BMS Faces Shareholder Opposition in $74 Billion Bid to Acquire Celgene and Lead Oncology Market

Bristol-Myers Squibb

Biopharmaceutical and Nutritional Product R&D and Sales

With a transaction value reaching $74 billion and involving two industry giants, Bristol-Myers Squibb’s (BMS) acquisition of Celgene, disclosed on January 3, sent shockwaves through the industry. BMS aimed to integrate Celgene’s existing pipeline to position itself as a leader in solid tumors and hematologic malignancies; however, this strategy did not fully win over shareholders.

The promotional slogan on the homepage of Bristol-Myers Squibb’s global official website underscores the management’s high regard for this transaction.

Approximately two months after announcing the acquisition, Bristol-Myers Squibb (BMS) filed an application with the U.S. Securities and Exchange Commission on February 22. Two of its major shareholders, Wellington Management and Starboard Value, publicly opposed the transaction. Moreover, as early as January 14, U.S. Representatives Peter Welch and Francis Rooney raised concerns with the Federal Trade Commission and the Department of Justice regarding their review of BMS’s proposed acquisition. They argued that the deal could stifle healthy competition in the field, particularly in oncology.

Wellington Management, which holds approximately 8% of Bristol-Myers Squibb’s (BMS) shares, and another BMS shareholder, Starboard Value, jointly announced on February 27 their opposition to the $74 billion acquisition. Wellington cited three primary reasons, stating that the deal imposes excessive risk on BMS shareholders. Starboard, which holds a 1% stake, described the transaction as “poorly conceived and ill-advised” and said it would seek support from other BMS stakeholders to block the deal. Dodge & Cox, another shareholder with a 2% stake, also expressed its opposition to the transaction.

Subsequently, in an open letter to shareholders on February 28, Bristol-Myers Squibb (BMS) outlined the benefits of the transaction, highlighting four specific points, including:

1. Bristol-Myers Squibb (BMS) has achieved continuous growth for 10 consecutive years, and its combination with Celgene will create a biopharmaceutical enterprise with leading scale;

2. Following the merger, BMS is expected to launch six new marketable drugs in the near future, five of which are from Celgene’s R&D pipeline, with total revenues exceeding $15 billion;

3. Celgene will enrich BMS’s early-stage research pipeline; leveraging a more diversified platform, BMS will be well-positioned to develop more innovative products, thereby driving robust growth over the next decade;

4. Within three years following the completion of the transaction, the company is expected to generate approximately $45 billion in free cash flow, which will help the company rapidly reduce its debt. By 2022, the merger is projected to achieve approximately $2.5 billion in cost synergies.

In an open letter to shareholders, Bristol-Myers Squibb (BMS) stated that the merged company will have 10 drugs in Phase III clinical trials, six of which are expected to be launched in the near term. The early- and mid-stage pipeline includes 21 immuno-oncology and solid tumor products, 10 hematologic oncology products, 10 immunology and inflammation products, and 9 cardiovascular and fibrotic disease products.

BMS will hold a special shareholders’ meeting on April 12, 2019, at 10:00 a.m. Eastern Time, to vote on the acquisition. In addition to the three major shareholders mentioned above who oppose the deal, the positions of Norinchukin Zenkyoren Asset Management (10.14%), The Vanguard Group (7.02%), and BlackRock (7.02%) will be crucial. Notably, Vanguard also holds a 7.5% stake in Celgene, while BlackRock holds a 7.43% stake; they are unlikely to cast votes against the transaction to block it.

Bristol-Myers Squibb (BMS) is a century-old multinational pharmaceutical company. In its early years, BMS reached an agreement with Sanofi to secure the North American rights to the anticoagulant drug clopidogrel. Following its approval by the U.S. Food and Drug Administration (FDA) in 1998, the drug rapidly evolved into a blockbuster medication, rivaling the status of the legendary “first-generation miracle drug” Lipitor. Just three years after its launch, the two companies achieved $1 billion in sales, with subsequent performance soaring to approach annual revenues of nearly $10 billion. This drug remains hailed by the industry as an unparalleled legend.

In 2009, Bristol-Myers Squibb (BMS) spun off from Mead Johnson and began its transformation into a “next-generation biopharmaceutical company.” It built a biopharmaceutical empire through acquisitions of companies such as IFM Therapeutics and Cormorant, with a product portfolio covering cardiovascular diseases, cancer, immunology, and other fields.

In 2011, the CTLA-4 monoclonal antibody Yervoy (ipilimumab) was launched, gradually becoming the company’s “new favorite.” In July 2014, Opdivo (nivolumab) made its debut as the first PD-1 inhibitor approved globally, ushering in the commercialization era of the “miracle anti-cancer drug” PD-1. Opdivo outperformed Merck & Co.’s Keytruda in terms of indications, enabling Bristol-Myers Squibb (BMS) to maintain a leading position in the competitive landscape of immunotherapy. In 2015, BMS achieved a major breakthrough with its immunotherapy combination Opdivo plus Yervoy as first-line treatment for non-small cell lung cancer, further solidifying its leadership in immunotherapy. In 2017, BMS secured a decisive advantage in its patent dispute with Merck & Co., obtaining two key patents along with a $625 million upfront payment and tiered royalties ranging from 2.5% to 6.5% on Keytruda sales.

Nevertheless, a series of clinical trial setbacks for Bristol-Myers Squibb (BMS) inflicted significant losses on the company. The failure of the Phase 3 trial of Opdivo as a first-line monotherapy for non-small cell lung cancer (NSCLC) caused the company’s stock price to drop 16% in a single day, wiping out $20 billion in market capitalization. Subsequently, the Phase 3 trial of Opdivo as a second-line monotherapy for small cell lung cancer (SCLC) failed to meet its endpoints, and the accelerated review application for the I/O combination maintenance therapy for SCLC was forced to be withdrawn. In total, BMS’s market capitalization shrank by $46 billion.

Bristol-Myers Squibb’s advantages in the patent war have not translated into good fortune for its clinical trials; instead, its long-time rival Merck & Co. has gained increasing momentum.

On January 10, 2017, Merck & Co. received FDA approval for the supplemental application of “Keytruda + pemetrexed + carboplatin” as a first-line treatment for non-small cell lung cancer (NSCLC), regardless of PD-L1 expression levels, and was granted priority review status, thereby gaining a competitive advantage in the first-line NSCLC treatment landscape.

Undoubtedly, Opdivo and Yervoy carry excessive expectations for Bristol-Myers Squibb (BMS). Although the company currently holds a leading position in the immunotherapy landscape, Merck & Co. is closely trailing, and any slight misstep could result in BMS being overtaken. Facing intense pressure, BMS needs to inject fresh momentum into its pipeline to rapidly establish a competitive advantage beyond the PD-1 market.

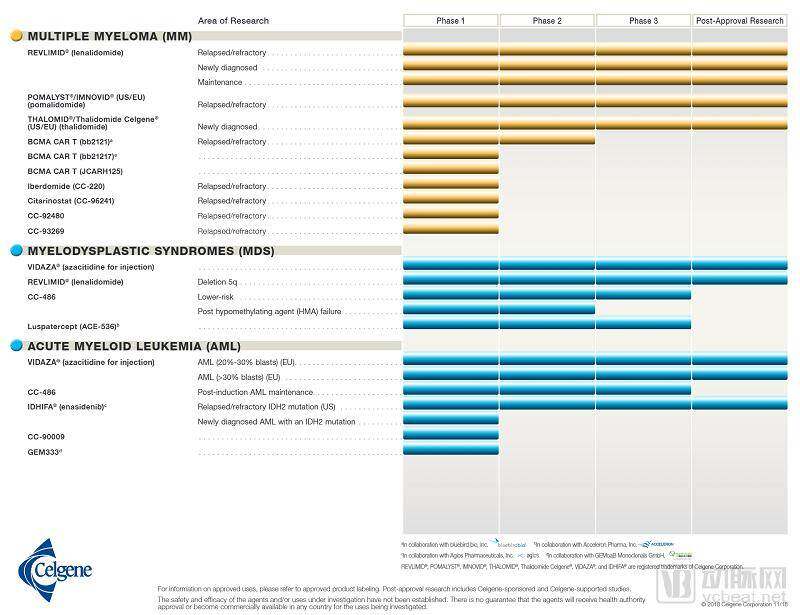

From this perspective, Celgene is a suitable target. Not to mention the CAR-T products acquired through its purchase of Juno, Celgene’s multiple myeloma drug Revlimid alone can generate nearly $10 billion in sales for the company. Coupled with the strategic partnership between Celgene and BeiGene, Bristol-Myers Squibb (BMS) will hold two PD-1 inhibitors and one CAR-T therapy, truly becoming a giant in the treatment of both solid tumors and hematologic malignancies.

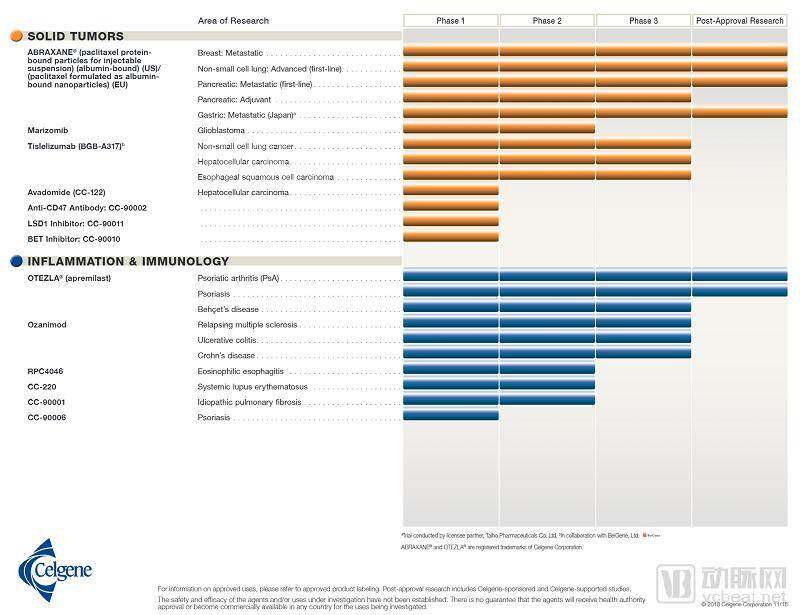

Combined with the two companies’ respective portfolios in immunology, inflammation, and cardiovascular disease, the merged entity will have nine blockbuster products with annual revenues exceeding $1 billion.

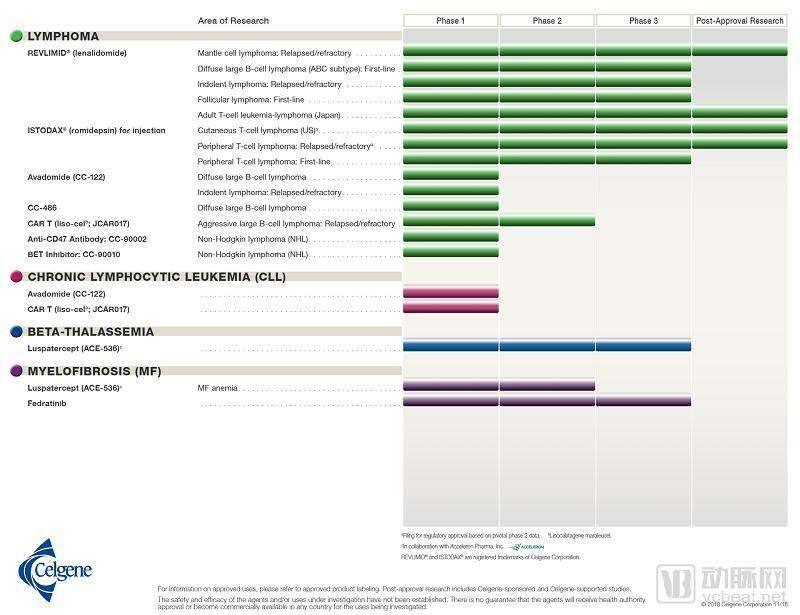

Celgene's Product Pipeline

This transaction was carefully considered by management, reflecting a strategy that has been in place for over a decade. By focusing on high-value investment opportunities and external innovation sourcing to complement its internal portfolio and product pipeline, Bristol-Myers Squibb (BMS) has achieved sustained and robust growth for ten consecutive years. Furthermore, this deal will significantly expand BMS’s clinical assets, enabling the company to develop more competitive and innovative drugs.

BMS predicts that, following the integration of its pipeline, the company will have six products slated for imminent launch, with potential revenues exceeding $15 billion. Leveraging its proprietary portfolio and Celgene, BMS is poised to assume a leadership position in oncology beyond 2025. Furthermore, as its product pipeline diversifies, the company will uncover opportunities across a broader range of therapeutic areas, thereby driving BMS’s growth in the latter half of the next decade.

But why did such a seemingly attractive deal face public opposition from shareholders? The first accusation made by Wellington was that the transaction exposed shareholders to excessive risk.

Revlimid is currently Celgene’s top-selling drug, generating $9.685 billion in sales in 2018. However, it is also approaching the inevitable challenge faced by all innovative drugs: patent expiration. Key patents for Revlimid in Europe will remain in force until 2022, while its U.S. drug patents have been extended until 2026. As Celgene’s largest revenue driver, Revlimid’s exposure to generic competition starting in 2022 would compel Bristol-Myers Squibb (BMS) to accept a 90% decline in Revlimid-related revenue.

Furthermore, Bristol-Myers Squibb (BMS) offered $74 billion for a 69% stake, implying a per-share price of approximately $152.77, whereas Celgene’s 52-week high valuation was $95.30. Moreover, the agreement stipulates that for each share of CELG stock held, Celgene shareholders will receive one share of BMS stock plus $50 in cash, along with Contingent Value Rights (CVRs) with an expected future value of $9 in cash.

For BMS shareholders, such a decision is arguably “ill-considered.”

But that’s not all; along with the pipeline, BMS also acquired Celgene’s liabilities. In its investor report, BMS stated that its current long-term debt stands at only $7.3 billion; however, the acquisition would add $32 billion to the company’s balance sheet. Additionally, BMS would need to assume $20 billion of Celgene’s debt. As a result, BMS’s debt insurance costs surged to their highest level since May 2010, and the company’s credit default swap (CDS) spread rose by 66%.

Wellington Management noted in its announcement that it believes Bristol-Myers Squibb (BMS) is not reaping returns from its earnings as easily as previously anticipated, and that the value of returns provided by management to shareholders is less attractive. However, the announcement did not specify the exact nature of these returns.

Whether the BMS acquisition was worth the price remains uncertain, but Celgene’s executives are undoubtedly among the “first to get rich.” Fierce Pharma previously calculated that if Celgene CEO Mark Alles were to step down after the completion of the BMS merger, he would receive approximately $27.9 million.

Citing the proxy statement filed with the U.S. Securities and Exchange Commission, Fierce noted that upon his departure, Alles would receive approximately $17 million in equity, $10 million in cash, as well as miscellaneous allowances and benefits. Reportedly, this amounts to roughly three times his current salary and benefits package.

In addition to Alles, other executives at Celgene will also reap financial benefits from the merger. According to reports, three executives will receive compensation equivalent to 2.5 times their salary and bonus if they depart after the completion of the BMS transaction: Chief Financial Officer David Elkins is set to receive $15.1 million, Chief Strategy Officer Peter Kellogg $11.9 million, and Head of Research and Development Rupert Vessey $12.2 million.

Compared to the other two opponents, Wellington’s announcement was relatively courteous. Another shareholder, Starboard Value, stated bluntly in its announcement that it would solicit input from other stakeholders to block the transaction. Meanwhile, Representatives Peter Welch and Francis Rooney directly questioned whether the acquisition would stifle healthy competition in the field—particularly in oncology—ultimately leading to higher drug prices and harming consumers.

Welch and Rooney argue that the new products acquired post-merger can supplement or enhance the competitive advantage of Bristol-Myers Squibb’s (BMS) own oncology portfolio, thereby diminishing the competitiveness of other drugs in the same class. This, in turn, would grant BMS greater leverage in price negotiations with insurers. In a letter to regulators, the two wrote, “The larger the company becomes after a merger, the easier it is to form a monopoly, and the more capable it is of employing strategies such as rebates to prevent healthcare providers from accessing more affordable or equally effective alternative products.”

This is not the first time stakeholders have opposed a major merger. In 2018, during Takeda’s acquisition of Shire, a group of Takeda shareholders also opposed the deal. Despite the objections, the transaction was completed in January. Subsequently, Takeda became one of the biggest market disruptors, with its stock price falling 42% by the end of 2018 and its market capitalization shrinking by approximately $20 billion; meanwhile, Shire gained $6 billion in revenue. Similarly, Bayer suffered a significant setback when it acquired Monsanto, with its second-quarter net profit declining 34.7% year over year.

It is reported that since the acquisition was announced, Celgene’s stock price has soared, rising from a low of $58.59 to its current level of $86; BMS’s stock price also saw a slight increase during the same period and is currently trading at around $52.

BMS executives expressed optimism, even excitement, about the deal, while investors appeared negative, even resistant. The underlying reason simply boils down to differing perspectives.

Although Celgene’s patent crisis and debt burden may pose risks to Bristol-Myers Squibb (BMS), the value of its pipeline to BMS cannot be denied. According to Celgene’s 2018 annual report, the company achieved total annual revenue of $15.281 billion, a year-on-year increase of 17.52%. Among its products, four drugs each generated annual sales exceeding $1 billion.

Moreover, the U.S. drug patent for its flagship product, Revlimid, has been extended to 2026. This means that Celgene will continue to enjoy exclusive rights in the United States for four years after the patent expires in Europe, thereby avoiding a cliff-like crisis.

In addition, Bristol-Myers Squibb previously acquired fedratinib from Impact Biosciences and has since submitted marketing applications for the treatment of myelofibrosis to both the FDA and the EMA. Following the acquisition of JUNO Therapeutics, the jointly developed CAR-T therapy liso-cel (JCAR017) initiated Phase II clinical trials for the treatment of relapsed/refractory DLBCL and CLL in the fourth quarter of 2018.

With two PD-1 inhibitors and one CAR-T therapy in its portfolio, BMS is poised to become the most influential player in the solid tumor and hematologic malignancy sectors, bolstered by Celgene. Coupled with Celgene’s leadership in the inflammation market, BMS will be further strengthened.

From the perspective of pipeline complementarity alone, Celgene is indeed a highly suitable target and holds strong potential to generate long-term returns. As for why it sparked fierce opposition from shareholders, it is likely that, when weighing risks against benefits, the price paid for the acquisition appeared somewhat excessive.