IMPACT Therapeutics Surges Over 70% on Hong Kong Debut, Highlighting Synthetic Lethality Innovation

IMPACT Therapeutics

Targeted Anti-Cancer Innovative Drug Developer

Nanjing IMPACT Therapeutics, Inc. was listed on the Main Board of the Hong Kong Stock Exchange today, with stock code 7630. The global offering comprised 41,977,000 H shares, at an offer price of HK$20.1yuan. This is a biotechnology company founded in Nanjing in 2009, specializing in precision anticancer therapies based on synthetic lethality.

At today’s opening, IMPACT Therapeutics opened at HK$34.2, surging 70.15%, with a market capitalization of HK$9.445 billion.

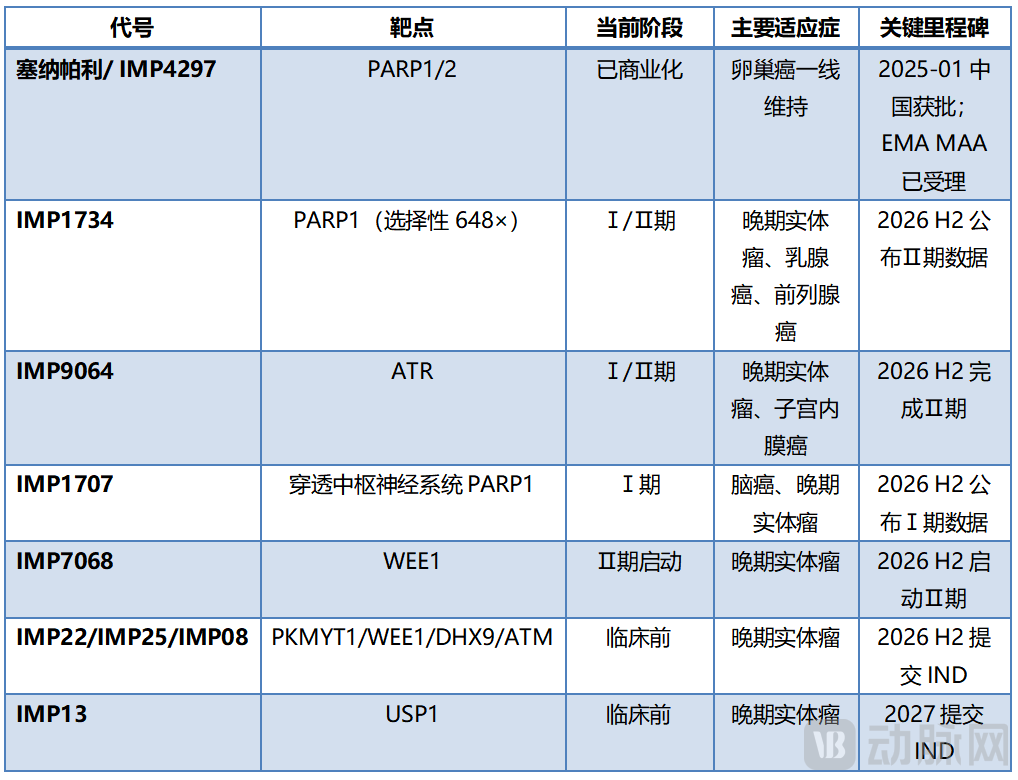

Regarding product progress, the company’s core product, senaparib (IMP4297, a PARP1/2 inhibitor), was approved in China in January 2025 for first-line maintenance treatment of ovarian cancer in the “all-comers” population. It was formally included in the 2025 National Reimbursement Drug List in January 2026. In its first year of commercialization, senaparib generated sales revenue of RMB 20 million with a gross margin of 92.2%. The company’s total annual revenue reached RMB 38.25 million (a year-on-year increase of 14.0%), while R&D expenses amounted to RMB 184 million. In addition to senaparib, the company has 11 synthetic lethality pipeline products at various stages, covering seven major targets: PARP1, ATR, WEE1, PKMYT1, DHX9, ATM, and USP1.

IMPACT Therapeutics’ first product has just launched in the Chinese market, while its European regulatory application is underway. The company is backed by several strategic cornerstone investors, including Tencent, Lilly Asia Ventures (LAV), and Worldwide Healthcare Partners (WWHCP). Drawing on IMPACT Therapeutics’ HKEX prospectus and publicly available global industry data, this report analyzes the company’s positioning within the synthetic lethality sector across four dimensions: industry landscape, commercialization progress, R&D pipeline, and support from strategic capital.

01

In the synthetic lethality space, what is the differentiated positioning of senaparib?

Let’s rewind to 11 years ago. Olaparib, a PARP1/2 inhibitor co-developed by AstraZeneca and Merck & Co., received FDA approval in December 2014, marking the first commercial validation of synthetic lethality as a drug mechanism. Eleven years later, in January 2025, senaparib was approved in China, becoming the seventh marketed PARP1/2 inhibitor globally and the third approved in the Chinese market for first-line maintenance therapy in “all-comer” patients with ovarian cancer (the first two were the imported olaparib and the domestically developed fluzoparib, which were approved in China in 2019 and 2021, respectively).This competitive landscape has already attracted participation from numerous domestic and international enterprises. Senaparib’s approval in China for “first-line maintenance therapy across the entire population” reflects a structural shift often underestimated in industry discussions—the global divergence in regulatory pathways.

● A divergence: The FDA is accepting applications, while the NMPA and EMA have not followed suit

This issue traces back to the U.S. Food and Drug Administration (FDA). Between 2022 and 2025, the FDA twice narrowed the approved indications for several PARP inhibitors. The first adjustment occurred in 2022, when the indication for niraparib as second-line maintenance therapy in advanced epithelial ovarian cancer was restricted from the all-comer population to patients with BRCA mutations. The second came in 2025, when the indication for first-line maintenance therapy was similarly narrowed from the all-comer population to patients with homologous recombination deficiency (HRD-positive), on the grounds that the overall survival (OS) benefit in the homologous recombination proficient (HRP) subgroup did not reach statistical significance. During the same period, however, neither the European Medicines Agency (EMA) nor China’s National Medical Products Administration (NMPA) followed suit. The EMA maintained its position that approval should be granted if the primary analysis population in the registration trial meets the primary endpoint, without requiring separate demonstration of OS benefit in each biomarker-defined subgroup. Meanwhile, the NMPA has continued to include PARP inhibitors for first-line maintenance therapy in the all-comer population in its clinical guideline recommendations. Both Chinese and European clinical guidelines explicitly recommend PARP inhibitors for first-line maintenance therapy in the entire ovarian cancer population, resulting in two distinct regulatory pathways diverging from that of the FDA.

The industrial implications of this divergence are straightforward. For a Chinese biotech company, the “all-comers” label for senaparib constitutes a tangible asset within both the NMPA and EMA regulatory frameworks. The prospectus explicitly discloses that the company does not plan to submit a New Drug Application (NDA) to the FDA; instead, its commercialization strategy focuses on the China market under NMPA regulation and the European market under EMA regulation—a deliberate strategic choice. Senaparib’s Marketing Authorization Application (MAA) was submitted to and accepted by the EMA in August 2025, with approval expected in the second half of 2026. It was formally included in China’s National Reimbursement Drug List on January 1, 2026, at a retail price of RMB 4,650 per box.

● From PARP Inhibitors to Seven Novel Targets: A Broad Industrial Track

However, Senaparib is merely IMPACT Therapeutics’ entry-level product. Broadening the scope to the entire synthetic lethality landscape, the industry logic over the past five years has shifted from “PARP inhibitors dominating the field” to “seven novel targets advancing in parallel.” According to Frost & Sullivan data, the global synthetic lethality drug market was valued at $2.4 billion in 2020 and reached $4.3 billion in 2024 (CAGR 15.6%), with projections to hit $8.7 billion by 2029 and $16.1 billion by 2033. In China, the market grew from $200 million in 2020 to $500 million in 2024 (CAGR 25.9%), and is expected to reach $1.4 billion by 2029.

A more direct industry signal—the transaction market. Between 2019 and 2024, the total value of global business development (BD) deals related to synthetic lethality amounted to approximately $25 billion. In December 2024 alone, Hengrui Medicine licensed the global rights to its PARP1 selective inhibitor, HRS-1167, to Merck KGaA for an upfront payment of $170 million and a total deal value of $1.55 billion; CSPC Pharmaceutical Group licensed the global rights to its MAT2A inhibitor, SYH2039, to BeiGene for an upfront payment of $150 million and a total potential value of $1.835 billion; and IDEAYA Biosciences licensed the global rights to its Pol θ inhibitor, IDE705, to GSK for an upfront payment of $80 million and a total potential value of $1.1 billion. A timely update is required: as of May 2026, Merck KGaA officially announced on March 5, 2026, the termination of its global licensing agreement with Hengrui Medicine for HRS-1167, resulting in Hengrui reclaiming the global rights to the asset. This market development occurred after the completion of IMPACT Therapeutics’ prospectus draft.

What is the most direct industrial implication of this landscape for IMPACT Therapeutics? The answer lies in its pipeline. Among the 12 candidates, with the exception of senaparib, drugs such as IMP1734 (a selective PARP1 inhibitor), IMP9064 (an ATR inhibitor), IMP7068 (a WEE1 inhibitor), IMP22 (a PKMYT1/WEE1 inhibitor), IMP25 (a DHX9 inhibitor), IMP08 (an ATM inhibitor), and IMP13 (a USP1 inhibitor) all target areas where business development (BD) consensus on collaboration has already been established in the market. Individually, each candidate may not necessarily rank among the global top tier, but collectively, they constitute multiple industrial interfaces for a biotech company within the global partnership market.

Figure 1: Overview of IMPACT Therapeutics’ Pipeline Progress (Source: “Business” section of the H-share prospectus)”Chapter)

02

Product Performance of Senaparib in Its First Year of Commercialization

Having discussed the industry landscape, we now return to the product itself. Senaparib (IMP4297) has been the core pipeline focus selected by IMPACT Therapeutics since its establishment in 2009. The project was initiated in 2012, entered clinical trials in 2018, completed Phase III registration trials in 2024, and received marketing approval from the National Medical Products Administration (NMPA) in January 2025 for first-line maintenance treatment of ovarian cancer in the “all-comers” population (regardless of BRCA mutation status). This marks a key milestone in IMPACT Therapeutics’ transformation from a research-oriented biotech company to a commercial-stage enterprise. Key data sets from the first year of commercialization reflect the product’s initial market penetration in China.

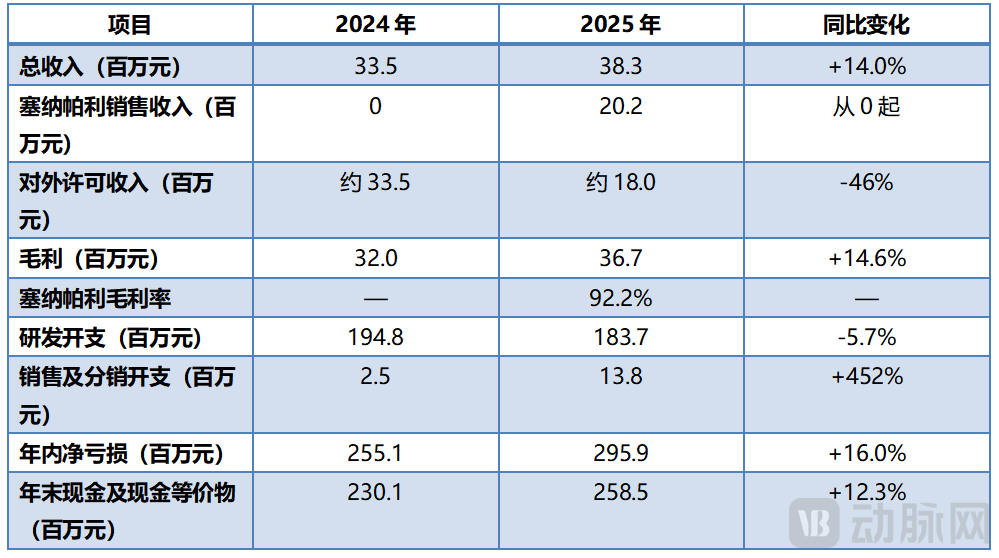

Figure 2: Core Financial Data of IMPACT Therapeutics from 2024 to 2025 (Source: Accountant’s Report in Appendix I to the HKEX Prospectus)

● The Product Logic Behind a 92.2% Gross Profit Margin

Let us first examine a set of intuitive figures. In its first year of commercialization, Senaparib achieved sales of RMB 20.2 million and a gross profit of RMB 18.7 million, with a gross margin of 92.2%. This performance is broadly comparable to that of olaparib and niraparib in the Chinese market, reflecting the product characteristics of PARP inhibitors as oral small-molecule targeted therapies: high gross margins and low material costs. With a retail price of RMB 4,650 per box, Senaparib was formally included in the National Reimbursement Drug List (NRDL) effective January 1, 2026, covering first-line maintenance treatment for the “all-comer” population with ovarian cancer. This signifies that, starting in 2026, Senaparib will enter a new phase of patient accessibility supported by national insurance coverage. In terms of the product landscape in the Chinese market, Senaparib, together with niraparib (approved in September 2019) and fluzoparib (approved in 2021 by Hengrui Medicine), constitutes the trio of PARP1/2 inhibitors approved for first-line maintenance treatment in the “all-comer” population with ovarian cancer. In contrast, GSK’s niraparib (distributed in China by Zai Lab) has its indication restricted to the BRCA-mutated or homologous recombination deficiency-positive (BRCA/HRD+) subgroups. Senaparib and fluzoparib jointly form the domestic Chinese PARP1/2 inhibitor camp, creating an industrial coexistence pattern with imported products.

● “Leverage Channels, Don’t Hire Them”——Division of Labor with Zhongmei Huadong

Returning to the sales segment. In December 2023, IMPACT Therapeutics entered into a contractual sales service agreement with Hangzhou Zhongmei Huadong Pharmaceutical, a wholly-owned subsidiary of Huadong Medicine (SZ.000963), for senaparib in the Chinese market. Leveraging its mature distribution network, Zhongmei Huadong is responsible for the promotional execution of senaparib in China. The advantage of this division of labor is that the company does not need to build a large-scale sales team in the early stages of commercialization. In 2025, selling and distribution expenses amounted to RMB 13.82 million (compared to RMB 2.5 million in 2024), aligning with sales revenue of RMB 20.2 million, resulting in a selling expense ratio of approximately 68%.

● Next Steps After Inclusion in the National Medical Insurance Program

On January 1, 2026, senaparib was officially included in the National Reimbursement Drug List (NRDL) of China, marking the entry of the product into a new phase of promotion. Domestic counterparts in China provide a reference: after fluzoparib was approved in 2021, it gradually became the leading domestic PARP inhibitor in the Chinese market, leveraging Hengrui’s sales network and NRDL coverage. Senaparib’s channel execution is undertaken by Zhongmei Huadong, and its promotional pace over the next two to three years, supported by NRDL reimbursement, warrants close monitoring. From an industry perspective, as PARP inhibitors are widely recommended in clinical guidelines as first-line maintenance therapy for ovarian cancer, coupled with improved accessibility driven by NRDL coverage, the product promotion has a solid industrial foundation.

03

How Do 12 Pipeline Assets Build a Synthetic Lethality Product Portfolio?

What comes after senaparib? This is a question that most Phase 18A biotech companies must confront. IMPACT Therapeutics’ answer is: In addition to senaparib, the company has 11 candidate drugs—comprising four clinical-stage products and seven preclinical candidates—covering seven synthetic lethality targets, namely PARP1, ATR, WEE1, PKMYT1/WEE1, DHX9, ATM, and USP1, along with novel antibody-drug conjugate (ADC) and degrader platforms. The R&D team consists of 59 members, with core personnel possessing 10 to 20 years of experience in the field of oncology synthetic lethality. Among these 11 candidates, IMP1734 and IMP9064 have entered Phase I/II clinical trials, representing the two core directions for the company’s R&D deliverables over the next 24 months.

● IMP1734: What would happen if the off-target effects on PARP2 were eliminated?

Let’s start with IMP1734. All currently marketed PARP1/2 inhibitors—olaparib, senaparib, fluzoparib, niraparib, talazoparib, pamiparib, and rucaparib—are dual PARP1/PARP2 inhibitors. They share a common “class effect”: since PARP2 is also involved in DNA repair in normal hematopoietic cells, hematologic toxicities are a characteristic feature of this drug class, limiting dosing levels and opportunities for combination therapies. The design rationale behind next-generation PARP1-selective inhibitors is to eliminate off-target effects on PARP2. IMP1734 exhibits more than 648-fold greater activity against PARP1 than against PARP2. In theory, this selectivity allows it to significantly reduce hematologic toxicities while retaining antitumor efficacy, thereby supporting higher dosing, a wider therapeutic window, and broader potential for combination regimens. If the Phase II data expected in the second half of 2026 confirm the anticipated profile of “significantly improved safety without compromising objective response rate (ORR),” IMP1734 has the potential to become the successor product to senaparib in the portfolio.

However, IMPACT Therapeutics is not the only player in this race. PARP1 selectivity has emerged as one of the most closely watched subfields within the synthetic lethality landscape. As a representative next-generation PARP1-selective inhibitor, AstraZeneca’s AZD5305 (saruparib) initiated multiple Phase III clinical trials between 2024 and 2025. Data from the PETRA trial presented at AACR 2024 showed that, in patients with HRR-mutated solid tumors (including BRCA1/2, PALB2, and RAD51C/D mutations), the 60 mg dose achieved an objective response rate (ORR) of 48.4%, a median duration of response (DoR) of 7.3 months, and a median progression-free survival (PFS) of 9.1 months. Jiangsu Hengrui Medicine’s HRS-1167 was licensed to Merck KGaA (Germany) in October 2023 for an upfront payment of €160 million (with potential total value reaching €1.4 billion); however, Merck terminated this collaboration in March 2026. IMP1734 is currently in Phase I/II development, following a different R&D timeline compared to the aforementioned competitors. Through a global collaboration agreement with U.S.-based Eikon Therapeutics, the company has introduced third-party resources to bolster both its clinical advancement and global development capabilities—a point that will be elaborated on later.

● Looking Further Ahead: ATR, WEE1, and a Set of Novel Targets

Beyond the PARP family, IMPACT Therapeutics has achieved broad coverage across multiple novel synthetic lethality targets. IMP9064 is the first ATR-selective inhibitor in China to enter clinical development. Its Phase II trial focuses on monotherapy for advanced endometrial cancer, and it has received IND approval for combination therapy with senaparib in ovarian and pancreatic cancers—a key industrial direction in the synthetic lethality landscape, as ATR inhibitors can delay resistance to PARP inhibitors and expand the eligible patient population. IMP7068 (WEE1) has completed Phase I trials. Four preclinical candidates—IMP22 (PKMYT1/WEE1), IMP25 (DHX9), IMP08 (ATM), and IMP13 (USP1)—are expected to file INDs sequentially between 2026 and 2027. This portfolio is characterized by its “broad coverage,” enabling the company to establish a comprehensive industrial interface in the synthetic lethality sector through simultaneous multi-target advancement, thereby creating numerous footholds for future industry collaborations with multinational pharmaceutical companies.

● Eikon Protocol—Entrusting global development to an overseas partner

Returning to Eikon, mentioned earlier. In May 2023, IMPACT Therapeutics entered into a global collaboration agreement with Eikon Therapeutics, a biotechnology company based in California, USA, concerning IMP1734 and IMP1707. Founded in 2019 by Dr. Roger Perlmutter (former President of Merck Research Laboratories and former Vice President of R&D at Amgen), Eikon boasts an internationally leading team background and capabilities in early-stage global clinical development. While specific economic terms were not disclosed in detail in the prospectus, the related patent-sharing arrangements indicate that Eikon plays a substantial role in the global development and commercialization of IMP1734 and IMP1707. For a Chinese biotech company focused on the NMPA and EMA regulatory markets, this equates to securing an industry partner with international experience for key global markets.

● The Real Ledger of R&D Funding

Finally, regarding cash. IMPACT Therapeutics is listed under Chapter 18A of the Main Board Listing Rules of the Hong Kong Stock Exchange. The approval of Senaparib by the NMPA in January 2025 constitutes compliant evidence that its “core product has passed IND proof-of-concept” within the meaning of Chapter 18A. As of the end of 2025, the company had RMB 258.5 million in cash on its balance sheet; combined with the proceeds from this IPO, the company will secure more ample financial resources for R&D and commercialization. One detail worth noting: the “net liabilities of RMB 957.9 million” shown on the balance sheet primarily stem from the accounting treatment under HKFRS, which classifies “preferred ordinary shares” as financial liabilities. The preferential rights attached to these financial instruments will terminate upon listing, and the related financial liabilities will be reclassified to equity. Consequently, after the completion of the IPO, the company will transition from a net liability position to a net asset position.

04

The Pace of Industry Development Supported by Professional Institutional Investors

Having discussed the products and pipeline, we now turn to the shareholder aspect. The CEO is a 68-year-oldDr. Cai Suixiong joined IMPACT Therapeutics in January 2010, was appointed as a director in June 2014, and holds a 3.6% equity stake.IMPACT Therapeutics boasts a prestigious roster of institutional shareholders. Its largest shareholder is Lilly Asia Ventures, controlled by Dr. Shi Yi, which holds approximately 15.62% of the shares. Other notable shareholders include Liyi Investment, Decheng Capital, Tencent, Junshi Biosciences, and WuXi AppTec,GTJA,institutions such as Yuexiu Fund and Hualing Capital. The cornerstone investor lineup for this global offering consists of institutions including Lilly Asia Ventures (LAV), Tencent, and Worldwide Healthcare Partners LLC (WWHCP). The LAV USD Group (a collective term for the offshore investment vehicles of Lilly Asia Ventures) holds 15.62% of the pre-IPO shares, making it the company’s largest single shareholder group; Tencent holds 6.66% through Guangxi Tencent Venture Capital Co., Ltd.; and WWHCP, together with its affiliate Exome Asset Management, holds approximately 0.39%.

These investment institutions share a common trait: they are all industry-focused investors who have maintained long-term tracking of China’s innovative drug industry chain. Lilly Asia Ventures (LAV), founded by Dr. Shi Yi in 2008, has invested in dozens of Chinese innovative drug companies over the past 17 years, including Innovent Biologics, Zai Lab, Hutchmed, and Legend Biotech. Its portfolio strategy is characterized by “early-stage positioning, continuous multi-round participation, and long-term industrial partnership.” LAV participated in IMPACT Therapeutics’ journey from Series A financing to its initial public offering (IPO) and continued its involvement as a cornerstone investor in this IPO. As an industry investor that has closely tracked the company’s pipeline for many years, this decision reflects its professional judgment on the pace of pipeline development. Since around 2020, Tencent has increased its early-stage investments in Chinese biotech firms focused on innovative drugs and is already listed among the shareholders of companies such as Innovent Biologics, Hutchmed, and Libang Medicine. Its investment in IMPACT Therapeutics represents not only an industrial investment in China’s biotechnology supply chain but also a strategic move to secure a position in the synergistic space of “AI + drug R&D.”

● Three Key Milestones to Watch Over the Next 24 Months

From an industry observation perspective, there are three key milestone nodes worth tracking for the company over the next 24 months.

The first point concerns the post-2026 National Reimbursement Drug List (NRDL) inclusion progress of Senaparib’s product promotion. Following its inclusion in the NRDL, the patient coverage and prescription rollout pace of Senaparib under insurance reimbursement throughout the year reflect the depth of market penetration for this core product in China—making it the most noteworthy industry development to watch over the next 12 months.

The second is the EMA’s review outcome for the European MAA of senaparib in the second half of 2026. The MAA was accepted in August 2025. Once approved, it will be indicated for the “all-comer” population with ovarian cancer.”First-line maintenance therapy: The company will pursue two commercial pathways in the European market—independent sales or out-licensing—marking the global expansion of senaparib.”the first substantial threshold.

The third is the Phase II clinical data for IMP1734 in the second half of 2026. This represents a critical milestone for the PARP1-selective pipeline, marking its transition from product concept to clinical validation. If the Phase II data simultaneously demonstrate a safety advantage (specifically, lower hematological toxicity compared with dual inhibitors) and a favorable objective response rate, IMP1734 is poised to become a core asset for the company’s future business development partnerships or clinical advancement.

Viewing these three developments together reveals that they all fall within the period from the second half of 2026 to the first half of 2027. In other words, the first year following the company’s listing represents a concentrated window for the realization of industrial progress—each milestone achieved will enrich the company’s industry narrative. This underpins the rationale for industrial capital to support the company from its early stages through to its IPO.

05

# Final Thoughts

Viewed holistically, IMPACT Therapeutics is not a typical early-stage 18A biotech. A classic 18A case usually involves a company holding an early-stage clinical pipeline, requiring five to eight years to achieve commercialization. In contrast, IMPACT Therapeutics already has senaparib, which has been approved in China, was included in the National Reimbursement Drug List just four months ago, and carries a “pan-population” label. Additionally, the company boasts a pipeline of 11 synthetic lethality assets at various stages, a clearly defined differentiated strategy of “no FDA submission, focusing on NMPA and EMA approvals,” and an asset-light commercialization path that leverages existing channels rather than building its own sales force. Taken together, the company resembles an industrial model that has completed a full R&D-to-commercialization loop in China’s synthetic lethality sector. Its industry narrative is more advanced, with a denser window for milestone delivery over the next 24 months.

Subsequent industrial progress can be tracked along several key threads: the product promotion of senaparib following its inclusion in the National Reimbursement Drug List (NRDL), the progress of the European Medicines Agency (EMA) review, the realization of clinical data for IMP1734, the R&D advancement of multi-target pipelines including ATR, WEE1, and PKMYT1 inhibitors, the implementation of the global collaboration with Eikon, and the realization of future industrial partnership opportunities. Each thread corresponds to specific milestone nodes, with each milestone representing a step in the company’s transition from a biotech firm to a mid-sized pharmaceutical company.

References:

1. “Prospectus for the Global Offering of Impact Therapeutics Inc.” – The Stock Exchange of Hong Kong Limited, May 2026, Stock Code: 7630;

2.《Full Year and Q4 2024 Results Announcement》《Annual Report 2024》——AstraZeneca PLC;

3.《FY 2024 Results》《Annual Report 2024》——GSK plc;

4. “2025 Annual Report” – Jiangsu Hengrui Medicine Co., Ltd. (600276.SH), disclosure of anti-tumor product revenue;

5. Public regulatory documents from the NMPA, EMA, and FDA regarding the approval and indication adjustments of PARP1/2 inhibitors for first-line maintenance therapy in ovarian cancer;

6. Frost & Sullivan Industry Analysis Report on the Synthetic Lethality Drug Market and the Global PARP1/2 Inhibitor Market, 2024–2025.