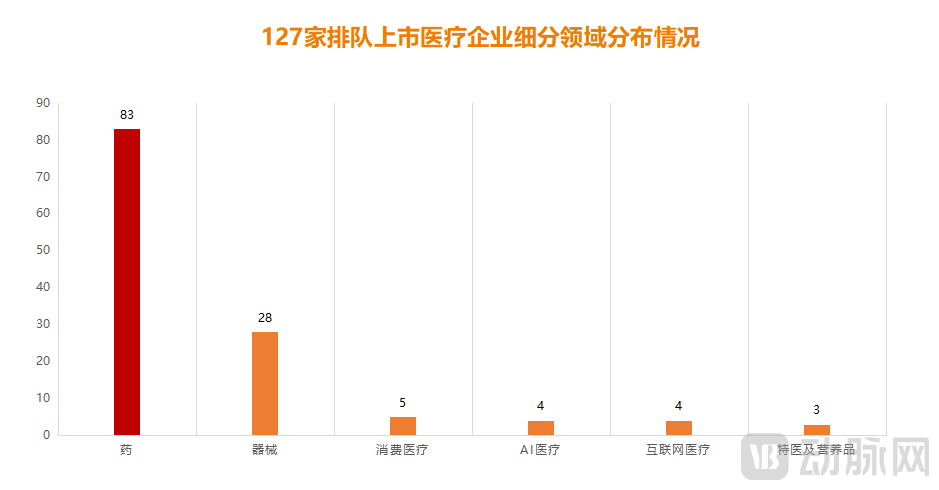

First is the “Survivalist Camp”, this is the largest group. Their business models have not yet been fully proven or have encountered phased obstacles, and they generally need to go public to obtain cash flow for survival.. According to statistics from VCBeat, among the 127 healthcare companies currently queuing for IPOs, 69 are still operating at a loss. The majority of these are innovative drug developers that lack mature commercialized products; however, their substantial R&D expenditures have severely strained their cash flows, with some companies holding insufficient cash reserves to ensure stable operations through the remainder of this year.

Figure 3. Proportion of Net Losses Among 127 Healthcare Companies Queuing for IPO

Figure 3. Proportion of Net Losses Among 127 Healthcare Companies Queuing for IPO

This phenomenon is commonplace in the Hong Kong stock market, where the introduction of the “Chapter 18A” listing regime has provided a fertile ground for a cohort of pre-profit biopharmaceutical companies to go public.This has also resulted in 56 of the 92 healthcare companies currently awaiting approval for listing on the Hong Kong Stock Exchange being in a loss-making position., the vast majority of them are innovative drug companies with no revenue but annual R&D expenses exceeding RMB 100 million. For instance, Taili Bio, which filed its IPO application earlier this year, focuses on innovative oncology therapies. Its most advanced core pipeline is currently only in Phase II clinical trials, meaning it will take at least another 3–5 years before approval and market launch. However, its R&D spending is growing rapidly, leading to an expanding net loss that reached RMB 123 million in the first three quarters of 2025. Therefore, going public is not merely a matter of development for the company, but a life-or-death struggle for survival.

In fact,“Survivalists” face not only cash flow pressures but also challenges stemming from valuation adjustment mechanisms (VAMs).It is reported that during the capital winter of 2023–2024, many healthcare companies, in order to survive, had no choice but to sign stringent “redemption right” agreements when raising funds, commonly known as “valuation adjustment mechanisms” (VAMs). Take Simcere Zaiming as an example; a subsidiary spun off from Simcere Pharmaceutical, it completed a RMB 970 million Series A financing round in 2024. While this brought valuable cash flow, it also entailed signing a VAM clause—If Simcere Pharmaceuticals fails to achieve its IPO target by the end of 2028, investors shall have the right to require the company to repurchase their shares in accordance with the valuation adjustment mechanism (VAM) agreement, at a repurchase price equal to the principal plus annualized interest at a rate of 7%.. Thus, under the pressure of valuation adjustment mechanisms and hefty interest payments, Simcere Pharmaceutical had no choice but to accelerate its push for an initial public offering.

According to statistics from VCBeat, among the 127 healthcare companies currently queued for initial public offerings (IPOs), more than 40% have filed multiple applications, with 15 companies having applied three times or more. In addition, a significant number have switched listing venues; for instance, as many as 16 companies have moved from China’s A-share market to the Hong Kong Stock Exchange. Furthermore, some companies have experienced considerably prolonged IPO timelines, with many waiting up to five years since their initial filing. Although these paths have been fraught with challenges, for the “survival-oriented” firms,Going Public Is the “Pledge of Allegiance” for Sustaining Corporate Survival。

Next is the “Scale-Up and Strengthen” faction. Unlike those focused on survival, they pursue IPOs primarily to expand their business operations or to leverage capital markets to reinforce their competitive moats.Taking global expansion as an example, this is a critical pathway for many healthcare companies seeking new growth curves. The Hong Kong stock market serves as an ideal springboard for this purpose; its substantial capital reserves and capabilities in international capital operations not only support medical device companies in completing overseas registrations and building sales networks but also bridge key business development (BD) transactions for innovative pharmaceutical companies in overseas markets.

The most closely watched IPO of 2025 was undoubtedly Hengrui Medicine’s secondary listing on the Hong Kong Stock Exchange. As China’s leading innovator in pharmaceuticals, its strategic move to list in Hong Kong holds significant representative value. In its prospectus, Hengrui Medicine clearly stated that the funds raised from the Hong Kong offering would be allocated to several key areas, with the construction of a North American clinical trial base being a crucial component. By establishing a presence in North America, Hengrui Medicine aims to integrate more deeply into the global pharmaceutical R&D ecosystem, gain access to cutting-edge scientific resources and clinical data, accelerate the development of innovative drugs, and enhance the competitiveness of its products in international markets. In short, the Hong Kong listing marks a historic leap for Hengrui Medicine, transforming it from “Hengrui China” into “Global Hengrui.”

Among the 127 companies currently in the IPO queue, there is a similar case: Mindray Medical. In 2018, Mindray Medical successfully listed on the Shenzhen Stock Exchange, becoming the first medical device company on the ChiNext board to achieve a market capitalization exceeding RMB 100 billion. In November 2025, Mindray officially launched its bid for a listing on the Hong Kong Stock Exchange. In response to investor inquiries, the company stated that the Hong Kong listing would significantly promote the strategic synergy between its “business globalization” and “capital globalization.” According to statistics from VCBeat, there are currently 17 A-share listed companies seeking H-share listings. Their objective is clear: to leverage the international capital platform and endorsement capabilities of the Hong Kong stock market to achieve dual breakthroughs in financing diversification and global strategy.

The final category is “the ‘desperate-to-go-public’ camp.”, they are essentially star enterprises in their respective fields and embarked on their IPO journeys early on. However, for various reasons, they have yet to achieve their goals. Nevertheless, they have not given up; some have made three or even four attempts to go public, while others have shifted their listings to multiple exchanges. The reason behind such “desperate” efforts isThis is because going public is not only the culmination of demonstrating regulatory compliance in its operations, but also the starting point for validating its new business model.. For them, as long as they remain at the table, there is still an opportunity to turn the tide against the odds.

IPO Logic Shifts: “Old Maps” Can’t Find “New Continents”!

In 2026, both the Hong Kong stock market and the A-share market are sending positive signals, with a significant acceleration in review efficiency. This is not mere rumor; at a recent meeting of the Finance Committee of the Legislative Council, Mr. Paul Chan, Financial Secretary of the Hong Kong Special Administrative Region Government, explicitly stated that to efficiently align with market demands, the Hong Kong Exchanges and Clearing Limited (HKEX) and the Securities and Futures Commission (SFC) are working overtime to expedite the processing of IPO applications, striving to facilitate the successful listing of more high-quality enterprises on the Hong Kong stock market.

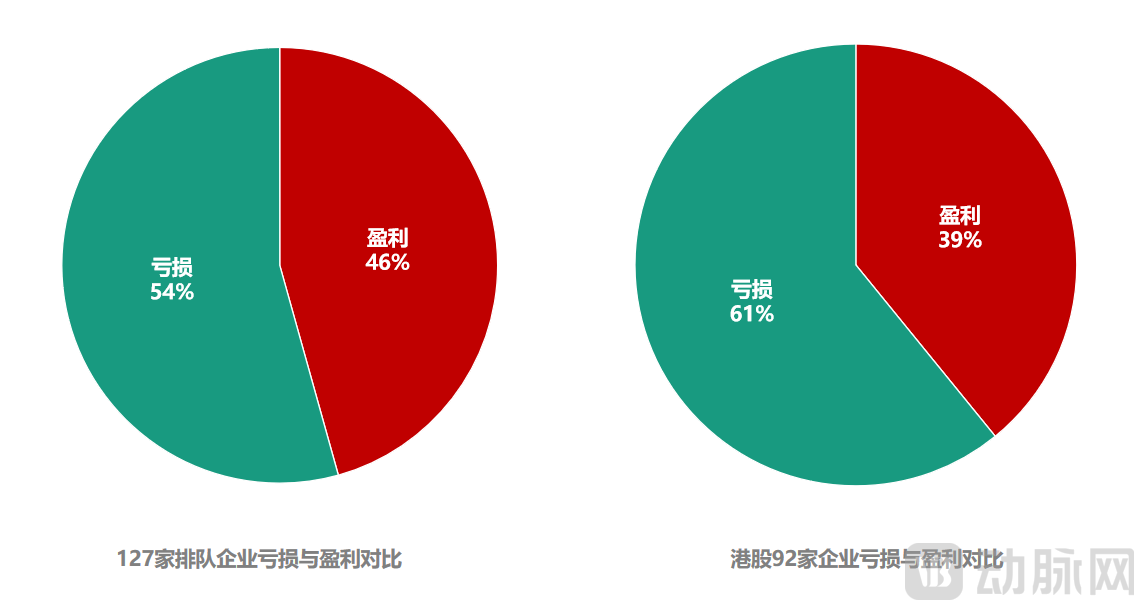

Figure 4. Number of IPOs in China’s Healthcare Sector, 2021–2025

Figure 4. Number of IPOs in China’s Healthcare Sector, 2021–2025

The same holds true for China’s A-share market. Since the relaunch of the fifth set of listing criteria on the STAR Market in June 2025, the average processing time from application acceptance to approval has been significantly shortened across the three major exchanges—Shanghai, Shenzhen, and Beijing. Taking Hygen Biopharma, which went public last year, as an example,It took only 14 days from the submission of the registration application to the approval of the IPO, setting the fastest record since the implementation of the registration-based system reform.By 2026, the review efficiency continues to accelerate; in just the first two months of the year, four healthcare companies have already gone public on the A-share market, a figure that represents half of the total for the entire year of 2025.

Therefore, for the 127 healthcare companies currently in the IPO queue, 2026 is undoubtedly an opportunity. Many industry experts are optimistic about this, believing that 2026 may become a “banner year” for healthcare IPOs. However, whether a company can ultimately go public depends on its own “core competitiveness.” As the industry gradually shifts from conceptual hype to value creation, the secondary market’s definition of “core competitiveness” is undergoing a profound transformation.

Specifically,First, it is essential to possess absolute core competitiveness, which can manifest as technological leadership in a niche sector, a unique business model, or breakthrough therapies that address unmet clinical needs.。

Taking brain-computer interfaces (BCIs) as an example, at the beginning of 2026, BrainCo and NeuroXess successively launched IPO bids on the Hong Kong Stock Exchange and the STAR Market, respectively. Although neither company has achieved full profitability and their commercialization processes still have some way to go, the capital market remains highly confident in their prospects. On one hand, BCIs possess high technical barriers and scarcity, with clear and rigid demand across multiple clinical scenarios. Coupled with their alignment with national strategic priorities, they hold immense future commercial potential. On the other hand, both BCI companies are leaders in their respective fields. Taking BrainCo as an example, it has established an independent technological system covering the entire chain of non-invasive BCIs and has been the first to deploy its technology into multiple medical-grade solutions, demonstrating strong industrialization capabilities and first-mover advantage in the market.

Some unprofitable innovative pharmaceutical companies also exhibit these distinct characteristics. Taking Tainuomaibo as an example, it is a typical “zero-revenue” innovative drug company. According to its prospectus, its cumulative losses from 2022 to 2024 reached RMB 1.39 billion. Nevertheless, Tainuomaibo’s path to an initial public offering (IPO) remains promising. On one hand, as a star enterprise, it has raised over RMB 2 billion in financing since its establishment ten years ago, with nearly thirty well-known institutions and industry players among its shareholders. On the other hand, its pipeline quality is highly robust. Its first drug, Stedutamab Injection, has already been approved for marketing. This is a global first-in-class innovative drug for tetanus prevention, with a future market size expected to exceed RMB 1 billion, which will significantly enhance the company’s profitability.

Second, there must be certainty, including specific timelines for product launch, clear commercialization progress, a schedule for achieving profitability, and the ability to deliver on business development (BD) or overseas partnerships. These are key indicators determining whether a company can successfully go public.。

By analyzing the 37 healthcare companies that successfully went public in 2025, we have identified several common characteristics: their pipelines are generally in the mid-to-late stages; core products are nearing or have already achieved commercialization; there is a significant increase in out-licensing deals; cash flow has improved markedly; and revenue has surged substantially or the companies have already turned profitable.

In this regard, a seasoned investor remarked, “Having experienced the bubble and reshuffling of the past two years, investors have become increasingly mature, and correspondingly, their requirements for IPO projects are now higher,”Capital will increasingly flow to healthcare companies with proven or high-potential overseas business development (BD) track records, as well as clear product launch timelines and sales forecasts.. Conversely, companies lacking such certainty will face significant pressure in their IPO processes, and their valuations will encounter certain challenges.”

Thus, among the 127 healthcare companies currently in the IPO queue, we have observed numerous instances of such “certainty.” For example, regarding pipeline progress, Danuo Medicine’s core product, lifortinidazole (TNP-2198), had its marketing authorization application accepted in August 2025 and is poised for imminent approval. Additionally, in terms of business development (BD), companies including Chengyi Biopharma, Jingyin Pharmaceutical, Mabwell Biosciences, and CSPC Innovation completed multiple significant transactions in 2025. Finally, at the performance level, Lupeng Pharmaceuticals, Medcaptain, and Duoning Biology all achieved their first turnaround from loss to profit in 2025, thereby strengthening their prospects for going public.

The third point is compliance, meaning that all aspects—including finance, legal affairs, clinical operations, and corporate governance—must withstand rigorous scrutiny.。

Recently, the Hong Kong Securities and Futures Commission (SFC) and the Hong Kong Exchanges and Clearing Limited (HKEX) jointly sent a letter to IPO sponsors, expressing concern over the decline in quality of some recent new listing applications and non-compliant behaviors. They emphasized that while encouraging applications, it is essential to strictly uphold quality standards. This move effectively sends a clear signal of tightening regulatory oversight, indicating that HKEX’s compliance review of companies seeking listings will enter a more rigorous and refined phase.

This is highly necessary. In this regard, a representative from the HKEX’s Biotech Listing Advisory Group stated, “For healthcare companies,Compliance is not merely a threshold for “passing review,” but the cornerstone of a company’s long-term value and its credibility in the capital markets.—Any financial irregularities, legal loopholes, and governance deficiencies are likely to be subjected to heightened scrutiny during the IPO process, potentially even becoming latent risks for post-listing stock price volatility or delisting crises. Therefore,Emphasizing compliance is, in essence, underscoring the sustainable development capacity of healthcare enterprises; only in this way can they truly earn regulatory trust and investor confidence.。”

Taking Xuanzhu Biopharma, which successfully went public in 2025, as an example, the company proactively disclosed the origins of its core technologies and detailed breakdowns of R&D expenditure accounting to substantiate the authenticity of its R&D capabilities. It also confirmed that its technical personnel had no non-compete disputes or intellectual property infringement issues with their former employers. Another representative case is Jiahemeikang, a healthcare informatics enterprise. During its IPO review process, it obtained the Level 3 Certification for Classified Protection of Cybersecurity and provided detailed explanations during regulatory inquiries on how data anonymization was implemented, clearly defining access controls for data collection, usage, and circulation.

Overall,The current IPO market is seeking a more sustainable balance between “quantitative growth” and “qualitative improvement.”On the one hand, the multi-tiered capital market has provided healthcare enterprises with more diversified listing options, driving continuous expansion in industry financing scale; on the other hand, stock exchanges are placing greater emphasis on enhancing the intrinsic value of listed companies, imposing higher requirements on R&D innovation capabilities, commercialization prospects, and compliance governance standards.

In this regard, a senior investor remarked, “Currently,The listing logic for the healthcare industry has quietly shifted, accelerating from a past focus on “scale expansion and pipeline volume” toward “commercialization capability, earnings visibility, and differentiated innovation.” Capital markets are now placing greater emphasis on companies’ self-sustaining revenue generation and the clinical value of their core products, rather than merely their R&D stage or conceptual narratives.。”

Going public is not the goal, nor is it by any means the only one.

In stark contrast to the flood of healthcare companies going public, few have successfully crossed the profitability threshold.

It is reported that in 2025, only two Chapter 18A biotech companies successfully removed the “B” marker from their stock tickers. The vast majority remain trapped in the predicament where their listing marked their peak performance. Hampered by homogeneous drug pipelines, pricing pressures, and macroeconomic volatility, these companies have been unable to escape sustained losses and are now facing existential crises after exhausting their financing. According to VCBeat, numerous healthcare companies have recently faced rumors or announcements of delisting, bankruptcy reorganization, sales of core assets, or privatization, accelerating an industry reshuffle focused on the secondary market.

This indicates that,Going public is not the finish line, but rather the starting point for enduring the rigorous scrutiny of the public market. A successful IPO merely signifies a phase of achievement and provides substantial capital support; however, the critical test determining whether these healthcare companies can weather economic cycles and achieve sustainable development lies in their ability to effectively translate R&D investments into commercial outcomes.。

Certainly, in the context of diversified industry development, going public is not the only path for healthcare companies to achieve sustainable growth or realize a leap in value.Business development (BD), mergers and acquisitions, overseas market expansion, or focusing on niche segments as “hidden champions” are all models that can help companies build long-term competitiveness.。

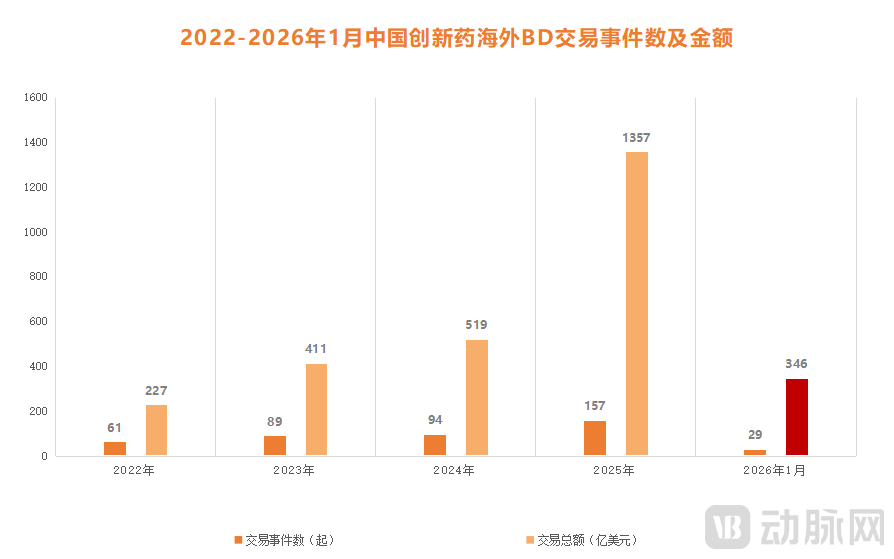

Figure 5. Number and Value of Overseas Business Development (BD) Transactions for Chinese Innovative Drugs, January 2022–2026

Figure 5. Number and Value of Overseas Business Development (BD) Transactions for Chinese Innovative Drugs, January 2022–2026

Specifically, for innovative drug companies, overseas business development (BD) transactions are currently booming. According to data from VBInsight, the total value of BD deals involving Chinese innovative drugs reached $34.6 billion in just the first month of 2026, representing a year-on-year increase of approximately 55%. Therefore, if innovative drug companies can seize these opportunities, they can not only improve their cash flow through upfront and milestone payments but also lay the foundation for subsequent independent global expansion or financing at higher valuations.

For medical device companies, there are numerous pathways to pursue high-quality development. One approach is through mergers and acquisitions (M&A). According to data released by Haoyue Capital, the value of domestic M&A transactions in China’s medical device sector increased by 45% year-on-year in 2025. Furthermore, private equity (PE) and venture capital (VC) firms accounted for 67% of the number of domestic M&A deals in the first half of 2025, nearly twice the proportion attributable to strategic investors. Another avenue is the global expansion of Chinese-made medical devices, which is yielding substantial returns. Data from the China Chamber of Commerce for Import and Export of Medicines and Health Products shows that China’s medical device exports reached $24.1 billion in the first half of 2025, representing a 70% increase compared to the same period in 2019. A significant portion of these exports consists of high-end, sophisticated medical devices.

Therefore, in the face of the current wave of healthcare IPOs, we must adopt a rational perspective: while acknowledging the catalytic role of capital markets in driving medical innovation, we must also remain vigilant against valuation bubbles fueled by capital, homogeneous competition, and the subsequent tests of corporate profitability. As the industry gradually returns to value creation,The “IPO-driven” motive is waning, but the market’s role as a litmus test is becoming more prominent, truly filtering out high-quality healthcare companies that possess core technological barriers, sustainable business models, and long-term value creation capabilities.。

1. “Behind the Surge in 2025 Hong Kong Stock Exchange Biopharmaceutical IPOs: How Are Biotechs Transitioning from an ‘IPO Fever’ to a ‘Battle for Survival’?” — China Times;

2. “A-Share IPO Review Accelerates, with Multiple Companies’ Queue Times Under Six Months” — 21st Century Business Herald;

3. “31 Healthcare Star Companies Race for HKEX Listings, Igniting Life-or-Death IPO Battles!” — MedLine Insight;

4. “2026 Healthcare Outlook: A Hundred Companies Queue for HKEX Listings—Can the Healthcare Sector Create Another ‘Miracle’?” — 36Kr

Appendix: Current Status of the 127 Medical Companies in the Queue: