Medical 3D Printing Market Enters Implementation Phase: Orthopedics Emerges as Key Battleground, Organ and Tissue Printing Achieves Breakthrough

Excellent

Digital Orthopedic Medical Products and Solutions Service Provider

As a representative technology in the field of advanced manufacturing, 3D printing has been widely applied across various industries, including aerospace, automotive manufacturing, healthcare, and culture, sports, and entertainment, driving industrial transformation and upgrading. According to forecasts by SmartTech, a giant in the 3D printing industry, the global market size for medical 3D printing will reach $8.9 billion in 2022, with North America holding the largest market share and the Asia-Pacific region experiencing the fastest growth.

From the perspective of the application stages of 3D printing in the healthcare industry, primary-stage applications such as dental restoration, customized prosthetics, surgical guides, and implants dominate the market. Due to advantages including a large market size, low market concentration, and increasingly mature technology applications, orthopedic implants have attracted widespread participation from various enterprises and are poised to become a key growth hotspot in the medical 3D printing market in 2018.

As an intermediate stage of medical 3D printing—simple organ tissues—bioprinting technology companies represented by Organovo and BlueLight Innovations have successfully printed cellular tissues, cartilage tissues such as ears, and vascular tissues, achieving success in trials and shortening the distance to human clinical applications. Medical 3D printing has entered a transitional period from the primary stage to the intermediate stage, with promising prospects for future development.

From the perspective of the capital market, domestic medical 3D printing companies are actively seeking capital investment. With the introduction of supportive policies by the China Food and Drug Administration (CFDA) for medical 3D printing and the increasing maturity of technological applications, 2018 may witness a surge in capital interest in medical 3D printing enterprises, particularly those specializing in orthopedic implants and organ/tissue engineering.

Report Description:

This report primarily employs literature review and field interviews. By systematically analyzing relevant data published by organizations such as the 3D Printing Medical Devices Professional Committee of the China Association for Medical Devices Industry, SmartTech Market, and Frost & Sullivan, and by conducting interviews with professionals in the medical 3D printing sector, it provides a detailed analysis of the current development status of the domestic medical 3D printing market.

Table of Contents:

I. 3D printing has a long history of development, with downstream application services becoming the primary driver of industrial growth

II. Progressive Improvement of Policies, Regulations, and Certification Systems

III. Enhanced Independence in R&D Technology, Narrowing the Gap with Foreign Counterparts

IV. North America Holds the Largest Market Share, While the Asia-Pacific Region Experiences the Fastest Growth

V. China’s Medical 3D Printing Market Enters a New Phase: Rapid Growth in Dental Restoration, Orthopedic Implants Become the Key Focus of Market Competition, and New Breakthroughs Achieved in Organ and Tissue Engineering

VI. Precision Medicine, Non-Transplant Applications of Organs, and New Drug R&D May Become Future Trends

Medical 3D Printing Has Entered a Transitional Phase from the Primary to the Intermediate Stage

China’s 3D printing technology sees enhanced indigenous innovation, narrowing the gap with foreign counterparts

The Policy and Regulatory Framework for Medical 3D Printing Is Being Gradually Improved

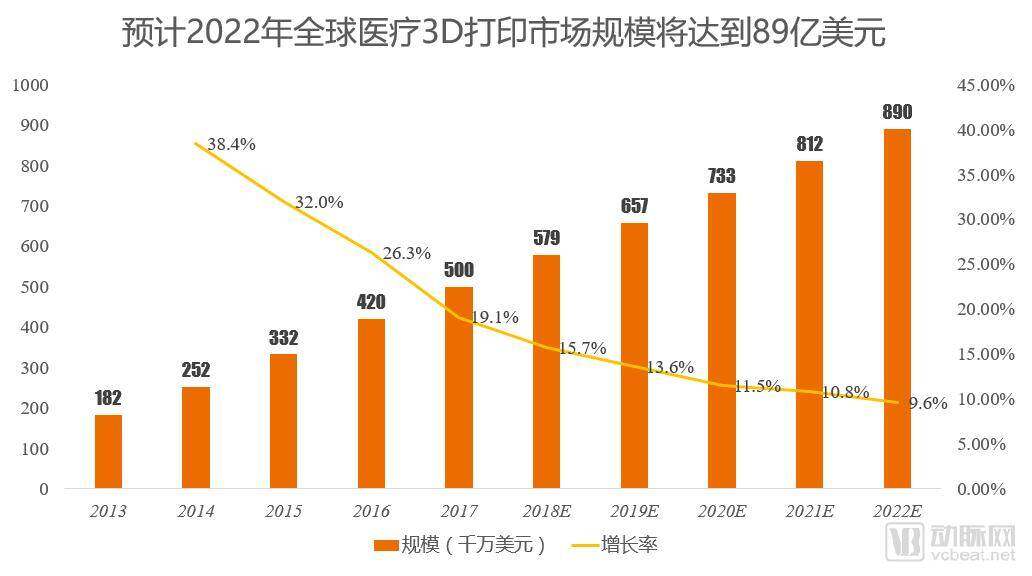

Medical: The global market size for 3D printing in healthcare is projected to reach $8.9 billion in 2022, with a compound annual growth rate (CAGR) of 17.2%.

Orthopedic implants account for 93% of the total implant market size, which is expected to reach RMB 29 billion by 2022.,Becoming a Key Battleground in the Medical 3D Printing Market

New Progress in Bio-3D Printing Product Trials: Promising Prospects for Future Human Clinical Applications

Key Charts:

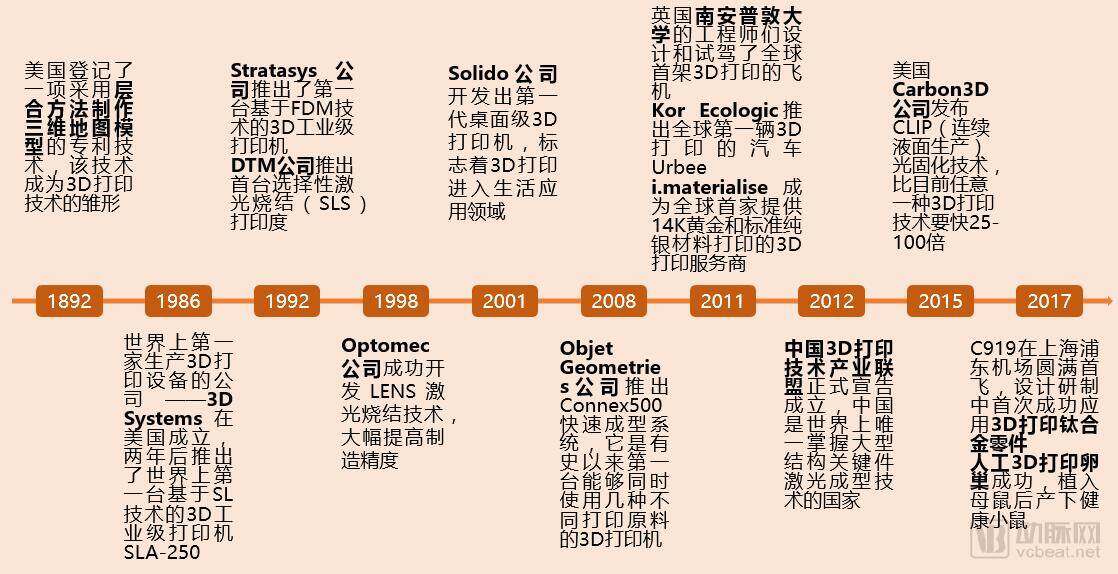

1. Milestones in the Development of 3D Printing Technology: The Evolution of 3D Printing Spans Over 100 Years

2. Development Stages of Medical 3D Printing: Organ and Tissue Printing Represents the Advanced Stage

3. Industry Chain Map of Medical 3D Printing: Application Services Become the Main Driving Force for the Development of the Medical 3D Printing Industry

4. Industrial Policies for Medical 3D Printing: Relevant Policies on Medical 3D Printing

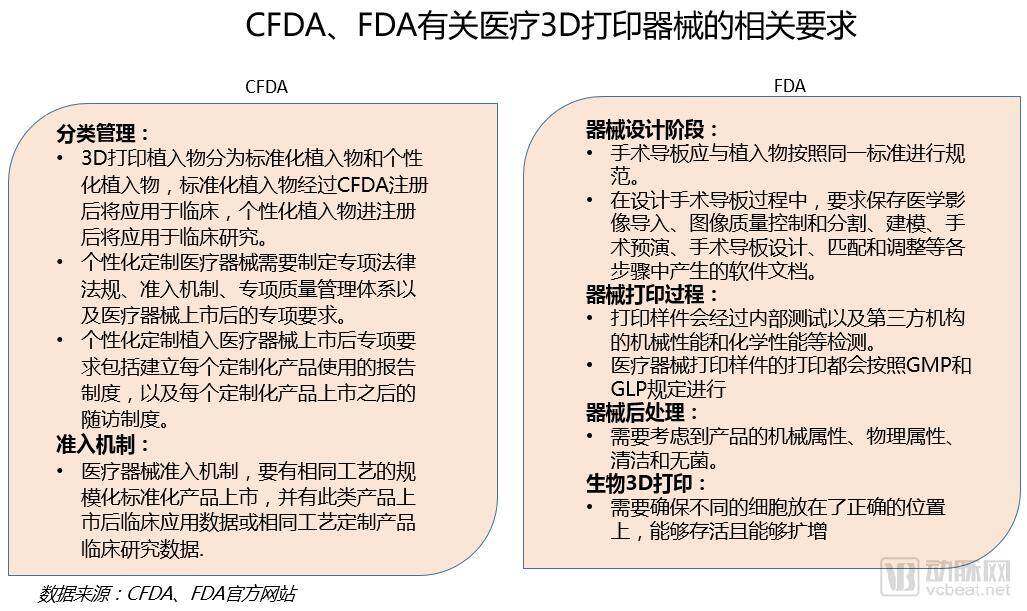

5. Relevant Requirements of the CFDA and FDA for Medical 3D-Printed Devices

6. Medical 3D Printing Technology: Comparison of the Basic Status of Mainstream 3D Printing Technologies

7. Global Market Size of Medical 3D Printing, 2013–2022

8. Market Share of Medical 3D Printing in Major Global Regions in 2017

9. List of 3D Printing Companies in China Involved in Dental Products

10. Market Size of Orthopedic Implants in China, 2013–2022

11. Volume of Orthopedic Implant Surgeries in China, 2013–2022

12. List of Medical Companies Specializing in 3D-Printed Orthopedic Implants

13. Major Events in China’s 3D-Printed Orthopedic Implants Industry in 2017

14. Major Events in the Field of Biological 3D Printing in 2017

15. Investment and Financing Status of Medical 3D Printing Enterprises in 2017

16. Operating Performance of AK Medical from 2014 to 2016

This article excerpts selected content from the report, including the development history, policies, and global market size of medical 3D printing. To read the full text, please long-press the QR code below to become a VCBeat member, access the complete report, and learn more about the current applications and future trends of medical 3D printing.

Scan the QR code to become a VCBeat member

3D Printing Has Been in Development for a Long Time, and Downstream Application Services Have Become the Main Driving Force for Industry Growth

3D printing technology is a technique that constructs physical objects by layer-by-layer printing, using bondable materials such as metal powders, nylon, and plastics based on digital model files. Traditional part manufacturing is achieved through material removal and machining processes, whereas 3D printing technology is realized through the gradual accumulation of materials.

Comparison of 3D Printing and Traditional Manufacturing Processes

From the perspective of process comparison, 3D printing technology can achieve high-precision printing through pre-modeling, offering high efficiency and material savings that are unmatched by traditional manufacturing processes.

3D Printing Technology Has Been Developing for Over 100 Years

Data Source: Compiled from Public Information

3D printing technology originated in the United States in 1892. After nearly a century of slow development, the launch of the world’s first industrial 3D printer by 3D Systems in 1988 marked the true commercialization of 3D printing technology. Subsequently, new technologies such as FDM, SLS, LENS, and CLIP emerged and were applied in fields including aerospace, automotive manufacturing, jewelry processing, and healthcare. The establishment of the China 3D Printing Technology Industry Alliance in 2012 signaled that 3D printing had been placed on the agenda for industrialized development.

China introduced 3D printing technology into the healthcare sector in the late 1980s, primarily to assist physicians in creating three-dimensional models of pathological lesions for preoperative planning and patient communication. With the advancement of 3D printing technology and its deep integration with medical practice, its applications have gradually expanded to include dental restoration, customized prosthetics, surgical guides, and implant manufacturing. In the future, it is expected to converge with biomedicine to enable the printing of simple viable tissues, such as cellular structures, and even complex organ tissues like livers and hearts.

Data source: The New World of 3D Printing

As a primary application area for 3D printing technology, the medical sector has attracted active strategic investments from both domestic and international companies due to its promising market prospects. These players range from large conglomerates such as Canon, Autodesk, Baoti Group, and China Nonferrous Metal Industry’s Foreign Engineering and Construction Co., Ltd. (CNFC), to startups like Organovo and Blue Light Yingnuo.

Clinical Applications Become the Primary Driver for the Development of the Medical 3D Printing Industry

As the foundation of 3D printing, software is predominantly imported due to factors such as substantial R&D investment, high-caliber R&D teams, and long development cycles. Companies like Autodesk, SOLIDWORKS, and Materialise monopolize 70% of the modeling software market share.

Currently, the medical 3D printer market is still dominated by foreign brands. Printers manufactured by Canon, Stratasys, and 3D Systems offer high precision, superior surface quality, and shorter production times, capturing nearly 85% of the market share for medical 3D printers. In recent years, domestic enterprises have entered the 3D printing market through technology introduction and collaborations. Xi'an Bright Laser Technologies (BLT) was among the first companies in China to focus on metal 3D-printed implants. In 2014, BLT, in collaboration with Xijing Hospital affiliated with the Fourth Military Medical University, customized the world’s first 3D-printed scapula and clavicle, which were successfully applied in clinical surgery. In 2015, BLT, together with Tangdu Hospital affiliated with the Fourth Military Medical University, successfully performed the world’s first thoracic bone replacement surgery using 3D-printed implants. In 2017, a metal 3D-printed calcaneus produced by BLT in partnership with Dongwang Technology was successfully implanted at Xianyang No. 1 People’s Hospital, marking the first personalized metal 3D-printed implant surgery in the Xianyang region.

BLT-Printed Calcaneal Implants

Image source: Sohu Technology

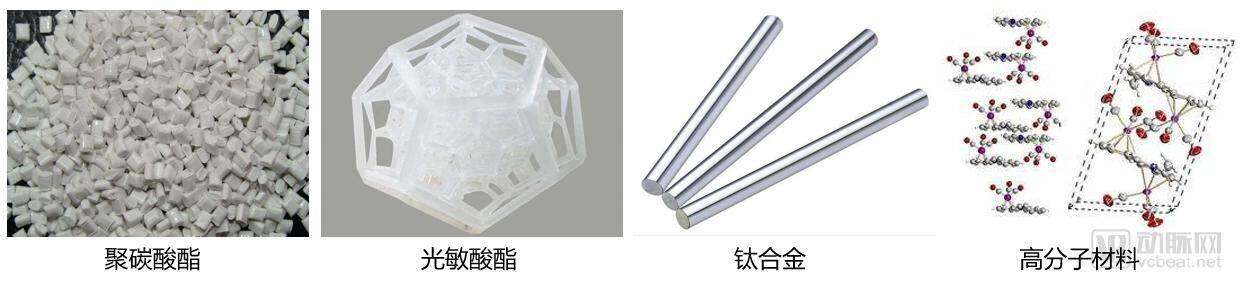

Medical 3D printing materials mainly include plastics, resins, metals, and biomaterials. Plastics primarily involve polycarbonate, polystyrene, TPU, PET, PBA, polyvinyl alcohol, and polyoxymethylene, with domestic supply being predominant. Silver Age Technology, Kingfa Sci. & Tech., and Esun are the main suppliers of 3D plastic materials.

The resins are primarily photosensitive resins, which feature high strength, heat resistance, and waterproofing. They offer rapid curing, high molding precision, and excellent surface finish. Companies such as Xinjiayi Technology and Palachi Technology specialize in the production of photosensitive resin materials.

Metallic materials, represented by titanium alloys and nickel-based superalloys, offer a series of advantages including uniform and stable composition, controllable particle size distribution, low oxygen content, high sphericity, and excellent flowability. As a leading domestic producer of titanium and titanium alloys, Baoji Titanium Industry Group has gained significant recognition in both the Chinese and international markets, becoming synonymous with “China Titanium.”

Biomaterials mainly include polymers, inorganic materials, hydrogels, and living cells. These materials must exhibit good biocompatibility and mechanical properties similar to those of human soft tissues. Due to the high standards required for biomaterials, manufacturers are predominantly foreign companies such as NatureWorks and Thermo Fisher Scientific. As a representative domestic enterprise engaged in the research and development of 3D bioprinting materials, Hangzhou Genefly Biotechnology Co., Ltd. has developed living cell products that meet the standards for human tissue repair and is gradually introducing them to the market.

3D Printing: Main Material Types

Medical 3D-printed products have a wide range of applications, covering preoperative planning, dental restoration, surgical guides, prosthetics, internal implants, and organ tissues. Preoperative planning, dental restoration, surgical guides, prosthetics, and internal implants belong to the primary stage of medical 3D printing, where the technology is relatively mature and has achieved clinical application in the medical field. A large number of domestic enterprises have entered this sector: Jike San Medical and Zhejiang Derda Medical focus on preoperative planning; Born Biomedical and Printech specialize in dental restoration; while AK Medical and Excellent engage in orthopedic implants, among others.

Due to the technical complexity and ethical concerns surrounding 3D-printed organ and tissue technology, its application is currently confined to the experimental stage. Foreign enterprises are significantly ahead of their domestic counterparts. For instance, Organovo, headquartered in San Diego, USA, offers a comprehensive product portfolio ranging from internal organs to skin, and from tissues to organs, including micro-livers, liver tissues, mini-kidneys, kidney tissues, transplantable kidneys, bone tissues, muscle tissues, and skin tissues. Its products are primarily used for drug development and therapy testing during clinical research, enabling the assessment and determination of drug effects on organs, thereby facilitating faster and more efficient drug discovery and reducing R&D costs.

Sichuan BlueLight Inno Biotech Co., Ltd. is a representative enterprise in China specializing in bio-3D printing. Focusing primarily on the research and development of stem cell application technologies, the company’s R&D team has successfully developed 3D-bioprinted blood vessels and implanted them into rhesus monkeys. In the future, the company will accelerate the clinical translation of stem cell technologies for applications in organ repair and tissue regeneration.

Vascular Tissues Implanted in Rhesus Monkeys

Image source: West China City Daily

Policies, Regulations, and Certification Systems Are Being Gradually Improved

The government has consistently attached great importance to the development of 3D printing in the healthcare sector. On February 7, 2014, the China Food and Drug Administration issued the Notice on the Special Approval Procedures for Innovative Medical Devices (Trial), which streamlined the approval process for 3D-printed products to support and encourage innovation in medical 3D printing. VCBeat has compiled relevant policies in recent years regarding government support for the development of medical 3D printing.

Policies Related to Medical 3D Printing

From the perspective of policy-issuing authorities, the State Council and its subordinate departments, including the China Food and Drug Administration (CFDA), the Ministry of Science and Technology, and the National Development and Reform Commission, have explicitly stated their strong support for the application of 3D printing in the medical field. This support covers various areas of medical 3D printing applications, such as implants, biomaterials, and tissue organs. Furthermore, the CFDA has put forward specific requirements for medical 3D-printed products to guide their innovation and development.

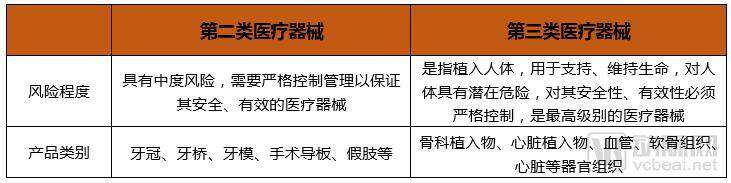

Based on the risk levels of medical devices, the China Food and Drug Administration (CFDA) primarily classifies and regulates 3D-printed medical devices as Class II and Class III medical devices.

Both the China Food and Drug Administration (CFDA) and the U.S. Food and Drug Administration (FDA) have established stringent requirements for the market access of medical 3D-printed devices. The CFDA implements classified management of medical 3D-printed devices in accordance with the “Medical Device Classification Rules,” strictly controlling usage risks. It places particular emphasis on the regulation of personalized implants, including the formulation of specialized regulations, market access mechanisms, quality management systems, and even post-market reporting and follow-up protocols. Meanwhile, the FDA has specified distinct requirements for each stage of medical 3D-printed devices, encompassing design, printing, and post-processing, thereby ensuring product quality and safety from the source. Additionally, the FDA has set forth functional requirements for bioprinted medical devices.

Although no specific policies or regulations targeting medical 3D printing have been issued to date, relevant government departments are accelerating the research and formulation of regulatory policies for medical 3D printing. On February 26, 2018, the China Food and Drug Administration (CFDA) released the "Guiding Principles for Technical Review of Registration of Custom-made Additive Manufacturing Medical Devices" (Draft for Comments), which clearly specified requirements regarding the description, product performance, animal testing, and medical-engineering interaction conditions for passive implantable medical devices used in bones, joints, and teeth.

(1) Product Description: Describe the interface structure of the product and its connection to human tissue.

(2) Product Performance: Conduct mechanical testing of the product in accordance with its intended use, and perform necessary biocompatibility tests.

(3) Animal studies: Provide information on the species, strain, source, age, sex, body weight, housing environment and conditions, diet, and health status (including unexpected deaths) of the animals. Conduct a comprehensive evaluation and comparison of new bone formation and local tissue responses following implantation of the test and control samples.

(4) Medical-engineering interaction conditions: Validation of manufacturing hardware and software, printing processes, raw materials, post-processing methods, and product testing is required to ensure process compliance and product safety.

The release of the "Technical Review Guidelines for the Registration of Customized Additively Manufactured Medical Devices (Draft for Comment)" signifies that China has incorporated the technical processes of 3D-printed implantable devices into its regulatory framework.

Strengthened Independence in R&D Technology, Narrowing the Gap with Foreign Countries

Currently, the technologies primarily involved in the medical 3D printing industry include Electron Beam Selective Melting (EBSM), Selective Laser Sintering (SLS), Stereolithography (SLA), and Selective Laser Melting (SLM).

From the perspective of the advantages and disadvantages of various technologies, EBSM and SLM technologies are primarily applied to the printing of metal products. Due to their high technical barriers, the core technologies for such equipment are controlled by international giants such as Stratasys, 3D Systems, and EOS, resulting in high purchase prices and maintenance costs for complete systems. The SLS technology features a simple process and low equipment costs, but it yields poor-quality finished products and requires long printing times. Compared with SLS technology, SLA technology produces higher-quality finished products with larger build dimensions, but the equipment cost is high.

In the medical field, demand for metallic implants is strongest, creating vast application opportunities for Electron Beam Selective Melting (EBSM) technology. AK Medical has utilized EBSM technology to manufacture orthopedic implants such as hip joints and vertebral bodies, successfully obtaining medical registration certificates from the China Food and Drug Administration (CFDA). On January 5, 2018, Tianjin Qingyan Zhishu Technology Co., Ltd. released its latest generation of open-source electron beam metal 3D printers, the QbeamLab. This marks a breakthrough achievement for China in the EBSM sector, signifying enhanced independence in China’s 3D printing technology and a gradual narrowing of the technological gap with foreign counterparts. Furthermore, experts from the China Association for Medical Devices Industry predict that the annual compound growth rate of the EBSM technology market will reach as high as 25%, making it the primary 3D printing technology applied in the medical field.

Zhibei Technology's QbeamLab 3D Printer

Image source: Sandi Shikong 3D Printing Network

North America Accounts for the Largest Market Share, While the Asia-Pacific Region Shows the Fastest Growth

With the advancement of 3D printing technology and rising healthcare consumer spending, the global medical 3D printing market is poised for gradual expansion, reaching a market size of $8.9 billion by 2022, with a compound annual growth rate (CAGR) of 17.2%.

Data Source: SmartTech Market

Data Source: SmartTech Market

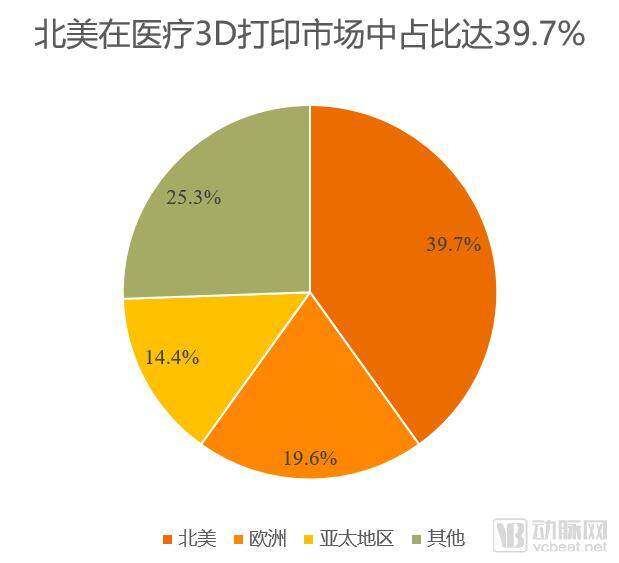

From the perspective of the distribution of the medical 3D printing market across major global regions, North America holds the largest share at 39.7%, followed by Europe, while the Asia-Pacific region accounts for a relatively small proportion of only 14.4%. This is primarily because countries represented by the United States started early in 3D printing technology, with the emergence of industry giants such as Stratasys and 3D Systems providing technical support for the application of 3D printing in the healthcare sector. Furthermore, the higher per capita income and well-established health insurance systems in North America have fostered a substantial consumer base.

However, with the rising level of economic development in the Asia-Pacific region and the gradual adoption of 3D printing technology in the healthcare industry, the Asia-Pacific region will become the fastest-growing market for medical 3D printing. As the largest healthcare consumer in the Asia-Pacific region, China holds immense potential for the development of its medical 3D printing market.

The remaining content of this report:

V.China's Medical 3D Printing Market Enters a New Phase: Rapid Growth in Dental Restoration, Orthopedic Implants Become Key Competitive Focus, and New Breakthroughs Achieved in Organ and Tissue Engineering

(I) Commercialization of Prosthodontics Achieved with Rapid Development

(II) The orthopedic implant market has become a key battleground, with various enterprises entering the fray

(3) Breakthroughs in Organ and Tissue Testing: Human Clinical Applications on the Horizon

(4) Medical 3D Printing Companies Actively Seek Capital, Potentially Ushering in an Investment Boom

VI. Precision Medicine, Non-Transplant Applications of Organs, and New Drug Development May Become Future Trends

(1) 3D Printing Empowers Precision Medicine: Customized Medical Devices Enhance Therapeutic Efficacy

(II) Enhanced Non-Transplant Application Value of 3D-Printed Organs and Tissues

(3) 3D-Printed Drugs: On-Demand Drug Manufacturing Becomes Possible

Please refer to the full report.

Scan the QR code below to becomeVCBeat Official Member, you can obtainFull Version of the "2017 Report on the Current Status of 3D Printing Applications in Healthcare". Gain deeper insights into the current industrial landscape and development trends in the field of medical 3D printing. Furthermore, over the coming year, you will have unrestricted access to the completeIndustry Trends Report, promptly access the latest global investment and financing information, with comprehensiveHealthcare Enterprise Database,AlsoMassive Resource Integration。

Special thanks to Zhao Xiaowen, Founder of Excellent, and Jiang Zhiwei, Head of Marketing at Medvance, for their strong support of this report.

Scan to become a VCBeat member