2026 Report on Healthcare Large Model Commercialization: Application Implementation and Business Closure as the Industry's Core Theme

After just a few years of practical refinement, large medical models have successfully moved past their nascent and explosive growth phases, entering a new stage characterized by the clearing of industry bubbles and a gradual shift toward rational, stable growth. Through surveys and interviews with more than ten innovative enterprises, three investment institutions, and several clinical experts, this report examines the current state of commercial deployment of large medical models both within and outside hospitals. It analyzes business models, implementation pain points, and core prerequisites across different scenarios, summarizes future development trends, and aims to provide reference for industry participants, thereby helping large medical models truly empower the high-quality development of the healthcare sector.

The views are as follows:

1. From the perspectives of policy orientation, technological iteration, and capital allocation, jointly promoting application implementation and achieving a closed-loop commercialization model has become the core theme of industry development.

2. On-premises implementation of IT upgrades is the mainstream trend, yet its value is underestimated: Within hospitals, large medical language models are primarily commercialized through three models: upgrading traditional health information systems, registration as medical devices, and inclusion as a cost item in healthcare services.

3. Commercial implementation faces fewer barriers in out-of-hospital settings, which are categorized into three major models: ToG (to Government), ToB (to Business), and ToC (to Consumer). Among these, the ToB model is the most mature in terms of deployment; the ToG model focuses on primary care and regulatory scenarios; and the ToC model exhibits trends toward functional aggregation and diversified business models.

4. Future large medical models will exhibit a trend of deep specialization within hospitals and diversified integration outside hospitals. Consumer-facing scenarios will gradually transition from single-service offerings to full-cycle health companionship, while diverse payment models will become the core support for scalable implementation.

Since the initial exploration and pilot applications of large medical models began in 2023, their technological and application development has accelerated continuously, driven by a combination of factors including capital investment, technological iteration, policy guidance, talent supply, and market demand. The overall pace of development has significantly outstripped that of traditional medical technologies, steadily advancing the field of medical artificial intelligence toward maturity and refinement.

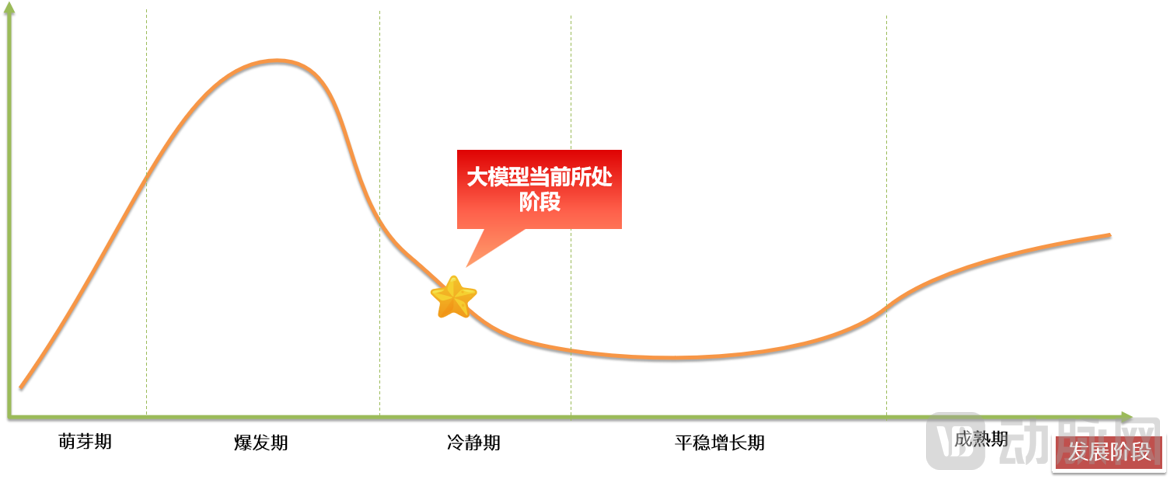

After three years of practical exploration and industry refinement, large medical models have moved past the nascent and explosive growth phases. The sector is currently undergoing a rationalization process, clearing out market bubbles and entering a more sober period characterized by steady growth and sustained maturity.

Development Stages of Large Medical Models

During this critical phase of development, industry-related policies have successfully undergone a breakthrough transition from encouraging technological innovation and exploration to promoting practical application and refining payment systems, achieving significant policy milestones. Regulatory authorities and governing bodies have sequentially introduced a series of practical, implementable application scenarios, while approving nearly 300 registration certificates for AI-based medical devices. Furthermore, healthcare security administration departments in multiple regions across China have formally incorporated AI-related medical service items into the national medical insurance reimbursement coding system.

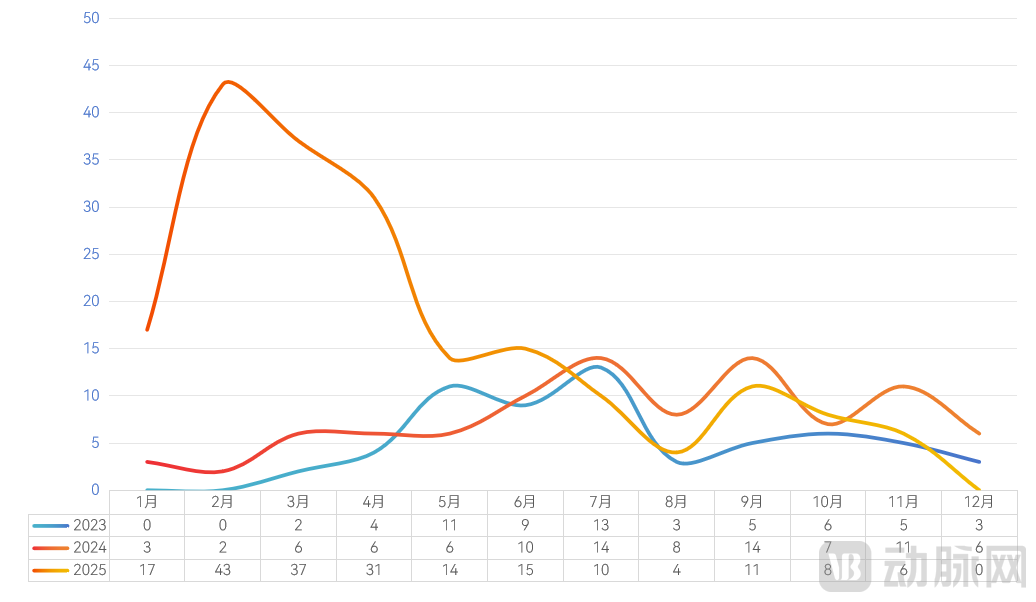

Meanwhile, the pace of centralized launches for various large medical models within the industry has shown a clear slowdown. The period of explosive, concentrated releases and rapid growth witnessed in the first half of 2025 has passed. Large model products developed by various industry participants have now entered a phase characterized by continuous refinement, precise iterative upgrades, and in-depth specialization. This indicates that the industry gaps requiring coverage by large medical models are diminishing, with the focus shifting towards making these models “more user-friendly” and “smarter.”

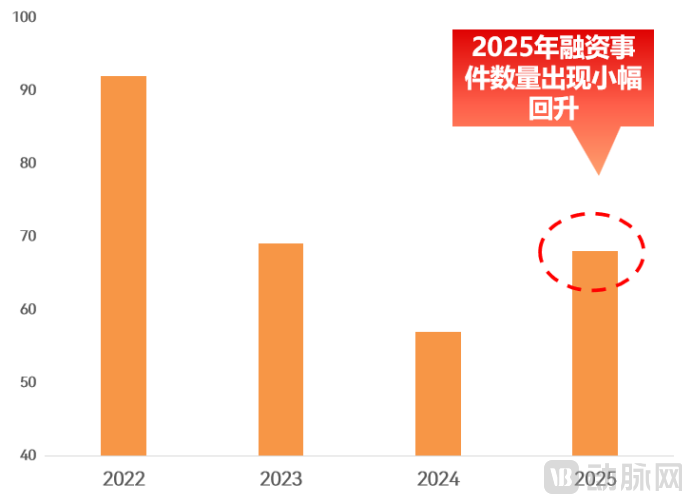

From the overall performance of the capital market, the rapid rise of large medical models has driven a moderate increase in the number of investment and financing activities across the entire medical AI sector. As industry investment logic shifts from a sole focus on R&D capabilities to prioritizing application scenarios and practical implementation outcomes, the distribution of financing rounds exhibits a typical dumbbell-shaped structure. Capital is increasingly concentrating on medical large model enterprises that offer clear application scenarios and demonstrate strong execution capabilities and growth potential.

Currently, the entire healthcare large language model (LLM) industry is at a critical inflection point, transitioning from a period of rational cooling to one of steady growth. Driving the practical deployment and application of technologies and products has become the central theme in the industry’s development.

Hospitals are the primary setting for the intensive deployment of large medical models. According to VCBeat’s “2025 Report on the Medical Artificial Intelligence Industry,” similar to other AI applications, the in-hospital use cases of large models can be categorized into three major groups: clinical departments, diagnostic and technical departments, and hospital-level operations.

Clinical DepartmentsThe functionalities of large medical models in this scenario primarily revolve around assisted diagnosis, physician assistance (such as medical record organization and literature search), and scientific research. According to surveys, the penetration rate of large models for assisted diagnosis and physician assistance is continuously increasing. Furthermore, with the emergence of large-model-based agents and increasingly convenient model access interfaces, the commercialization process of large models for clinical research has become relatively more mature.

Medical Technology DepartmentLarge models focused on assisted diagnosis benefit from clear performance validation standards (such as sensitivity and specificity) and the ability to verify their “effectiveness” through existing medical device approval pathways. Consequently, product commercialization in hospital settings is relatively advanced, although these solutions remain in the stage of awaiting scaled commercial deployment.

Hospital SideCompared with large models designed for clinical and medical technology departments, this type of large model is more service-oriented, with its commercialization loop focusing more on efficiency and cost control. For example, Neusoft Group has implemented comprehensive, multi-scenario deployments tailored to hospital needs. Based on its Tianyi Medical Large Model, it has developed over 120 “AI agents” covering smart clinical care, smart management, and smart services, achieving scaled application in more than 100 medical institutions across China.

The deployment of large medical models typically exists as a technological foundation, fully demonstrating their intelligent value and core role by empowering various specific medical applications. Meanwhile, some large medical models adopt the “model-as-application” approach, being directly applied to diverse specific medical scenarios to achieve direct integration between technology and clinical contexts.

Sales Models of the Four Mainstream Large Medical AI Models. When large medical AI models are marketed, their product forms exhibit diverse characteristics. Based on industry practices and current market conditions, they can be broadly categorized into four types: software-based solutions, integrated hardware-software systems, service-oriented offerings, and industry foundational platforms.

Four Major Product Forms of Large Medical Models

Within hospital settings, different product forms correspond to distinct business models. Currently, the commercial implementation of large medical models (including AI applications empowered by large medical models) in hospital scenarios has not deviated from traditional existing commercialization patterns within hospitals, and can be broadly categorized into three types: information systems, medical devices, and health services. Taking health services as an example, this model leverages the medical authority and high-quality physician resources of public hospitals to ensure the professionalism and standardization of health management services, while also utilizing the personnel and service advantages of professional health management organizations. This achieves complementarity between medical resources and health management services, promoting the development of health management services toward greater standardization and refinement.

In this collaborative model, large medical AI models are typically developed by health management enterprises. Rather than being sold as products to healthcare institutions, they are deeply integrated into the companies’ own health management teams to expand the upper limit of service capabilities, thereby achieving cost reduction and efficiency improvement. For instance, JD Health, leveraging its “JD Zhuoyi 2.0” platform, collaborated with the First Affiliated Hospital of Wenzhou Medical University and the NHC Key Laboratory of Clinical Nutrition and Intervention to jointly release an “AI-Driven Standardized Full-Process Management Solution for Clinical Nutrition.” This initiative establishes a “Clinical Nutrition + Foods for Special Medical Purpose (FSMP)” network, addressing pain points in nutritional assessment and intervention for both inpatients and outpatients, and incorporating nutritional therapy into traceable and evaluable clinical pathways.

In out-of-hospital settings, the primary business models for large medical AI models can be categorized into three main types: those targeting government entities, enterprises, and individual consumers (B2C).

Primary care is one of the four major hotspots for the implementation of large medical AI models. Given that functions in primary care settings are strongly guided by policy, large medical AI models applied to key functional areas benefit from greater momentum for practical deployment. Upon closer examination of specific application scenarios, large medical AI models for imaging-assisted diagnosis, general practice, traditional Chinese medicine (TCM), and chronic disease management have emerged as focal points for implementation in primary care. By the end of 2025, the Intelligent Medical Assistant, powered by the iFlytek Spark Medical Large Model, had covered 31 provinces and municipalities across China, spanning 806 districts and counties, and serving more than 77,000 primary healthcare institutions. It has provided over 1.1 billion AI-assisted diagnostic recommendations, facilitated the generation of more than 450 million standardized electronic medical records, identified over 120 million inappropriate prescriptions, and prompted corrections leading to more than 1.95 million clinically valuable diagnostic adjustments. These large-scale implementation outcomes substantiate the core value of AI technology in empowering primary healthcare.

Cost reduction and efficiency enhancement are strong drivers for the deployment of B-side large medical models. In application scenarios where large models can significantly improve efficiency and reduce costs, there are already numerous mature commercial implementations on the B-side, including scaled deployments. Focusing on out-of-hospital application scenarios for large models, this section analyzes pharmaceutical companies, out-of-hospital health service providers, and insurance companies as the primary paying entities.

(1) Innovative Pharmaceutical Companies

Large medical models are deeply integrated into the entire drug development process, empowering every link from target discovery and molecular design to clinical trial optimization. This directly addresses the longstanding pain points of traditional new drug R&D, namely long development cycles, high costs, and low success rates. For instance, large models also play a significant role in the post-marketing phase. While China now ranks second globally in the number of innovative drugs launched, challenges such as difficult hospital access and reimbursement for high-value innovative medicines remain prominent. Exorbitant pricing limits drug accessibility and further hinders the conversion of innovative achievements into financial support for sustained corporate R&D.

The in-depth application of artificial intelligence technologies, represented by large language models, has become a key lever for addressing this pain point. For instance, Medbanks Health provides pharmaceutical companies with AI-powered “Smart Pharma” solutions, offering comprehensive commercialization strategies across the entire drug lifecycle—including market insights, patient management, and channel planning—to help pharmaceutical firms integrate diverse healthcare payment mechanisms. According to its prospectus, from January to October 2025, 62.7% of Medbanks Health’s revenue came from its Smart Pharma solutions. The company has partnered with more than 140 pharmaceutical enterprises, including 90% of the top 20 global pharmaceutical companies.

(2) Out-of-Hospital Health Service Providers

Large medical AI models are deeply penetrating the entire healthcare service workflow and organically integrating the full ecosystem of out-of-hospital health management, directly addressing the industry’s long-standing core pain points: severe service homogenization, low operational efficiency, and insufficient personalized interventions.

Addressing the differentiated demands of various B-end clients, Zhizhen Technology has developed tailored, tiered solutions. On one hand, it delivers underlying model and medical tool capabilities via an open platform using APIs, tokens, and other methods to serve enterprise clients with R&D capabilities. On the other hand, leveraging WiseClaw—the world’s first medical Agent platform—as its core infrastructure, and integrating technical modules such as MCP, Skill, OpenClaw, and Harness, it supports enterprises in building configurable, traceable, and governable medical AI agents. Furthermore, zero-code products like Expert Avatar H5 meet the lightweight application needs of professionals such as physicians and nutritionists. Currently, Zhizhen Technology has partnered with over 300 top-tier Grade A tertiary hospitals and more than 500 leading healthcare enterprises across China, demonstrating the deployment capability and market validation of its medical AI products in real-world business scenarios.

(3) Insurance Company

In recent years, with the rise in national income levels and growing health awareness, the share of commercial health insurance in the payment system has been gradually increasing. In response to a market characterized by a wide variety of products and complex policy terms, comprehensive service providers covering the entire lifecycle of commercial insurance products have emerged. These entities not only assist insurers in product design but also build bridges connecting consumer bases with major insurance companies, offering one-stop services that span sales, underwriting, and claims processing, thereby effectively addressing the challenge of matching supply with demand.

In the field of innovative drugs, the value of third-party platforms is particularly prominent. As multi-payer systems remain an emerging sector, third-party platforms leverage their established expertise and experience to accelerate collaboration between pharmaceutical companies and insurers, thereby increasing the success rate. Furthermore, when confronted with complex cross-regional business scenarios, these platforms assume the burden of intricate calculations and assessments, significantly reducing the input costs for both pharmaceutical enterprises and insurance institutions.

The consumer-facing (C-end) sector represents the most diverse scenario for exploring the commercialization of large medical AI models. Taking health management as an example, it is not only a critical health need for individuals with chronic diseases but also an urgent, unmet demand for medical insurance providers, commercial insurers, pharmaceutical companies, enterprises, and clinical research. Consequently, the payers and business models in chronic disease management exhibit significant diversity.

Drawing on the white paper’s innovative analysis of scenario-based implementation of large medical models and corporate practical initiatives, this report has selected ten outstanding cases demonstrating the application value of large medical models. (The above is an excerpt from the main content of the report; scan the QR code in the figure below to access the full report.)

The above is an excerpt from the report. Scan the QR code below to access the full report:

Special Thanks to the Following Experts for Their Strong Support of This Report (in Order of Interviews):

ZhiZhen Tech

Li Dong, Vice President of Neusoft Corporation and General Manager of the Healthcare Business Unit

Dr. Zhang Xia, Dean of Neusoft Research Institute and Dean of Neusoft Intelligent Medical Technology Research Institute

Liang JunzeDeputy General Manager, Healthcare Business Unit, Neusoft Group

He Zhiyang, Dean of the iFlytek Medical Research Institute

Ren Haiping, Researcher at the Institute of High-Performance Devices, Chinese Academy of Sciences

Experts from JD Health Exploration Research Institute (JDH XLab)

Liu Rongyun, Founder of Shengshengji

Zhang Xinyan, Founder of Huimei Digital Technology

Zhang Zhiyun, Co-founder of Nanda Feite

Li Linfeng, Vice President of Technological Innovation and AI Architect at Yidu Tech

Report Table of Contents:

Chapter 1: The First Year of Practical Implementation for Large Medical Models

1.1 Policy: Identify Scenarios, Develop Vertical Domains, and Facilitate Implementation

1.2 Technology: The explosive release of large models has come to a pause, with scenarios closely aligned with policy guidelines

1.3 Capital: Converging toward enterprises with clear application scenarios and strong implementation capabilities

Chapter 2: Current Status of Commercial Deployment of Large Medical Models Within Hospitals

2.1 Comprehensive Overview of In-Hospital Applications of Large Medical Models

2.2 Analysis of the In-Hospital Business Model for Large Medical AI Models

Chapter 3: Current Status of Commercial Deployment of Large Medical Models Outside Hospitals

3.1 Panorama of Out-of-Hospital Applications for Large Medical Models

3.2 Analysis of Out-of-Hospital Business Models for Large Medical AI Models

Chapter 4 Future Trends

4.1 In-Hospital Serious Medical Large Language Models: Building Trust Endorsement Through Specialty-Specific Entry

4.2 Limited Consumer-Side Monetization: Emergence of More Integrated and Diversified Commercial Models

4.3 Continuous Improvement of Infrastructure Accelerates the Deployment of Large Medical Models

4.4 The G-B-C Innovation Model: Tripartite Integration Driving a Value Cycle