Innovent Biologics 2025 Results: RMB 13 Billion Revenue and First-Ever Profitability, Marking the Transition from Biotech to Biopharma

Innovent

High-end Biologics Developer

Introduction: The “Landing” Moment for China’s Innovative Drugs

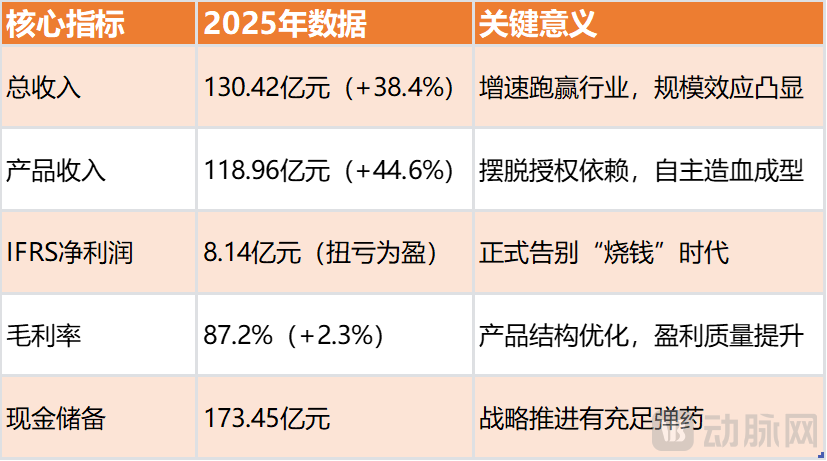

In 2025, China’s innovative drug sector has long moved past the era of “burning cash for valuation” and its associated wild growth. Layoffs, pipeline cuts, and a cooling financing environment have become the industry norm. Against this backdrop, Innovent Bio (01801.HK) released its annual results like a thunderclap, cutting through the fog surrounding Biotech transformations: total revenue reached RMB 13.042 billion, a year-on-year increase of 38.4%; product revenue surpassed RMB 11.896 billion, crossing the RMB 10 billion threshold for the first time; and net profit under IFRS amounted to RMB 814 million, ending years of persistent losses.

This is no ordinary financial report; it is proof that a leading Chinese biotech company has successfully navigated its “trial by fire” to reach solid ground. In just ten years, Innovent Bio has completed a journey many peers are still struggling with, transforming from an R&D-focused company reliant on financing for survival into a mature pharmaceutical enterprise capable of self-sustaining revenue generation. Its 2025 performance holds the key to understanding China’s innovative drug sector as it shifts from “quantitative accumulation” to a “qualitative leap,” and answers a core question: What is the ultimate endgame for biotech companies?

I. Profitability Is Not Accidental

Many attribute Innovent Bio’s profitability in 2025 to “good luck”—with new chronic disease products catching the market wave and oncology products achieving steady volume growth. However, looking beyond the surface of the financial statements reveals that this profitability is the inevitable outcome of long-term strategic planning, as well as a corrective response to the industry’s common pitfalls of “blind R&D” and “prioritizing fundraising over commercialization.”

In 2025, of Innovent Bio’s total revenue of RMB 13.042 billion, RMB 11.896 billion came from product sales, accounting for a significant 91.2% and representing a year-on-year growth of 44.6%, far exceeding the overall revenue growth rate. Behind these figures lies Innovent’s complete departure from reliance on “licensing fees”—the days of earning upfront payments and milestone payments by licensing its pipeline to overseas pharmaceutical companies have finally become a thing of the past.

Compared with 2024, the proportion of product revenue increased by 3.8 percentage points, while licensing fee revenue amounted to only RMB 957 million. Although stable, it has declined from a “core revenue source” to a “supplementary item.” This signifies that Innovent Bio has truly achieved a closed loop of “R&D–manufacturing–sales,” capturing market share and generating profits through its own products rather than relying on capital infusions or licensing deals for survival—this is the fundamental distinction between a Biopharma and a Biotech.

An IFRS net profit of RMB 814 million, seemingly a one-time breakthrough from loss to profitability, is in fact the cumulative effect of three key initiatives, with no element of luck involved.

First, the realization of economies of scale. After product revenue surpassed RMB 10 billion, sales, administrative, and production costs were significantly diluted—the same sales team could cover more products, and increased capacity utilization at the same production bases directly reduced unit costs. Second, optimization of the product mix: the revenue share of high-margin GLP-1 chronic disease medications (such as Xinermi) and core innovative oncology drugs increased, driving the overall gross margin up from 84.9% in 2024 to 87.2% in 2025, a year-on-year increase of 2.3 percentage points. Finally, disciplined expense control—sales, administrative, and R&D expense ratios were optimized in tandem, avoiding blind expansion of expense scales despite revenue growth. This diluted unit costs and improved operational efficiency, ultimately resulting in a 419.6% surge in core business performance (Non-IFRS net profit).

More critically, the Non-IFRS net profit reached RMB 1.723 billion, a year-on-year surge of 419.6%. This metric, which excludes one-time gains and losses, truly reflects the core business’s cash-generating capability of Innovent Bio: its profitability stems not from incidental investment income or government subsidies, but from strong product sales and stable cost control.

In 2025, Innovent Bio’s R&D expenditure amounted to RMB 2.624 billion, representing a slight year-on-year decrease of 2.1%, while its R&D expense ratio declined from 28.4% in 2024 to 20.1%. This stands out as somewhat “atypical” within an industry context that often equates higher R&D investment with greater excellence, yet it precisely reflects Innovent’s clear-headed strategic approach.

Rather than following the trend of overcrowding its pipeline with popular targets, it has focused its capital on late-stage clinical development and high-potential global assets—such as IBI363 and IBI343, which have entered Phase III trials and hold promise as “blockbuster” drugs—thereby avoiding scattered, indiscriminate investment. This approach of “precision R&D” delivers greater value than merely inflating R&D expenditures.

Its robust cash reserves further bolster its confidence: RMB 17.345 billion, a substantial increase from 2024. Coupled with its first-ever positive operating cash flow, this means Innovent Bio no longer needs to rely on financing for survival. These funds serve as “ammunition” for advancing global clinical trials and expanding commercialization, as well as a “safety cushion” against industry volatility. In 2025, when financing markets cooled, this cash reserve became its greatest competitive advantage.

Overview of Key Data from Innovent Bio’s 2025 Annual Report

II. Oncology Holds the Line, Chronic Diseases Break Through

Innovent Bio’s profitability hinges on a “two-pronged” strategy: solidifying its core oncology business while unlocking new growth opportunities in chronic diseases. This is not some lofty, high-minded strategy, but rather the most pragmatic approach to survival amid intense industry competition. Many biotech firms have stumbled by betting on a single front—either focusing solely on oncology and getting exhausted in red-ocean competition, or blindly pivoting to chronic diseases without delivering tangible products. Innovent, however, has struck the right balance, identifying a new growth engine just as oncology growth began to lose momentum.

Oncology is Innovent Bio’s “foundational capital” and the bedrock that enabled it to weather the industry’s downturn. By the end of 2025, its portfolio included 13 marketed oncology products covering high-incidence cancers such as lung, liver, and gastric cancers. This rich product lineup ranks among the top in China’s innovative pharmaceutical sector—constituting its competitive moat.

Tyvyt (sintilimab), as a leading domestic PD-1 inhibitor, has avoided the quagmire of "price wars" and instead maintained steady growth by continuously expanding into new indications and increasing market penetration. Small-molecule targeted drugs such as JiepaLi and DaBoLe, after being included in the National Reimbursement Drug List in 2025, rapidly penetrated grassroots markets, compensating for lower prices with higher volumes and contributing stable cash flow.

More critically, a robust product portfolio enables “combination therapy”—for instance, pairing Tyvyt with other targeted agents to achieve superior clinical outcomes. This makes hospitals and physicians more inclined to choose Innovent’s products, resulting in significantly higher customer stickiness compared to biotech firms with only a single product. It can be said that while the oncology business is not Innovent’s “growth engine,” it serves as its “ballast stone.” Securing this core foundation provides the confidence needed to strategically expand into chronic disease management.

If oncology represents Innovent Bio’s “defense,” then its chronic disease business constitutes the company’s “offense” in 2025 and serves as the key variable driving profitability. Prior to 2024, Innovent’s chronic disease pipeline was virtually empty; however, in 2025, the breakthrough success of three new products has propelled it to become a “dark horse” in the chronic disease sector.

Xin Er Mei (mazdutide) has been the biggest contributor—as the world’s first dual-target GCG/GLP-1 agent, it delivers both weight loss and glucose-lowering effects, rapidly becoming a “phenomenal product” after its launch. It is worth noting that 2025 marked the explosive growth phase of the GLP-1 sector; however, instead of following the trend to develop “me-too” products, Innovent Bio seized the first-mover advantage through differentiated targets, driving sales to soar.

Xinbile (tolerceptamab) and Xinbimin (teprotumumab) address the gaps in the chronic disease pipeline: the former is the first domestically produced PCSK9 inhibitor included in the National Reimbursement Drug List, rapidly penetrating the cardiovascular and cerebrovascular fields; the latter is the first innovative drug for thyroid eye disease in China in 70 years, establishing a solid foothold through differentiated competition. These three products are not merely “fillers”; rather, they precisely target market voids, with each generating substantial revenue.

By the end of 2025, 12 of Innovent Bio’s 18 marketed products had been included in the National Reimbursement Drug List (NRDL)—a testament to its mature commercialization capabilities. While many biotech firms develop promising products but struggle with commercial sales, Innovent’s thousand-strong sales team can swiftly navigate NRDL negotiations and hospital formulary access, effectively translating scientific achievements into tangible revenue. This constitutes its core competitive advantage over peers.

III. Greater Emphasis on Practical Implementation in R&D and Globalization

The core of innovative drug development is R&D, but not “slogan-driven R&D”; globalization is a trend, but not “blind overseas expansion.” Innovent Bio’s 2025 R&D and global strategy feature little flowery language, adhering to a single logic: pursue actionable, value-creating initiatives, avoid wasting a single penny, and refrain from ineffective deployments.

In 2025, Innovent Bio’s R&D pipeline shed many early-stage projects that merely served to pad the numbers, while adding numerous core assets with genuine potential to compete in the global market—this is the key to its improved R&D efficiency.

IBI363 is the most noteworthy candidate—a PD-1/IL-2α-biased bispecific antibody targeting the global challenge of PD-1 resistance. It is important to note that the current PD-1 market has become a highly competitive “red ocean,” with many pharmaceutical companies still developing “me-too” products. In contrast, Innovent Bio has directly entered the realm of “next-generation immunotherapy,” which boasts a potential market size exceeding $40 billion. In 2025, global Phase III clinical trials for this drug were initiated, marking leading progress worldwide. Once successfully launched, it will become Innovent’s “trump card” for globalization.

IBI343 (CLDN18.2 ADC) in the ADC field is equally impressive. Targeting gastrointestinal tumors such as gastric and pancreatic cancers, it has demonstrated excellent clinical data, with a potential market size exceeding $8 billion. The drug has entered global Phase III trials and partnered with Takeda Pharmaceutical to jointly advance its global development. Rather than going it alone, leveraging partners’ resources to accelerate product commercialization represents a pragmatic R&D strategy.

Also, IBI324 (a VEGF/Ang-2 bispecific antibody) targets the retinal disease market, with a potential market size of $15 billion. Its Phase Ib data are positive, and Phase III trials are planned for 2026. Each of these pipeline assets addresses clear market needs and holds the potential to become a “blockbuster” drug. This approach is far more substantive than spreading bets across numerous early-stage projects and relying on pipeline quantity to “tell a story.”

In its early years, Innovent’s approach to globalization was simply “selling rights”—licensing out the ex-China rights of its pipeline to overseas pharmaceutical companies in one-off deals, earning upfront payments and milestone fees, with no further involvement in subsequent development. While this model appeared safe, it failed to generate long-term returns or secure strategic control.

In 2025, Innovent Bio’s globalization strategy finally advanced to version 2.0—its collaborations with Takeda and Eli Lilly are no longer mere “out-licensing” deals but “co-development” partnerships. The collaboration with Takeda, with a total value exceeding $11.4 billion, focuses on the joint development of pipeline assets such as IBI343. The seventh collaboration with Eli Lilly, with potential payments of up to $8.5 billion, extends their decade-long partnership. These two deals, totaling over $20 billion, account for more than 10% of China’s total out-licensing value for innovative drugs in 2025, sufficiently demonstrating the global competitiveness of Innovent’s pipeline.

More importantly, through this “co-development” model, Innovent Bio can deeply engage in global clinical trials and regulatory submissions, while also sharing in overseas sales royalties—moving beyond “one-time earnings” to enjoying long-term global revenue from its products. Meanwhile, Innovent has established a hundred-strong team abroad and built an international operational system, demonstrating not just “paper strategies” but genuine global market deployment—this is the globalization posture that a Biopharma company should embody.

IV. Advancing to Biopharma: Why Innovent?

Many people ask: Why was Innovent Bio the first to successfully transform from a biotech startup into a biopharma company? It was not due to good luck or abundant financing, but because it was more “pragmatic” than its peers—avoiding hype and storytelling, and focusing on initiatives that are commercially viable and executable. This is its core competitive advantage.

First, full-industry-chain capability is not a “slogan” but a source of confidence. Unlike many biotech firms that focus solely on R&D, Innovent Bio has built out the entire value chain—target discovery, clinical development, manufacturing, and commercialization—from the outset. It operates manufacturing facilities compliant with GMP standards in China, the United States, and Europe, enabling in-house production and sales without reliance on contract manufacturing organizations (CMOs) or external commercial teams. This capability translates into resilience during industry downturns: while others struggle to secure manufacturing capacity through CMOs, Innovent can produce independently; while others fail to move their products, Innovent can leverage its own commercial team to penetrate the market.

Second, a dual-engine strategy of “R&D + BD” drives growth, avoiding blind independence while not relying solely on partnerships. Innovent Bio’s R&D does not follow the herd into hyper-competitive me-too development; instead, it focuses on high-potential targets. Its business development (BD) neither indiscriminately licenses nor partners without discernment, but rather collaborates with industry giants such as Takeda and Eli Lilly to achieve complementary strengths—leveraging its own robust pipeline alongside their global commercial channels and clinical capabilities to jointly develop products and share profits. This model delivers higher efficiency than pure in-house R&D and generates greater returns than simple licensing-out arrangements.

Third, commercialization capability is the “key to monetization.” The ultimate goal of innovative drugs is to achieve sales and generate profits. Innovent Bio’s commercialization team has proven its worth through performance—12 products have been included in the National Reimbursement Drug List (NRDL), with multiple products experiencing rapid volume growth, effectively translating R&D achievements into tangible revenue. Many biotech companies fail at the “last mile” precisely due to a lack of commercialization capabilities, whereas Innovent Bio’s early strategic positioning enabled it to seize this opportunity.

Fourth, a commitment to long-termism, free from the constraints of short-term gains. From betting on PD-1 inhibitors, to establishing a presence in chronic disease management, and advancing globalization, every step taken by Innovent Bio has been driven not by “quick wins,” but by strategic long-term planning. It neither expanded blindly amid the financing boom nor slashed its pipeline during industry downturns; instead, it steadily strengthened its foundation. By 2025, this approach finally yielded a qualitative breakthrough—a level of strategic discipline that is particularly rare in the often-restless innovative drug sector.

V. Lingering Concerns After Going Public

Of course, Innovent Bio’s 2025 was not perfect; even after achieving stability, significant concerns still lie ahead. We neither heap praise nor shy away from problems—this is the most objective perspective for observing the industry and the company.

The most immediate risk is competition. In the oncology sector, the PD-1 market has already become a red ocean, with mounting price pressures; despite its portfolio advantages, Innovent Bio is not immune to this intense domestic rivalry. In the chronic disease sector, the GLP-1 track has attracted strategic deployments from all major domestic and international players, meaning competition will intensify in the coming years. Whether Xin Er Mei can maintain its “first-mover advantage” remains uncertain. If it fails to sustain differentiation and rapidly penetrate the market, its growth trajectory is likely to slow down.

Next is R&D risk. Innovent Bio’s long-term value hinges almost entirely on its global pipeline, including IBI363 and IBI343. The outcomes of clinical trials for these products remain uncertain; moreover, overseas regulatory approvals are complex, with protracted review processes by the U.S. FDA and the European EMA. Any delays or setbacks could adversely affect the company’s valuation and market expectations.

There are also challenges in global operations. Managing an overseas team of over 100 employees across cultures and regions is inherently difficult; collaborating with giants such as Takeda and Eli Lilly poses additional tests in coordinating project timelines and allocating benefits. Market regulations and health insurance policies vary by country, requiring Innovent Bio to adapt quickly. Otherwise, even with successful product launches, it will be challenging to penetrate overseas markets.

Finally, there is the volatility of the capital markets. The valuation of innovative drug companies has always relied on “storytelling based on their pipelines.” Once pipeline progress falls short of expectations or industry policies change, stock prices may experience significant fluctuations. Although Innovent Bio has achieved profitability, investor expectations will rise accordingly. If subsequent performance growth fails to meet these heightened expectations, the company is likely to face pressure from a valuation correction.

VI. Final Thoughts: Is Innovent Bio’s Present the Future of Biotech?

Innovent Bio’s 2025 performance is not merely its own triumph, but also a “bellwether” for China’s innovative drug industry—demonstrating that the ultimate destiny of a biotech company is neither to be acquired by giants nor to rely perpetually on financing for survival, but to evolve into a self-sustaining biopharma with global competitiveness.

In the short term, from 2026 to 2027, Innovent Bio’s growth momentum remains robust: its oncology portfolio will provide stable cash flow through volume expansion under the National Reimbursement Drug List (NRDL) and the expansion of new indications; its chronic disease products are in a phase of rapid growth, with brands such as Xin’ermei and Xinbile continuing to see significant volume increases. Multiple securities firms predict that its revenue is expected to exceed RMB 20 billion in 2027, while its profitability will continue to improve.

From a medium- to long-term perspective, Innovent Bio’s growth ceiling hinges on its global pipeline. If IBI363 and IBI343 successfully achieve global market approval, the company will be able to tap into a multi-billion-dollar global market, transforming from a leading player in China into a globally leading biopharmaceutical enterprise—this is both its ambition and its goal. By 2030, it aims to advance at least five molecules into global Phase III clinical trials. This roadmap is not mere rhetoric but is grounded in its current pipeline strength and global strategic layout.

However, we must also clearly recognize that Innovent’s success is difficult to replicate. It benefited from the golden decade of innovative drug development in China, with ample financing support, precise strategic layout, and an efficient execution team—conditions not all biotech companies possess. Industry differentiation continues; in the future, more biotech firms will be eliminated. Only those enterprises that, like Innovent, are pragmatic, clear-headed, and strategically resilient will survive the winter and achieve a successful “landing.”

Innovent’s 2025 performance is both a satisfactory result and a new beginning. Its experience demonstrates that China’s innovative drug industry has moved beyond “wild growth” into an era of “intensive cultivation.” The ultimate battle for biotech companies hinges not on fundraising capacity or the size of their pipelines, but on product strength, commercialization capabilities, and strategic steadfastness in long-termism.