2026 CT Industry Research Report: Ultra-High-End CT Leads the Way, Domestic X-ray Tubes Accelerate Rise

Over the past year, the CT industry has undergone significant transformation. In terms of complete systems, the approval of two domestically produced photon-counting CT scanners marks a pivotal shift for high-end imaging equipment from “replacement” to “leadership.” The five major players—Siemens, Canon, United Imaging, Neusoft, and GE—have now formally converged, ushering the ultra-high-end imaging sector into a new era of competition and collaboration. Meanwhile, phased-array CT has achieved tens of millions of pixels by adopting a novel approach combining “static dual-ring arrays” with “electronic phased scanning.”

On the other hand, with the upgrading of market structure and high-end CT scanners dominating the market, companies focused on mid- to low-end CT systems face challenges in cost reduction and transformation under the volume-based procurement policy, making market consolidation inevitable.

Regarding core components, X-ray tubes have attracted concentrated capital investment, favorable policies have been frequently introduced, and the localization process has accelerated. However, domestically produced X-ray tubes remain largely confined to the aftermarket, with no breakthroughs yet in the high-end segment and slow progress in material innovation.

Which Chinese-made imaging company will become the next Mindray? Is it possible for X-ray tube manufacturers to go public or break into the GPS OEM market? The road ahead is long, but the future holds promise.

This report analyzes CT industry products and core components through surveys of 12 enterprises and nearly 20 experts, yielding the following conclusions:

1. In 2025, China’s CT market officially entered a new phase of development characterized by stable sales volume, rising prices, a shift toward high-end models, and accelerated substitution of imports with domestically produced alternatives. The market share of domestic brands for CT scanners with 64 slices or fewer and those with 128 slices or more rose to 73% and 43%, respectively.

2. Investment focus in the CT sector has shifted significantly toward upstream core components, with nearly 40% of financing concentrated in the field of CT X-ray tubes, and liquid metal bearing technology gaining favor from investors.

3. Following the implementation of the policy exempting routine CT scanners with 64 slices or fewer from clinical trials, regulatory requirements at the registration stage will be relaxed. This will lower entry barriers and improve efficiency in the mid-to-low-end CT sector, thereby accelerating the substitution of domestic products for imports.

4. Domestic X-ray tubes have increased their market share by leveraging the window of opportunity provided by anti-dumping policies; however, compatibility policies with complete systems remain inadequate. It may be necessary to refine standards based on typical models, starting from the perspectives of underlying interfaces, protocols, and performance parameters.

5. CT systems are transitioning toward specialization and deep AI integration, with standing CT representing a major innovative direction; future CT tube technology may place greater emphasis on micro-focus capabilities; in after-sales service, bundled imaging solutions may become a trend, while spare parts management requires further standardization.

6. Over the next 3–5 years, the pace of domestic replacement for X-ray tubes will accelerate significantly, with market share expected to rise substantially. The industry may simultaneously experience downward price pressure, capacity consolidation, and a technological shift toward high-end restructuring.

Overview: CT System Structure Upgraded; Core Components Attract Concentrated Capital Investment

Phase: A Dual Phase of Maturity and Structural Upgrading, with Steady Market Growth

China’s CT market is in a dual phase of maturity and structural upgrading. At present, the CT markets in developed countries worldwide have entered a mature stage of development, with growth rates stabilizing; their core development focus is on technological optimization and refined operations within the installed base.

The overall development logic of China’s CT market is undergoing a fundamental shift, gradually transitioning from the previous “incremental expansion” model reliant on new installations to a high-quality development stage centered on improving quality and efficiency within the installed base, while simultaneously advancing technological iteration and upgrades.

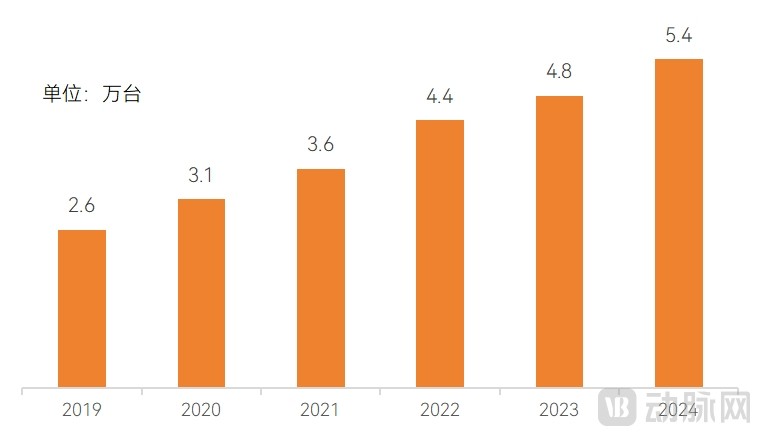

According to the China Association of Medical Equipment, from 2022 to 2024, the average annual increase in new CT units in China was nearly 5,000, with the installed base continuing to expand steadily. The specific changes in the number of CT units installed in China from 2019 to 2024 are as follows:

Figure: Installed Base of CT Equipment in China

Data Source: China Association of Medical Equipment

Financing: Tilting toward core components, with concentrated bets on X-ray tubes

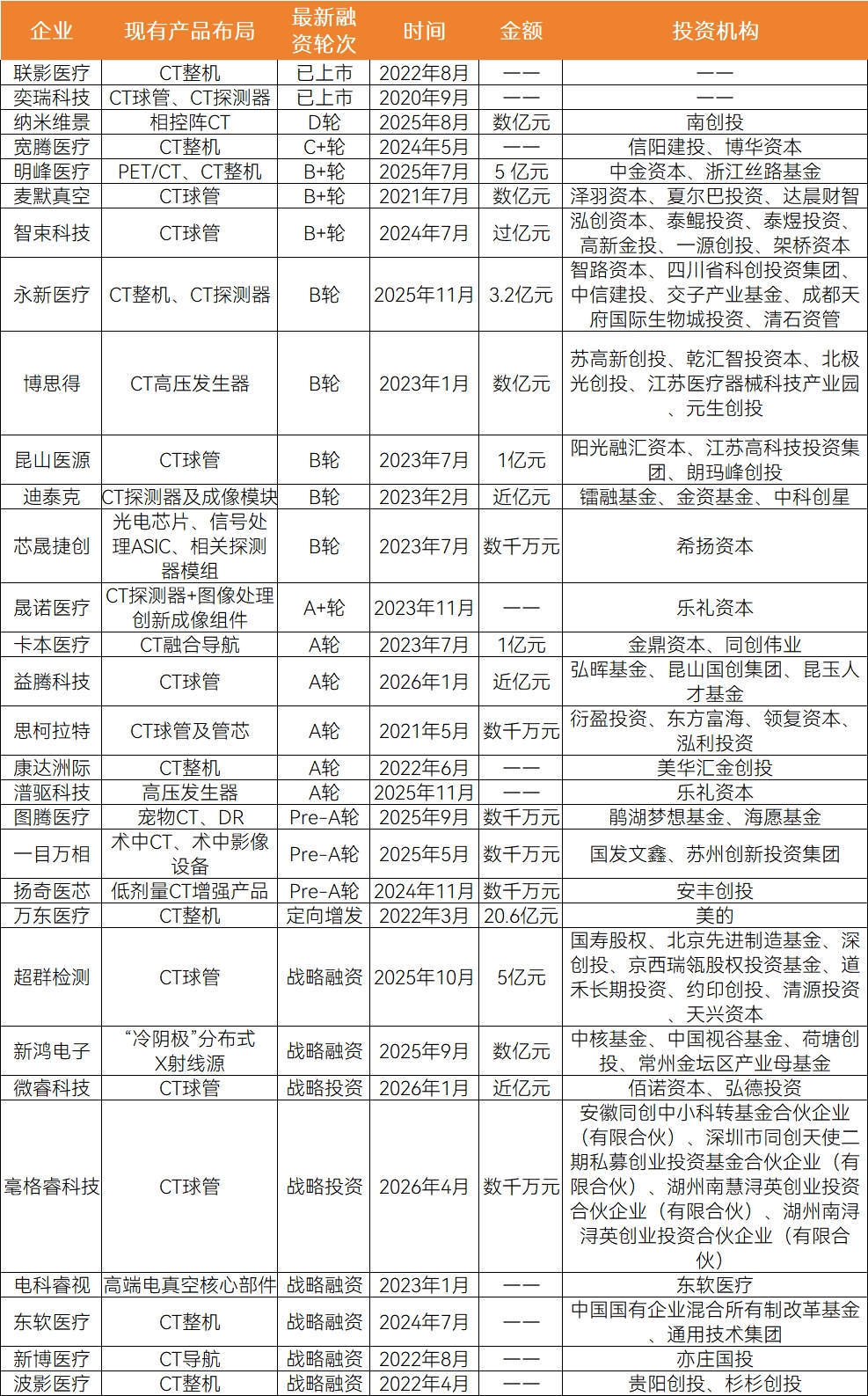

According to incomplete statistics from VBInsight on the latest financing rounds in the CT industry, investment in recent years has primarily covered complete systems, core components (X-ray tubes, detectors, high-voltage generators), and supporting technologies. Capital has been increasingly directed toward core components, particularly X-ray tubes.On the timeline, from 2024 to early 2026, multiple financing rounds exceeding RMB 100 million were completed, demonstrating capital markets’ confidence in the long-term development of the CT industry.

In terms of core components, companies addressing critical bottlenecks such as CT X-ray tubes and detectors have secured intensive financing, with approximately 40% of the funding concentrated in X-ray tubes; the financing rounds are primarily Series B and earlier.

In 2026, three X-ray tube manufacturers have secured financing: Weirui Technology, Yiteng Technology, and Haogerui Technology. All three companies are engaged in the development of liquid metal bearing technology.

Furthermore, Zhisu Technology (Series B+) is the most advanced in terms of financing rounds among companies deploying liquid metal bearing technology for X-ray tube assemblies. This indicates that, as a core component of high-end X-ray tubes, liquid metal bearing technology is highly favored by capital investors.

In the high-voltage generator sector, Pudrui Technology, backed by a team with renowned foreign enterprise experience, has completed its latest funding round, while established player Boside secured the largest amount of financing in recent years. Additionally, enabling technologies such as signal processing and imaging components have attracted minor investments within the medical imaging ecosystem.The details are as follows:

Figure: Statistics on Recent Financing in the CT Industry

Data Source: Public Data

Market: Stable Volume and Rising Prices, Premiumization Upgrade, Domestic Penetration

In 2025, the CT market officially entered a new phase of development characterized by stable volume and rising prices, a shift toward high-end models, and accelerated localization.

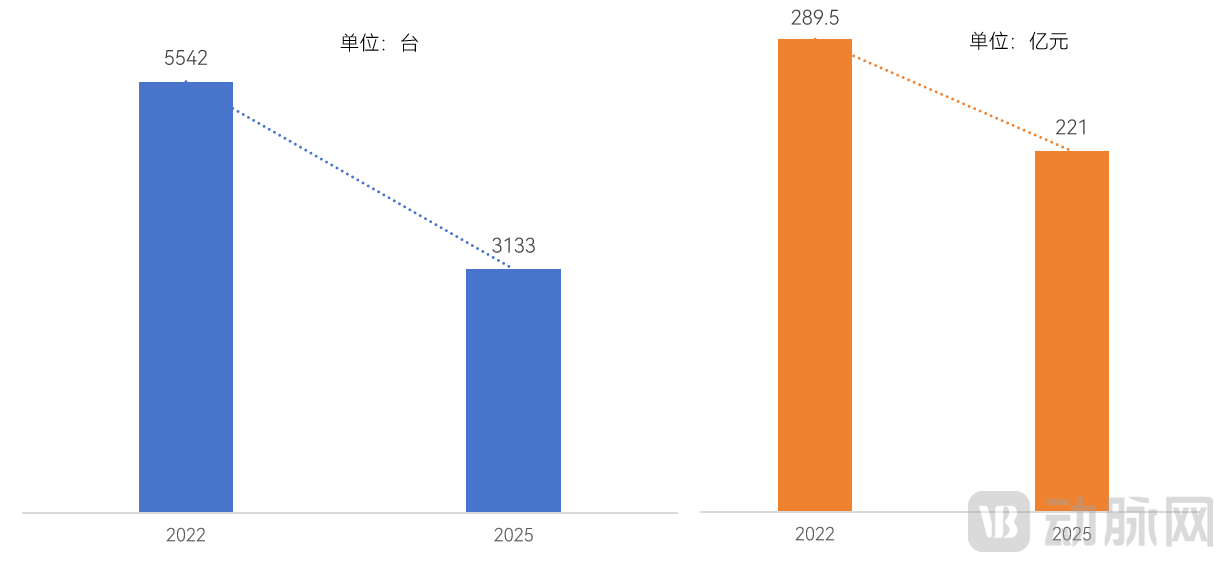

From a longitudinal perspective, public bidding data for 2025 show that a total of 3,133 CT units were procured nationwide in China, with a total value of RMB 22.1 billion. According to MDCLOUD (Medical Device Data Cloud), the total winning bid amount for CT equipment in China was RMB 28.95 billion in 2022, with a total volume of 5,542 units.

As can be seen, against the backdrop of centralized procurement, the average purchase price of CT scanners in 2025 (RMB 705,000) increased significantly compared to that in 2022 (RMB 522,000), with stable volume and rising prices.

Figure 2022 and 2025 CT Winning Bid Quantity and Amount

Data Source: Public Tendering and Bidding

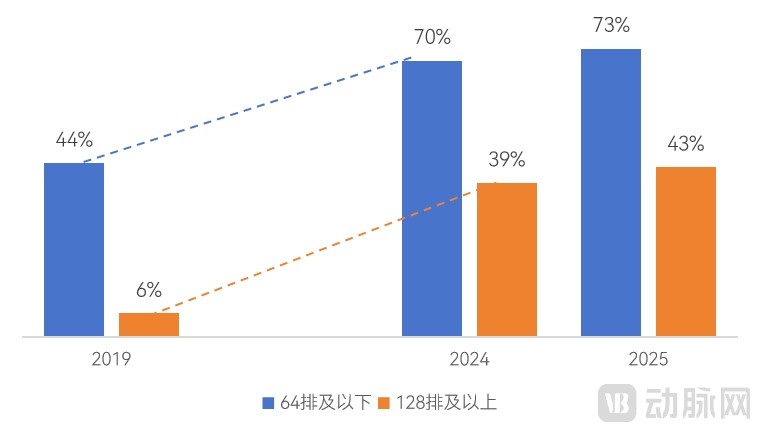

“Increased Domestic Production” is another keyword for the CT market in 2025. According to public bidding data, in the market for CT scanners with 64 slices or fewer, the share of winning bid amounts secured by domestic brands rose from 44% in 2019 to 70% in 2024; in the market for CT scanners with 128 slices or more, the share held by domestic brands increased from 6% in 2019 to 39% in 2024. By 2025, these figures had further climbed to 73% and 43%, respectively.

Figure: Proportion of Bid-Winning Amounts for Domestically Produced 64-Slice and ≥128-Slice CT Scanners in 2019, 2024, and 2025

Data Source: Public Bidding and Tendering, VBInsight

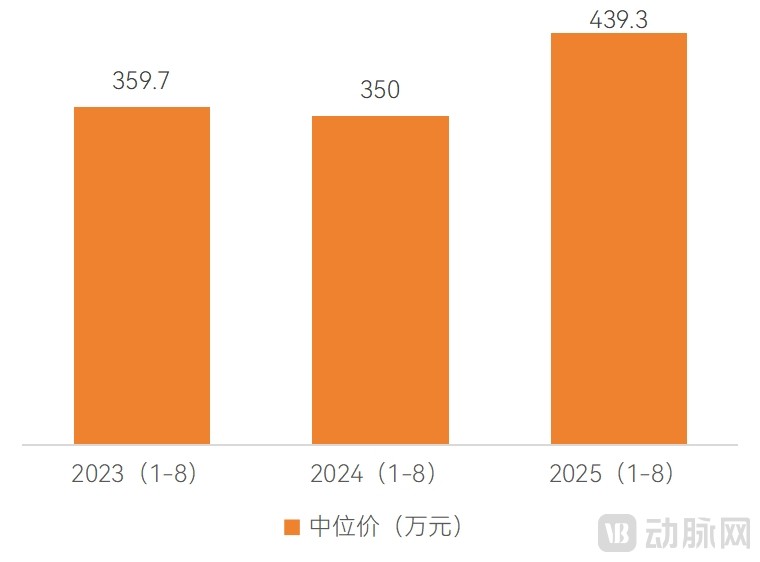

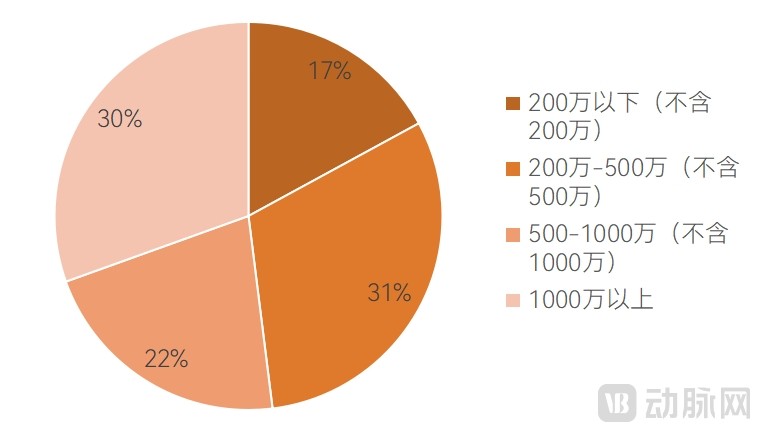

Based on the CT market data from January to August 2025, “premiumization” emerged as the core trend: the median price increased by 25.5%, rising from RMB 3.5 million in the same period of 2024 to RMB 4.393 million. Furthermore, data on the distribution of winning bid prices for CT equipment from January to August 2025 shows that high-end models priced above RMB 5 million accounted for approximately 52% of the total, becoming the primary force in market procurement. The details are as follows:

Figure: Median CT Prices and Price Distribution Share, January–August 2023–2025

Data Source: High-End Medical Device Research Institute Data Center

Figure: Distribution Share of Median CT Prices from January to August 2025

Data Source: High-End Medical Device Research Institute Data Center

Product: High-End CT Leads the Market, Niche Scenarios Create Blue Ocean Opportunities

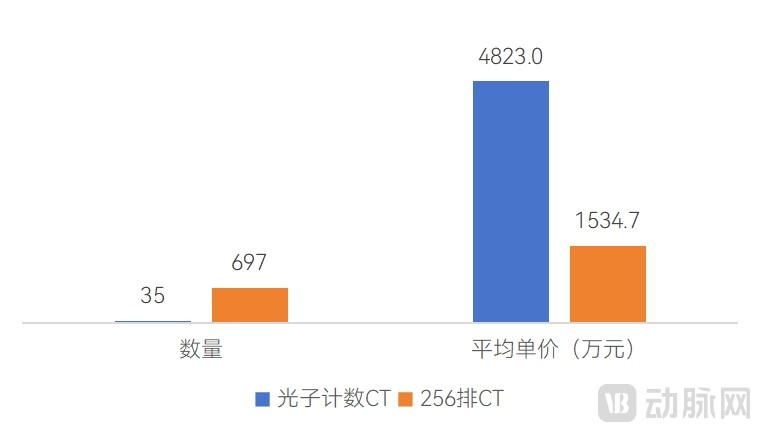

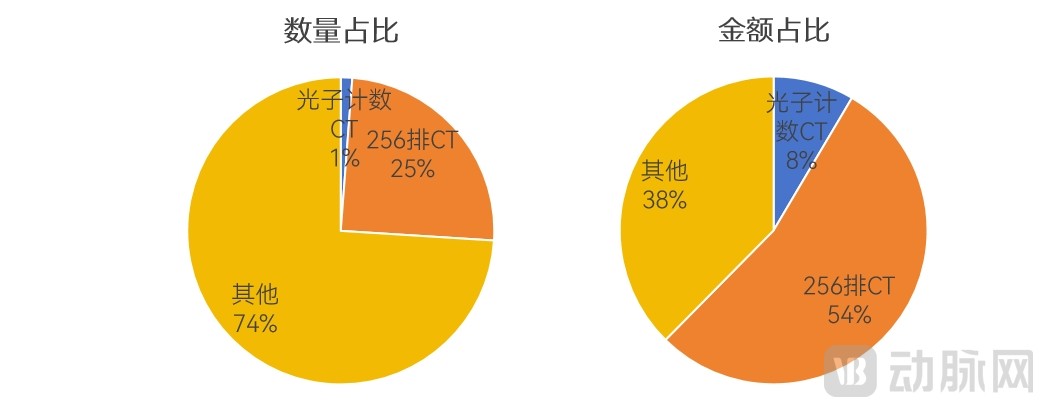

Based on the 2025 tendering data, photon-counting CT accounted for 1.2% of the winning bid count but captured 8.5% of the winning bid amount, while 256-slice CT secured 53.9% of the winning bid amount with a 24.8% share of the winning bid count; together, they represented 62.4% of the total winning bid amount.The quantity and value share of 128-slice CT scanners both stood at 9.6%, further underscoring the trend toward high-end dominance.

Figure: Tender Quantity and Average Unit Price of Photon-Counting CT and 256-Slice CT in 2025

Data Source: Public Bidding

Figure: Proportion of Bid Quantity and Amount for Photon-Counting CT and 256-Slice CT in 2025

Data Source: Public Bidding

Data Source: Public Bidding

Ultra-High-End: Photon-Counting CT Leads the Way, Phased-Array CT Achieves Breakthroughs

In 2025, photon-counting CT, hailed as the third revolution in CT technology, is transitioning from concept to clinical commercialization, ushering in a new era of high-end medical imaging.

Unlike conventional CT, photon-counting CT employs novel semiconductor detectors capable of individually counting and analyzing the energy of each X-ray photon, thereby achieving a qualitative leap in ultra-high spatial resolution, direct multi-energy spectral imaging, and lower radiation dose, providing unprecedentedly precise information for early disease diagnosis.

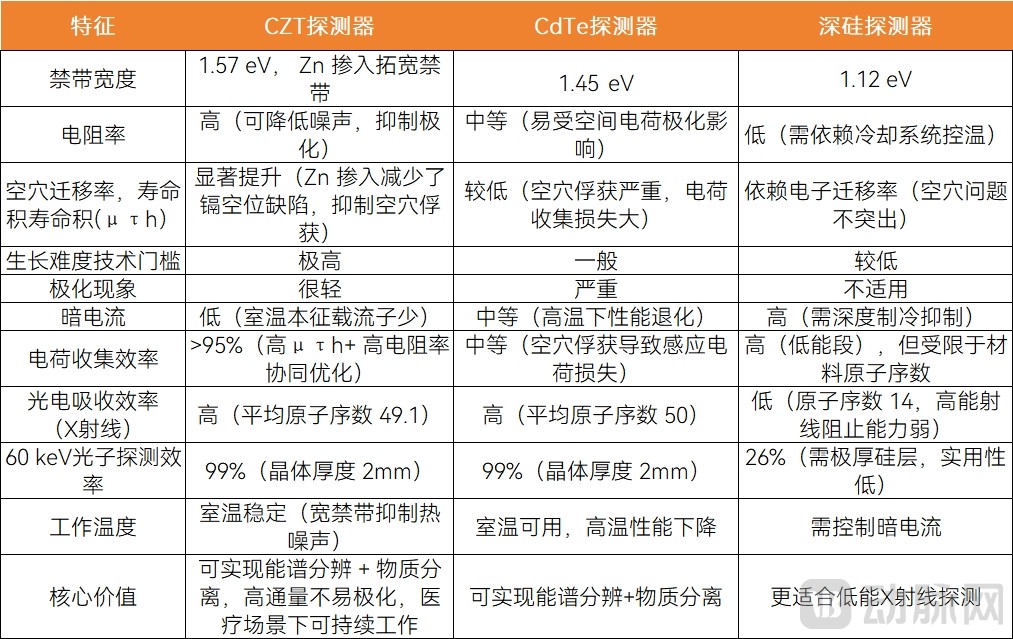

Among currently approved photon-counting CT systems, Siemens Healthineers has adopted the CdTe approach, while Neusoft Medical, United Imaging Healthcare, and Canon Medical Systems all use CZT as the detector material, and GE Healthcare has chosen deep Si. The selection of different materials essentially represents a trade-off among core performance metrics, including detection efficiency, energy resolution, spatial resolution, cost control, and clinical adaptability. Specifically,Below:

ChartCharacteristics of Mainstream Photon-Counting CT Detectors

Data Source: Advanced Technology Group, VBInsight

Against the industry backdrop of CZT becoming the mainstream technological route, domestic enterprises are accelerating their layout to achieve autonomous and controllable capabilities across the entire industrial chain. For instance, Leading Medical Technology has independently developed CZT crystals, ASIC chips, and photon-counting CT systems, thereby fully mastering the core technologies of the entire PCCT chain based on CZT detectors. These technologies include the purification and synthesis of ultra-high-purity elemental materials, single-crystal growth and processing, chip and device design and development, as well as CT system integration and imaging algorithm development, enabling mass production of CZT crystals.

Another highly anticipated ultra-high-end CT system is the phased-array CT, which features a fundamentally different technological pathway and core advantages compared to photon-counting CT.

The disruptive nature of phased-array CT lies in its abandonment of the traditional mechanical rotation architecture. By adopting a static dual-ring array combined with electronic phased scanning as its core, it achieves a leap from “mechanical motion-based imaging” to “precise electronic imaging,” earning it the industry moniker of “a new species in the field of CT.”

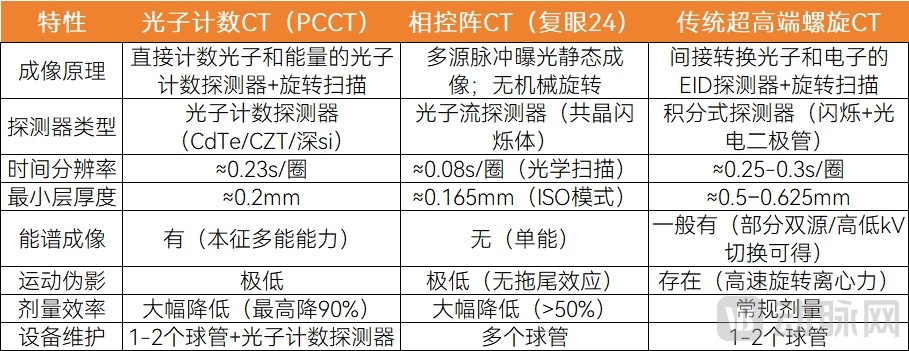

NanoVision’s first phased-array CT product, “Compound Eye 24,” received NMPA approval in late December 2025. Specifically, the differences among phased-array CT, photon-counting CT, and conventional ultra-high-end CT are as follows:

Figure: Differences between Photon-Counting CT, Phased-Array CT, and Conventional Ultra-High-End CT

Source: VBInsight

Phased-array CT presents new opportunities for healthcare institutions, along with corresponding challenges. These include hardware compatibility (such as PACS upgrades and network bandwidth), software adaptability (including AI algorithms and workstation processing capabilities), and clinical management.

At present, both photon-counting CT and phased-array CT are primarily used for scientific research; however, their technical pathways are being progressively validated, offering broad prospects for development.

With continuous breakthroughs in core components such as detectors and X-ray tubes, along with algorithmic advancements, expanding clinical indications, and gradually decreasing costs, these two technologies are poised to accelerate their transition from research settings to routine clinical practice. This shift will facilitate commercial deployment and large-scale installation, spearheading the next generation of medical imaging technology revolution.

Mid-to-Low End: Volume-Based Procurement Deeply Reshapes the Market, Transformation Becomes Imperative

In 2025, the normalization of centralized procurement is reshaping market logic. The driving force behind industry development is shifting from incremental expansion to the renewal of existing installations and penetration into primary care settings. While centralized procurement promotes the standardization of CT equipment configuration at the primary care level, it is also accelerating the elimination and replacement of outdated devices.

The mid-to-low-end CT market has largely completed its transition to domestically produced alternatives, with pricing structures returning to a reasonable profit margin. The focus of competition is gradually shifting toward higher-tier segments, and full-lifecycle stability is receiving increased attention.Higher After-Sales Service Requirements for Centralized Procurement: Extended Warranty Periods and Open Post-Processing Software for County-Level Medical Consortia, with Warranties Commonly Extended to Five Years.

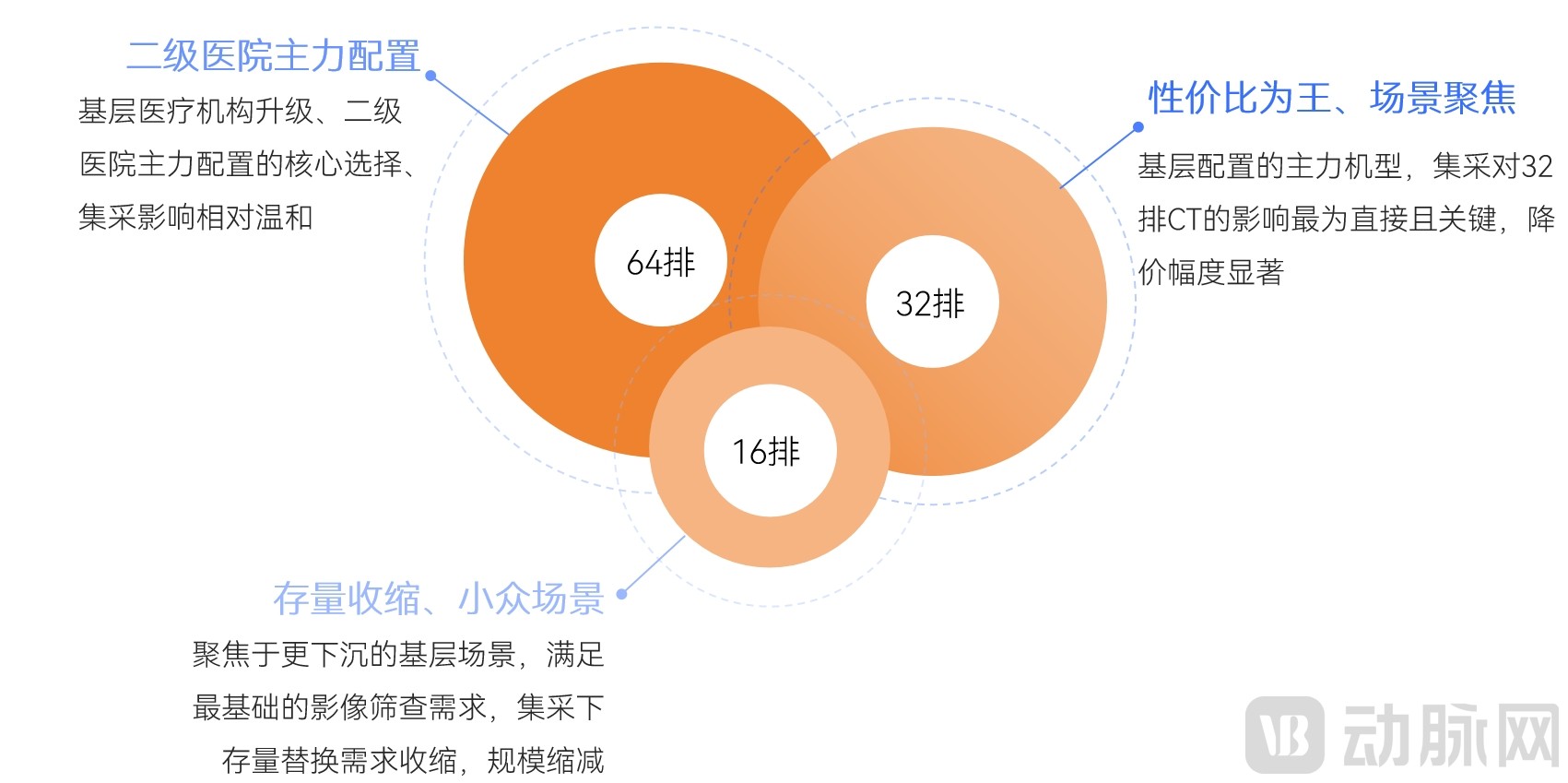

VBInsight believes that over the next 5 to 10 years, the development trends for CT scanners with 64 slices or fewer will be characterized by stratified consolidation, technological upgrades, and scenario-specific segmentation. Additionally, as a core policy variable, centralized procurement will profoundly influence the development trajectories, market landscape, and manufacturer strategies for various mid- to low-end CT models, with significantly differentiated impacts on 64-slice, 32-slice, and 16-slice CT systems. Specifically:

Figure: Development Trends of 64-Slice, 32-Slice, and 16-Slice CT Scanners Under the Centralized Procurement Framework

Source: VBInsight

Furthermore, the deregulation of clinical exemption policies at the registration stage has provided significant benefits to the low- and mid-end CT industry by lowering entry barriers, improving efficiency, and accelerating the substitution of domestically produced devices. On April 29, 2026, the National Medical Products Administration (NMPA) released the “Catalogue of Medical Devices Exempt from Clinical Evaluation (2026 Draft for Comment),” which includes routine CT scanners with 64 slices or fewer in the clinical exemption category. This means that standard CT systems with 64 slices or fewer may be exempt from clinical trials.

As a result, this will significantly shorten the product registration cycle, reduce clinical investment and certification costs, substantially lower the entry barriers for small and medium-sized manufacturers, accelerate the launch of new products and expand supply in primary healthcare markets, thereby further promoting the domestic substitution of mid- to low-end CT scanners.

Meanwhile, the lowering of entry barriers will attract a large number of companies to deploy conventional models with similar specifications, intensifying homogeneous competition and price wars in the 64-slice and below CT segment. This will accelerate the reshuffling of the existing market, leading to the gradual exit of small and medium-sized manufacturers lacking cost control and channel advantages.

For companies primarily positioned in the low-to-mid-end CT market, market consolidation is inevitable, making transformation an imperative path. However, the investment costs, difficulties, and feasibility of moving upmarket to high-end segments, expanding overseas, or focusing on niche markets vary significantly. The suitability, advantages, and challenges differ accordingly for each strategy, as detailed below:

Figure: Comparison of Three Transformation Pathways

Data Source: VBInsight

Overall, the cost of expanding overseas is lower than that of investing in upstream R&D, and competition is less intense, making it a potentially viable short-term survival strategy. Under competitive pressure from companies such as United Imaging Healthcare, it is challenging for firms focused on mid- to low-end CT systems to achieve technological breakthroughs in the mid- to high-end segments and build their brands. By leveraging appropriate overseas marketing channels and partners, these companies may generate certain cash flows in international markets, sustain operations, and create opportunities for future mergers, acquisitions, or collaborations.

Figure: Comparison of Competitiveness and Input Costs Under Three Transformation Pathways

Source: VBInsight

Segmented Scenarios: Four Major Categories Each Hold Their Ground, with Medical Essentials Leading and Pet Care Filling the Growth Gap

In recent years, with the refinement and precision of clinical diagnosis and treatmentRising DemandCT systems for specialized scenarios, such as intraoperative CT, large-bore CT for radiotherapy, and mobile CT, are gradually gaining prominence. Leveraging their strong adaptability to specific clinical settings and outstanding clinical value, these systems are penetrating multiple fields, including clinical diagnosis and treatment, emergency medical care, and veterinary medicine. Although their market size is smaller than that of mid-to-high-end CT systems, they are experiencing significant growth, emerging as a new highlight in the CT industry, with a relatively clear competitive landscape.

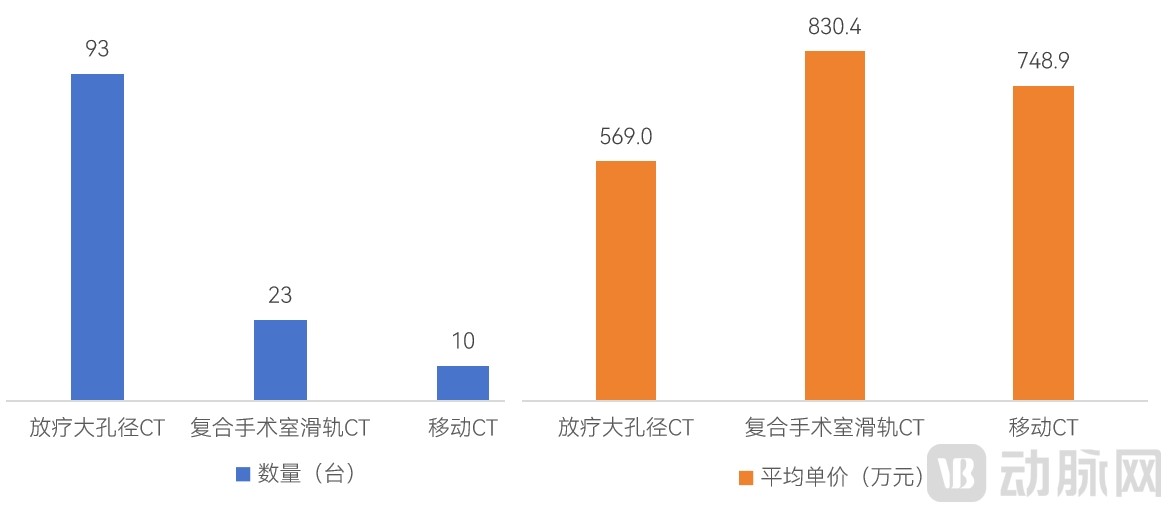

Taking the 2025 bid award data as an example, the publicly disclosed number of awarded bids for large-bore CT scanners for radiotherapy, hybrid operating room rail-mounted CT scanners, and mobile CT scanners was 93, 23, and 10 units, respectively, with average unit prices of RMB 5.69 million, RMB 8.304 million, and RMB 7.489 million, respectively, as detailed below:

Figure: 2025 Winning Bid Quantities and Average Unit Prices for Large-Bore CT for Radiotherapy, Hybrid Operating Room Rail-Mounted CT, and Mobile CT

Data Source: Public Tendering and Bidding

It is worth noting that pet CT scanners, as specialized equipment focused on the field of veterinary medicine, have not yet been included in the regular procurement systems of public hospitals. However, they represent one of the fastest-growing categories within niche CT applications, with their core growth driven by the rapid rise of the veterinary healthcare industry and the upgrading of diagnostic and treatment needs for pets.

In the future, as precision medicine is implemented, primary healthcare capacity is expanded, and emergency medical systems are improved, market demand for CT scanners across various specialized scenarios will continue to be released steadily. On the technological front, overall development will iterate toward intelligence, integration, and scenario-specific applications, with equipment becoming deeply integrated into clinical diagnosis and treatment workflows.

Innovation: Accelerated Localization of X-ray Tubes, Bundled After-Sales Services Become an Industry Trend

X-ray Tube: Compatibility Policies Remain Inadequate, with Liquid-Bearing Technology as the Core Direction for Iterative Development

The dumping of imported X-ray tubes has impacted the domestic industry, while anti-dumping investigations have created a policy window for domestic substitution. Currently, China has become the world’s largest consumer market for medical CT X-ray tubes, with domestic demand showing a continuous growth trend.

From 2022 to 2024, the domestic demand for medical CT X-ray tubes in China was 16,478 units, 16,844 units, and 17,119 units, respectively. Policy support for the domestic substitution of CT X-ray tubes has been substantial. On April 4, 2025, the Ministry of Commerce initiated an anti-dumping investigation into imported medical CT X-ray tubes originating from the United States and India, marking China’s first-ever investigation into industrial competitiveness concerning imported medical CT X-ray tubes.

This anti-dumping investigation has provided a strategic window for the industrialization of domestically produced CT X-ray tubes. Since 2025, the market share of Chinese-made CT X-ray tubes has steadily increased. This marks not only China’s first anti-dumping investigation targeting CT X-ray tubes—a core component of high-end medical equipment—but also represents a profound contest for supply chain dominance.

New Industry Registration Regulations Raise Reliability Thresholds, Promoting Standardized Development. In March 2026, the “Guiding Principles for Registration Review of Reliability Evaluation of X-ray Tube Assemblies for CT” were officially released, marking the continuous improvement of China’s regulatory policies on CT tube approval and replacement tube oversight.

The guidelines have introduced a new reliability review phase, imposing stricter requirements on tube life testing and compatibility testing. This has made the registration and certification process more rigorous and standardized, effectively raising the industry entry barrier.

On this basis, the regulatory framework for the substitution of X-ray tubes is also becoming increasingly clear. Previously, there was a certain gray area in the regulation of domestically produced X-ray tubes for substitution applications—OEMs were concerned that using third-party X-ray tubes might affect machine performance or pose safety hazards, leading to occasional disputes in the market and requiring the Market Supervision Administration and the Drug Administration to devote resources to coordination and resolution.

As the policy framework continues to be refined, these issues are gradually being resolved. Currently, the National Medical Products Administration (NMPA) has explicitly encouraged the development of domestically produced X-ray tubes and has established a standardized framework for reliability evaluations, laying the foundation for further refinement of compatibility assessment criteria in the future.

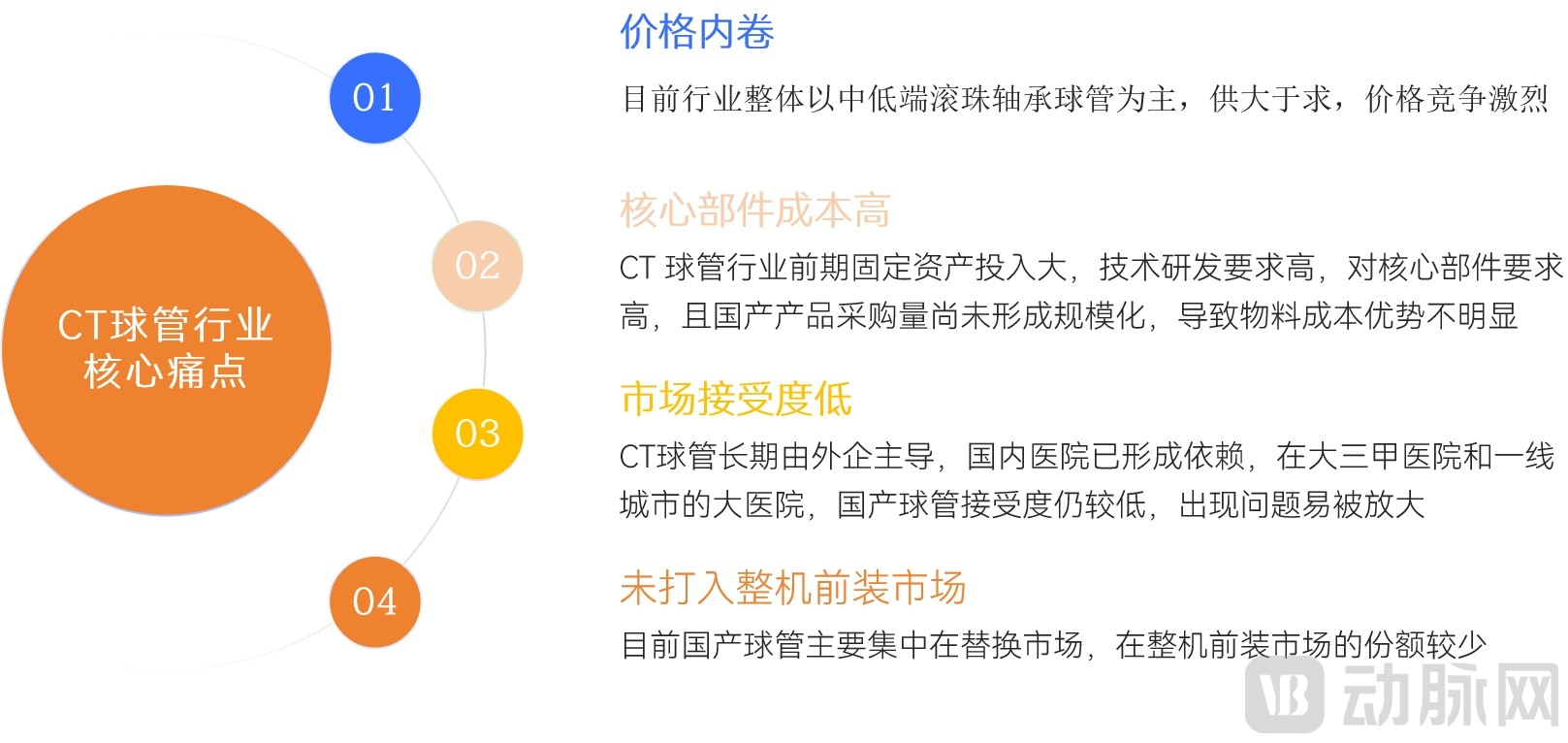

Despite policy support, domestically produced X-ray tubes in China still face four core pain points: intense price competition, high costs of core components, low market acceptance, and limited penetration into the original equipment manufacturer (OEM) pre-installation market.

Figure: Core Pain Points in China’s Domestic X-ray Tube Industry at the Current Stage

Source: VBInsight

The manufacturing difficulty of X-ray tubes lies in the bottleneck constraints on their core components, such as liquid metal bearings and anode disks.In the evolution of core technologies for medical imaging equipment, the emergence of liquid metal bearings is regarded as a watershed moment in the history of CT X-ray tube development.Compared with traditional ball bearings, the use of liquid metal bearings offers at least four advantages:

Figure: Advantages of Liquid Metal Bearing Technology

Data source: VBInsight

On the other hand, liquid metal bearing X-ray tube structures are complex and involve intricate manufacturing processes, with multiple technical bottlenecks present in core production stages.The overall process chain is long, with high technical barriers, and has long faced multi-dimensional “chokehold” challenges, resulting in extremely high thresholds for industry R&D and mass production.Despite the high barriers to entry in the industry, a few companies have successfully achieved independent breakthroughs and industrialization by leveraging their profound technological accumulation and systematic R&D layout.

As Zhishu Technology took the lead in mastering liquid-bearing axis technology, its self-developed X-ray tubes now cover all mainstream 64-slice CT models on the market and have surpassed the 8-million heat unit (MHU) threshold. Its 30-MHU product, currently the most advanced single-ended high-voltage liquid-bearing axis X-ray tube available, is also scheduled for launch this year. The company’s products are already exported to more than 20 countries overseas, with annual sales exceeding RMB 100 million in 2025.

As the core direction for the iterative upgrade of CT X-ray tubes, liquid metal bearings possess significant dual value in both technology and commercialization. Leveraging their comprehensive advantages, liquid metal bearings have become the core technological support determining the future development of CT X-ray tubes, leading the trajectory of technological upgrades and shaping the competitive landscape of the market.

From a commercialization perspective, liquid metal bearings are compatible with high-end models. With the continuous maturation of liquid metal bearing technology and the decline in mass production costs in recent years, their application is no longer limited to high-end CT scanners but has begun to extend to mid-range models, thereby broadening their application scenarios and market potential.

The anode target disk of the CT X-ray tube performs the core function of X-ray generation, with stringent technical requirements for its structure, material selection, and high-temperature welding. The primary role of the anode target disk is to receive bombardment by high-energy electron beams to generate X-rays. Its performance and reliability significantly influence the service life of the X-ray tube, imposing rigorous demands on raw material properties, heat dissipation design, stability during high-speed rotation, and manufacturing processes.

Furthermore, the stringent requirements for high-temperature tolerance, weldability, and material purity create extremely high barriers to the manufacturing processes of anode target disks. Weirui Technology has overcome key technical challenges; its independently designed rotating anode targets demonstrate significantly improved heat dissipation efficiency and service life. It is the only enterprise in China with mature, independent manufacturing capabilities for both core components—the “anode target disk” and the “liquid metal bearing”—and possesses R&D and manufacturing expertise for both molybdenum-based and steel-based liquid metal bearings.

At the current stage, the primary gaps between domestically produced X-ray tubes and top-tier foreign counterparts are manifested in two aspects: the lack of breakthroughs in high-end tubes and insufficient stability in mid- to low-end tubes.

On the one hand, domestically produced low- and mid-end X-ray tubes have essentially resolved the challenge of going from zero to one; however, breakthroughs in high-end X-ray tubes are urgently needed. After years of development in China’s CT X-ray tube industry, ball-bearing X-ray tubes for systems with fewer than 64 slices have basically overcome the hurdle of moving from nonexistence to existence, enabling domestic manufacturing capabilities.

However, in the mid-to-high-end segment, such as X-ray tubes compatible with CT scanners of 64 slices or more, particularly those with liquid metal bearings, the technology remains immature and imperfect, awaiting breakthroughs. High-end X-ray tubes rely on imports. Globally, only four foreign companies—GPS (GE Healthcare, Philips, Siemens Healthineers) and Canon—can produce liquid metal bearing tubes, and they do not sell them externally. Domestic X-ray tube manufacturers must independently overcome these technical challenges, and there is currently a significant gap in this area.

On the other hand, domestically produced mid-to-low-end X-ray tubes exhibit inferior reliability and consistency. From a product perspective, the gap between domestic and imported X-ray tubes is primarily reflected in quality reliability and stability. Domestic mid-to-low-end X-ray tube products lag behind their foreign counterparts in process consistency, mainly due to smaller production scales that have not yet achieved mass manufacturing status.

If top-tier foreign products are rated a perfect 10, then leading domestic products would likely score around 7; while a gap remains, progress is being made rapidly.In the future, with the large-scale release of domestic production capacity for X-ray tubes, continuous optimization of manufacturing processes, and improved policies, the industry will see significant improvements in process standardization and procedural normalization. This will gradually narrow the gap with imported products in terms of service life, operational stability, and batch-to-batch consistency.

Trends: AI-empowered CT, comprehensive after-sales service packages, and more standardized spare parts management

At this stage, AI is deeply integrated with ultra-high-end CT and MRI systems, no longer serving merely as an auxiliary tool but becoming a core component of the equipment’s performance.

An integrated, multimodal, end-to-end AI-driven intelligent solution for disease-specific diagnosis, treatment, and management, combining software and hardware. It covers the full spectrum from screening and assessment to diagnosis, treatment, research, and management. By enabling deep synergy with high-end CT and MRI equipment, it visually demonstrates a leapfrog upgrade of AI technology—from empowering single-point tools to empowering entire workflows, and from technological demonstration to realizing scenario-based value—while also providing a new pathway for monetizing the clinical value of high-end imaging equipment.

Overall, the evolution of medical AI’s intrinsic capabilities has propelled it to a new position. As the potential of the physical architectures of photon-counting CT and MRI approaches its limits, the outcome of the competition in software intelligence will determine who occupies the new strategic high ground and will reshape the competitive landscape of the entire high-end medical imaging equipment sector.

On CT systems, specialization is becoming the core direction for breakthroughs.Traditional general-purpose CT scanners often adopt an "all-in-one universal design" to meet the routine examination needs of multiple departments. However, in certain specialized fields, pain points persist, including insufficient specialization, low scanning efficiency, and image details that fail to meet the diagnostic standards required by specific specialties.

Specialized CT innovation is centered on extreme adaptation to specific clinical scenarios, forming differentiated layouts across multiple tracks, such as large-bore CT for radiotherapy. Additionally, dedicated orthopedic CT and dedicated cardiovascular CT follow the same principle.

On the other hand, morphological innovations, such as weight-bearing CT, represent a major direction for innovation. Traditional CT scanning relies on patients lying in a supine position; however, gravity can cause displacement of visceral organs and alter the mechanical loading on the musculoskeletal system, leading to a "mismatch" between clinical diagnosis and imaging findings.

For instance, in lumbar disc herniation, increased intervertebral disc compression during standing makes the herniation more pronounced, whereas lying down often “masks” the lesion due to positional relaxation, easily leading physicians to misjudge the condition. This contradiction has long plagued departments such as orthopedics, oncology, and pulmonology, even resulting in deviations in treatment plans and surgical planning.

In contrast, standing CT can reveal dynamic physiological or pathological changes induced by gravity (body weight) and load that are undetectable in conventional supine CT scans. It provides a novel platform for studying anatomical and physiological changes under gravitational conditions, thereby opening new avenues for scientific and clinical research across various medical specialties.

Currently approved representative products in China include: In April 2024, Kaiying Medical launched Standing 128, China’s first precision tomographic standing CT system developed independently; on September 8, 2025, the NMPA officially approved the market launch of OmegaCT One, independently developed by Sinovision Technology, which is the world’s first standing whole-body spiral CT with a super-large 1-meter bore.

Furthermore, against the backdrop of centralized procurement, the industry faces mounting cost pressures. To meet the demand for low-cost procurement at the primary care level, entry-level CT systems have begun incorporating DR X-ray tubes as a substitute for traditional dedicated CT X-ray tubes. This approach enables basic CT scanning and imaging capabilities at a lower hardware cost, representing a significant innovation pathway for cost reduction and efficiency improvement in mid-to-low-end CT scanners, thereby aligning with the pricing framework of centralized procurement.

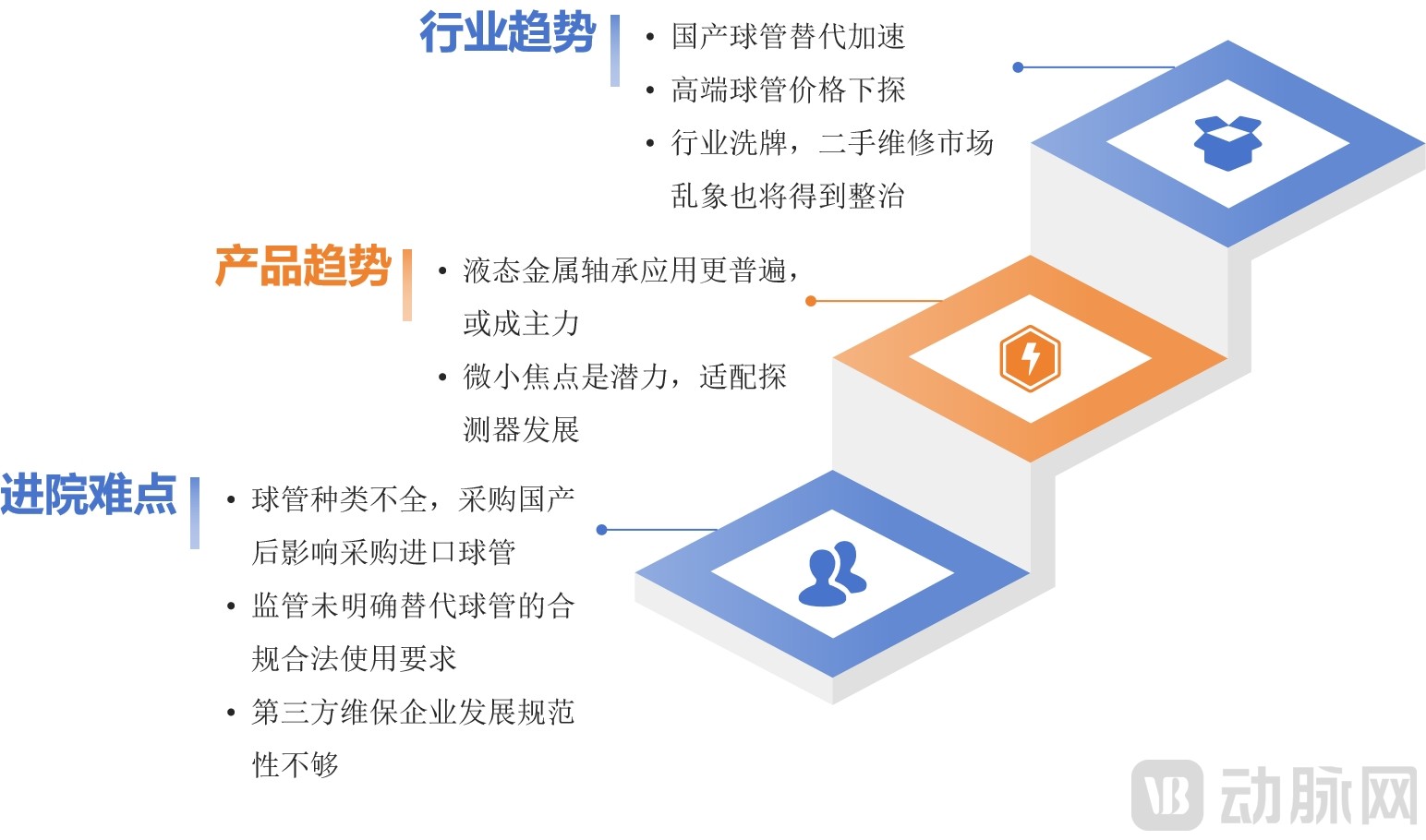

Figure: Challenges in Hospital Adoption of Domestically Produced CT X-ray Tubes and Future Trends

Source: VBInsight

After-sales services may be delivered through comprehensive managed solutions or bundled packages, ranging from single-point maintenance to full-lifecycle value management. Amid the industry shift from incremental procurement to installed-base operations and maintenance, after-sales service for CT equipment is transitioning from the traditional model of “passive breakdown repair and OEM-only maintenance” to an innovative paradigm characterized by “proactive full-lifecycle management and comprehensive bundled managed services.” Third-party maintenance providers are also accelerating their market penetration, leveraging cost advantages and service flexibility, thereby becoming a core driver of industry transformation.

For example, some county-level medical consortia have achieved centralized management of all imaging equipment within their jurisdictions by introducing comprehensive trusteeship services.

Furthermore, spare parts management and supply chain innovation remain challenges to be addressed. Spare parts supply is the core guarantee of CT after-sales service; however, the current CT spare parts industry suffers from the key pain points of being “slow, expensive, and counterfeit.” This severely constrains the improvement of quality and efficiency in after-sales services, increases the operational and maintenance burden on healthcare institutions, and even affects the orderly conduct of clinical diagnosis and treatment.

Based on the report’s analysis of innovation in the CT industry and corporate practical initiatives, this report selects ten exemplary cases of innovation in the CT industry:

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:

Chapter 1 Overview: CT System Architecture Upgrades and Concentrated Capital Investment in Components

1.1 Phase: A Dual Phase of Maturity and Structural Upgrading, with Steady Market Growth

1.2 Financing: Tilted toward core components, with concentrated bets on X-ray tubes

1.3 Market: Stable Volume and Rising Prices, Premiumization, and Penetration of Domestic Products

Chapter 2 Products: High-End CT Dominates the Market, Niche Scenarios Create Blue Oceans

2.1 Ultra-High-End: Photon-Counting CT Leads the Way, Phased-Array CT Achieves Breakthroughs

2.2 Mid-to-Low End: Volume-Based Procurement Deeply Reshapes the Market, Making Transformation an Imperative Path

2.3 Sub-segments: Four Major Categories Maintain Their Respective Tracks, with Medical Essentials Dominating and Pet Care Filling the Growth Gap

Chapter 3 Innovation: Accelerating Localization of X-ray Tubes, with Bundled After-Sales Services Becoming an Industry Trend

3.1 X-ray Tube: Compatibility Policies Remain Imperfect, with Liquid-Metal Bearing Technology as the Core Direction for Iterative Development

3.2 Trends: AI-Empowered CT, Comprehensive After-Sales Service Bundling, and More Standardized Spare Parts Management

Chapter 4 Corporate Case Studies

4.1 ZhiShu Technology: The Creator and Leader of Liquid Metal Bearing CT X-ray Tubes in China

4.2 Advanced Tech Group: Anchoring in Core Technologies to Build a Full Industrial Chain for High-End Medical Imaging

4.3 Weirui Technology: A Technology-Driven Provider of X-Ray Solutions

Please scan the QR code to add our assistant and obtain the full report. If you have already added us, please initiate a conversation:

Special Acknowledgments (in the order of research interviews):

Mr. Zhang Mengru, Partner at Leli Capital,Mr. Yue Dongxiao, Head of Industry Research at Leli Capital,Ms. Liu Haitao, Executive Director of Investment Management Department II, Shanghai State-owned Capital Venture Guide Fund,Mr. Li Chenxi, Partner at Enshe Family Office,Mr. Hu Qiupeng, Partner at Shanghai Bainuo Capital,Mr. Su Xiaoping, Vice President of Xiandao Group & Chairman and CEO of Alltech Medical SystemsMr. Nie Xipeng, Founder and General Manager of Weirui Technology; Mr. Hu Yinfu, Founder and General Manager of Zhishu Technology