Yisi Medical Poised for a Comeback in China's 2026 Stapler Tender

ESM

Developer of High-End Medical Devices for Minimally Invasive Oncology Surgery

Since 2021, the Chongqing-led Eight-Province Alliance, the Fujian-led Fifteen-Province Alliance, and the Beijing-Tianjin-Hebei “3+N” Alliance have successively included surgical staplers in their centralized procurement programs. Leveraging these multi-provincial alliances and provincial-level centralized procurement initiatives, the prices of surgical staplers have declined nationwide, significantly reducing the medical financial burden on patients. This has also accelerated the substitution of imported products with domestically manufactured ones, driving the industry into a transitional period of high-quality development.

In 2026, a new round of centralized procurement for surgical staplers kicked off, with the Beijing-Tianjin-Hebei Alliance sounding the charge in April. Unlike previous rounds, the procurement rules for surgical staplers have been continuously iterated and refined through multiple rounds and alliances, gradually maturing. Meanwhile, the national principle of “anti-involution” has further optimized the underlying logic of centralized procurement, introducing new directional guidance for this latest round and providing broader development opportunities for innovative enterprises with core competitiveness.

What changes will occur in the new round of volume-based procurement? How will it affect the market landscape? Which types of enterprises will benefit more? VCBeat will provide an in-depth analysis below.

A Review of the Centralized Procurement Process for Surgical Staplers: Through Multiple Rounds of Practice, the Procurement Rules Have Been Continuously Refined.

From 2020 to 2021, Hunan, Jiangsu, Shanxi, and Fujian provinces all launched provincial-level centralized procurement of surgical staplers. The procurement rules categorized products into major groups such as endoscopic staplers, circular staplers, hemorrhoid staplers, and open linear staplers, and grouped them by brand based on prior-year sales volume or procurement quantity within the province.

Under such rules, international brands such as Medtronic and Johnson & Johnson hold a distinct advantage due to their early market entry and higher market share. In contrast, domestic brands, having launched their products more recently and holding a lower market share, find that some of their highly valuable innovative products are allocated limited procurement volumes.

Subsequently, the centralized procurement and follow-up procurement initiatives for staplers under the Beijing-Tianjin-Hebei “3+N” Alliance explored distinguishing procurement units by registration certificate, with each procurement unit encompassing all specifications and models. The Chongqing-Guizhou-Yunnan-Henan Alliance explored classification based on product parameters (such as staple material, formed staple height, and device body length)……

These volume-based procurement initiatives have driven down the overall price of surgical staplers, but the rule-oriented approach of “awarding bids to the lowest bidder” has led to a certain degree of “bad money driving out good.” More than 100 newly established surgical stapler companies, despite lacking technological expertise and quality accumulation, have seized significant market share by leveraging the opportunities presented by volume-based procurement. Meanwhile, some mature companies have focused solely on compressing product costs, reducing investments in technological innovation and new product development.

Furthermore, most previous volume-based procurement (VBP) rules did not differentiate between the regulatory classifications (Class II and Class III) of surgical stapler registration certificates, although this distinction is crucial for clinical safety and industry regulatory compliance. Taking laparoscopic surgical staplers as an example, Class II devices are indicated for the resection, transection, and anastomosis of lung, gastric, and intestinal tissues in open or laparoscopic procedures and must not be used for vascular transection. In contrast, Class III devices expand the scope of clinical application to include organs such as the liver, gallbladder, and pancreas, as well as blood vessels, on top of the indications covered by Class II devices. These clinical scenarios entail a higher risk level than those associated with Class II staplers.

National medical device regulatory regulations explicitly stipulate that healthcare institutions shall not use medical devices beyond their approved indications. However, previous centralized procurement rules did not differentiate between Class II and Class III products, resulting in a situation where many hospitals had only selected Class II endoscopic staplers in their procurement lists. Consequently, physicians were compelled to use Class II endoscopic staplers off-label. This reality underscores the rationale for incorporating the regulatory classification of product registration certificates into group categorization considerations in the design of new centralized procurement rules.

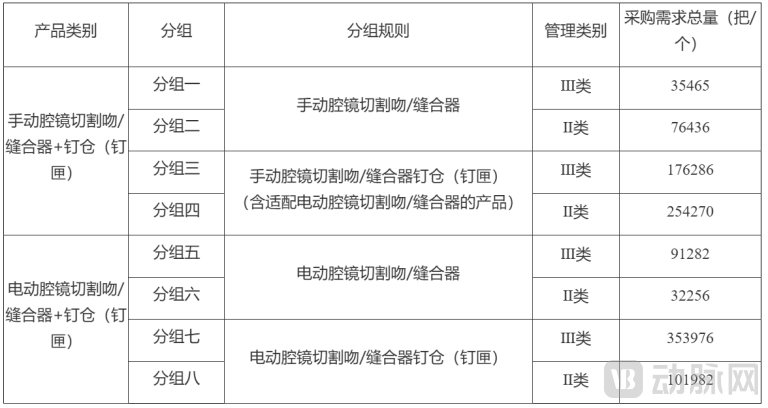

Following multiple rounds of exploration and practice by various alliances, the Chongqing 8-Province Alliance (actually comprising 10 regions) proposed more mature and reasonable grouping rules for the centralized procurement of surgical staplers in 2025: products were divided into eight groups based on “product registration certificate classification (Class II/Class III) + power output method (electric/manual).” This grouping approach not only addresses the safety regulatory requirements associated with registration certificate categories but also accounts for the technical differences between electric and manual surgical staplers. According to the declared procurement volumes, the procurement volume for electric surgical staplers exceeded that of manual ones, and Class III devices had higher procurement volumes than Class II devices.

(Grouping of Staplers in the Chongqing Alliance Centralized Procurement)

In addition to the iterative optimization of grouping methods, the selection and allocation rules for volume-based procurement (VBP) are also evolving. Previously, VBP primarily adhered to a “lowest-price-only” approach. However, after the National Healthcare Security Administration proposed the VBP principles of “stabilizing clinical practice, ensuring quality, preventing bid rigging, and curbing cutthroat competition” in July 2025, VBP will place greater emphasis on the clinical value, product quality, and health economic value of medical products.

For example, in the most recent round of renewed centralized procurement for coronary stents, the winning bid prices of companies such as Blue Sail Medical, Lepu Medical, and MicroPort Medical increased to varying degrees compared with the initial centralized procurement, with Blue Sail Medical’s quoted price rising by more than 75%. This has allowed selected enterprises to secure reasonable profit margins while enabling greater investment in technological upgrades and product innovation, thereby fostering a virtuous cycle of “centralized procurement empowering innovation, and innovation feeding back into clinical practice.” This logic will similarly apply to the new round of centralized procurement for surgical staplers, creating a more favorable development environment for companies with core innovative capabilities.

Overall, the grouping methodology for the new round of centralized procurement of surgical staplers is likely to reference the rules established by the Chongqing 8-Province Alliance, categorizing products based on “product registration certificate management class + power output method.” The selection criteria are expected to take into account comprehensive factors such as clinical value, quality level, and health economics.

In recent years, the domestic surgical stapler industry in China has experienced rapid development: open surgical staplers have achieved import substitution, domestic brands of endoscopic staplers are now competitive with foreign giants such as Johnson & Johnson and Medtronic, and motorized staplers are accelerating their localization rate by leveraging the opportunities presented by centralized volume-based procurement.

Amid industry development, some companies have grown by riding the trend, while others have missed opportunities. ESM, once the leading domestic player in laparoscopic staplers, missed out on the developmental dividends of regional centralized procurement due to the delayed approval of its electric stapler products.

Stripped of Its Past Glory, Can This “Former King” Break Through the New Round of Centralized Procurement to Reclaim Its Industry Throne?

Building the Leader of China's Medical Device Industry

In 2001, Nie Honglin, founder of ESM (EziSurg Medical), joined MicroPort Medical. He led the R&D team to achieve domestic development and manufacturing of endovascular stent grafts for the aorta, as well as 3D electroanatomic mapping and ablation systems for cardiac electrophysiology. His efforts paved the way for the establishment and growth of China’s first leading medical device companies, laying a solid foundation for what are now MicroPort Endovastec and MicroPort EP MedTech.

After years of deep engagement in the medical industry, he observed that the domestic market for minimally invasive oncologic surgery remained monopolized by international brands, with very low adoption rates of such procedures in China. The high cost of imported products continued to be a key barrier hindering the widespread adoption of minimally invasive techniques. Determined to establish a new high-end Chinese brand in the field of minimally invasive surgery, he founded ESM in 2011.

From its inception, ESM established a clear brand positioning. In an interview years ago, Nie Honglin stated that ESM aims to create reliable, accessible, and affordable comprehensive minimally invasive surgical solutions through technological innovation and premium quality, striving to become a leading enterprise in China’s medical device industry and a globally influential high-end brand.

This philosophy has ingrained technological innovation and premium quality into the corporate DNA of ESM. To develop high-end products that meet clinical needs, Nie Honglin led his team in visiting dozens of clinical experts, integrating physicians’ feedback on pain points and practical operational requirements into product design, and conducting repeated validation and adjustments.

For example, Professor Zheng Minhua, Vice President of Shanghai Ruijin Hospital, has reported that internationally standardized laparoscopic staplers typically have a rotation angle of no more than 45 degrees. This limited curvature is insufficient for rectal cancer surgery, often preventing the complete and smooth resection of tumors in some cases of low-lying rectal cancer. To save their lives, some patients must undergo removal of the tumor along with the entire anus.

To address this critical challenge, Nie Honglin led the R&D team to pioneer a unique “flexible joint + dual-ligament” technical solution, diverging from the technological pathways of imported brands. This innovation marked the world’s first increase in the unilateral deflection angle of surgical staplers from 45 degrees to 60 degrees (achieving 120 degrees for bilateral deflection). Compared with the 38–45 degree unilateral deflection angles offered by international brands, ESM’s large-angle laparoscopic stapler significantly enhances accessibility and operational convenience in confined surgical spaces. It broadens the indications for sphincter-preserving surgery in patients with low rectal cancer, enabling more patients to retain their anal sphincter during the procedure.

Through in-depth engagement with numerous leading clinical experts and the successful execution of many medical-engineering collaborative projects, ESM has developed profound expertise and insights into its stapler and ultrasonic scalpel products. The company has achieved comprehensive technological breakthroughs, laying a solid foundation for its stapler and ultrasonic scalpel products to later receive the First Prize for Provincial Scientific and Technological Progress.

Driven by multiple innovations, ESM’s stapler products are highly competitive. In professional comparative tests conducted by SGS in Europe, ESM’s ultra-large-angle laparoscopic stapler demonstrated a 10% higher suture strength than imported products, with a titanium staple malformation rate of less than 30% that of imported counterparts, securing a decisive advantage.

These distinct advantages have led to widespread clinical recognition and adoption of ESM’s surgical staplers, driving a broader shift in physicians’ perception of domestic stapler brands. Initially, domestically produced staplers were primarily used in general surgery, while thoracic surgeons remained hesitant to employ them in higher-risk thoracic procedures. Against this backdrop, ESM, as a representative domestic brand, leveraged its innovative product features and reliable stapling quality to achieve a breakthrough in thoracic surgery first, gaining endorsement from numerous leading thoracic surgery experts. This subsequently paved the way for the expanded application of other domestic staplers in thoracic surgery.

Leveraging its innovative advantages, ESM’s endoscopic stapler products have consistently ranked first in market share among domestically produced staplers since their launch. At their peak, these products were adopted by over 1,400 hospitals across China, with more than 40% being key Grade A tertiary hospitals.

Beyond the domestic market, ESM’s stapler product series has been exported to 90 countries and regions worldwide after obtaining international certifications such as U.S. FDA clearance, EU CE marking, and UK MHRA approval. These products have entered many mainstream hospitals globally and gained recognition. In 2025, ESM further won the bid for the largest national stapler centralized procurement project in the United States and signed a supplier cooperation agreement with Vizient, Inc., the largest group purchasing organization (GPO) in the U.S., marking its entry into the mainstream American hospital market.

Notably, in the past two years, international giants have frequently initiated patent litigation against Chinese stapler brands. Against this backdrop, ESM has continued to make steady progress in mainstream European and American markets. This success is attributed to ESM’s adoption of an independent innovation pathway, which differs from the “imitation–high-level imitation–partial innovation” model pursued by most enterprises.Patent data shows that within five years of its founding, ESM filed 71 patent applications, including 12 Chinese invention patents and 48 international invention patents.To date, the total number of patents filed has reached 380, including 72 Chinese invention patents and 176 international invention patents, demonstrating the high value of these invention patents.

In addition to technological innovation and product breakthroughs, ESM has taken the lead among domestic brands in promoting the widespread adoption of minimally invasive techniques in China. In 2017, ESM invested tens of millions of RMB to support Health News, the official newspaper of the former National Health and Family Planning Commission, in launching the “321 Project—Program for Promoting Appropriate Technologies for Cancer Prevention and Treatment in Prefecture- and County-Level Hospitals.” The project aimed to establish 20 clinical demonstration and training bases in at least 10 provinces within three years and to popularize minimally invasive surgical techniques for cancer treatment in at least 100 prefecture- and county-level hospitals across China. The initiative achieved significant social impact, not only accelerating the dissemination of minimally invasive surgical technologies but also driving a substantial increase in the utilization of the company’s products. Following ESM’s example, several other domestic brands have launched promotion and popularization efforts of varying scales in different regions.

In 2021, the volume of minimally invasive surgeries in China increased from 5.8 million in 2015 to 15.7 million, marking a substantial rise in the adoption of minimally invasive surgical techniques domestically. This growth underscores the value of ESM’s exemplary role in fulfilling its corporate social responsibility, aligning with its industry standing as a leading domestic brand.

Missing Out on Short-Term Growth Dividends, Proactively Embracing the New Round of Centralized Procurement

From an industry development perspective, the previous round of alliance- and provincial-level centralized procurement for staplers has significantly driven the growth of domestically produced electric endoscopic staplers. According to Frost & Sullivan data, from 2023 to 2025, although the market size of manual endoscopic staplers in China increased from RMB 3.53 billion to RMB 3.66 billion, the compound annual growth rate (CAGR) was only 1.82%; in contrast, the market size of electric endoscopic staplers grew from RMB 3.87 billion to RMB 5.88 billion, with a CAGR reaching 22.93%.

(Changes in the Market Size of Endoscopic Staplers in China, Data Source: Frost & Sullivan)

However, as a leading enterprise in the domestic stapler field, ESM did not benefit from the short-term development dividends of the previous phase.

In the previous round of centralized procurement, ESM actively responded to the policy by proactively reducing its bid price for manual staplers by 80% in accordance with the “price-for-volume” mechanism. The company aimed to capture greater market share, serve more patients, and support healthcare insurance cost containment through innovative technology, premium quality, and lower prices. This significant price reduction positioned ESM as one of the high-end brands with the lowest selected product prices among the top ten industry players at that time.

However, the uncertainty introduced by centralized procurement rules, coupled with inconsistent enforcement across different regions, has plunged ESM’s domestic business into a predicament of continuous declines in both sales volume and revenue.

On the other hand, the previous round of centralized procurement officially included electric staplers within its scope. However, ESM’s approval for the registration certificate of its electric staplers failed to keep pace with the procurement timeline, causing it to completely miss out on the previous round. Understanding the underlying reasons reveals a regrettable mismatch between industrial aspirations and centralized procurement policies, as ESM had previously devoted its primary R&D resources to state-commissioned scientific research tasks.

Since 2015, ESM has responded to the call of industry regulatory authorities by suspending R&D projects for single-use electric staplers and officially launching R&D initiatives to transition high-value consumables—such as electric staplers and ultrasonic hemostatic scalpels, which were priced excessively high at the time—from single-use to reusable formats. This effort aims to reduce the per-procedure costs and medical burden associated with high-value consumables like staplers and ultrasonic scalpels.

Unexpectedly, this reusable electric stapler product—characterized by a lack of industry standards, testing methods, and registration review guidelines at the time, yet filled with technical challenges and innovations—ultimately obtained its registration certificate in 2021 through the priority review pathway after a six-year process. However, it was then discovered that the volume-based procurement (VBP) rules favored disposable electric staplers. This misjudgment of the divergent policy orientations among different government departments planted a significant risk for ESM’s development in the first round of VBP.

Although ESM urgently initiated the development of disposable electric staplers as soon as it anticipated the policy direction of centralized procurement, it still missed the previous round of procurement cycles. Consequently, it failed to secure any market share in the electric stapler segment, which accounts for more than 50% of the total laparoscopic stapler market.

As can be seen, ESM failed to benefit from the phased development dividends of the previous round of centralized procurement, whether for manual or electric staplers. The company’s domestic revenue and gross profit margin both declined, while other domestic brands significantly gained market share and achieved substantial performance growth.

It is in such adversity that the resilience of brand development becomes evident. Over the past three years, while corporate brands were overshadowed by the clamor of industry trends, ESM has remained steadfast in its original entrepreneurial mission. Despite sustained losses, the company has upheld its premium brand positioning and commitment to high-quality standards, invested in technological innovation, continuously launched new products, and made significant strides into the global market.

For example, following the implementation of the previous round of centralized procurement, ESM successively launched a comprehensive product portfolio of Class II and Class III manual and powered staplers. It simultaneously introduced two technical solutions: cartridge versions with integrated knives and staple-only versions without knives, thereby better meeting diverse clinical application needs. To date, ESM has become one of the Chinese domestic stapler brands with the most complete portfolio of laparoscopic stapler products.

In addition to its product portfolio, ESM has been continuously strengthening its global expansion and making steady progress. From 2023 to 2025, ESM filed nearly 80 new patent applications, including 20 Chinese invention patents and more than 20 international invention patents. The company entered nearly 30 new country and regional markets and established a global platform for exchange and collaboration among leading experts in minimally invasive surgery. By implementing the “bringing in and going out” strategy, ESM supports cross-border exchanges and cooperation between Chinese and foreign experts, promotes the achievements and culture of minimally invasive surgical techniques, and enhances the global influence of China’s minimally invasive surgical medicine.

Today, ESM’s minimally invasive surgical products, represented by its surgical staplers, have been successfully sold to more than 90 countries and regions worldwide. They have entered the mainstream hospital markets in developed countries in Europe and America, gained recognition from numerous international leading experts, and continue to accelerate their growth in the global market.

Meanwhile, Nie Honglin, founder of ESM, has consistently adhered to a long-termist philosophy, personally steering the company’s strategic direction, staying true to its entrepreneurial origins, and remaining committed to the corporate vision of “building a high-end brand with significant global influence.” In 2025, ESM sequentially initiated reforms of its international and domestic marketing organizations and, for the first time, established the position of full-time CEO, appointing Hu Hai, a renowned leader in the medical industry, to oversee corporate operations and strategic implementation.

Hu Hai has dedicated 30 years to the healthcare industry, having held positions at multinational healthcare giants such as GE Healthcare, Boston Scientific, Johnson & Johnson Medical, and Smith & Nephew. He previously served as Vice President of Johnson & Johnson China and as President and Executive Director of Smith & Nephew China. With extensive business management experience, he has repeatedly led teams in participating in national and provincial centralized tendering and volume-based procurement programs.

After departing from a multinational healthcare giant, Hu Hai, an industry leader who has already “scaled Mount Tai,” set his personal career goal to join and lead a leading Chinese enterprise with the greatest innovation potential, aiming to “scale Mount Tai” once again by steadily growing it into a global high-end brand. ESM’s vision of building a leading Chinese brand and a global high-end brand aligns closely with Hu Hai’s professional aspirations. This mutual commitment, grounded in a shared vision, is poised to inject new, robust momentum into ESM’s corporate development, particularly contributing to the success of its next round of volume-based procurement.

Following setbacks in the initial round of centralized procurement, ESM’s persistence in technological innovation and management transformation has laid a solid foundation in advance for success in the new round of centralized procurement.

New Round of Centralized Procurement: Can ESM Make a Triumphant Comeback?

With the Beijing-Tianjin-Hebei Alliance opening information maintenance for endoscopic cutting stapler consumables in April, it signals the official commencement of a new round of centralized procurement in 2026.

In the face of a new round of centralized procurement opportunities and evolving policy trends, whether ESM can make a triumphant comeback warrants in-depth analysis.

First, if the rules for the new round of centralized procurement of staplers in 2026 draw on the grouping experience from the Chongqing centralized procurement, ESM’s product portfolio is expected to align with all groups, meeting the diverse clinical needs of each category. Such a comprehensive product lineup is rare, with only a handful of companies among nearly 200 domestic stapler manufacturers in China possessing it, positioning ESM to gain a significant advantage in distributor recruitment and volume-based procurement negotiations.

Secondly, the new round of centralized procurement policies tends to favor value-based payment, prioritizing products with greater clinical value, product quality, and health economic value. ESM’s independent innovations have endowed its stapler products with excellent operability, safety, and reliability in clinical practice, earning a strong reputation among mainstream hospitals and physicians across China. Many leading experts consider ESM’s staplers to be a rare domestic brand that can serve as a reliable and reassuring substitute for imported products, aligning closely with the requirements of the new centralized procurement framework.

For example, ESM’s globally pioneering “60° large-angle” design not only highlights advantages in clinical accessibility but also easily overcomes pelvic space constraints during low rectal cancer surgery. It enables perpendicular transection of the deep rectum, thereby increasing the sphincter preservation rate, significantly improving patients’ postoperative quality of life, and delivering substantial clinical benefits.

In thoracic surgery, ESM’s unique patented “detachable bird-beak” design enables smooth insertion into narrow tissue spaces when the bird-beak is attached, effectively reducing the risk of tearing during vessel dissection. After removing the bird-beak, surgeons can safely perform anastomoses on thick tissues such as the lungs and stomach without concern for bird-beak-induced injury to healthy tissue, offering both clinical benefits and health economic value.

ESM’s proprietary “curved cartridge + uniform-height staple” design achieves superior titanium staple formation rates and reduces post-anastomosis tissue edema and the risk of staple line dehiscence. Compared with traditional flat cartridges, the curved surface of the cartridge more efficiently expels interstitial fluid and adipose tissue during the pre-compression phase, ensuring more uniform tissue compression. This not only optimizes conditions for titanium staple formation but also lowers the risks of marginal edema, postoperative staple line dehiscence, and anastomotic leakage. By fundamentally enhancing staple line quality and reducing the need for postoperative interventions, this design balances clinical benefits with health economic value.

ESM’s patented composite anvil design optimizes structural rigidity. Combined with an I-beam cartridge assembly, it achieves an optimal balance in tissue compression force. This design effectively mitigates the clinical risks associated with imported brands: excessive compression force that may cause tissue crush injury, and insufficient compression force that may lead to tissue slippage and poor staple formation. By significantly reducing tissue slippage and incorporating a full-effect staple-guiding surface on the anvil, the system substantially improves the rate of proper titanium staple formation.

It also features an ultra-light electrosurgical device weighing approximately 600g, which is 13%-62.5% lighter than mainstream brands, reducing hand fatigue for the operator; the firing vibration in a bent state is only 0.25 degrees, compared to up to 5 degrees of vibration in imported brands, significantly reducing vascular traction and tearing.WaitRisk.

Overall, ESM’s numerous technological innovations, which are closely aligned with clinical needs, can provide physicians and patients with enhanced safety and efficacy, reduced risks, and more significant health economic value. Coupled with its consistently leading reputation for quality, the company is well-positioned to better meet clinical and medical insurance requirements in the new volume-based procurement program.

Finally, which types of enterprises are more likely to emerge victorious in the new round of volume-based procurement (VBP)? We believe that companies with mature and long-term corporate brand strategies, marketing strategies, innovation capabilities, and quality assurance systems; those that effectively leverage resources from medical-engineering collaboration; and those committed to continuously fulfilling social responsibilities and supporting the advancement, promotion, and widespread adoption of medical technologies in China are more likely to gain support from VBP policies and secure the endorsement of hospital decision-makers.

In recent years, centralized volume-based procurement (VBP) policies have significantly reshaped the market landscape in the field of minimally invasive surgery. Prior to VBP implementation, there were fewer than 30 domestic brands in the surgical stapler segment. During the first round of VBP, more than 170 domestic surgical stapler brands were successively selected for inclusion. A considerable number of these brands have not yet established independent R&D and manufacturing capabilities; they primarily conduct related business through original equipment manufacturing (OEM) arrangements and lack autonomous quality control capabilities.

Amid this round of centralized procurement and industry reshuffling, some companies rushed to enter the market, while some founders exited through mergers and acquisitions. Certain enterprises abandoned in-house R&D, and others became embroiled in patent litigation battles. Nearly 80% of companies are struggling around the RMB 30 million revenue mark, with slim margins or operating at a loss. No widely recognized new industry leader has emerged, resulting in an overall landscape characterized by fragmentation, small scale, and disorganization.

Amidst the turmoil, can ESM—which missed out on the initial round of opportunities but has remained steadfast in its global vision, commitment to innovation and quality, and assumption of corporate social responsibility—and which once proclaimed its ambition to “become a leading enterprise in China’s medical device industry and build a high-end brand with significant global influence”—make a triumphant comeback in the new round of centralized procurement competition? Only time will tell.

It is worth noting that although ESM’s preparations have been relatively comprehensive, the company still faces uncertainties stemming from various external challenges in the new round of centralized procurement:

1. Against the backdrop of anti-corruption efforts in the healthcare industry, will hospitals adopt a more cautious approach to volume reporting by excluding non-hospital brands and maintaining the existing brand landscape within their institutions, thereby effectively undermining the priority principles of clinical value, product quality, and health economic value promoted in this round of centralized procurement?

2. There are numerous stapler manufacturers (over 200). Although market dynamics dictate that consolidation toward leading enterprises is inevitable, the many companies facing elimination are unlikely to exit willingly. Consequently, many will treat the hospital volume declaration phase as a make-or-break battle, engaging in fierce competition with unpredictable outcomes for each account. Post-selection delivery obligations, however, constitute a separate matter.

3. Although various sectors have offered numerous interpretations and expectations regarding the rules for the new round of centralized procurement, significant uncertainty remains until the official release.