AC Immune Secures $12.5M Upfront from Lilly to Advance Next-Gen Tau-Targeting Alzheimer’s Therapies

AC Immune

Biopharmaceutical Manufacturer

On April 7, 2026, a transaction announcement sent the shares of Swiss biotech company AC Immune (ACIU) soaring more than 15% in intraday trading.

Eli Lilly and the company focused on precision medicine for neurodegenerative diseases have reached an amended agreement that expands their collaboration in Alzheimer’s disease (AD) and other neurodegenerative disorders: Eli Lilly will pay an upfront fee of CHF 10 million (approximately USD 12.5 million, or nearly RMB 100 million), with additional milestone payments due when candidate drugs enter Phase I clinical trials, while AC Immune remains eligible for over CHF 1.7 billion in subsequent milestones and sales royalties.

This is not the first collaboration between Eli Lilly and AC Immune. In 2018, the two parties signed a licensing agreement to jointly advance the development of small-molecule tau aggregation inhibitors. The amended agreement expands the scope of collaboration to include new lead candidates and backup compounds, with plans to initiate studies related to an Investigational New Drug (IND) application in the first half of 2026.

$12.5 Million Investment in AD Therapy

AC Immune was founded in 2003, and its core technology platform, “Morphomer,” is dedicated to developing small-molecule drugs capable of crossing the blood-brain barrier and targeting intracellular tau protein aggregates.

It is important to note that this approach represents a distinct departure from current mainstream Alzheimer’s disease (AD) therapies. Over the past decade, AD drug development has focused almost exclusively on beta-amyloid (Amyloid)—a pathway exemplified by Biogen/Eisai’s Leqembi and Eli Lilly’s donanemab (Kisunla). Amyloid plaques deposit outside neurons and are relatively accessible to clearance by antibody-based therapies. In contrast, tau protein neurofibrillary tangles form inside neurons, requiring small-molecule drugs not only to cross the blood-brain barrier but also to precisely inhibit intracellular protein aggregation without inducing toxicity. This challenge is widely recognized as one of the most difficult hurdles in neuroscience.

AC Immune’s platform is strategically designed to address this challenge. Its Tau Morphomer candidate drug can cross the blood-brain barrier following oral administration and specifically bind to pathological tau protein conformations, demonstrating potential in preclinical models to inhibit tau aggregation and spread. The company also possesses the SupraAntigen platform (for active immunotherapy) and the morADC platform (for antibody-drug conjugates), forming a diversified pipeline spanning tau, amyloid-beta, and alpha-synuclein targets.

Why Is Eli Lilly Doubling Down Now? The Answer Lies in Its Alzheimer’s Disease Pipeline Strategy.

Eli Lilly’s donanemab (Kisunla) received FDA approval in 2024, but its market performance has fallen short of expectations. On one hand, amyloid-targeting antibody therapies generally face safety controversies, with a high incidence of ARIA (amyloid-related imaging abnormalities), which limits their clinical adoption. On the other hand, donanemab’s efficacy data are not particularly impressive, and its once-monthly intravenous infusion regimen poses challenges to patient adherence. More importantly, the amyloid hypothesis itself is being reevaluated, as clinical evidence remains insufficient to demonstrate that plaque clearance can truly reverse cognitive decline.

The neuroscience community believes that tau protein aggregation has a stronger correlation with cognitive decline. The density of tau tangles is highly correlated with the degree of cognitive impairment in patients with Alzheimer’s disease. This means that even if amyloid-beta is cleared, the disease will continue to progress as long as tau pathology continues to spread.

As Andrea Pfeifer, CEO of AC Immune, stated in this transaction: “A growing body of scientific evidence indicates that targeting intracellular Tau can slow or even completely halt pathological progression.”

Furthermore, the modest $12.5 million investment exemplifies a classic strategy employed by large pharmaceutical companies to manage R&D uncertainty: securing options on early-stage pipelines at low cost. Evan Seigerman, an analyst at BMO Capital Markets, commented, “Do not view this $12.5 million as Eli Lilly’s ultimate bet on AC Immune’s technology; rather, it is more akin to an inexpensive ticket to the 2030 neuroscience market. Even if it fails, the impact on Eli Lilly’s substantial cash flow will be negligible; but if it succeeds, it could become the next blockbuster drug.”

Leveraging the GLP-1 Cash Cow to Shape the Future Pipeline

If we cast our minds back to the first quarter of 2026, the amended agreement between Eli Lilly and AC Immune may have been merely a small piece in its business development (BD) portfolio, given that Eli Lilly’s deal-making pace in Q1 could be described as intensive acquisition.

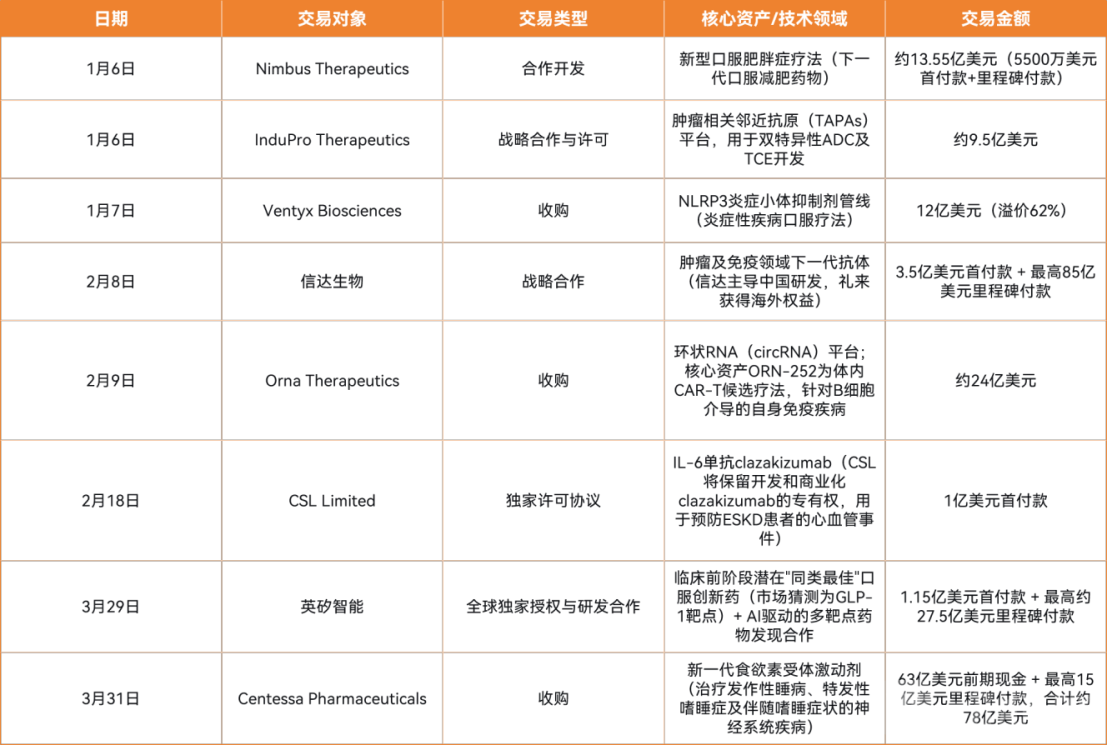

Key Transactions Disclosed by Eli Lilly in Q1 2026

Key Transactions Disclosed by Eli Lilly in Q1 2026

Before reviewing Q1 transactions, it is first necessary to emphasize that in late November 2025, Eli Lilly’s closing market capitalization surpassed $1 trillion. The landmark significance of this historic moment lies in the fact that a pharmaceutical company has broken the long-standing monopoly of tech giants in the “trillion-dollar club,” standing shoulder to shoulder with global technology leaders such as Apple and Microsoft.

For Eli Lilly, maintaining a trillion-dollar market capitalization also means that the company must stockpile products for the next decade at a pace far exceeding the industry average.

The core underpinning its trillion-dollar market capitalization is the performance of tirzepatide (Mounjaro/Zepbound) in the fields of weight loss and metabolic health. In 2025, combined sales of these two products reached $36.5 billion. However, reliance on a single product would become the most significant vulnerability for a company valued at over $1 trillion. Thus, the eight deals densely announced by Eli Lilly in the first quarter of 2026 were, to some extent, a defensive campaign to safeguard its trillion-dollar valuation, as the company seeks to systematically channel the substantial cash flow generated by its GLP-1 drugs into its future pipeline.

In terms of deal-making pace, on January 6, 2026, Eli Lilly announced two partnerships on the same day, and the following day acquired Ventyx Biosciences for $1.2 billion, securing its pipeline of NLRP3 inflammasome inhibitors. In February, Eli Lilly maintained this high-intensity transaction rhythm, with the cumulative total value of deals exceeding $10 billion. The cluster of transactions concentrated in late March further propelled Eli Lilly’s M&A activities in the first quarter to a climax, nearly reaching a single-deal value of over $10 billion.

Viewing the Q1 transactions collectively reveals Eli Lilly’s strategic logic with clarity: in metabolism, the company is fortifying its moat through collaboration with Nimbus and licensing from Insilico Medicine; in neuroscience, it is positioning itself for the next generation of blockbuster therapies via the acquisition of Centessa; in oncology immunotherapy, it is building differentiated technology platforms through partnerships with Orna, InduPro, and Innovent; and in inflammation, it is supplementing its portfolio with the broad-spectrum NLRP3 target through the acquisition of Ventyx. This strategic alignment corresponds with the maturation of Eli Lilly’s new drug portfolio, where newly approved products such as Jaypirca, Kisunla, and Omvoh have already contributed nearly $1 billion in revenue in 2025.

Neuroscience is regarded as Eli Lilly’s second growth curve. Meanwhile, the intent to hedge risks is also clearly evident. The amyloid pathway in the Alzheimer’s disease (AD) field carries uncertainty, making tau protein a key alternative; the autoimmune sector requires a more diversified target portfolio; and cell therapy demands more cutting-edge platform technologies.

The deeper logic lies in Eli Lilly’s maximization of the substantial cash flow advantages generated by GLP-1 therapies. In 2025, Eli Lilly’s R&D expenditure reached $13.337 billion, a year-on-year increase of 21%, accounting for over 20% of its total revenue. This has established a virtuous cycle of R&D investment, new product launches, cash flow growth, and reinvestment—a cycle that continues to accelerate even at the scale of a trillion-dollar market capitalization.

Collectively Combating Patent Cliff Anxiety: Fueling a Wave of M&A Among Pharmaceutical Giants

Eli Lilly is not an isolated case.

In the first quarter of 2026, mergers and acquisitions (M&A) in the global pharmaceutical industry witnessed an unprecedented surge, with multiple multinational corporations (MNCs) simultaneously embarking on aggressive acquisition sprees. From a broader perspective, Eli Lilly’s active dealmaking in Q1 2026 also reflects the transformation underway in the global pharmaceutical sector: Against the backdrop of an impending patent cliff, with approximately $236 billion worth of drugs globally facing patent expiration, MNCs must bolster their pipelines through external in-licensing and acquisitions.

By 2026, the patent cliff has become a well-worn cliché. However, to further understand the starting point of the collective anxiety among multinational corporations (MNCs), we must look at a set of figures. According to an analysis by Evaluate, nearly 40% of the 487 new drugs approved by the FDA between 2014 and 2023 are expected to surpass the traditional $1 billion annual sales threshold for “blockbuster” drugs at their peak sales. Yet, the industry’s actual profit distribution has long moved beyond the Pareto principle (the 80/20 rule), concentrating in a more extreme manner: super blockbusters, accounting for only 4% of the total number of new drugs, have captured nearly 30% of the industry’s new drug revenue.

Such a yield curve has forced the core strategies of every multinational corporation (MNC) to gradually converge, namely, to create the next Keytruda or the next Opdivo at all costs. However, it is precisely at this juncture that the cornerstone supporting excess profits is accelerating its erosion.

From 2025 to 2030, global pharmaceutical sales totaling approximately $236 billion will face the direct impact of patent expirations. The exclusivity periods for nearly 70 blockbuster drugs will expire sequentially, with industry giants such as BMS, Pfizer, AstraZeneca, and Novartis being particularly heavily affected.

At the core of this “patent cliff” are large-molecule biologics and complex biological products, including higher-barrier technologies such as immunotherapies and novel diabetes drugs; consequently, the impact is broader in scope and more structural in nature. Meanwhile, today’s multinational corporations (MNCs) have more concentrated pipelines, with a handful of large-molecule drugs often accounting for the majority of corporate profits. Once patents expire, it is the underlying business model that comes under threat.

Accompanying this is the倒逼 effect of the U.S. Inflation Reduction Act (IRA). The IRA’s drug price negotiations officially took effect in January 2026, with the first batch of 10 drugs included in the price reduction list. This means that the business model relying on a single blockbuster drug faces sharply increased risks. Multinational corporations (MNCs) must diversify their pipeline portfolios to mitigate these risks.

This sense of crisis has been reflected in the capital movements of multinational corporations (MNCs) during the first quarter, such as Eli Lilly’s increased investment in AI-driven drug discovery. For pharmaceutical companies of this scale, fundamentally addressing pipeline gaps requires new, reusable platforms capable of sustained output, rather than merely a few specific products. This is precisely the underlying reason why AI-driven drug discovery has been comprehensively upgraded to core infrastructure status starting in 2026.

Eli Lilly’s increased investment in Q1 is noteworthy not only because it holds the highest valuation among pharmaceutical companies, but also because it exemplifies a typical strategic approach adopted by multinational corporations (MNCs): leveraging AI to compress R&D costs and timelines, while reinforcing its innovative technology portfolio by capitalizing on its core strengths, and simultaneously maintaining strategic investments in longer-term pipeline areas such as Alzheimer’s disease (AD) therapies.

By the time the patent cliff truly bottoms out in 2030, the surviving major pharmaceutical companies will not be those with the largest product pipelines, but rather those that have completed platform-level transformations earliest and successfully established structural barriers in next-generation therapies.

Returning to the deal between Eli Lilly and AC Immune. The $12.5 million upfront payment may appear insignificant on Eli Lilly’s M&A list for Q1 2026, but it aligns with a strategic narrative common among multinational corporations (MNCs): leveraging the substantial cash flows generated by blockbuster drugs to pave the way for growth in the next decade.

Tau protein remains the most formidable challenge in the field of Alzheimer’s disease (AD) and represents the most promising alternative avenue beyond the amyloid-beta pathway. Whether the combination of AC Immune’s technology platform with Eli Lilly’s clinical development and commercialization capabilities will bear fruit by 2030 remains uncertain. Yet, the first strokes defining the competitive landscape of the global pharmaceutical industry in the next decade may well be drawn by the deals struck in 2026.