Global Top 3 Synbio Player Leadsynbio Files for Hong Kong IPO

Leadsynbio

Pharmaceutical raw materials, intermediates R&D and production

In February 2026, the latest batch of A1 listing applications disclosed by the Hong Kong Stock Exchange included a synthetic biology company named “Suzhou Leadsynbio Technology Co., Ltd.” (hereinafter referred to as “Leadsynbio”), with Huatai Financial Holdings (Hong Kong) serving as the exclusive sponsor.

Founded in 2015, the company had ranked among the global leaders in three niche segments—D-ethyl ester (a key intermediate of florfenicol), florfenicol, and NMN—as of September 30, 2025. Meanwhile, it recorded net losses during the track record period, with a gross profit margin of −10.8% in 2024.

Why is a Chinese synthetic biology company that has already achieved global leadership in multiple niche categories experiencing sustained losses? What are its motivations for filing an A1 application with the Hong Kong Stock Exchange at this particular moment? Among listed synthetic biology leaders on China’s A-share market, such as Cathay Biotech and Huaheng Biotechnology, what industrial position does Leadsynbio occupy? Furthermore, how significant is the window of opportunity created for Chinese players like Leadsynbio by the recent trend of century-old Western chemical giants, such as BASF and DSM-Firmenich, actively divesting their vitamins and nutrition businesses?

This article systematically analyzes Leadsynbio’s A1 prospectus for its Hong Kong IPO and public data from comparable companies across six dimensions: market landscape, product portfolio, financial fundamentals, production capacity logic, competitive positioning, and risks and key observations.

01

What Is Happening to the Global Landscape of Synthetic Biology?

Over the past decade, the synthetic biology industry has undergone a complete cycle shift from “story-driven” narratives to “industrial realization.” Early U.S. companies represented by Amyris and Solazyme successively went bankrupt or were divested in recent years, as they failed to cross the “valley of death” between the laboratory and factory scale-up. In contrast, Chinese synthetic biology companies have gradually established viable industrialization pathways since 2017, with firms such as Cathay Biotech (listed on the STAR Market in 2020), Huaheng Biotechnology (2021), and Bloomage Biotechnology (2019) sequentially entering the capital markets.

According to Frost & Sullivan data, the global synthetic biology market was valued at approximately USD 21.5 billion in 2024 and is projected to expand to USD 99.6 billion by 2030, surpassing USD 212.9 billion by 2035. The compound annual growth rate (CAGR) is expected to be 28.7% from 2024 to 2030, and 16.4% from 2030 to 2035. This growth rate is relatively rare among subsectors of the manufacturing industry.

■ DriversSynthetic BiologyThree Forces Driving Industry Growth

First is the leap in technological maturity. The successive maturation of AI protein structure prediction tools such as AlphaFold (2018) and ESMFold (2022), coupled with the expansion of automated high-throughput screening platforms from 96-well to 384-well and even 1536-well formats, along with the decline in gene sequencing costs at a pace faster than Moore’s Law, has compressed the DBTL (Design-Build-Test-Learn) R&D cycle in synthetic biology from months to weeks. Theoretically, fermentable molecules are being transformed into stable manufacturing processes in industrial facilities at an accelerating rate.

Next is the green transformation of downstream demand. Policy constraints such as the EU’s REACH regulation, the U.S. BIOSECURE Act, and China’s “Dual Carbon” strategy are driving the migration of traditionally chemically synthesized intermediates and end products toward biomanufacturing. In sectors including active pharmaceutical ingredients (APIs), vitamins, flavors, fragrances, and bio-based materials, “green substitution” has evolved from an optional choice into a critical compliance imperative for survival.

Most noteworthy is the proactive retreat of European and American giants. In February 2024, DSM-Firmenich announced the spin-off of its Animal Nutrition & Health (ANH) business, including vitamins and carotenoids; by February 2026, DSM-Firmenich finalized the divestiture agreement for the ANH business. During the same period, BASF continued to scale back its Nutrition & Care division, with full-year 2024 revenue reaching EUR 6.43 billion, a 6.7% decline from EUR 6.89 billion in 2023. The exit of these two century-old European and American chemical conglomerates has freed up substantial supply-side market share for Chinese synthetic biology companies—particularly in three niche segments: D-series vitamins and their intermediates, high-value-added enzyme preparations, and carotenoids, where structural industrial transfer is most evident.

■ Differentiated Positioning of the Chinese Team’s Sector Map and Leadsynbio

Synthetic biology-related companies listed on China’s A-share market have formed several distinct “vertical camps”: Cathay Biotech (688065.SH) focuses on long-chain dicarboxylic acids and bio-based polyamides, reporting revenue of RMB 2.958 billion, a gross margin of 31.25%, and net profit of RMB 489 million in 2024; Huaheng Biotechnology (688639.SH) has established its competitive moat through amino acid (valine, alanine, inositol) fermentation processes, with 2024 revenue of RMB 2.178 billion and a gross margin of 28.87%; Bloomage Biotech (688363.SH) has expanded from hyaluronic acid into cosmetics and functional foods. These three companies all exemplify the typical “vertical champion” path.

Leadsynbio’s differentiated positioning lies in its alternative approach: leveraging a single DBTL engineering platform to expand in parallel into three relatively independent downstream markets—active pharmaceutical ingredients (APIs) and intermediates, nutritional products, and animal health products—thereby creating a “horizontal multi-product” portfolio. The advantage of this strategy is strong resilience to economic cycles, as a price collapse in any single product category is insufficient to undermine the overall business. The trade-off, however, is weaker economies of scale for individual products, since capacity expansion for each category requires separate capital investment.

02

How Do 14 Commercialized Products Secure a Top-Tier Global Market Share?

As of September 30, 2025, Leadsynbio had achieved industrial-scale production and commercial sales for a total of 14 products. Among these, L-glufosinate was commercialized by the company’s associate, Hunan Lier Biotechnology (established in 2016), using Leadsynbio’s proprietary process. The prospectus explicitly discloses that Leadsynbio possesses “breakthrough original process routes” for five products: D-ethyl ester, L-left, R-HPBE, DHEA, and L-glufosinate. The term “breakthrough” refers to process routes that do not follow existing market solutions but are instead novel synthetic pathways independently designed by the company and successfully industrialized for the first time.

In Leadsynbio’s product matrix, three categories underpin the company’s global market position.

■ D-ethyl ester: Replaces the traditional process used for decades

D-ethyl ester isFlorfenicolkey intermediate. As of September 30, 2025, Leadsynbio held a 44.5% share of the global D-ethyl ester market, ranking first worldwide, followed by the second and third largest players with shares of 42.5% and 13.0%, respectively. The prospectus explicitly states, “Our proprietary process for D-ethyl ester has replaced the traditional manufacturing methods that have been used in the market for decades.” Building on this core product, the company has extended its operations upstream to produce the intermediate p-(methylsulfonyl)benzaldehyde and downstream to manufacture the active pharmaceutical ingredients (APIs) florfenicol and thiamphenicol, thereby establishing a complete vertical integration chain.

■ Florfenicol: Second in the world

In a specific niche market related to florfenicol, Leadsynbio holds a 24.5% global share, ranking second worldwide. The market size was approximately RMB 17.83 billion in 2024 and is projected to reach RMB 54 billion by 2035, representing a compound annual growth rate (CAGR) of 10.6%. This product category, together with D-ethyl ester, constitutes the most important source of cash flow for Leadsynbio.

■ NMN: Ranks Among the Top Two Globally

NMN (β-nicotinamide mononucleotide) has been the most prominent molecule in the global anti-aging sector over the past five years. Leadsynbio ranks second with an 11.4% global market share. The global NMN market was valued at RMB 2.71 billion in 2024 and is projected to reach RMB 25.45 billion by 2035, representing a compound annual growth rate (CAGR) of 22.6%—making it the fastest-growing segment within Leadsynbio’s product portfolio. Notably, Leadsynbio has obtained relevant FDA filings and EFSA PC1537 authorization for its NMN products, positioning it as one of the few Chinese synthetic biology companies with simultaneous access to both the U.S. and European mainstream markets.

■ Core Pipeline Products: 14 Commercialized and 7 in R&D Reserve

In addition to the three star products mentioned above, Leadsynbio also has commercialized products in several niche categories, including 25-hydroxyvitamin D3 (animal health, with a global market share of 2.2%), L-glufosinate (herbicide, commercialized by its joint venture), thiamphenicol (antibiotic API), R-HPBE and L-norvaline (chiral intermediates), DHEA enzyme and UDCA enzyme (enzyme preparations), and NAD/NADP (enzyme cofactors). Its R&D pipeline further covers seven pre-commercial products, such as NR, Reb M (natural sugar substitute), selenomethionine, β-carotene, canthaxanthin, lutein, lycopene, and astaxanthin. The combination of 14 commercialized products and 7 pipeline products forms a portfolio of 21 products, placing Leadsynbio among the top tier in terms of scale within China’s synthetic biology industry.

According to Frost & Sullivan, Leadsynbio is “one of the very few companies worldwide capable of translating multiple proprietary process routes from laboratory scale to industrial production.” Such a distinction is rare in the synthetic biology industry—while laboratory breakthroughs are abundant, only a handful of companies have successfully crossed the threshold of “scaling up to ton-level production.”

03

Why Did a Gross Loss Occur During the Track Record Period?

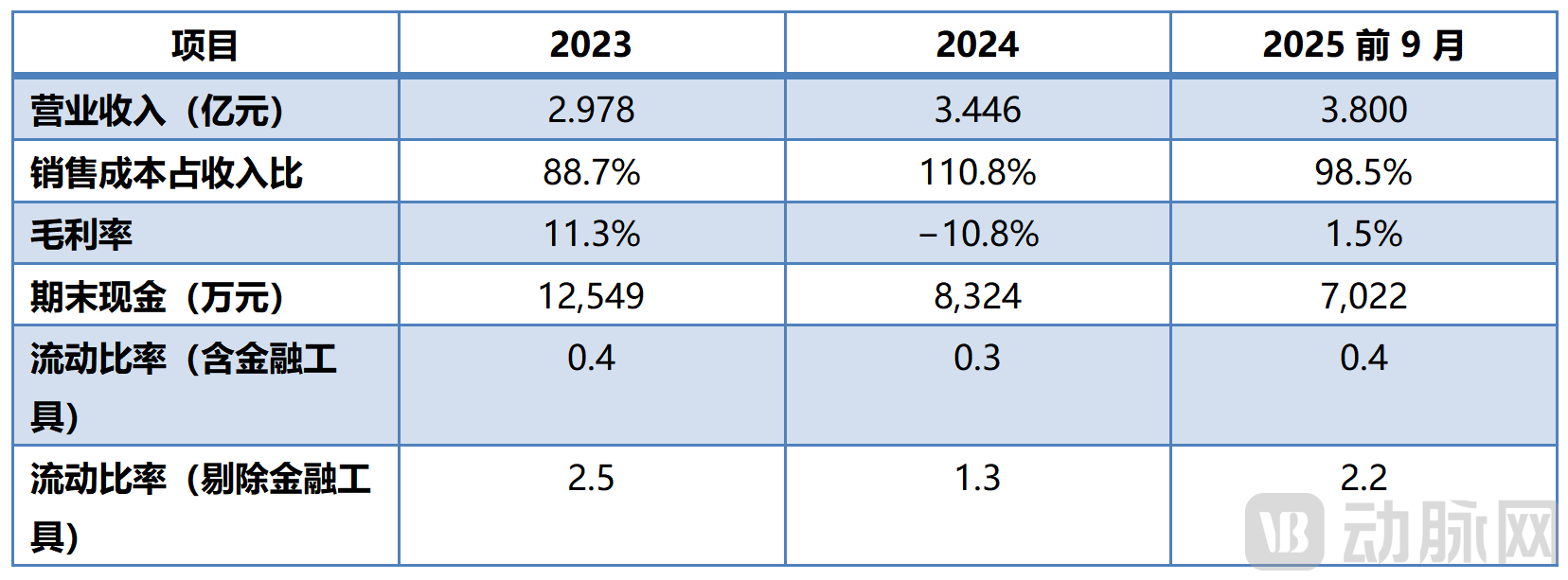

Financial data for the past three years disclosed in the prospectus show that Leadsynbio generated RMB 297.8 million in revenue with a gross margin of 11.3% in 2023; RMB 344.6 million in revenue with a gross margin of −10.8% in 2024; and RMB 380 million in revenue in the first nine months of 2025 (surpassing the full-year total for 2024), with the gross margin recovering to 1.5%.

Figure 1: Key Financial Data of Leadsynbio Over the Past Three Years (Source: HKEX A1 Prospectus)

By analyzing the facts disclosed in the prospectus, the gross loss in 2024 was primarily attributable to the combined effect of three factors:

First, the impact of the capacity expansion cycle. In July 2024, the Anhui production base suspended operations to facilitate the project expanding annual capacity from 900 tons to 2,625 tons, resulting in an annual utilization rate of only 46.1% for the Anhui facility.

Second, there is the upstream-downstream coupling transmission between the two production bases. The raw material D-ethyl ester for florfenicol produced at the Anhui base is supplied by the Hunan base. During the production halt in Anhui, the capacity for D-ethyl ester in Hunan was also underutilized. As a result, Hunan’s utilization rate dropped from 87.2% in 2023 to 45.9% in 2024. With both bases operating below capacity simultaneously, unit fixed costs were amortized at elevated levels.

Third is the price collapse in the nutritional supplements sector. The unit price of nutritional supplements fell from RMB 1,052 thousand per ton in 2023 to RMB 471 thousand per ton in 2024, and further declined to RMB 368 thousand per ton in the first nine months of 2025—a cumulative drop of 65% over two years. During the same period, sales volume increased from 10 tons to 116 tons (on an annualized basis), representing more than a tenfold growth. This is a typical manifestation of the synthetic biology-based nutritional supplements sector during the concentrated capacity expansion phase from 2023 to 2024, characterized by simultaneous explosive growth in sales volume and a precipitous drop in unit prices.

By the first nine months of 2025, Anhui’s capacity utilization rate rebounded to 60.5%, while Hunan’s returned to 89.7%. Coupled with sustained growth in active pharmaceutical ingredient (API) sales volumes, the gross profit margin recovered from −10.8% to 1.5%. Based on the company’s current capacity utilization and product mix, if Hunan’s utilization rate stabilizes above 85% in 2026 and the unit price of nutritional products steadies within the range of RMB 350,000–400,000 per ton, there is a high probability that the gross profit margin will return to the 8%–12% level. This represents the most critical metric to monitor over the next 12 months.

Furthermore, the revenue contribution from the top five customers decreased from 67.8% in 2023 to 29.2% in 2024, while the share from the single largest customer dropped from 25.5% to 11.7%, indicating a significant diversification of the customer base. The cost proportion attributable to the top five suppliers declined from 44.4% to 27.5%, reflecting enhanced bargaining power in procurement. Both sets of data serve as positive signals.

04

Why Submit the HKEX A1 Application at This Precise Moment?

To understand why Leadsynbio chose this specific timing to file for an IPO on the Hong Kong Stock Exchange, one must examine its cash position, capacity planning, and capital market windows together.

Leadsynbio currently has RMB 70.22 million in cash on hand. From RMB 294.9 million at the beginning of 2023 to RMB 70.22 million by the end of September 2025, the company experienced a cumulative net cash outflow of RMB 224.7 million over 33 months, with an average monthly burn rate of approximately RMB 6.81 million. At the current pace, the company’s existing cash reserves are projected to last for about 10 more months. The A1 application for its Hong Kong IPO was submitted in February 2026. Under the normal review process for the Main Board of the Hong Kong Stock Exchange, the period from A1 submission to listing typically takes 6 to 9 months, with an expected listing window between August and November 2026. This timeline nearly coincides with the point at which the company’s cash reserves are projected to be exhausted, reflecting a carefully calculated scheduling strategy.

The prospectus discloses that the use of IPO proceeds is divided into three categories: upgrading R&D capabilities, new capacity construction and automation upgrades, and working capital and general corporate purposes. The specific percentage breakdown was redacted as “[compiled]” at the A1 stage and is expected to be disclosed during the PHIP stage.

At the governance structure level, Dr. Xie Xinkai, the founder, directly holds 20.25% of the shares. Together with the three employee stock ownership platforms under his control—Suzhou Hanghui (9.36%), Suzhou Hanghong (4.20%), and Suzhou Hangrong (2.25%)—and his concert party, Gu Shenping (0.09%), he collectively exercises 36.14% of the voting rights. The Board of Directors comprises eight members (including three executive directors, one of whom is based in Hong Kong; two non-executive directors; and three independent non-executive directors), which meets the standard requirements of the Main Board Listing Rules of the Hong Kong Stock Exchange.

05

Where does Leadsynbio stand among Cathay Biotech, Huaheng Biotechnology, BASF, and DSM?

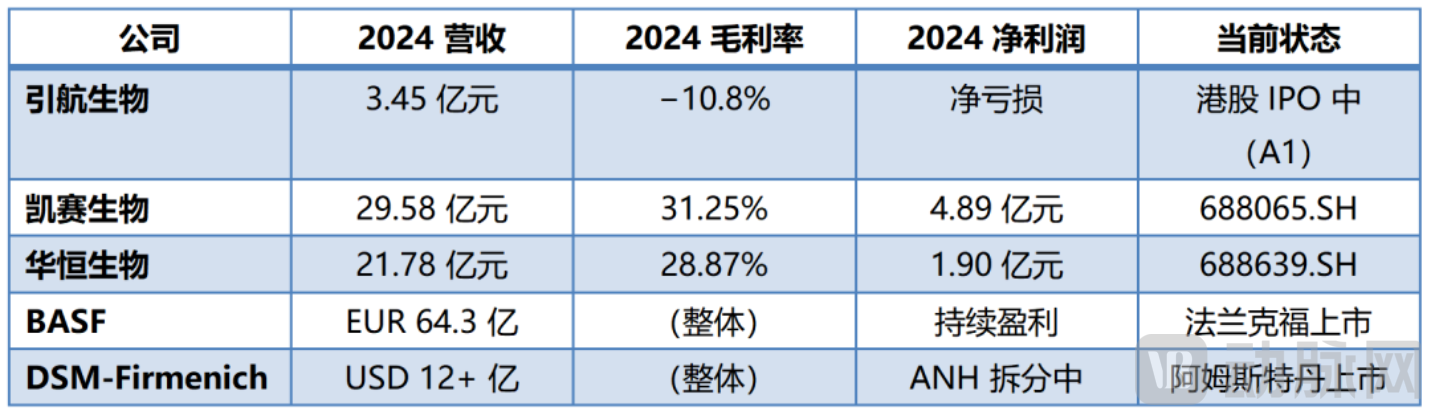

Figure 2: Comparison of Core Financial Data Between Leadsynbio and Comparable Companies (Source: 2024 Annual Reports of Each Company)

Cathay Biotech offers a “proven” model: founded in 1997, listed in 2020, and achieving sustained profitability only in 2023, it took approximately 23 years from inception to the full commercialization of its long-chain dicarboxylic acid series. In 2024, Cathay Biotech reported revenue of RMB 2.958 billion (a year-on-year increase of 39.91%), a gross profit margin of 31.25%, net profit attributable to shareholders of RMB 489 million (a year-on-year increase of 33.41%), and an asset-liability ratio of merely 10.75%. In 2025, revenue rose to RMB 3.295 billion, with a gross profit margin of 34.22%—this is what one would expect from a synthetic biology company that has become the undisputed global leader in a core product category and entered a phase of sustained profitability driven by economies of scale.

Huaheng Biology offers a case study in “cyclical fluctuations.” In 2024, Huaheng reported operating revenue of RMB 2.178 billion (a year-on-year increase of 12.37%), but its gross profit margin declined from 44.46% to 28.87% (a drop of 15.59 percentage points), while net profit attributable to shareholders amounted to RMB 190 million (a year-on-year decrease of 57.80%). The situation further weakened in 2025, with the gross profit margin falling to 21.27%. Even leading companies in synthetic biology that have achieved scale are not immune to the severe impact of product price cycles. This is a reality that Leadsynbio must confront: even ranking among the global leaders in a specific product category does not guarantee escape from cyclical dynamics.

The story of BASF and DSM-Firmenich represents the other side of the coin. For a century, vitamins have been the core profit source for DSM, the Dutch company, which was among the first in the world to industrialize the production of vitamin B, vitamin D, and vitamin E. Its decision to divest its Animal Nutrition & Health (ANH) business essentially acknowledges its inability to compete on cost in this category.Chinese EnterprisesBASF’s continued contraction of its Nutrition & Care division follows the same logic: for bulk nutritional ingredients such as vitamins and carotenoids, the cost structures in Europe and the United States can no longer compete with Chinese players. The product segments being exited by these two century-old European and American chemical giants are precisely the core product lines of Leadsynbio.

Connecting these three comparisons, Leadsynbio’s position on the global landscape can be described as follows: In terms of product market share, it has already achieved a standing comparable to what Cathay Biotech and Huaheng Biotechnology have attained in their respective niche categories; however, in terms of commercial scale and profitability, it remains at a stage similar to where Cathay Biotech was ten years ago and Huaheng Biotechnology was five years ago. From the perspective of company establishment, Cathay Biotech has been operating for 23 years, Huaheng Biotechnology for 16 years, while Leadsynbio is currently in its 11th year. This time gap represents the source of Leadsynbio’s mid-to-long-term growth potential.

06

Which indicators are worth continuous monitoring?

The five major risk factors listed in the original prospectus are all real and present:

First, the product portfolio is relatively concentrated, with D-ethyl ester and its derivatives constituting the majority of revenue; price fluctuations in this single category will significantly impact total revenue. Second, end-market demand is changing rapidly, and the collapse in nutritional supplement prices is already a fact that may be replicated by other categories. Third, industry competition is intense, with existing players continuously expanding capacity and new entrants emerging sequentially; the market share vacated by European and American companies may not necessarily be fully captured by Leadsynbio. Fourth, net losses may persist during the performance record period; if the gross margin fails to stabilize within the 8% to 12% range from 2026 to 2027, the company may face continued dilution from financing. Fifth, there is pressure from technological advancements, as synthetic biology sees disruptive breakthroughs every two to three years; if the "dual-engine" capability fails to continuously deliver new proprietary processes, the company’s competitive moat may be rapidly eroded.

Based on the above facts and comparisons, the following six key indicators can be monitored to track the operational status of Leadsynbio over the next 24 months:

First, can the gross profit margin for the full year of 2025 return to above 5%? This serves as a critical validation of whether the recovery in capacity utilization rate is stable.

Second, the trend in unit prices of nutritional supplements. Whether categories such as NMN have stopped declining will determine the profit margin for Leadsynbio’s second growth curve. If unit prices stabilize or rebound, it indicates that industry capacity expansion has been absorbed; if they continue to fall, it suggests that NMN-related products have entered a “red ocean” phase.

Third, the performance contribution of the associate company, Hunan Lier. The glufosinate-P market has experienced significant cyclical volatility, with prices halving at one point in 2024, which directly impacts Leadsynbio’s income statement through the “share of profits of associates” line item.

Fourth, the capital expenditure pacing of the 180,000-ton NaBH4 project and the status of downstream order fulfillment. This is a key variable affecting the company’s asset turnover ratio over the next five years.

Fifth, the commercialization timeline for the next batch of new products among the 14 commercially available offerings. When will products such as R-HPBE, DHEA, and UDCA enzymes—which are already commercialized but currently contribute minimally—become the next generation of D-ethyl esters?

Sixth, the net fundraising scale and pricing of the Hong Kong IPO. This will directly determine the company’s capital structure and production expansion pace over the next three years, as well as the urgency of secondary financing.

07

# Conclusion

A primary market investor who has long tracked the synthetic biology industry once told the author: “The keyword for synthetic biology in the past decade was ‘storytelling’; for the next decade, it will be ‘delivery.’” From this perspective, Leadsynbio’s IPO filing represents more than just an application for listing; it places before the Hong Kong stock market an industry-level question: “Can Chinese synthetic biology companies convert their leading global product market share into sustained profitability during the window of opportunity created by the withdrawal of European and American giants?”

The company’s true value lies not in the volume of D-ethyl ester sold today, nor in the cash remaining on its balance sheet, but in its ability over the next five to ten years to translate its capability—as one of the very few companies worldwide that can scale multiple proprietary process routes from laboratory to industrial production—into sustained profitability and a replicable business model.

Cathay Biotech took 23 years, and Huaheng Biotechnology took 16 years. As a company that has been in operation for 11 years, what pace Leadsynbio will adopt to achieve its subsequent development is an industrial issue worth tracking over the next 5 to 10 years. During this period, every quarterly financial report, every announcement of capacity expansion, and every progress in the commercialization of new products are all interim submissions to this engineering problem.

Primary data sources: Suzhou Leadsynbio Technology Co., Ltd.’s application version (A1, first submission) for listing on the Main Board of the Hong Kong Stock Exchange, submitted on February 12, 2026; Frost & Sullivan industry research reports; Cathay Biotech’s annual reports for 2024 and 2025; Huaheng Biotechnology’s annual reports for 2024 and 2025 and its Q1 2026 quarterly report; BASF Report 2024; and public information from DSM-Firmenich.

This article provides objective analysis and industry observations and does not constitute any investment advice.