Top 10 Pharma Giants Report H1 Revenue Near $200 Billion and 3,587 Active Clinical Trials Targeting Oncology

Pfizer

Pharmaceutical R&D Developer

Drug development is a slow-evolving process. Large pharmaceutical companies with centuries of history enjoy significant first-mover advantages in this field. These giants control the world’s most valuable drugs, top-tier talent, and substantial capital resources. Collaborations and competitive dynamics among these industry leaders shape the overall direction of the pharmaceutical sector, while multi-billion-dollar mergers and acquisitions frequently draw intense attention to the companies at the pinnacle of the industry.

Major pharmaceutical companies have successively released their performance reports for the first half of 2019 (1H 2019), and the latest ranking of the top ten pharmaceutical giants has been unveiled. What subtle shifts have occurred in the industry landscape during the first half of this year? Which companies have broken into the top ten, and which have quietly dropped out? How much longer can Humira retain its throne as the “king of drugs”? How has Keytruda performed following the continuous approval of new indications? How is China’s volume-based procurement reshaping the global pharmaceutical landscape? And how are these pharmaceutical giants strategizing for their future development?

Top 10 Pharmaceutical Companies in H1 2019: New List

The landscape of the top 10 global pharmaceutical companies underwent slight changes in the first half of 2019. Eli Lilly, which broke into the top 10 in 2018 with revenue of $24.556 billion, saw its H1 2019 revenue drop to $10.729 billion following performance corrections, falling behind AstraZeneca’s $11.187 billion and dropping out of the top 10. Meanwhile, Bristol-Myers Squibb (BMS), driven by the strong performance of Eliquis and Opdivo, secured the ninth position previously held by Eli Lilly, with revenue reaching $12.193 billion.

Meanwhile, Pfizer remains at the top of the ranking with revenue of $24.661 billion. However, driven by Roche’s rapid growth in the first half of the year, the gap between the two has narrowed to less than $400 million. If Pfizer’s performance continues to show weak growth in the second half of the year, Roche has the opportunity to surpass Pfizer and claim the top spot among pharmaceutical companies by the end of 2019. Additionally, Merck & Co. swapped positions with Johnson & Johnson, propelled by the strong momentum of its drug Keytruda.

Both Pfizer and Sanofi highlighted in their annual reports the impact of China’s “4+7” volume-based procurement program on their revenues. In 2018, Pfizer’s primary growth drivers were China and other emerging markets, with the Chinese market achieving over 20% growth. However, in the first half of 2019, Pfizer’s Upjohn division, which focuses on off-patent and generic medicines, experienced a significant decline in performance, largely attributable to a 20% drop in its China business due to the volume-based procurement program. Sanofi issued warnings regarding certain products in its pipeline, indicating that sales of Plavix and Aprovel/Avapro might decline in the second half of the year as China’s volume-based procurement initiative advances.

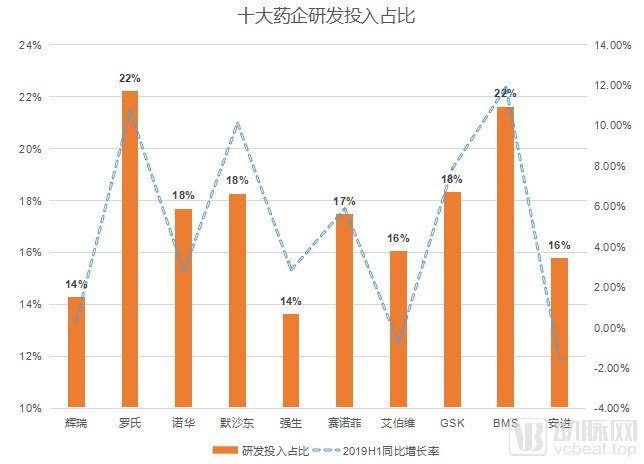

Comparison of R&D Investment Proportions and H1 2019 Growth Rates Among the Top 10 Pharmaceutical Companies

Pharmaceutical companies generally maintain their R&D investment at around 15-20% of their revenue (Johnson & Johnson did not disclose the R&D investment for its pharmaceutical business, so the data reflects the proportion of total R&D investment). Interestingly, when we overlay the year-on-year growth rate of pharmaceutical companies with their R&D investment, a clear positive correlation emerges between the two.

New drug development is gradually becoming decentralized, with a large number of startup pharmaceutical companies entering this high-barrier, heavily regulated industry. Consequently, many large pharmaceutical companies are progressively reducing their R&D expenditures and acquiring new drug pipelines through mergers and acquisitions. However, in terms of the correlation between R&D investment and pharmaceutical company growth, maintaining an R&D expenditure ratio of approximately 20% may be key to sustaining rapid growth.

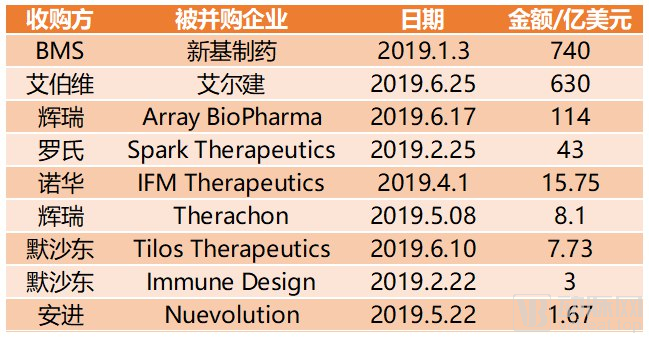

Top 10 Pharmaceutical M&A Deals in H1 2019

The most closely watched acquisitions in the first half of 2019 were undoubtedly Bristol Myers Squibb’s (BMS) acquisition of Celgene at the beginning of the year and AbbVie’s acquisition of Allergan in mid-year. The transaction values of these two deals were roughly similar, and the sentiment in the secondary market appeared largely consistent as well.

On January 3, 2019, Bristol Myers Squibb (BMS) announced its acquisition of Celgene for $74 billion. BMS’s stock price plummeted that day, falling from $52.43 to $45.12, a decline of 14%. A similar situation occurred with AbbVie. On June 4, 2019, AbbVie announced it would acquire Allergan for $63 billion. AbbVie’s stock price plunged that day, dropping from $78.45 to $65.70, a decrease of 16%.

If compared by revenue-generating capacity, Celgene is undoubtedly far more valuable than Allergan. Celgene holds Revlimid, the second-most valuable drug globally, which generated $8.4 billion in revenue and $3.1 billion in net income in the first half of 2019, approaching the scale of the top ten pharmaceutical companies. Allergan has not yet released its second-quarter financial report; although its revenue for the first quarter of 2019 reached $3.6 billion, it reported a net loss of $2.4 billion.

AbbVie’s acquisition of Allergan was likely driven by the hope of identifying the “next Humira” from Allergan’s drug pipeline. Allergan is one of the few major pharmaceutical companies that does not operate in the oncology space. It currently has 68 clinical trials underway, with 43 of them in Phase III/IV stages. Its core business spans neurological disorders, gastrointestinal diseases, ophthalmic conditions, and other therapeutic areas, focusing primarily on indications with large patient populations and suboptimal existing treatments, such as macular edema, diabetic gastroparesis, and migraine.

Therefore, in the coming years, Allergan is likely to see a succession of drug launches, each with significant market potential. If even one of these drugs achieves substantial success, Allergan will have the opportunity to reverse its downward trend. This is precisely why AbbVie has made a significant bet on Allergan.

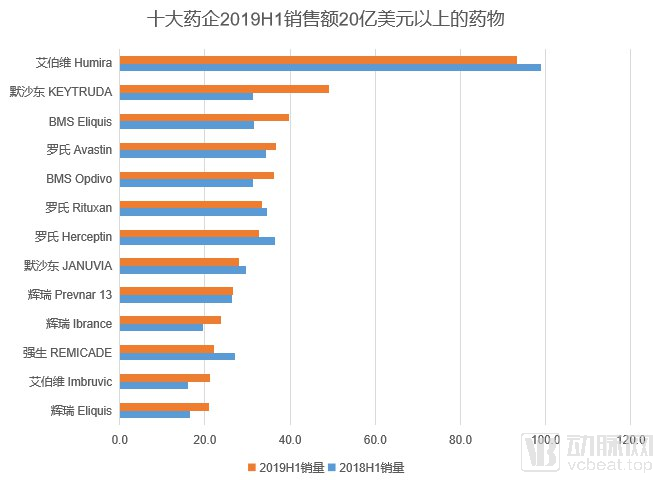

Top 10 Pharmaceutical Companies’ Drugs with Sales Exceeding RMB 2 Billion in H1 2019

AbbVie’s Humira finally showed signs of fatigue in the first half of 2019, with sales reaching $9.32 billion, a decrease of $570 million compared to the same period in 2018, representing a year-on-year decline of 5.84%. Although Humira’s semi-annual sales of nearly $10 billion still left competing drugs far behind, as we predicted at the beginning of the year, the decline in sales caused by patent expiration in the European market has indeed impacted AbbVie’s overall performance. AbbVie’s performance in the first half of 2019 decreased by 0.80% year-on-year, with Humira undoubtedly being the most critical contributing factor.

In the PD-1 market, the competition between Keytruda and Opdivo has long been a topic of widespread discussion. In the first half of 2018, Opdivo still held a slight lead. However, amid Keytruda’s aggressive expansion of indications, Keytruda surpassed Opdivo in sales for the first time by the end of 2018. The performance in the first half of 2019 firmly declared Keytruda’s victory in this rivalry.

Keytruda’s sales in the first half of 2019 reached $4.9 billion, a year-on-year increase of 56.60%. Although Opdivo also maintained growth, with its sales hitting a new high of $3.62 billion, it has been left far behind by Keytruda. More alarmingly, among the 638 clinical trials currently under development by Merck & Co., 414 are related to Keytruda.

Celgene’s Revlimid, the second best-selling drug in 2018, reached a new sales peak of $5.31 billion in the first half of 2019 (1H 2019), representing a year-on-year increase of 13.3%. Amid declining sales of Humira, Revlimid has emerged as the strongest contender for the next “blockbuster drug” title. However, Keytruda is rapidly catching up, narrowing its sales gap with Revlimid to $400 million in 1H 2019 thanks to its robust growth. If Keytruda can maintain this strong momentum in the second half of the year, it will have the opportunity to challenge Revlimid for the top spot in 2019.

Although Opdivo did not prevail in its competition with Keytruda, its sales of $3.62 billion in the first half of 2019 (1H 2019) were sufficient to place it among the top five single-drug products by sales volume across the top ten pharmaceutical companies. In addition to Opdivo, Eliquis, another star drug in Bristol Myers Squibb’s (BMS) portfolio, also performed well in the first half of the year, with total sales reaching $3.97 billion, an increase of $810 million compared to the same period in 2018 (1H 2018). These two drugs accounted for 62% of BMS’s total sales in 1H 2019, helping BMS secure a position among the top ten pharmaceutical companies.

On July 30, 2019, VCBeat compiled data on 13,418 commercially sponsored, active drug clinical trials from ClinicalTrials.gov. By systematically reviewing information on indications, phases, sponsors, and current status for each trial, VCBeat ultimately consolidated the data into a Global Drug Clinical Trials Database.

To more clearly illustrate the strategic directions of the top ten pharmaceutical companies, we screened 3,587 clinical trials directly participated in by these companies during the first half of 2019 (H1 2019) from clinical databases. We conducted a comprehensive analysis of their pipeline richness, therapeutic area distribution, and focus on high-demand indications.

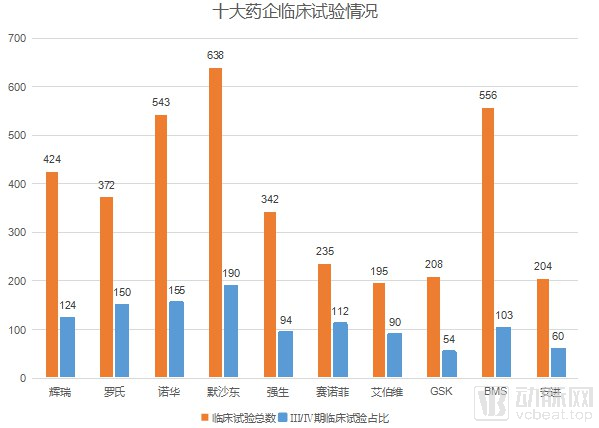

Number of Clinical Trials in Development and Proportion of Phase III/IV Clinical Trials Among the Top Ten Pharmaceutical Companies

As of July 30, 2019, the clinical trial landscape of the top ten pharmaceutical companies is shown in the figure above. The status of clinical trials reflects the drug pipeline reserves of these companies. Merck & Co., Bristol Myers Squibb (BMS), and Novartis each had more than 500 registered clinical trials, with Merck leading the pack with 638 clinical trials, including 190 Phase III/IV trials. AbbVie, on the other hand, had only 195 ongoing clinical trials, making it the only company among the top ten with fewer than 200 trials. The lack of a robust downstream drug pipeline may have been one of the key reasons behind AbbVie’s acquisition of Allergan.

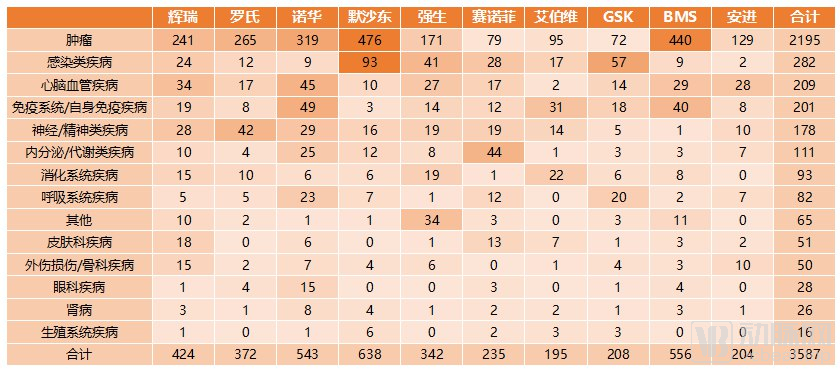

Distribution of Therapeutic Indications in Clinical Trials Under Development by the Top 10 Pharmaceutical Companies

In terms of allocation across therapeutic areas, the top ten pharmaceutical companies are roughly divided into two camps.

One group includes Merck & Co., Roche, and Bristol Myers Squibb (BMS). The majority of sales for these three pharmaceutical companies is largely driven by a few top-performing drugs. In terms of clinical pipeline strategy, these companies also focus primarily on their key drug pipelines. The advantage of this approach lies in the fact that long-term R&D efforts within the same therapeutic area can accelerate the accumulation of expertise, thereby streamlining subsequent development processes. Additionally, successful single-agent drugs can deliver substantial growth momentum; for instance, Merck experienced explosive growth in the past two years, largely propelled by the strong performance of Keytruda. However, the drawbacks of this strategy are also evident, as it leaves companies highly vulnerable to the impact of patent cliffs.

Other pharmaceutical companies have a relatively balanced distribution across indications. Pfizer has established a presence in nearly all disease areas, while Novartis, the third-largest pharmaceutical company, did not even have a single drug with sales exceeding $2 billion in the first half of 2019. This development strategy is more stable, ensuring long-term, steady growth in performance without sudden market shocks from other drugs, and carries minimal patent cliff risk. However, the downside is a lack of explosive growth potential, as diversified investments may lead to slower progress in certain fields.

Oncology is a key therapeutic area of focus for the top ten pharmaceutical companies. In particular, Merck & Co. and Bristol Myers Squibb (BMS) have made substantial efforts to expand the indications for Keytruda and Opdivo, respectively. The second most heavily watched therapeutic area is infectious diseases. Major pharmaceutical companies are actively strategizing their presence in areas such as HIV, HCV, and pneumococcal disease, where clinical solutions are either unavailable or suboptimal.

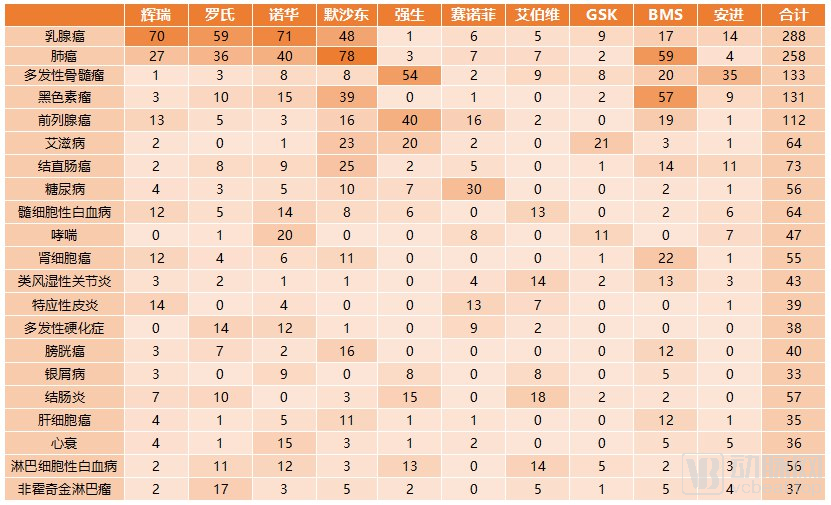

Distribution of Popular Indications in Clinical Trials Under Development by the Top 10 Pharmaceutical Companies

In terms of specific indications, the five most highly regarded indications are all oncology-related. Large pharmaceutical companies primarily focus on oncology and chronic diseases. The former addresses critical unmet patient needs, while the latter offers strong market prospects. Rare diseases remain relatively underrepresented in clinical trials conducted by large pharmaceutical companies, with “major diseases” continuing to be their core focus.

Breast cancer and lung cancer are currently the two most closely watched indications. The field of breast cancer finally saw new progress in 2019. In March 2019, Roche’s Tecentriq received FDA approval for the treatment of triple-negative breast cancer (TNBC), becoming the first immunotherapy approved for this indication. Novartis’s Ibrance was approved in April 2019 for the treatment of male breast cancer. Additionally, in late July, Merck & Co. announced that Keytruda, in combination with chemotherapy, had met its primary endpoint in the treatment of triple-negative breast cancer, demonstrating significant improvement compared to chemotherapy alone. Given the current landscape of breast cancer research and development, this therapeutic area is poised for successive breakthroughs in the coming years. However, which drug will ultimately dominate the market will depend on clinical efficacy and market acceptance.