Medtronic's Two-Decade Revelation: Innovation Is Precious, But R&D Is Too Costly – Why Giants Have Turned Into M&A Machines

Medtronic

Chronic Disease Medical Device and Therapy Developer

In 2017, a devastating wildfire swept through Santa Rosa, California, in the United States. Two factories belonging to Medtronic, the global medical device giant, happened to be located there. Perhaps blessed by good fortune, the facilities emerged from the fire completely unscathed.

This incident was even regarded as a harbinger of Medtronic’s strategic shift.

In late 2017, the same year as the fire, Medtronic acquired Crospon, a gastrointestinal disease diagnostics company, for $45 million, and subsequently acquired QT Vascular’s Chocolate PTA balloon for $28 million. In early 2018, Medtronic announced a restructuring plan to cut costs. Meanwhile, to reduce its debt ratio, the company unveiled a plan to repurchase $1.2 billion worth of senior notes to repay debt. In May, Medtronic sold its 25% stake in China-based LifeTech Scientific Corporation to China Everbright Limited and another undisclosed investor.

In fiscal year 2017, following frequent mergers and acquisitions, Medtronic’s revenue reached $29.953 billion. In fiscal year 2018, Medtronic set forth its objectives for the coming years, namely organic revenue growth of 4% or more and an 8% increase in adjusted earnings per share (EPS). Judged by outcomes, Medtronic firmly secured the top position in the Top 10 Global Medical Device Companies ranking published that year by Medical Design & Outsourcing, in the post-merger era.

A review of Medtronic’s development history reveals repeated expansions in scale and business scope, accompanied by the consistent implementation of several strategic development guidelines. For giants in the medical device industry, mergers and acquisitions are an indispensable component of their growth trajectories.

In this regard, VCBeat (WeChat Official Account: vcbeat) takes the industry giant Medtronic as a case study to outline its development journey from inception to becoming an industry leader, aiming to illustrate the typical growth path of medical device giants:

1. In the early stages of development, companies were primarily driven by technological R&D;

2. Following the successful commercialization of its technology and products, the company began to achieve marketing at scale;

3. Driven by strategic considerations, the company has embarked on the inevitable path for medical device giants—mergers and acquisitions.

Meanwhile, we also attempt to answer why numerous medical device companies, after reaching mature scale, have all converged on an expansion model dominated by mergers and acquisitions.

Medtronic’s development to its current stature was not achieved overnight.

In 1949, Earl Bakken, who had earned a Bachelor of Science degree in Electrical Engineering, began working at Northwestern Hospital. Driven by his interest in electricity and electronics, he started paying attention to the electronic devices that hospitals had just begun to use after World War II. He discovered that although these devices were advanced and sophisticated, there was no dedicated staff responsible for their maintenance and repair.

Earl Bakken realized his opportunity had arrived.

That same year, Earl Bakken abandoned his academic career. Persuaded by him, his brother-in-law, Palmer Hermundslie, also quit his job at a local lumber mill. Together, they established a medical instrument repair company in a 600-square-foot abandoned garage, naming it Medtronic.

Medtronic’s initial progress in its small workshop was far from smooth, with only $8 in revenue during the first month—merely the compensation for repairing a centrifuge. It was not until the second year, when Earl Bakken and Palmer Hermundslie became agents for several medical device companies in the U.S. Midwest, that Medtronic’s business truly began to grow.

The 1950s marked Medtronic’s first period of expansion, during which the company’s workforce grew and more than half of its revenue was generated through agency sales. Meanwhile, Earl Bakken and Palmer Hermundslie leveraged their agency roles to connect with numerous physicians and laboratory researchers in the Midwest, who frequently enlisted Medtronic engineers to help modify and design specialized instruments.

Medtronic, having identified new business opportunities, began its transformation by launching a manufacturing division dedicated to producing customized products for customers. During this period, Medtronic manufactured nearly 100 types of devices, but only 10 evolved into genuine product lines, including two models of external defibrillators, one animal ventilator, one heart rate monitor, and one physiological stimulator.

In 1960, Medtronic manufactured the first implantable cardiac pacemaker, thereby establishing its leadership position in the global pacemaker market. A garage and an apartment could no longer accommodate the rapidly growing company, so Medtronic relocated its headquarters to a 15,000-square-foot facility in Minnesota. By 1962, Medtronic’s product line had expanded to 21 items, with sales rising from $180,000 in 1960 to $500,000. In 1963, annual sales increased further to $985,000, and profits reached $73,000. That year, Medtronic sold an average of 100 pacemakers per month, with 20% of orders coming from overseas.

In the mid-1960s, Medtronic manufactured its first transvenous pacemaker. Its pacing leads could be maneuvered through the veins to reach the heart, eliminating the need for thoracotomy or general anesthesia. Furthermore, several studies initiated during this period on pain management for non-cardiac conditions laid the foundation for Medtronic’s presence in the neuromodulation field. Subsequently, in 1969, Medtronic launched implantable spinal cord stimulators and brain stimulators.

By the 1970s, Medtronic’s sales surpassed $200 million; however, the continuous emergence of new medical device companies reduced its U.S. market share from 60% to 40%. Subsequently, Medtronic began expanding into other fields: its Neuromodulation business unit was formally established in 1976, launching the Neuromod 3700 (a deep brain stimulator for suppressing chronic pain) and the ESI (a device for treating scoliosis); it also introduced Pisces, the first spinal cord stimulator for treating chronic limb pain. In 1977, Medtronic established its Heart Valve business unit and launched the Medtronic “Hall” mechanical heart valve.

At the outset of the 1980s, Medtronic got off to a strong start: in 1981, the company launched Versatrax, the first pacemaker capable of simultaneously sensing and pacing both the atria and ventricles; in 1985, Medtronic introduced the world’s first single-chamber rate-responsive pacemaker. Meanwhile, the company continuously expanded its product portfolio through external acquisitions. Entering the 21st century, Medtronic successfully transformed from a company with a single product line into a diversified, international leader in medical technology, driven by internal growth and strategic acquisitions.

Medtronic, a Fortune Global 500 company, has also assembled a new leadership team. Current Chairman and CEO Omar Ishrak spent 16 years at General Electric, where he served as Director and Senior Vice President, and additionally held the position of President and CEO of GE Healthcare Systems. Michael J. Coyle currently serves as Group Vice President and President of the Cardiovascular Business; prior to joining Medtronic, he provided executive consulting services to numerous private equity firms, venture capital firms, and medical device technology companies. Mr. Coyle previously served as President of the Cardiac Rhythm Management (CRM) division at St. Jude Medical, where he led the company’s global pacemaker, implantable cardioverter-defibrillator (ICD), and cardiac resynchronization therapy businesses. Notably, Medtronic maintains close collaboration with China. Alex Gu, President of Greater China, simultaneously leads multiple divisions including Emerging Markets and Private Hospitals (ER/PH), R&D centers, business development, and medical and clinical affairs. Previously, he held executive positions at General Electric and Covidien. Additionally, Mr. Gu is one of the founders of the AdvaMed China Steering Committee.

It is evident that prior to the 1990s, Medtronic leveraged its proprietary technologies to gain industry renown, secure orders, and gradually expand its market presence, thereby taking shape as an emerging industry giant. However, although the U.S. medical device market is substantial in overall size, it exhibits a high degree of “fragmentation” due to its extensive product diversity: most individual product categories have limited market sizes, with constrained scales in each segment. To achieve further breakthroughs, Medtronic needed to explore alternative strategies.

The continuous renewal of Medtronic’s leadership team has brought diversified development paths to the company, with senior management opting for strategic mergers and acquisitions as a means of expansion. This initiative has allowed the flagship products of various acquired companies to “converge into a sea,” thereby establishing Medtronic’s diverse product lines.

Currently, Medtronic's medical devices are mainly divided into four major categories:

1. Cardiovascular (CVG) category, including cardiac rhythm disease management, coronary intervention business, cardiac surgery business, and peripheral vascular intervention business;

2. Minimally Invasive Therapy Group (MITG), comprising surgical services, patient monitoring, and rehabilitation businesses;

3. Restorative Therapies Group (RTG), including spine/orthopedics, neuromodulation/pain management, surgical technologies, and neurovascular businesses;

4. Diabetes category, covering insulin pumps, continuous glucose monitoring systems, and comprehensive diabetes treatment;

5. In addition, Medtronic also operates in the field of medical devices related to respiratory and pulmonary diseases, brain disorders, digestive and gastrointestinal diseases, ear-nose-throat (ENT) conditions, spinal disorders, and urology.

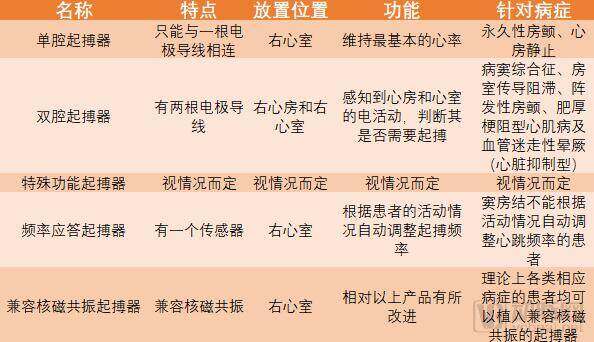

Among these, the implantable cardiac pacemaker, which has established the company’s market leadership, is synonymous with Medtronic and falls under the category of cardiovascular (CVG) devices. This implantable electronic device integrates bioengineering, electronics, and clinical applications to treat symptomatic bradycardia caused by various etiologies. Cardiac pacing therapy is a relatively mature technology and has become one of the representative achievements in biomedical engineering. To date, cardiac pacemakers remain the most widely used treatment for bradycardia.

Medtronic offers a wide range of pacemaker models and types, generally categorized into single-chamber pacemakers, dual-chamber pacemakers, specialized-function pacemakers, rate-responsive pacemakers, and MRI-compatible pacemakers. The specific type of pacemaker to be implanted in each patient is determined by the physician based on the patient’s individual clinical condition and cardiac rhythm status. For patients, the most suitable pacemaker is the best choice.

Chart by VCBeat based on Medtronic product list

Implantable Cardioverter-Defibrillator (ICD) is an electronic device capable of identifying and promptly terminating malignant ventricular arrhythmias. It can automatically detect life-threatening arrhythmias, such as ventricular fibrillation, and deliver defibrillation shocks within ten seconds, thereby saving patients' lives. It is a highly effective therapeutic measure for the prevention of sudden cardiac death.

Medtronic’s Minimally Invasive Therapies Group (MITG) devices include two types of catheters for catheter ablation therapy in atrial fibrillation: radiofrequency catheters and cryoballoon catheters. Radiofrequency catheters deliver radiofrequency current (a type of high-frequency electromagnetic wave) to ablate diseased tissue, causing coagulative necrosis of the endocardium and subendocardial myocardium, thereby treating tachyarrhythmias by blocking reentrant circuits or eliminating focal triggers. Cryoballoon catheter ablation works through the endothermic evaporation of a liquid refrigerant, which removes heat from the tissue, lowers the temperature at the target ablation site, destroys abnormal electrophysiological cellular tissue, and thus reduces the risk of arrhythmias.

In the treatment of coronary heart disease, drug-eluting stents produced by Medtronic are regarded as another revolution in interventional therapy for coronary heart disease. The principle involves coating the surface of bare-metal stents with trace amounts of drugs that are slowly released into the vascular wall tissue, effectively inhibiting neointimal hyperplasia within the stent.

Medtronic’s product portfolio in the field of diabetes is equally impressive. Its insulin pump is a programmable electronic device, similar in size to a pager, that can be worn on the waist. By continuously delivering insulin subcutaneously, it mimics the physiological pattern of insulin secretion—namely, low-level basal insulin secretion during fasting states and bolus insulin secretion during meals—thereby helping patients achieve better glycemic control.

The paired continuous glucose monitor (CGM) reflects blood glucose levels by measuring the glucose concentration in subcutaneous interstitial fluid via a glucose sensor. This device requires a physician to implant the probe subcutaneously in the periumbilical region of the abdomen. It obtains blood glucose readings by generating electrical signals through chemical reactions between the probe and glucose in the subcutaneous interstitial fluid.

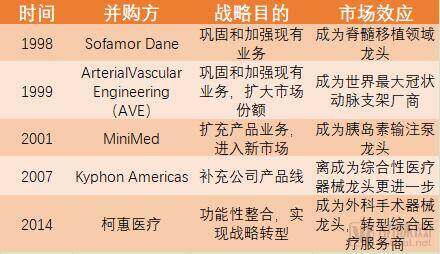

It is worth noting that while Medtronic established the basic framework of its product portfolio through technological R&D, it was strategic M&A that truly helped the company perfect its product system. In addition to expanding Medtronic’s existing product markets, these M&A deals also brought entirely new product businesses to the company.

Since the 1990s, Medtronic has completed nearly 100 M&A transactions, with a total disclosed value exceeding $73 billion. Among these, several acquisitions played a pivotal role in Medtronic’s development, enabling a qualitative leap in its legacy businesses.

VCBeat’s chart of Medtronic’s M&A activities, compiled based on data from the Guotai Junan Pharmaceutical Team

Recognizing the limitations in the development of the medical device industry, Medtronic is also attempting a business transformation, with one direction being the field of minimally invasive surgery, which has become a hotspot in recent years due to technological innovation. This transformation is similarly achieved through strategic mergers and acquisitions.

In January 2015, Medtronic completed its acquisition of the Irish medical device company Covidien for nearly $50 billion. Following the acquisition, Medtronic relocated its headquarters from the United States to Dublin, the capital of Ireland, and established a new Minimally Invasive Therapies Group (MITG) primarily based on Covidien’s existing businesses. This division focuses on conditions affecting the lungs, pelvis, kidneys, gastrointestinal tract, and obesity, with a commitment to advancing minimally invasive therapies. Covidien’s neurovascular business was merged with Medtronic’s Restorative Therapies Group (RTG) to provide products and therapies for cerebrovascular and pericerebral vascular diseases.

Minimally invasive surgery is a branch of medical science that utilizes minimal trauma or small access routes to introduce specialized instruments, physical energy, or chemical agents into the human body. It performs surgical procedures such as inactivation, resection, repair, or reconstruction of lesions, deformities, and injuries within the body to achieve therapeutic goals. Its hallmark is significantly reduced trauma to patients compared to corresponding traditional open surgeries. Data indicate that the global market size in the field of surgical instruments is approximately USD 15–20 billion.

In the fourth quarter of 2017, the Minimally Invasive Therapies Group delivered outstanding performance, with global revenues reaching $2.605 billion. According to the company’s financial report, the Surgical Innovations business achieved high single-digit growth, while the Patient Monitoring and Recovery business recorded mid-single-digit growth. This performance was primarily driven by advanced mechanical stapling and energy products, including specialized staple cartridges for endoscopic linear cutters, the Valleylab™ FT10 Energy Platform, and LigaSure™ vessel sealing instruments.

According to previous forecasts by Evaluate MedTech, Medtronic was projected to rank third and Covidien fifth in 2020. However, following the completion of the merger, this forecast is set to be rewritten: Johnson & Johnson may be “forced” to relinquish its top spot, while the merged Medtronic will become the global leader in the medical device industry.

According to senior executives at Medtronic, the low overlap between its business and that of Covidien allows this merger to deliver additional product portfolio expansion. Internal integration efforts between the two companies have already commenced, creating a combined entity with more than 85,000 employees across over 160 countries and regions worldwide. This transaction will enable Medtronic to incorporate Covidien’s product lines, thereby expanding its scale and scope of operations to better compete with Johnson & Johnson. Commenting on the development, a Wall Street analyst remarked, “The era of à la carte medical device selection has arrived.”

Medtronic’s other business transformation also closely follows the trend.

On September 20, 2018, Medtronic announced the acquisition of Mazor Robotics, an orthopedic robotics company, for $1.64 billion to enhance spinal surgery outcomes. Within less than a year, relevant media outlets reported on successful surgical cases. On April 16, 2019, the inaugural 2019 Medtronic China Fund & Baidu Ventures Medical Robotics Competition was officially launched at the Pujiang Technology Plaza in Lingang, Shanghai, aiming to encourage the development of medical robotics in the Chinese market.

Coincidentally, in addition to Medtronic, the medical divisions of well-known diversified giants such as Johnson & Johnson, Philips, and Boston Scientific also began acquiring surgical robotics companies during the same period, leading to a sudden surge in the surgical robotics sector.

As analyzed by the U.S. Government Accountability Office (GAO), given the limited scale of development in niche segments of the medical device industry, major industry giants have acquired surgical robotics companies not only to consolidate their existing core businesses but also for two additional reasons. First, the surgical robotics sector is a highly promising market with significant momentum; according to estimates by Boston Consulting Group (BCG), the global medical robotics market was projected to reach a valuation of $11.4 billion by 2020, with the growing prevalence of chronic diseases expected to further expand the market for surgical robots. Second, such mergers and acquisitions can diversify corporate business portfolios and help stimulate markets that have already shown signs of stagnation.

“This is a high-cost capital project,” said Dave Anderson, Vice President and Authorized General Manager at Medtronic. “That said, if surgical robots can reduce surgeons’ operating time by 40%, we are confident that the total cost of surgery can be lowered by 10%. With rational utilization of surgical robots, you will see how quickly they drive the development of the healthcare industry and the economy.”

Overall, technology-driven medical device companies must undergo consolidation to dominate the industry.

For Medtronic, having undergone a technology-driven transformation, achieved maturity in its own business development, and reached scale in market size, it has grown into an industry giant. It now focuses more on the market side, while facing the challenge of “a large ship being hard to turn” in terms of R&D. To protect its position and avoid disruption by small and medium-sized innovative companies, mergers and acquisitions have become Medtronic’s direct approach to breaking through product and technological fragmentation.

In the years following the 2016 U.S. presidential election and the introduction of new healthcare reform legislation, medical device giants such as Johnson & Johnson, Medtronic, Philips, Boston Scientific, and Becton Dickinson have all engaged in active mergers and acquisitions (M&A). These highly strategic business activities may also underscore the unique role of M&A in the medical device sector: when the industry landscape undergoes significant changes, M&A becomes a means for companies to achieve rapid transformation.

Medtronic’s Acquisition Activities Have Not Ceased.

On May 13, 2019, Medtronic announced its withdrawal from certain orthopedic business segments. Sharrolyn Transfeldt Josse, Vice President and General Manager of Core Spinal, still stated, “It is foreseeable that the spinal market will be substantial in the future, with growing demand for titanium-based products.” To this end, Medtronic acquired Titan Spine—a startup that expanded into the artificial joint market through low-cost and bundled payment models—to enhance the competitiveness of its titanium spinal products.