China's First Homegrown Radiopharmaceutical Approved: Top 10 Most Anticipated Domestic Radiopharmaceuticals

April 2,National Medical Products Administration (NMPA) website shows that Radio Medicine (under Gilead Pharmaceuticals) independently developedClass I radioactive innovative drug technetium [99mTc] Pexiretide Injection (99mTc-3PRGD2)、and the preparation of technetium [99m[Tc] Pexiretide Kit Approved for Marketing via Priority Review and Approval Program for Auxiliary Examination of Regional Lymph Node Metastasis in Patients with Suspected Lung Cancer.

This is China's first approved "First-in-class"”Class 1 New Drug for Nuclear Medicine Radiological Diagnosis, the First Domestically Produced One Approved for Market LaunchRadionuclide-Drug ConjugatesRDC is also the world’s first broad-spectrum tumor imaging agent for SPECT imaging.

Diagnostic nuclear medicines require the use of imaging equipment. Technetium [99mTc] The market launch of pexisretide injection willTransforming Nuclear MedicineSPECT/CT (Single-Photon Emission Computed Tomography) Imaging Technology: Current Technical Status and Common Misconceptions Regarding Its Inapplicability to Tumor Diagnosis, Staging, and Treatment Response MonitoringA direct commercial advantage is that SPECT/CT imaging offers lower clinical diagnostic costs and broader coverage in primary care hospitals.

Professor Li Fang from Peking Union Medical College Hospital, who serves as the Chairman of the Nuclear Medicine Equipment and Technology Branch of the China Association of Medical Equipment, once stated that99mTc-3PRGD2 is used for SPECT/CT imaging, and its clinical diagnostic cost is certainly lower than that of PET/CT (Positron Emission Tomography/Computed Tomography). This will be a boon for our country, especially for primary healthcare hospitals.

99mThe market launch of Tc-3PRGD2 aligns with the 2026 theme for China’s domestically developed radiopharmaceuticals—commercial scale-up and the inflection point for validation—underpinned by the two key pillars in the radiopharmaceutical sector: the “China Market” and “Chinese Assets.”

1Scramble for Territory: The Overture to MNCs’ Commercialization in China

According to Frost & Sullivan’s forecast, the market size of radiopharmaceuticals in China is expected to expand to RMB 26 billion by 2030.

On November 5, 2025, Novartis announced that lutetium [177Lu] vipivotide tetraxetan (Pluvicto) had been approved for marketing in China with dual indications, becomingChina's First Therapeutic Radioligand Therapy (RLT) Drug, indicated for the treatment of prostate-specific membrane antigen (PSMA)-positive advanced prostate cancer. As a flagship product in Novartis’s radiopharmaceutical portfolio, Pluvicto achieved sales of $1.994 billion in 2025, representing a 42% year-over-year increase and reaching “blockbuster drug” status. The opening of the Chinese market will further accelerate its progress toward the projected peak annual sales of $5 billion.

On one hand, the Chinese market continues to hold a significant position among MNCs’ key global markets, and in the emerging field of therapeutic radiopharmaceuticals, it remains largely untapped. Taking Novartis as an example, its revenue in the Chinese market reached $4.2 billion in 2025, representing an 8% year-on-year increase; its core operating profit margin stood at 40.1%, up by 210 basis points year-on-year, achieving its original 2027 target two years ahead of schedule. Furthermore, among the priority development regions identified by Novartis, China ranks second only to the United States, underscoring the company’s strong commitment to the Chinese market.

On the other hand, the core of radiopharmaceuticals lies in the comprehensive establishment of isotope preparation, production and delivery, and clinical application scenarios, with a particular need for localized teams and the capability to expand into specialized hospital segments. Isotope production capacity, drug half-life, and delivery coverage constitute an "impossible trinity" for the commercialization of radiopharmaceuticals. The rigid trade-offs among these three factors endow the radiopharmaceutical industry with inherent regional monopoly characteristics, thereby driving industrial development and resource allocation toward concentration and oligopolization.

First, on the production side, the technical barriers to radionuclide production are extremely high, requiring specialized reactors and technologies, making it a core resource that multinational corporations (MNCs) strive to secure. In July 2025, Novartis established its first foreign-invested radiopharmaceutical manufacturing facility in China—the Novartis China Radiopharmaceutical Production Base—located within the Nuclear Technology Application (Isotope) Industrial Park in Haiyan County, Jiaxing City, Zhejiang Province. Leveraging the unique advantages of the Qinshan Nuclear Power Plant’s heavy water reactor, the project represents a total investment of approximately RMB 600 million and is expected to commence production by the end of 2026.

Second, on the distribution end, the lutetium (Lu-177) used in PaweiTuo has a half-life of approximately 6.647 days. Due to the limited time window for administration, short- to medium-term radiopharmaceuticals are typically produced as single-patient doses, requiring a network of nuclear pharmacies or drug centers to facilitate production and delivery. It is precisely for this reason thatResource integration within the industry has long revolved around licensed nuclear pharmacy assets.From a specific pathway perspective, for Novartis, building its own nuclear pharmacy would incur unnecessary time costs (a construction period of 3+ years) and financial pressure (an investment of over RMB 40 million per nuclear pharmacy). Therefore, in December 2025, Novartis andChina Isotope & Radiation Corporation (a subsidiary of China National Nuclear Corporation) – Atom High-TechSigned a commercial cooperation agreement for Pluvicto to provide customized product supply and solutions for healthcare institutions and patients.

Third, in terms of the industrial chain, it is necessary not only to have mature and complete upstream and downstream industries and supporting nuclear pharmacy facilities, but also to ensure the presence of medical institutions qualified for the clinical use of radiopharmaceuticals within a certain range.Establishing a commercialization pathway in China’s radiopharmaceutical market at the earliest possible stage means securing clinical hospital access and building a commercial network, which will constitute the core competitiveness of multinational corporations (MNCs) in China’s radiopharmaceutical sector.

2Pathfinding: Commercialization of Biotech Assets

Similarly to multinational corporations (MNCs), emerging radiopharmaceutical companies lacking compliance experience and hospital access resources in China will initially focus on building competitive advantages in single-product categories, before partnering with leading pharmaceutical and nuclear technology enterprises to secure early-mover advantage in less contested markets.

The First Chinese FIC Radiopharmaceutical, Pexirertide Injection, Also Adopts the Model of Collaborating with Giants in Pharmaceutical Commercial Circulation.

As early as November 2023, Baiyang Pharmaceutical entered into a commercialization cooperation agreement with Ruidiao, granting Baiyang Pharmaceutical the rights to its independently developedNuclear Medicine Tumor Imaging DiagnosisClass 1 Innovative Drugs99mexclusive commercialization rights in mainland China for a series of radiopharmaceuticals, including Tc-3PRGD2, and imaging equipment such as SPECT. In fact,In 2022, Baiyang Pharmaceutical Group made a strategic investment in Ruidiao, which is centered around the team led by Professor Wang Fan, Director of the Peking University Medical Isotope Research Center, becoming its second-largest shareholder.Public information shows that,Baiyang Pharmaceutical (SZ.301015)also possesses99mCommercialization rights for multiple independently developed radiopharmaceuticals, including Tc-HP-Ark2.

As the first domestically developed Class 1 innovative diagnostic radiopharmaceutical in China, Pexiretide Injection exhibits a distinctly different business model from the therapeutic radiopharmaceutical Pluvicto. While Pluvicto relies on significant survival benefits to justify its high pricing, with later-stage expansion dependent on reimbursement negotiations or commercial insurance coverage, it also heavily depends on a comprehensive ecosystem spanning the entire therapeutic radiopharmaceutical industry chain.

Pexiretide Injection leverages the existing SPECT/CT equipment that is already widely installed—The core of commercial promotion lies in clinical validation, physician education, and technology dissemination, with the aim of changing the perception that “SPECT/CT can be used for tumor diagnosis and treatment response assessment.”Efficient Brand Operations and Channel Penetrationis the key to success.As a leading enterprise in pharmaceutical commercialization, Baiyang Pharmaceutical possesses significant advantages in building innovative brands, achieving omnichannel coverage (partnering with over 14,000 large and medium-sized hospitals), and operating a collaborative ecosystem for pharmaceuticals and medical devices.

Pexirretide Injection is the world’s first approved radiopharmaceutical drug conjugate (RDC) targeting integrin αvβ3. By utilizing an RGD peptide molecular probe, it can specifically bind to integrin αvβ3 receptors on the surface of tumor cells and endothelial cells of tumor neovasculature. The RGD peptide drug is labeled with the radionuclide technetium [99mTc], enabling99mAfter intravenous injection, Tc-3PRGD2 accurately accumulates in tumor tissues, enabling precise imaging via SPECT/CT.

18F-FDG PET/CT is currently the gold standard for clinical imaging diagnosis and staging of various malignant tumors. However, PET/CT objectively involves high equipment costs, complex preparation of imaging agents, and high fees per examination (around RMB 10,000).as well as limitations such as the need for patients to pay out-of-pocket. In contrast,SPECT/CT devices have a high penetration rate across China, radiopharmaceutical preparation is simple, examination costs are low (approximately RMB 1,000 per scan), and the procedure is covered by medical insurance.

2025 ASCO Annual Meetingpublicly disclosed Phase III trial data, compared with conventional 18F-FDG PET/CT metabolic imagingHead-to-head comparison,Clarified that inDiagnosis of Lymph Node Metastasis in Lung CancerAdvantages in Specificity and Accuracy: Among 272 Lung Cancer Patients Undergoing Surgery,99mThe specificity of Tc-3PRGD2 SPECT/CT in the diagnosis of lymph node metastasis was 74.0%, significantly higher than that of 18F-FDG PET/CT (50.0%); in terms of accuracy,99mThe Tc-3PRGD2 SPECT/CT rate was 70.4%, significantly higher than the 54.9% observed with 18F-FDG PET/CT. This indicates that, among the same number of samples,99mTc-3PRGD2 SPECT/CT can more accurately identify true tumor lymph node metastases, reducing misdiagnosis.

In terms of false positive correction,99mTc-3PRGD2 SPECT/CTCorrected 152 patients (59%)18F-FDG PET/CT of a Total of 344 Lymph Node StationsFalse-Positive Diagnosis, and provided more accurate assessment of lymph node metastasis in 116 patients (45%). In contrast, 18F-FDG PET/CT demonstrated higher diagnostic efficacy in only 40 patients (15%). This suggests that inflammatory or other non-malignant lesions may be misdiagnosed as tumor lymph node metastases by 18F-FDG PET/CT. Regarding the differential diagnosis of pulmonary malignancies, among 268 patients who received pathological diagnosis of pulmonary lesions,99mTc-3PRGD2 SPECT/CT and 18F-FDG PET/CT showed no significant difference in the detection rate of malignant lung tumors (sensitivity: 96% vs. 98%, P=0.083).

3Business Development Awaits: Clinical Breakthroughs Propel Chinese Original Radiopharmaceuticals to Top of Expectations

For domestic biotech companies, regulatory approval and business development (BD) are the two key pathways to validate the global competitiveness of independently developed radiopharmaceuticals.Looking back at 2025, China’s domestically developed radiopharmaceuticals experienced a surge in clinical trial approvals, with Chinese assets entering critical validation pathways. Meanwhile, breakthroughs in radionuclide production—such as the commissioning of the Qinshan Nuclear Power Plant’s heavy water reactor and the commencement of construction on the Jiajiang medical isotope test reactor—are set to disrupt the existing isotope production landscape and further unlock the potential of the Chinese market.

The competition for market share by MNCs and the search for strategic pathways by biotech firms together constitute the supply and demand sides of Chinese assets. How market expansion and education in China will accelerate the regulatory approval, commercialization, and global expansion of these assets remains to be seen.

Overall, the radiopharmaceutical innovation sector, still in the early stages of asset development, is constrained by platform validation and radionuclide production, leading to inevitable homogenization and intense competition in pipeline targets and indications.According to the PharmaCube database, the top three targets (PSMA, FAP, and HER2) in China’s current radiopharmaceutical pipeline account for a significant proportion, with indications largely confined to prostate cancer and neuroendocrine tumors, and few first-in-class products. This suggests that, under Novartis’ dominant position in the global radiopharmaceutical landscape, alpha-emitting radionuclide assets may hold greater advantage by aligning with the global trend of transitioning from beta- to alpha-emitting radionuclides. For instance, in 2024, Raylun Technology licensed 225Ac-FL-091 to South Korea’s SK Biopharmaceutics Group in a deal worth a total of $571.5 million.

Meanwhile, the mainstream RDCs in radiopharmaceuticals are expected to continue leveraging China’s pharmaceutical engineering dividends and conjugation advantages.Benchmarking against the long-standing success of bispecific antibodies and ADCs at BD—RDCs are similarly composed of a targeting ligand, linker, chelator, and radionuclide. The experience accumulated by Chinese biotech companies in target selection, linker design, and conjugation processes within the ADC and bispecific antibody fields can be rapidly transferred to RDC development. For instance, Baili Tianheng’s Class 1 innovative Antibody Radionuclide Conjugate (ARC) has already entered clinical trials.PossessDual China-US Regulatory Submissions and Clinical Trials,Mature Conjugation Technology Platform, clinical data validation, industrialization capabilityChina'sBiotech, inExternal Relations in the RDC SectorCooperationTimePlaceMore attractive.

However, due to more complex safety considerations and a greater number of players in the industrial chain,The clinical development cycle for RDCs may be longer, and business development (BD) activities in the RDC sector are more likely to occur in the late-stage clinical phase, after preliminary efficacy and safety have been validated.

Can the RDC Field Recreate the Myth of Duality Biologics?

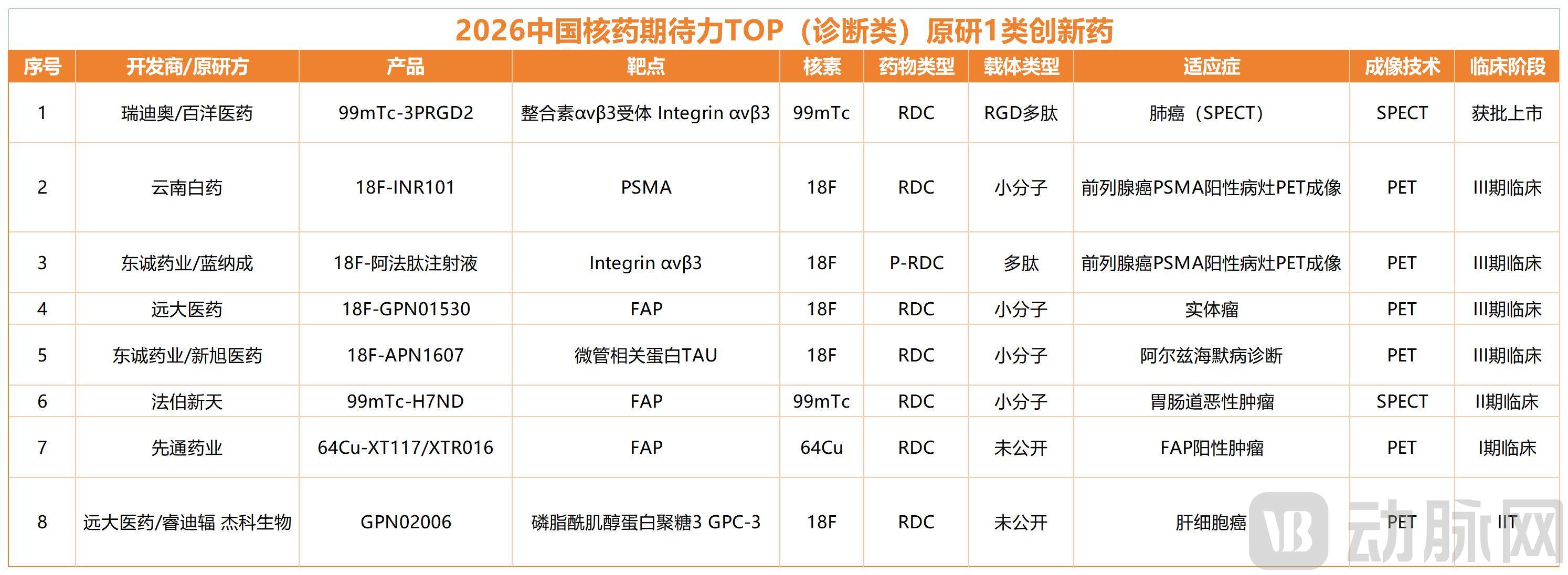

Graphic by VCBeat; rankings are not in any particular order.

VCBeat Graphic, Listed in No Particular Order