Medical Device Top 8 Battle: Medtronic Leads the M&A Marathon, with Johnson & Johnson and Philips Close Behind

Danaher

Product Design and Manufacturer

Siemens Healthineers

Medical Solutions Provider

Medtronic

Chronic Disease Medical Device and Therapy Developer

Cardinal Health

Healthcare Service Provider

Johnson & Johnson

Healthcare Product Manufacturers, Health Service Providers

According to EvaluateMedTech's forecast, the global medical device market will reach $477.5 billion by 2020. Despite the allure of this lucrative market, it must be acknowledged that the global medical device industry remains dominated by a few large international corporations.

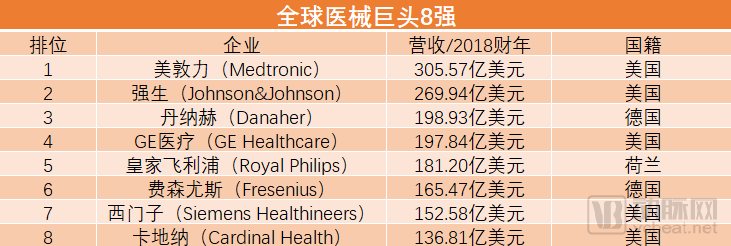

In mid-2019, major companies in the medical device sector successively released their annual reports for the 2018/2019 fiscal year. In light of this, VCBeat (WeChat ID: vcbeat) streamlined the Top 100 Medical Device Companies list published by Medical Design & Outsourcing, selecting the top eight companies to create a “Top 8 Medical Device Companies” ranking for cross-comparison.

Notably, a review of the development histories of these eight companies reveals that most have followed a growth pattern characterized by technology-driven origins, market expansion, and transformation through mergers and acquisitions. By examining their activities in the capital markets, we also seek to answer why medical device giants invariably become “shopping sprees” in their later stages of development.

Compiled by VCBeat from the 2018 fiscal year annual reports of various companies

From fiscal year 2017/2018 to fiscal year 2018/2019, many of the giants on the list underwent varying degrees of business adjustments (such as consolidating core businesses and divesting non-core operations), leading to changes in revenue compared to the previous fiscal year or even early-year expectations. These shifts can be glimpsed through the commercial activities of these industry leaders from 2018 to the present.

Medtronic

Medical Device Leader, Retains Top Spot

Despite Medtronic’s recent business divestitures, the company remained heavily focused on mergers and acquisitions between 2017 and 2019. An analysis of several M&A deals reveals that, on one hand, Medtronic continued to prioritize and strengthen its orthopedics and surgical businesses through acquisitions; on the other hand, its strategic entry into the surgical robotics sector has become increasingly clear.

Johnson & Johnson

Venturing into AI Healthcare + Surgical Robots

Since 2017, Johnson & Johnson has been continuously expanding its list of acquisitions of medical device companies. By early 2019, Johnson & Johnson had completed nine acquisitions, the most notable of which was the $3.4 billion acquisition of Auris Health, a surgical robotics company. Although Auris’s currently commercialized products are limited to applications in lung cancer surgery, Johnson & Johnson’s primary objective in the acquisition was to complement its previously acquired Orthotaxy orthopedic surgical assistance robot.

While strengthening its medical device segment, Johnson & Johnson is also accelerating the divestiture of other businesses, initiating a "fire sale" of its device portfolio.

Since 2017, Johnson & Johnson has successively announced the cessation of operations and exit from its Animas insulin pump business and Codman neurosurgery business. To date, after divesting its diagnostics, cardiovascular stent, diabetes care, and sterilization/disinfection businesses, Johnson & Johnson’s medical device segment has been streamlined to focus on orthopedics, surgery, and vision care, with a strategic emphasis on advancing surgical robotics technology.

These measures clearly demonstrate Johnson & Johnson MedTech’s determination to enter the AI medical device sector, particularly the field of surgical robotics.

Danaher

Life Sciences Emerge as the Primary Growth Engine

In 1969, DMG Realty Investment Trust, the predecessor of Danaher, was established; in 1986, the company was renamed Danaher and achieved strategic transformation through mergers and acquisitions. Danaher’s M&A strategy can be divided into four phases: finance-oriented, business-oriented, platform-oriented, and industry influence-enhancing.

It is worth noting that in 2004, during the third phase, Danaher entered the medical diagnostics field through the acquisition of Radiometer. In 2005, Danaher acquired Leica Microsystems to enter the life sciences sector. Through these two acquisitions, Danaher established its own medical diagnostics and life sciences platforms, laying the groundwork for future high-speed growth as a powerful engine, and undertook a series of strategic initiatives centered around these two segments.

Having completed 47 acquisitions from 1981 to 2019, Danaher can be regarded as a master of mergers and acquisitions even among medical device giants. In particular, the 2019 acquisition of GE Healthcare’s life sciences biopharmaceutical business (BioPharma) not only drove a significant surge in Danaher’s stock price but also positioned the company to achieve full-year 2019 revenue of $9.5 billion. This development is expected to propel the Life Sciences platform’s revenue well beyond that of the Medical Diagnostics platform, making it Danaher’s most important business segment.

GE HealthCare

Divestiture + M&A: A Parallel Development Strategy

Compared to GE Healthcare’s aggressive acquisition strategy, its divestitures are even more noteworthy. At the beginning of 2019, Danaher Corporation announced it would acquire GE’s Life Sciences biopharmaceutical business (BioPharma) for $21.4 billion. This business generated approximately $3 billion in revenue in 2018. Spurred by this news, GE’s stock opened more than 11% higher on the day of the announcement.

Both the divested BioPharma business and the retained Pharmaceutical Diagnostics business were acquired by GE. Compared to GE’s core medical diagnostic imaging business, its life sciences operations were integrated into GE Healthcare relatively late. As a result, the BioPharma business was able to form a powerful combination with Danaher’s life sciences portfolio, while the retained business continues to supply complementary contrast agents and molecular imaging consumables for GE’s imaging equipment. Consequently, GE Healthcare has benefited in the stock market.

Philips

The Arrival of the Digital Health Era

Since early 2017, Philips has completed 18 acquisitions in the medical technology sector and is transforming into a technology provider in the healthcare industry. Between 2017 and 2018, in addition to medical imaging technology, Philips’ acquisition strategy also focused on comprehensive healthcare service areas such as digital health (e.g., mobile health app developers, remote home care monitoring platforms) and big data-driven healthcare management.

Philips’ transformation in the healthcare sector exhibits three key characteristics: First, Philips has progressively consolidated and integrated its product lines around thematic focuses, making operations more holistic and efficiency-driven by centering them on relevant themes. Second, it has reduced its interest in non-healthcare businesses and is now fully recognized by the industry as a health technology company. Third, Philips has evolved from a manufacturer primarily focused on equipment and hardware into a solutions-oriented enterprise that, building on its existing advanced devices, addresses the entire patient care journey and disease lifecycle.

Fresenius

The Medical Device Giant Reigning Supreme in Dialysis

Fresenius, based in Germany, boasts a long history that can be traced back to the 15th century. In 1912, Eduard Fresenius, the owner and pharmacist of Hirsch Pharmacy, formally established Fresenius as a pharmaceutical manufacturing enterprise, primarily responsible for producing specialty medications such as therapeutic formulations, serum reagents, and rhinitis ointments. From 1933–1934 through the 1950s, Fresenius built new production lines for intravenous infusion devices. Starting in 1966, the company began exporting its dialysis equipment and dialyzers to international manufacturers, capturing a significant market share in this field. In the 1970s, Fresenius developed the world’s first hemodialysis machine with volume-balanced chamber-controlled ultrafiltration, leveraging this innovation to drive its subsequent growth. Today, Fresenius is a global leader in the provision of dialysis products and services.

Since the beginning of the 20th century, Fresenius, like other medical device giants, has embarked on a path of mergers and acquisitions. In addition to acquiring dialysis companies that consolidate its core business, it has also begun to acquire comprehensive healthcare service providers such as hospitals, in preparation for the company’s comprehensive transformation.

Siemens

Imaging Business Is the Main Revenue Driver, While Diagnostic Business Holds Significant Potential

Siemens Healthineers, which built its foundation on medical imaging equipment, holds an unquestionably core position in the medical imaging sector. Prior to its strategic restructuring, Siemens Healthineers operated three major business segments: Imaging Diagnosis (including ultrasound diagnosis), Advanced Therapies, and Laboratory Diagnostics. Among these, the Imaging segment generated significantly higher revenue than the other two divisions.

In terms of clinical treatment, its performance in the first quarter of 2019 declined compared to the same period in 2018. Siemens Healthineers primarily focuses on treatments in the cardiovascular and oncology fields; however, its current product portfolio is relatively limited. Given the broad prospects of "integrated diagnosis and therapy," its capital investment is likely to increase.

Furthermore, Siemens Healthineers established its medical diagnostics product line through major acquisitions, becoming the world’s second-largest medical diagnostics company, trailing only Roche. Although the revenue from its medical diagnostics business is not as substantial as that of its imaging division, the overall growth rate of the industry is comparable. Siemens Healthineers places particular emphasis on the Atellica solution, stating that it will optimize the platform in 2019 to reduce costs.

Cardinal Health

The Low-Key Diversified Conglomerate

Cardinal Health’s business comprises four major segments: the Pharmaceutical Wholesale and Distribution segment, the Medical Products and Services segment, the Medical Technologies and Services segment, and the Automation and Information Services segment. Among these, sales of pharmaceuticals and medical devices still account for more than 95% of its total revenue.

Meanwhile, like many medical device giants, Cardinal Health has grown rapidly through the acquisition of numerous companies, with a business scope that surpasses even those of many companies known for their diversification.

Through mergers and acquisitions, Cardinal Health has transformed from a pure pharmaceutical and medical device wholesaler into an industry-wide service provider, delivering “delightful” services to every segment of the supply chain and thereby creating an unprecedented market.

A review of the development history of the top eight medical device companies reveals that repeated expansions in scale and business scope, along with several strategic development guidelines, have consistently been intertwined with and inseparable from mergers and acquisitions.

Taking Medtronic as an example, since the 1990s, the company has completed nearly 100 M&A transactions, with a total disclosed value exceeding $73 billion. Several of these acquisitions played a pivotal role in Medtronic’s development, enabling a qualitative leap in its legacy businesses.

Based on this, we can outline the typical development path of medical device giants:

1. In the early stages of development, most companies were primarily driven by technological R&D;

2. After the successful commercialization of its technology and products, the company began to achieve marketing at scale;

3. For strategic reasons, the company has embarked on the inevitable path for medical device giants—mergers and acquisitions. Overall, technology-driven medical device companies must undergo industry consolidation to achieve market leadership.

For these industry giants, after undergoing technology-driven transformation, achieving mature business development, and reaching market scale, they tend to shift their focus toward the market side, while facing the challenge of being “too large to pivot” in R&D. To consolidate their positions and avoid disruption by small and medium-sized innovative companies, mergers and acquisitions have become a direct means for traditional medical device giants to break through product and technological silos.

Kind Reminder

This article is based on VCBeatSpecial Topic Pro“Top 8 Medical Device Companies: Johnson & Johnson and Philips Close Behind, Medtronic Leads the M&A Marathon”Compiled and generated; updates on the top eight companies will continue.

More unicorn rankings, more investment and financing news, more in-depth analyses of leading companies’ businesses, and more comprehensive industrial consulting insights—all available atVCBeatSpecial Topic Pro!