Huilun Pharma Files for Hong Kong IPO: A Case Study in Transition from Single-Product Dependence to a Portfolio of Global First-in-Class and China-Only Therapies

Huilun Pharma

Innovative Drug Developer

As the era of exclusive products fades and revenues are halved, how can a long-established pharmaceutical company continue to seek its next growth engine amidst changing times?

On April 2, 2026, Shanghai Huilun Pharmaceutical Co., Ltd. filed its prospectus with the Hong Kong Stock Exchange, with CITIC Securities serving as the sole sponsor. Behind this filing lies a highly representative transformation story within China’s pharmaceutical industry—from a generic drug manufacturer that benefited from specific cyclical dividends to a biotech company heavily investing in innovative drugs. Huilun Pharma’s 22-year development journey reflects the evolutionary trajectory of China’s chemical pharmaceutical sector.

Starting with Generics: Targeting Critical Care to Forge China’s Only Domestically Produced Single Product

Huilun Pharma’s growth is deeply intertwined with the industrial strategy of its founder, Dong Dalun. A 1984 graduate of Nanjing College of Pharmacy (now China Pharmaceutical University), Dong established Xintian Pharmaceutical in Guiyang in 1995 and successfully listed the company on the A-share market in 2017, thereby accumulating substantial industry resources and capital operation expertise in the field of traditional Chinese medicine (TCM). However, given the high challenges in standardization, the significant differences in clinical evidence systems compared to chemical drugs, and the limited pathways for internationalization within the TCM sector, he resolved to pioneer a new strategic direction.

In 2004, Dong Dalun embarked on his second entrepreneurial venture in Shanghai, formally establishing Huilun Pharma with a strategic focus on small-molecule chemical drugs, thereby creating a clear business differentiation from Xintian Pharmaceutical. At that time, China’s generic drug industry was still experiencing rapid growth, while policies supporting innovative drugs were gradually being refined. As the most mature form of pharmaceuticals, small-molecule chemical drugs offered substantial potential for structural optimization and clinical enhancement, which became the core strategic rationale for Huilun Pharma’s layout.

Around 2010, while most companies in the industry flocked to conventional generic drugs, Huilun Pharma made a pivotal strategic choice: to focus on developing improved new drugs in the field of acute and critical care. Although such drug development entails high technical challenges and stringent clinical requirements, it offers a clear competitive landscape and well-defined unmet clinical needs upon approval, thereby establishing formidable commercial barriers that are difficult to replicate. This differentiated decision became the core pillar of Huilun Pharma’s subsequent growth.

The core achievement of this strategy isSivelestat Sodium for Injection (Xiwena), approved in March 2020 through priority review. As the only domestically produced drug in China and the only approved targeted therapy worldwide for acute lung injury/acute respiratory distress syndrome (ALI/ARDS) associated with systemic inflammatory response syndrome, Xiwena precisely fills a critical gap in intensive care unit (ICU) medications for critically ill patients.By inhibiting neutrophil elastase, this drug effectively ameliorates lung injury, improves the oxygenation index, shortens the duration of mechanical ventilation and ICU stay, and enhances patient survival rates. It demonstrates an excellent safety and tolerability profile and is recommended by multiple authoritative domestic and international guidelines and expert consensus statements.

The “Windfall” Profits Brought by the Pandemic

The commercialization of Xiweina coincided with a special period of global public health challenges, during which its clinical value was rapidly validated and widely recognized.

In early 2020, as understanding of the pathogenic mechanisms of COVID-19 deepened, clinical observations revealed that severe cases often presented with acute lung injury caused by a “cytokine storm”—precisely the indication for Sivelestat. Against the backdrop of rising pulmonary infection cases, this medication for critical care witnessed a concentrated surge in clinical demand. It is crucial to emphasize that this explosive demand was not driven by opportunistic, trend-chasing marketing, but rather by the drug’s well-defined pharmacological mechanism and robust clinical evidence: Sodium Sivelestat protects lung tissue from further damage by inhibiting neutrophil elastase, thereby blocking the inflammatory cascade.

Data confirms the product’s commercial value: In 2023, Xiweina generated sales revenue of RMB 745 million, accounting for 75.7% of total revenue, driving Huilun Pharma’s full-year revenue to RMB 985 million and achieving a net profit of RMB 20.659 million.

However, as post-pandemic medical demand returns to normal levels, sales of Xiwena, a drug for the treatment of acute lung injury/acute respiratory distress syndrome (ALI/ARDS), have gradually returned to a rational range.Sales revenue dropped to RMB 424 million in 2024 and further adjusted to RMB 370 million in 2025, with its share of total revenue declining to 54.0%.

In response to this change, Huilun Pharma proactively optimized its operational strategies by adjusting distributor inventory structures, strengthening academic promotion at terminal hospitals, and expanding the patient population with conventional ALI/ARDS, thereby establishing a new demand equilibrium. Despite the structural adjustments, Xiweina has maintained its position as a core product, continuing to generate cash flow.

Diversified Expansion of Product Portfolio, with New Product Revenue Growing by Approximately 192.4%

To reduce reliance on a single product, Huilun Pharma is continuously advancing the diversification of its product portfolio, establishing a comprehensive coverage pattern encompassing “critical care + oncology + chronic diseases.” This strategy drives the upgrading of its revenue structure from “single-pillar support” to “multi-polar synergy,” with Zuoyu (Levoleucovorin for Injection) emerging as the most prominent growth curve.

Zuoyu, as the first injectable levoleucovorin in China to be declared and approved under Category 2 of improved new chemical drugs, is a key adjuvant medication for chemotherapy of gastrointestinal tumors such as colorectal cancer. It can be directly co-infused with 5-fluorouracil, enhancing clinical efficiency and safety. Its patented lyophilized powder injection formulation offers higher purity, greater stability, lower safety risks, and a longer shelf life compared to the original solution formulation.

In a domestic market landscape with only two approved products, Zuoyu achieved sales of RMB 25.863 million in 2024 and RMB 75.635 million in 2025, representing a year-on-year increase of approximately 192.4%, thereby becoming the second growth curve for Huilun Pharma.

Meanwhile, generic drugs such as Kangmairui (ticagrelor), Lierban (rivaroxaban), and Tinuoan (dienogest) continue to contribute stable cash flow. Kangmairui is indicated for acute coronary syndrome and outperforms clopidogrel in terms of onset speed, inter-individual variability, and recovery of coagulation function after discontinuation. As an oral Factor Xa inhibitor, Lierban is a commonly used anticoagulant in clinical practice. Tinuoan is the first commercially available generic dienogest in China, used for the treatment of endometriosis.

Although these products face pricing pressure from the volume-based procurement (VBP) policy, they have gained certainty in sales volume. The prospectus indicates that while VBP provides a guarantee of sales volume, it also exerts significant pressure on product pricing: Lierban (10 mg) saw price reductions of 97% to 99% in the fifth national VBP round, while Kangmairui (90 mg) experienced declines of 55% to 92%. Furthermore, as one of the core products, Tinuoan failed to win a bid in the 2025 VBP round. Consequently, Huilun Pharma anticipates a decline in its production and sales volume, dynamically adjusting its production and inventory strategies accordingly, and recorded tens of millions of yuan in inventory impairment provisions for Tinuoan in 2025.

The optimization of the revenue structure is clearly visible: the proportion of revenue from Xiweina decreased from 75.7% in 2023 to 54.0% in 2025, while that from Zuoyu increased from 2.4% to 11.0%, and that from Dinuoan rose from 7.2% to 13.4%.The proportion of Mindray, Lilban, and other products increased from 14.7% to 21.6%. A diversified product landscape haseffectively hedging against the volatility risk of a single product, thereby securing a valuable strategic window for innovative transformation.

10 Funding Rounds in 12 Years, with Bets from Several Local State-Owned Enterprises

While steadily expanding its business, Huilun Pharma has completed a 12-year capitalization strategy, securing ample funds for its transition toward innovative drug development. From the initiation of its Series A financing in October 2013 to the completion of its Series I round in September 2025, the company successfully closed ten financing rounds. Its post-money valuation surged from RMB 225 million to RMB 3.431 billion, representing an increase of more than 15-fold. Notably, Huilun Pharma maintained a consistent financing pace even during the biopharmaceutical capital winter of 2021–2023, fully demonstrating the capital market’s recognition of the company’s long-term value.

It is worth mentioning that,Huilun Pharma’s shareholder structure exhibits a diversified profile characterized by “industrial capital + local state-owned assets.”Local industrial capital from state-owned assets in Guizhou and Jiangsu has successively entered the fray, aligning respectively with the founder’s industrial roots, the location of production bases, and key regions for commercial expansion. Meanwhile, market-oriented financial investments from entities such as Hainan Zhongtai and Jiaxing Huayu have provided concurrent support, establishing a diversified and stable capital structure.

This capital structure aligns closely with Huilun Pharma’s industrial layout. Its production base is located in Taizhou, Jiangsu Province, and features manufacturing lines for both active pharmaceutical ingredients (APIs) and finished drug products. In 2024, the company also commenced construction of a new production facility in Zhijiang, Hubei Province, which is expected to begin operations in the second half of 2026, thereby reserving production capacity for the commercial manufacture of innovative drugs.

Huilun Pharma’s path to capitalization has also undergone exploration and adjustment. In 2022, Huilun Pharma initiated listing tutoring with the aim of going public on the STAR Market. However, due to factors such as tighter IPO policies in the biopharmaceutical industry, the listing process did not proceed as scheduled. In 2024, Xintian Pharmaceutical (an A-share listed company controlled by Dong Dalun) had planned to acquire an 85.12% equity stake in Huilun Pharma at a valuation of RMB 2.9 billion, but the deal was later terminated. Following the termination of the acquisition plan, Huilun Pharma did not immediately abandon its capitalization strategy; instead, it continued to explore various financing options, including an IPO in Hong Kong. Ultimately, Huilun Pharma chose to pursue an independent listing in Hong Kong to access a more international capital platform and a more flexible financing mechanism.

Innovative Drug Strategy Breakthrough: Multiple Products Possess First-Mover Advantages, Including Global First-in-Class and Domestic First-to-Market Status

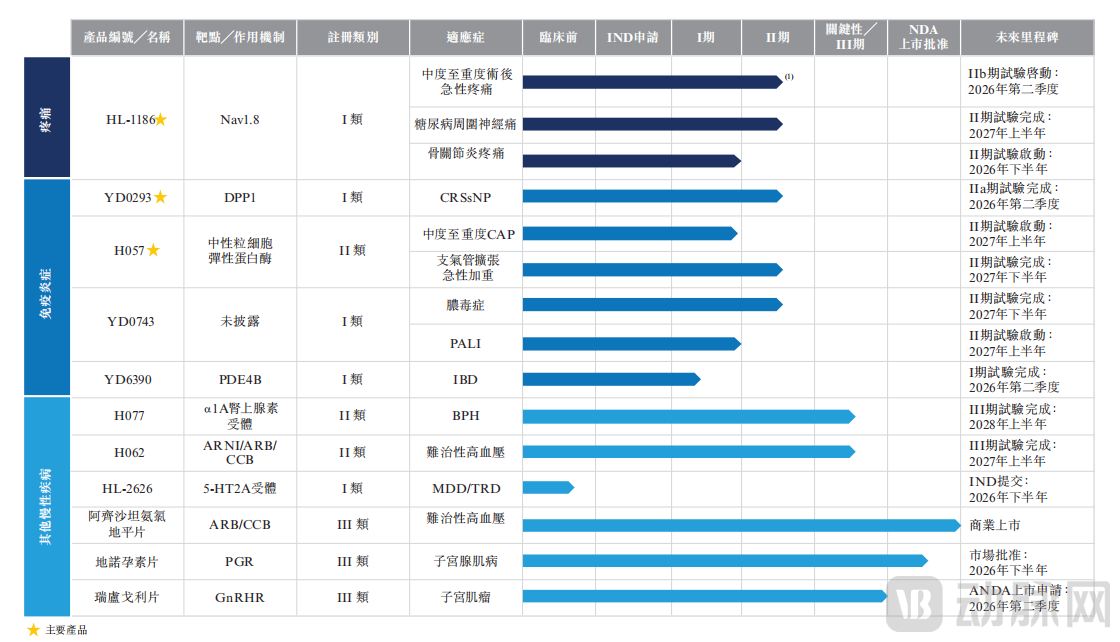

Standing at a new starting point for its IPO, Huilun Pharma has clearly defined innovation-driven R&D as the engine for long-term growth, transitioning from a “generic-and-innovation hybrid” model to an “innovation-driven” strategy. The vast majority of the proceeds from this Hong Kong IPO will be allocated to the clinical development of products in its pipeline.To date, the company has four Class I innovative drugs and three Class II improved new drugs in clinical development, covering multiple therapeutic areas including pain management, respiratory diseases, and oncology supportive care. Several of these products possess differentiated advantages as global first-in-class or domestic first-to-market innovations.

Huilun Pharma’s Pipeline, Source: Prospectus

· HL-1186As the first Nav1.8 inhibitor in China to enter clinical studies, it is a next-generation non-opioid innovative analgesic that the company is prioritizing. By targeting peripheral pain signaling channels, it delivers potent analgesia while avoiding addiction and central nervous system side effects. The product has currently completed two Phase IIa clinical trials for postoperative acute pain, with Phase IIb studies scheduled to launch in the second quarter of 2026. Concurrently, the company is expanding into major indications such as diabetic peripheral neuropathic pain and osteoarthritis pain. Against the backdrop of surging demand for non-opioid analgesics, this product is poised to become a core growth engine for the company’s future.

· YD0293It is the world’s only DPP-1 inhibitor targeting chronic rhinosinusitis without nasal polyps (CRSsNP), directly addressing the clinical unmet need for targeted therapies in the predominant sinusitis phenotype among Asian populations. While tens of millions of patients in China suffer from this condition, traditional treatment options offer limited efficacy. Phase I clinical trials have demonstrated favorable pharmacokinetic profiles and safety. The Phase IIa trial is expected to be completed in the second quarter of 2026, establishing a high clinical barrier through its exclusive target positioning.

· H057As the only inhaled sivelestat sodium product globally to have entered clinical trials, this upgraded and improved version of Xivena achieves precise pulmonary delivery via inhalation administration, reduces systemic adverse reactions, and expands into new indications such as community-acquired pneumonia and acute exacerbations of bronchiectasis. It complements Xivena in terms of dosage form and indications, further consolidating the company’s leading position in the field of severe respiratory critical care.

Furthermore, its pipeline includes several products that have entered pivotal clinical stages, such as YD0743 for sepsis, YD6390 for inflammatory bowel disease, H077 for benign prostatic hyperplasia, and H062 for refractory hypertension, with key milestones expected to be achieved sequentially over the next two to three years.

To support its innovation-driven transformation, Huilun Pharma had established two wholly-owned subsidiaries dedicated to innovative drug development by the end of 2025, building a comprehensive R&D engine that spans the entire process from drug discovery to regulatory approval. In terms of intellectual property, the company holds 107 granted patents and has 109 patent applications pending, covering major global markets including China, the United States, and Europe, thereby establishing a robust intellectual property protection system.

The Future of a “Hybrid Imitation-and-Innovation” Sample

Currently, Huilun Pharma is in a critical period of accumulating momentum for its innovative transformation, with financial data clearly reflecting the logic behind its strategic investments.

From 2023 to 2025, its revenue was adjusted from RMB 985 million to RMB 686 million, while net profit shifted from a profit of RMB 20.659 million to losses of RMB 124 million in 2024 and RMB 174 million in 2025. The losses were primarily attributable to the optimization of mature product portfolios and sustained increases in innovative R&D investment. R&D spending demonstrated robust growth, amounting to RMB 211 million, RMB 195 million, and RMB 234 million in 2023, 2024, and 2025, respectively. In 2025, R&D expenditure accounted for 34.2% of revenue, significantly exceeding the 10%–20% range typical of generic pharmaceutical companies in the industry.

In the long run, Huilun Pharma’s IPO narrative is essentially a proposition concerning the timing of transformation and strategic patience.

In this transformation, Huilun Pharma’s strengths lie in: proven commercialization capabilities (more than ten marketed products and a nationwide marketing network), a differentiated pipeline portfolio (innovative targets that are first-in-class globally or domestically), and comprehensive supply chain control (end-to-end manufacturing from APIs to finished dosage forms).

Yet the challenges are equally clear: the lingering effects of reliance on a single blockbuster product (Xiveina still accounts for over 50% of revenue), continued pressure from centralized procurement of generic drugs, the capital-intensive nature of innovative drug clinical development, and the erosion of profits by high selling expenses (selling expenses reached RMB 376 million in 2025, representing 54.8% of revenue). However, against the backdrop of the pharmaceutical industry’s return to innovation-driven value, Huilun Pharma’s balanced transformation path offers rare reference significance.

With mature businesses as its foundation and innovative R&D as its engine, Huilun Pharma’s path of balancing generics and innovation represents not only a company’s capital advancement but also a vivid microcosm of the Chinese pharmaceutical industry’s transition from imitation to innovation. Time will ultimately bear witness to the true quality of this transformation.