Beyond Diagnostic Assistance: How Leading Medical Imaging AI Companies Are Building a New Ecosystem and Exploring Novel Commercial Pathways

DeepWise

Developer of Artificial Intelligence Medical Imaging Diagnosis System

VoxelCloud

Developer of Intelligent Imaging Systems

YITU

Provider of Full-Stack Intelligent Healthcare Product Solutions

Airdoc

Retinal Imaging Artificial Intelligence Field Product Developer

HY Medical

Provider of Medical Imaging and Oncology Radiotherapy Platforms

Infervision

Artificial Intelligence Product Developer

SHANGGONG

Intelligent Diagnosis Product Provider for Fundus Imaging

In 1987, the Time Delay Neural Network (TDNN) proposed by Alexander Waibel can be traced back as the first CNN algorithm in history. However, due to limited computational power and data, CNNs did not become a focal point for scholars at that time. It was not until 19 years later, when Geoffrey Hinton from the University of Toronto redefined deep learning, that the representational learning capability of CNNs once again became a hot topic of widespread interest.

Subsequently, the application of CNN’s capabilities in data mining and machine learning to image processing gradually matured. Forward-thinking individuals began to realize that this emerging technology held substantial potential for development in the medical field.

Therefore, the first wave of entrants into the field of AI for medical imaging comprised professionals from the internet industry.

Since 2015, a large number of medical imaging AI companies have been established, flocking to the blue-ocean market of imaging AI. However, it was only after entering the field that many realized: without sufficient medical expertise, how could one overcome the formidable barriers? Recalling those early days, Chen Kuan from Infervision said with a wry smile, “At that time, I didn’t even want to look at the products I had developed.”

The transformation began in 2017. As waves of internet professionals continuously collaborated with physicians, gaining an in-depth understanding of clinical workflows, and as the state gradually recognized the importance of AI, AI products started to enter clinical pilot programs. A bridge of mutual assistance between physicians and entrepreneurs was established, enabling AI enterprises to experience rapid development over the following two years.

2019 marked a year of widespread adoption for medical artificial intelligence, as evidenced by the emergence of more companies focused on smart healthcare. Meanwhile, sectors such as health management, community care, and even medical aesthetics began cautiously exploring the integration of AI. In response, VCBeat conducted research on artificial intelligence, with a set of data that may help us gain a clearer understanding of the overall development of medical AI in 2019.

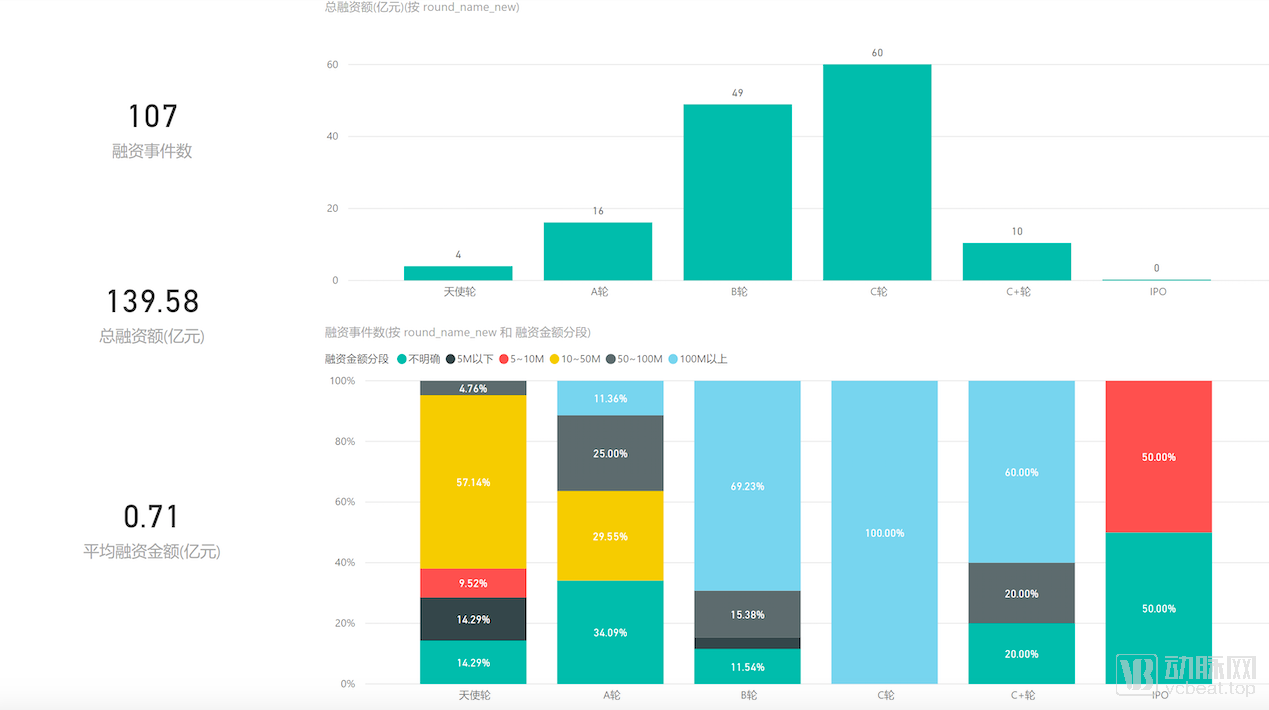

According to data from the VCBeat knowledge base, a total of 107 global medical AI financing events occurred between December 24, 2018, and August 20, 2019, with total funds raised amounting to RMB 13.958 billion (excluding financing events with undisclosed investment amounts). The specific distribution by funding round and financing amount bracket is shown in the figure below.

As clearly shown in this chart, medical AI financing events in 2019 were concentrated in Series B and Series C rounds. In contrast, no companies successfully completed an IPO, and there were only four angel-round deals. The overall distribution of these events followed a pattern of “large middle, small ends.” This may suggest that leading AI companies have established substantial barriers to entry, making it more difficult for new players to enter the market.

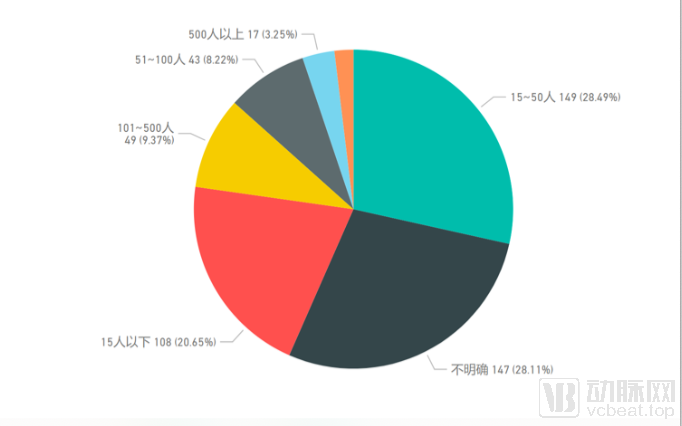

The scale of medical AI enterprises has also expanded. As shown in the chart above, companies with more than 50 employees account for only one-quarter of the total, indicating a clear concentration of high-quality resources.

Among these, AI imaging companies were among the earliest to engage in artificial intelligence; by observing their developments, we may gain insights into the broader industry. So, how have these companies fared?

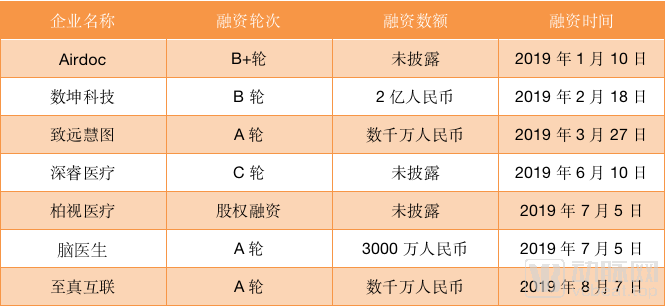

As shown in the figure above, with VoxelCloud completing its Series B financing and Infervision completing its Series C financing by the end of 2018, all leading medical imaging companies have secured new rounds of funding.

By mid-2019, leading medical imaging companies had already matured their products for pulmonary nodule detection and breast cancer screening. Leveraging data assets and hospital networks, these companies are gradually establishing competitive barriers, with their corresponding AI products entering the clinical approval stage.

During the approval waiting period, leading enterprises are continuously exploring the potential value of existing resources and seeking possible commercialization paths for AI. The most critical question now is: Who will become the payer for imaging AI?

Liu Shiyuan, Director of the Department of Diagnostic and Interventional Radiology and Nuclear Medicine at Changzheng Hospital, once stated, “The future work of radiology departments will undoubtedly be intelligent, with structured reporting.” Implicitly, AI is bound to become an integral part of radiology departments, but not just yet.

Beyond Radiology: Is There Still Room for AI Development? The Answer Is Yes. Pharmaceutical companies, patients, and insurance providers are all potential payers for AI imaging solutions, while hospitals are not limited to radiology departments in their willingness to pay for such products.

Let’s start with hospitals. Different hospitals have varying demands for products. For AI products to penetrate tertiary (Grade A) hospitals, they must address two key needs of physicians in these institutions: efficiency and research. Currently mature AI products for CT lung, CT liver, and brain MRI scans are designed to meet physicians’ demand for improved image interpretation efficiency. However, this accounts for only a portion of radiologists’ working time. A need more closely aligned with physicians’ priorities is research—specifically, assisting them in managing and leveraging data in the era of big data.

For township-level hospitals with relatively weaker medical capabilities, AI companies can build private clouds and cloud-based PACS connected to medical consortia, or provide in-house training to enhance physicians’ image interpretation and report-writing skills. Although this market segment is substantial, the construction budgets for smart hospital initiatives are constrained by the limited scale of these institutions, which in turn affects their willingness to pay for AI solutions. Nevertheless, township-level hospitals demonstrate a stronger willingness to pay for AI-assisted tools compared to tertiary Grade A hospitals.

The most likely paying healthcare institutions include private specialized hospitals, mixed-ownership hospitals, and third-party imaging centers. These three types of institutions lack the medical resources to compete with Grade 3A hospitals and thus require AI to fill the gap; they also suffer from a lack of public trust in their systems, necessitating AI to enhance the perceived technical prowess of these hospitals.

Overall, selling AI-enabled devices to hospitals, building cloud-based PACS platforms, or offering non-AI imaging-related services (such as digital film) will remain the primary revenue sources for AI companies for a considerable period, while the commercialization of AI-assisted diagnostic services still has a long way to go.

Revisiting Pharmaceutical Companies. AI imaging companies can meet three key needs of pharmaceutical firms: first, serving as a CRO to reprocess pathological data; second, leveraging big data tools to screen patients for clinical trials; and third, facilitating precise digital marketing for pharmaceutical companies through community-based collaborations.

The most accessible channel for monetization stems from digital marketing. AI imaging companies can collaborate with medical affairs departments to conduct real-world data studies, assisting in the validation of drug therapeutic efficacy and standardized diagnosis and treatment models. They can also partner with marketing and sales departments to build academic platforms that facilitate pharmaceutical sales.

Since these three types of business do not require AI imaging companies to obtain approval from the National Medical Products Administration (NMPA), but rather rely on resources integrated through their long-term strategic layouts, such collaborations are likely to become one of the important revenue sources for AI medical imaging enterprises.

Compared to the two aforementioned models, establishing patients as a stable source of revenue is significantly more challenging. Although AI-based multidisciplinary team (MDT) consultations and auxiliary diagnostics have been included in the fee schedules of many Grade A tertiary hospitals, the inherent uncertainty of AI technology makes it difficult for enterprises to encourage physicians to recommend AI products to patients.

Meanwhile, due to insufficient market education, the vast majority of patients still tend to choose traditional services without AI cores when deciding between AI-enabled and non-AI services. However, with advancements in technology, policy, and patient awareness, patients are likely to become stable payers in the future.

How Are Leading Medical Imaging Companies Seeking Growth Amidst Challenges? VCBeat interviewed nearly ten top-tier medical imaging AI companies in an effort to outline the underlying logic. It is important to note that while some of the companies mentioned have achieved breakthroughs in multiple areas, this article selects only a portion of each company’s innovative business lines as case studies.

Medical institutions serve as the starting point for AI companies. Nearly all early-stage AI imaging products were designed to serve physicians. Therefore, even though these products have not yet become profitable, they have laid the groundwork for the advancement of new offerings. While ensuring continuous iteration of existing products, companies are expanding outward from their initial focus on medical imaging.

Infervision: From Perfecting AI with Physicians to Building AI Together with Physicians

“Clinical practice is not the only avenue for physicians to realize their professional value. As medicine is an experience-based discipline, physicians hope to devote more time to organizing clinical experiences and exploring unknown possibilities, synthesizing these insights into academic papers for exchange and learning among like-minded peers,” stated Xi Weiling, President of Marketing at Infervision.

As collaboration with physicians has continued to advance, Infervision’s R&D team has gained a deeper understanding of clinical workflows and needs, enabling them to help physicians standardize data structures, leverage data effectively, and employ customized algorithmic models for scientific research. The concretization of this approach has given rise to the current InferScholar Center AI Scholar Research Platform.

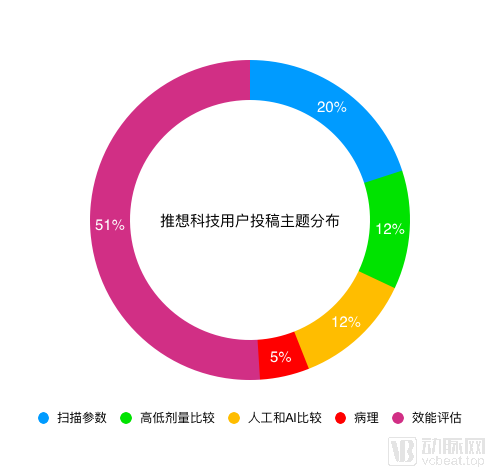

Focusing solely on RSNA submission statistics, this research platform facilitated the completion of over 300 RSNA submissions in 2019 by multiple affiliated clinical hospitals. The submissions covered areas including human versus AI comparison, pathology, performance evaluation, scanning parameters, and low- versus high-dose comparison (12%).

In this way, Infervision has effectively translated researchers’ experience in communicating with physicians, greatly expanding the value and application scenarios of deep learning in the healthcare sector, and enabling artificial intelligence to evolve from “assisting clinical diagnosis” to “assisting clinical research.”

Through this AI-based research platform, Infervision aims to provide original artificial intelligence research services across all departments and disease types in hospitals. The platform features dozens of AI algorithms and single-disease data management capabilities, supporting scientific research, teaching, and industrial transformation throughout the entire hospital. For Infervision, this model will help secure greater medical resources, empowering AI with enhanced creative potential.

DeepWise: The Value of Intangible Assets Is Difficult to Measure

Unlike Infervision, the DeepWise Research Institute, led by Professor Yu Yizhou, Chief Scientist at DeepWise and an IEEE Fellow, relies more on its own scientific research strength to establish comprehensive research collaborations with medical institutions and physicians. Balancing practicality with foresight, Professor Yu not only leads his team in tackling technical challenges for specific projects but also collaborates with external universities and research institutes to develop forward-looking technologies.

These research collaborations span a wide range of fields, covering common scenarios such as breast cancer, pulmonary nodules, and stroke, as well as pancreatic cancer, which is relatively niche in the AI community. This has laid a solid foundation for DeepWise’s strategy of addressing a comprehensive spectrum of diseases. Beyond medical applications, DeepWise has also produced numerous research achievements in the field of fundamental computer vision.

In 2019 alone, DeepWise Research Institute had eight papers accepted by CVPR 2019, a top-tier artificial intelligence conference, achieving innovative breakthroughs in technologies such as image recognition and medical image analysis, and ranking among the leading technology companies in China in terms of the number of published papers. At MICCAI, the premier international conference on medical image analysis held in October, and ICCV, the top international conference on computer vision held in November, DeepWise Research Institute had another ten research papers in the field of medical AI accepted. Additionally, two more papers from DeepWise were accepted by ER and MIA.

To date, DeepWise Research Institute has published more than 50 top-tier academic papers, with a cumulative impact factor exceeding 80 and an acceptance rate surpassing 50%. The institute has published nearly 30 papers in leading journals and conferences in artificial intelligence and machine learning, such as Science Robotics, TPAMI, TCyb, TIP, ICML, CVPR, ICCV, ECCV, and AAAI. These publications cover the three premier international conferences in computer vision and pattern recognition. Notably, DeepWise has presented academic achievements at the highly prestigious CVPR conference (ranked in the Top 10 of Google’s 2019 Academic Rankings) for two consecutive years, placing it among the forefront of AI technology companies in China. Additionally, in the field of medical image computing and analysis, the institute has published more than 20 papers at top-tier venues such as IPMI, MICCAI, ISBI, and RSNA.

The value of scientific research is difficult to quantify, but it will undoubtedly be a valuable asset.

HY Medical: Extending Downstream from Holistic Solutions to Achieve Profitability in Digital Film and Other Businesses

Over the past two years, in addition to refining their core AI-assisted diagnostic tools, many medical imaging AI companies have been improving their data middle platforms and sparing no effort to expand their presence in hospitals, aiming to build a sufficiently large market foundation to accelerate future product deployment. Among them, HY Medical stands out as a leader.

Through application-layer services such as the AI quality control platform, cloud imaging platform, AI-assisted diagnosis platform, big data research platform, digital smart films, and AI structured reporting, HY Medical can build bridges across regions. The more hospitals connected, the greater the value generated.

Taking digital smart film as an example, HY Medical integrates cloud-based films with AI-assisted diagnostic results. This means that when patients access their films via WeChat, SMS, or mobile apps, they also receive corresponding AI-assisted diagnostic reference results. The operation of this service is predicated on the smart imaging big data platform already deployed by HY Medical.

HY Medical told VCBeat, “The smart imaging big data platform serves as the foundation. Many hospitals chose to partner with us precisely because of our platform-based solution capabilities. Without the support of this platform, it would be difficult for us to integrate workflows across services such as digital film and research platforms. After several years of deployment, HY Medical is poised to further accelerate the implementation of its products.”

Shukun Technology: Focused on AI R&D for Cardiovascular and Cerebrovascular Diseases

As a leading AI company in the cardiovascular and cerebrovascular fields in China, Shukun Technology, having completed its Series B financing, is at the forefront of the industry. Compared to other medical imaging enterprises, Shukun Technology appears more focused on its existing AI products.

Since the global launch of its AI-assisted diagnostic system for coronary CTA in early 2018, Shukun Technology’s cardiac AI product portfolio—covering coronary CTA, coronary CT-FFR, plaque component analysis, gated calcium scoring, and aortic morphology and function—has established a comprehensive AI-driven diagnostic and therapeutic pathway for coronary artery disease, spanning from morphological to functional assessment. These solutions have been implemented in leading cardiovascular centers such as Beijing Anzhen Hospital and Fuwai Hospital, as well as in over 150 Grade IIIA hospitals across China, becoming integrated into routine departmental workflows and securing the largest share of the cardiovascular AI market.

In May this year, Shukun Technology launched the Jiafei CareSphere Advisor AI Imaging Diagnosis Platform, integrating five cardiac imaging AI solutions into a comprehensive, multi-task model-based AI solution tailored to clinical scenarios and organized by examination site. This platform fully covers the clinical workflow, establishing a holistic cardiac imaging artificial intelligence system that enables multi-dimensional analysis for single diseases, multi-task processing across anatomical regions, and end-to-end coverage of the entire diagnostic process.

Throughout its development, Shukun Technology has focused its efforts on the research and development and clinical trials of AI products for cardiovascular and cerebrovascular diseases. In this regard, CEO Ma Chun’e stated, “Currently, department heads at top-tier Grade 3A hospitals, presidents of regional central hospitals, and directors of private hospitals have provided positive feedback on our products and included them in upcoming collaboration plans, further strengthening our confidence that the commercialization path for cardiovascular and cerebrovascular solutions is entirely viable.”

“Of course, pharmaceutical companies and high-value consumables manufacturers have also approached us for collaboration. However, while considering these opportunities, we will continue to prioritize the implementation of our existing cardiovascular and cerebrovascular products, as this is the core through which Shukun demonstrates its value.”

Collaboration with medical device companies has become the norm for artificial intelligence (AI) enterprises, typically manifested as device giants building ecosystems akin to an App Store, where products from various AI companies compete. Nowadays, however, there is a growing trend of AI enterprises directly engaging in the customized design of medical devices. The advantage of customization lies in the ability of the devices to align maximally with the data and algorithmic requirements of AI, while also enabling product design tailored to specific scenarios.

The collaboration between pharmaceutical companies and AI firms differs from that with medical device manufacturers. Pharmaceutical companies place greater emphasis on the data independently collected and generated by AI enterprises during their hospital deployments. Leveraging this data enables pharmaceutical companies to make clinical trials and drug sales more targeted, resulting in significant cost savings. For instance, a pharmaceutical company selling cardiovascular and cerebrovascular drugs might seek collaboration with Shukun Technology, while a company marketing innovative diabetes treatments would engage SHANGGONG to assess the reliability of real-world data.

YITU Medical: Customizing Dedicated Low-Dose Bone Age DR for Children

In addition to continuously iterating on its existing AI products, YITU Medical is also exploring new partnerships to seek additional growth opportunities, with bone age assessment being one such area.

As an important indicator for assessing the growth and development of adolescents, bone age testing can more accurately and objectively reflect children's actual growth and development levels compared to indicators such as height and weight. Roughly estimated, in China

Over 100 million children and adolescents require annual growth and development monitoring. However, traditional bone age assessment methods are hampered by lengthy procedures, low efficiency in image interpretation, and poor consistency. Coupled with parental concerns about radiation exposure from X-rays, these factors significantly limit the clinical application of single-time bone age assessments and longitudinal bone age follow-ups.

Leveraging this as a breakthrough, YITU Medical launched an intelligent one-stop solution for pediatric growth and development assessment in July. This system is the first in the industry to achieve seamless integration of artificial intelligence technology with hardware devices (“software-hardware integration”), combining multiple features such as ultra-low radiation, intelligent imaging, AI-based image interpretation, and AI-driven growth and development assessment. The entire workflow—from imaging to interpretation to report generation—can be completed in just 5–10 minutes, with the intelligent image interpretation process taking only seconds. The absolute error between the AI’s interpretation results and those of senior pediatric endocrinologists is less than 0.3 years.

Yitu Medical told VCBeat, “When using general-purpose DR for bone age imaging, children’s other organs are exposed to a certain amount of scattered radiation, which has raised concerns among parents about radiation exposure. Therefore, addressing these two issues was the original intention behind our customized design of an intelligent one-stop solution for assessing children’s growth and development.”

Entering hospitals via medical devices is a sound strategy, but the regulatory approval category for AI products embedded in such devices still needs to be defined. For such a novel product, Yitu Medical may be able to pioneer new pathways through the approval process.

Tumashenwei: Extending to Clinical Departments through In-Depth Collaboration with Device Manufacturers

Tumai Shenwei has been a global strategic partner of GE Healthcare for some time. However, in terms of its 2019 initiatives, Tumai Shenwei is expanding the application scenarios of its products from serving radiology departments to covering clinical departments such as thoracic surgery, pulmonology, oncology, and radiation oncology, as well as multidisciplinary team (MDT) consultations. This expansion extends across all stages of screening, diagnosis, treatment, and rehabilitation.

In May, collaborations with Syno Vision, Dr. Li Zhong’s Physician Group, and Saiang International Medical Care highlighted Tuma Shenwei’s value in the practical application of 3D tumor image segmentation, delineation, and analysis during surgical procedures.

Currently, Tuma Shenwei can rapidly perform segmentation and volumetric measurement of organs, liver/lung/kidney segments, and automatically conduct quantitative analysis of the resection results; it supports clinicians in arbitrarily adjusting the position, angle, curvature, and other parameters of the segmentation plane according to surgical needs for surgical plan optimization; it enables the integration of anatomical structures with quantitative assessment of local function, effectively predicting postoperative hepatic function and surgical risks; it automatically calculates and delineates lesions on 3D images, meeting the requirements of various precision diagnosis and treatment applications.

SHANGGONG: Seeking Channels for Pharmaceutical Companies Starting from Chronic Disease Management

As an AI company focused on the management of eye diseases and diabetes complications, SHANGGONG is not involved in radiology. However, fundus AI has long faced commercialization challenges similar to those encountered by radiology AI. How can this bottleneck be broken? Pharmaceutical companies may be able to reach win-win agreements with AI enterprises.

Taking SHANGGONG’s focus on diabetes as an example, its treatment process is not a single point but rather a long continuum. Among all diabetic complications, ocular complications are the most challenging to manage. SHANGGONG provides AI-based screening for diabetic retinopathy to effectively manage these ocular complications, thereby establishing a smart management platform for diabetes and its complications.

Currently, SHANGGONG has established a medical service platform that encompasses scientific research, demonstration projects, departmental exchanges, and patient education. While providing patients with AI-based diabetic retinopathy screening services, the platform automatically updates patient information. Healthcare professionals utilize this platform to deliver free clinics, preventive education, and community-based diabetes management services to patients.

Liu Xiao stated, “Patients on the SHANGGONG platform tend to exhibit strong stickiness. As diabetes is a lifelong condition, patients undergo at least one check-up annually, which means they will remain active on the platform long-term, and we have an obligation to proactively remind them to get checked.” This demonstrates that the platform holds significant appeal for pharmaceutical companies.

In specific collaborations with large pharmaceutical companies, Liu Xiao categorizes them into two models: first, partnering with the medical affairs department to conduct real-world data studies, assisting in the validation of drug therapeutic efficacy and standardized diagnosis and treatment protocols; second, collaborating with the marketing and sales departments to build academic platforms and diversify forms of multi-party cooperation.

Overall, the key to SHANGGONG’s collaboration with pharmaceutical companies lies in its extensive hospital-patient network. This model is well-suited for establishing a patient-centric collaborative platform for pharmaceutical companies and physicians through innovative partnership frameworks.

Providing services directly to patients through the consumer end has gradually become a secondary option for many AI companies. By offering risk-free testing services, consumer-grade genetic testing has made a promising start. Similar to retail, for AI companies to pave the way for consumer payments, the key lies in how to effectively reach consumers.

Airdoc: From Ophthalmology to Optical Retail Stores

After securing Series B funding led by CITIC and Ping An in January 2019, Airdoc embarked on expanded AI research directed at consumers.

In the field of myopia prevention and control, Airdoc assists medical institutions in conducting vision prevention and screening for adolescents and making informed decisions on preventive measures. This includes analyzing the impact of multiple factors on myopia, such as daily outdoor activity time, near-work duration, daily life and study routines, poor eye-use habits, parental genetics, and nighttime lighting conditions. Airdoc provides comprehensive health risk assessments and eyeglass prescription recommendations, helping users mitigate vision impairment caused by various health risk factors.

Through its collaboration with Airdoc, Starry Vision has launched the “360-Degree Myopia Prevention and Control Solution,” which integrates end-to-end services including professional screening, AI-based prediction, regular follow-up examinations, AI-driven behavioral interventions, corrective solutions with professional products, and electronic health record management. This solution has now been implemented across its 1,200 Baodao Optical stores.

However, alleviating consumer apprehension toward AI requires joint market education efforts from both sides. Overall, this represents a significant B2C initiative.

VoxelCloud: Mobile-Based Diagnostic Initiatives

VoxelCloud Skin Insight was officially launched by VoxelCloud in December 2018. Leveraging a WeChat Mini Program as its platform, this consumer-facing AI product provides free image-based screening services directly to patients with skin conditions.

Specifically, patients can capture images of skin lesions using their smartphones and upload them to the cloud via the "Fuzhihui" platform. VoxelCloud will then leverage its dermatology knowledge graph to provide reliable reference recommendations for skin disease detection.

Many patients develop skin conditions in private areas, making it difficult for them to discuss their symptoms openly. VoxelCloud’s Skin Knowledge Hub provides patients with an opportunity to self-assess their condition before seeking medical attention, thereby encouraging proactive consultation. Furthermore, patients supported by the Skin Knowledge Hub can describe their symptoms more clearly to physicians during diagnosis and treatment, which also serves to support online medical consultations.

According to Ding Xiaowei, founder of VoxelCloud, although internet-based consultation platforms enjoy policy support, they still need to improve efficiency. In particular, many patients struggle to accurately describe their conditions during the initial complaint stage. To address this pain point, VoxelCloud’s Skin Knowledge Hub enables physicians to promptly analyze patients’ dermatological information and allows patients to gain preliminary insights into their conditions. Therefore, the significance of this application lies in enhancing the quality of online consultations and facilitating subsequent follow-up visits and monitoring.

In addition, such apps/mini-programs also serve the implicit functions of patient education and brand promotion. As patients use these apps/mini-programs, they naturally gain insights into their own conditions and the solutions suggested by the software, while companies benefit from increased brand awareness through patient engagement.

As evidenced by the aforementioned cases, although the core business of medical imaging AI enterprises remains centered on auxiliary diagnostic tools, the expansion of their imaging services is not confined to a fixed trajectory; every niche medical scenario presents an opportunity for the commercialization of imaging AI.

Overall, we can draw the following inferences.

1. Imaging AI products remain the core offerings of startups; while introducing new innovations, they continue to update their flagship products.

2. Regulatory approval remains the core issue hindering the commercialization of AI imaging companies, representing an uncontrollable risk factor for these enterprises.

3. Due to the non-public nature of medical data, the barriers established by companies conducting clinical trials are built up over time, making them difficult for most emerging enterprises to surpass, which has led to a rapid decline in the number of angel financing rounds. In the construction of these barriers, cloud technology has played a key role.

4. Through collaboration, AI enterprises have the potential to foster cooperation among various hospital departments and drive internal systemic reforms within hospitals.

5. Research collaboration serves as a unique avenue for AI companies to further strengthen their ties with hospitals on the basis of existing partnerships, thereby generating software revenue and building deeper technological moats.

6. AI products for ophthalmology are more likely to go directly to consumers than those for radiology, as consumers are more likely to have their eyes examined at primary care or non-medical institutions, which are closer to them.

7. Under traditional collaboration models, large medical device manufacturers do not provide direct revenue to AI companies, but they can offer a platform for AI enterprises to demonstrate their capabilities.

8. In contrast to traditional collaborations, under the new model of cooperation, AI companies play a leading role in medical device design.

9. In the process of developing AI and implementing it in hospitals, artificial intelligence companies can derive various imaging-related products, with data, algorithms, platforms, and users all having the potential to generate independent revenue in the future, or even become the primary commercialization models.

Now, perhaps we should re-examine the value of AI companies. The era of land-grabbing is over; how to quickly monetize existing value will become a hurdle that artificial intelligence enterprises need to overcome.