Eli Lilly to Acquire Kelonia Therapeutics for $7 Billion, Featuring $3.25 Billion Upfront, in Largest In Vivo CAR-T Deal in History

Under the terms of the agreement, Eli Lilly will acquire Kelonia Therapeutics. Kelonia’s shareholders will receive total cash consideration of up to $7 billion, including an upfront payment of $3.25 billion (approximately RMB 22.2 billion) and subsequent payments upon the achievement of certain clinical, regulatory, and commercial milestones. The transaction is subject to customary closing conditions, including routine regulatory approvals, and is expected to be completed in the second half of 2026.

This price far exceeded market expectations. Just the day before, The Wall Street Journal, citing sources familiar with the matter, reported that market expectations for the transaction amount remained at “more than $2 billion.” The jump from $2 billion to $7 billion marks a new acquisition record in the in vivo CAR-T field, as Eli Lilly offered this premium for a clinical-stage biotechnology company that is only six years old and has yet to bring any products to market.

Clinical Data Disclosure + Scarcity of Technology Platform, Value Doubles

The clinical data from Kelonia’s core pipeline candidate, KLN-1010, served as the most direct catalyst for the surge in valuation.

In December 2025, Kelonia presented initial data from the first three patients in a prominent oral session at the American Society of Hematology (ASH) Annual Meeting: all three patients achieved minimal residual disease (MRD) negativity without requiring lymphodepleting chemotherapy, exhibited robust CAR-T cell expansion, and demonstrated a favorable safety profile. While these findings garnered significant attention at the ASH meeting, the extremely small sample size (n=3) and short follow-up period left the market in a wait-and-see stance.

At the American Association for Cancer Research (AACR) Annual Meeting in April 2026, Kelonia presented updated and more comprehensive follow-up results—

In terms of efficacy: All four patients achieved a 100% MRD-negative response rate; the two patients with the longest follow-up durations maintained MRD negativity within three months. According to the International Myeloma Working Group (IMWG) criteria, all four patients remained in remission, with a maximum follow-up period of five months, and complete response was the best overall response.

In Vivo Expansion Levels: The expansion of CAR-T cells generated in vivo was comparable to that observed with ex vivo CAR-T cell therapy, reaching 85% of circulating T cells. Sustained CAR-T memory cells were observed in all four patients during the three-month follow-up period, indicating that the in vivo-generated CAR-T cells were not only sufficient in number but also possessed the potential for long-term persistence.

Safety Profile: The toxicity profile was favorable, with no occurrences of grade 3 or higher cytokine release syndrome (CRS), immune effector cell-associated neurotoxicity syndrome (ICANS), or delayed neurotoxicity. Cytopenias were significantly less frequent compared to ex vivo CAR-T therapy. The absence of a requirement for lymphodepleting chemotherapy directly reduced treatment-related toxicity and complexity.

More importantly, KLN-1010 received FDA IND approval in January 2026, becoming the first anti-BCMA in vivo CAR-T program to conduct multicenter clinical trials in the United States. This signifies a substantial reduction in regulatory risk for this pipeline, marking its transition from “early exploratory research” to “pivotal registration-enabling clinical trials.”

From ASH to AACR, a mere four months apart, Kelonia has achieved a pivotal transformation in its corporate identity,From an early-stage platform company with only sporadic IIT data, it has transformed into a clinical-stage asset holding FDA IND approval, with ongoing Phase I data validation and continuously improving data quality.This identity leap is the core reason why Eli Lilly was willing to raise its offer within 24 hours to “a $3.25 billion upfront payment + a total deal value of $7 billion.”

In addition to the continuous validation of clinical data, the scarcity of Kelonia’s technology platform is another pillar supporting its high valuation.

Kelonia's core technology is iGPS.®(In Vivo Gene Targeting System) platform, based on engineered lentiviral vector particles, directly generates CAR-T cells in patients through a single intravenous infusion. According to the company’s official description, this system employs envelope-modified lentiviral vectors to enhance in vivo gene delivery efficiency and utilizes targeting molecules to facilitate tissue-specific delivery, thereby enabling efficient and selective entry into T cells in vivo.

The uniqueness of its technological approach is reflected at three levels:

First, the "active targeting" mechanism.Conventional lentiviral vectors naturally tend to enter cells via the low-density lipoprotein (LDL) receptor, making them prone to “sequestration” by organs such as the liver. Kelonia has implemented dual modifications to its vector: it employs a VSV-G mutant to reduce hepatic tropism, while simultaneously expressing an anti-CD3 single-chain antibody on the viral surface to achieve precise recognition of T cells. This “de-targeting plus re-targeting” design presents a significant technical barrier within the industry.

Second, lymphodepleting chemotherapy is not required.Prior to traditional CAR-T therapy, patients must undergo lymphodepleting chemotherapy, which can cause side effects such as myelosuppression and an increased risk of infection. Kelonia’s clinical data demonstrate that iGPS®The vector enables robust expansion of CAR-T cells in patients without the need for lymphodepletion pretreatment. Jacob Van Naarden explicitly stated, “Autologous CAR-T therapy has significantly improved treatment outcomes for patients with various cancers, but significant barriers in manufacturing, safety, and accessibility mean that only a small fraction of eligible patients actually receive this therapy. Kelonia’s in vivo platform has the potential to change this landscape by delivering rapid and durable efficacy in a simpler, off-the-shelf format.”

Third, platform scalability. iGPS®Not only can it deliver CAR genes, but it can also deliver other therapeutic transgenes. Dr. Kevin Friedman, CEO of Kelonia Therapeutics, emphasized in a statement: “By leveraging Eli Lilly’s strengths, our in vivo iGPS®“The platform is poised to expand the application of cell therapies beyond their current use in hematologic malignancies, bringing transformative change to the treatment of a broader range of cancers and other serious diseases.”

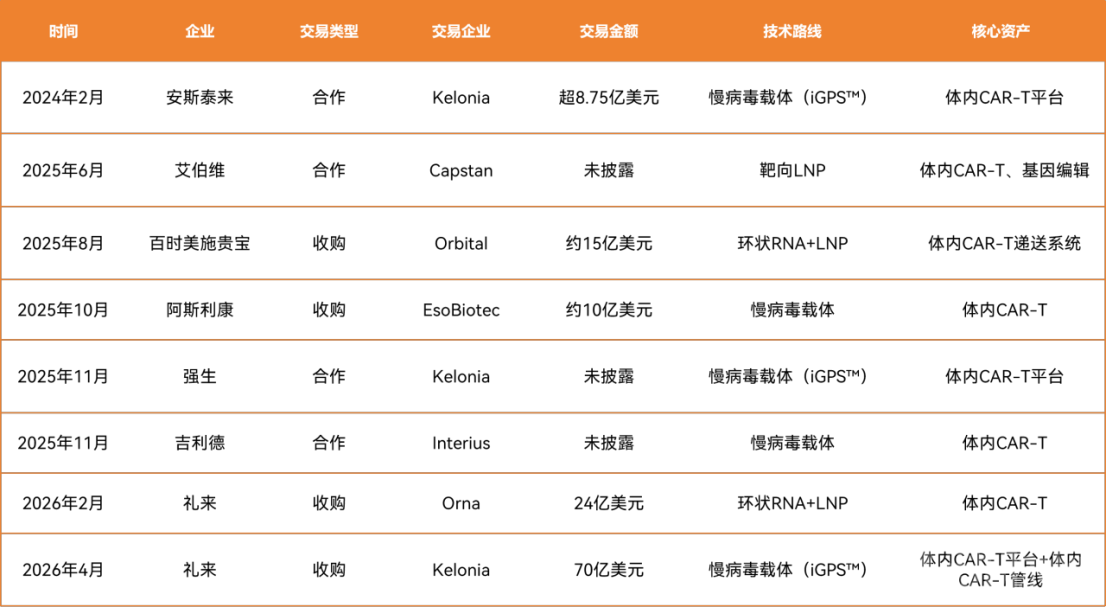

In the debate over technical approaches for in vivo CAR-T therapy, both lentiviral vector and lipid nanoparticle (LNP) platforms have their proponents. The advantage of the lentiviral vector approach lies in its integration into the T-cell genome, enabling long-term, stable expression of the chimeric antigen receptor (CAR), which naturally aligns with the need for “sustained cytotoxicity” in cancer treatment. Leveraging its proprietary platform, Kelonia has previously secured collaborations with Astellas (in February 2024, with a potential total value exceeding $875 million) and Johnson & Johnson (in November 2025).

As the Race Among Giants Heats Up, Is Eli Lilly a “Must-Buy”?

If Eli Lilly does not acquire Kelonia, who will?

This poses a major test for the market, given that over the past year, global pharmaceutical giants have been intensively positioning themselves in the field of in vivo CAR-T therapy.

From a timeline perspective, in 2026, Eli Lilly’s acquisition cost in the field of in vivo CAR-T therapy surged from $2.4 billion to $7 billion within just two months, nearly tripling. This not only reflects the high quality of Kelonia’s assets but also highlights the rapidly intensifying competition among industry giants for this strategic sector.

Prior to Eli Lilly, AstraZeneca, BMS, AbbVie, Gilead, and Johnson & Johnson had already entered the field. Leveraging its lentiviral vector technology platform and partnerships with Johnson & Johnson and Astellas, Kelonia has become a highly sought-after target in this therapeutic avenue.

If Eli Lilly does not make a move, Kelonia is likely to be acquired by Johnson & Johnson or Astellas, with whom it already has collaborative foundations, or by another major pharmaceutical giant that has not yet established a presence in the lentiviral vector space (such as Novartis or Pfizer). For Eli Lilly, this would no longer be merely a question of acquiring a company, but rather a defensive strategy essential to staying competitive.

Viewed alongside Eli Lilly’s $2.4 billion acquisition of Orna Therapeutics in February 2026, the Kelonia acquisition brings Eli Lilly’s cumulative investment in the in vivo CAR-T field to nearly $10 billion. Eli Lilly’s strategic intent is becoming increasingly clear: by securing both the lentiviral vector and LNP/circular RNA technological pathways, the company ensures it will remain competitive regardless of which approach ultimately prevails.

This dual-track strategy is unique among multinational corporations (MNCs). Most other pharmaceutical giants have chosen to bet on a single approach: for example, AstraZeneca opted for lentiviral vectors (via EsoBiotec), AbbVie chose lipid nanoparticles (LNPs) (via Capstan), and Bristol Myers Squibb (BMS) selected circular RNA (via Orbital). Eli Lilly remains the only major pharmaceutical company currently pursuing both mainstream pathways simultaneously.

Furthermore, the substantial cash flow generated by Eli Lilly’s GLP-1 product, tirzepatide, has provided ample resources for its aggressive investments in next-generation technology platforms. Beyond GLP-1, Eli Lilly is building its growth engine for the next decade. Pipeline assets in next-generation technology platforms—such as in vivo CAR-T, gene therapy, and RNA therapies—are essential strategies for large pharmaceutical companies to navigate economic cycles and mitigate risks associated with reliance on single products.