Import Substitution of High-Value Medical Consumables Is Imperative: Stents, Valves, and Dental Segments Lead the Way | Medical Innovation Series

Lepu Medical

Developer and Manufacturer of Cardiac Interventional Medical Devices and Pharmaceuticals

AMT Medical Inc.

3D-Printed Vascular Stent Technology Developer

MicroPort

High-end Medical Device R&D and Manufacturer

BIOMAGIC

Developer of Implantable Medical Devices

Allgens Medical

High-end regenerative medical materials and implantable medical device R&D provider

Venus Medtech

Artificial Heart Valve System Device Developer

Double Medical

Developer and Manufacturer of High-Value Medical Consumables

WEGO

Medical Device and Pharmaceutical R&D Manufacturer

China’s medical technical capabilities and healthcare quality have continued to improve, yielding a cohort of advanced medical technologies that meet or lead international standards and serve as global benchmarks, thereby enhancing the diagnosis and treatment capacity for major diseases. According to the Healthcare Access and Quality (HAQ) Index published in The Lancet, which ranks 195 countries and territories worldwide, China rose from 110th place in 1995 to 60th in 2015, and further to 48th in 2016, making it one of the countries with the most significant improvements globally.

Nevertheless, due to its relatively late development, China’s medical technology still relies heavily on foreign technologies in many areas, which is inconsistent with its status as a major global power. In response, China has proposed import substitution in the healthcare sector, aiming to rapidly narrow the gap with international advanced standards in the coming years. VCBeat (WeChat ID: vcbeat) has also analyzed the status of import substitution across multiple sub-sectors, starting with the current landscape in the high-value consumables segment.

According to projections by the Population Division of the United Nations Department of Economic and Social Affairs, China’s population under the age of 50 is expected to further decline by 2040, while the populations aged 60 and above, as well as those aged 80 and above, will rise significantly. The number of people in the oldest-old group (aged 80 and above) is projected to increase from 12 million in 2000 to over 40 million by 2030. Meanwhile, the elderly population aged 65 and above is expected to surge from the current 115 million to approximately 240 million by 2030.

The deepening aging of the population, continuous improvement in national living standards, and expanded coverage and depth of medical insurance have driven up the demand for interventional procedures, leading to a sustained increase in the demand for high-value medical consumables in China. On the policy front, incentives for medical device innovation and technological upgrades have established green channels for domestically produced innovative medical devices, promoting import substitution and breaking the monopoly held by foreign products. The combined forces of demand-side growth and policy support are driving the rapid development of the domestic high-value medical consumables market.

The Characteristics of High-Value Consumables Determine Their High Industry Barriers

High-value medical consumables possess certain unique characteristics, giving rise to phenomena specific to the industry. First, there is a high barrier to entry in this sector. This is because implantable high-value medical consumables must conform to human tissue structures and remain within the body for extended periods. Consequently, the state imposes strict oversight across all stages—including research and development, production, and distribution—and enforces rigorous licensing requirements for medical device manufacturers along with mandatory product registration systems.

From a technical perspective, the high-value medical consumables industry is a knowledge-intensive, capital-intensive, and multidisciplinary high-tech sector. Its products integrate multiple disciplines and technologies, including medicine, materials science, and biomechanics. The accumulation of proprietary technologies and the development of R&D capabilities in this field require a long-term process, with stringent requirements for production environments, manufacturing processes, and equipment. Without extensive long-term accumulation, new entrants are virtually unable to disrupt the existing competitive landscape.

The same logic applies to talent competition. As previously mentioned, the high-value medical consumables industry is interdisciplinary and heavily reliant on research and development (R&D) and innovation. Consequently, both R&D and production in this sector require a substantial number of highly skilled, multidisciplinary professionals. The development of mature high-value medical consumable products often necessitates collaborative efforts among high-level technical experts from diverse fields—including medicine, materials science, electronics, biomechanics, and mechanical manufacturing—for over five years. Since the high-value medical consumables industry started relatively late in China, experienced and outstanding R&D personnel and management talents are extremely scarce domestically.

Beyond the technological disparities between companies, marketing and brand building for high-value medical consumables also pose challenges for domestic enterprises. The characteristics of high-value medical consumables make the distributor agency model more suitable for this industry. Due to the nature of the high-value medical consumables sector, distributors tend to be relatively stable and generally do not switch代理 brands to avoid losing some hospital and physician clients. Large enterprises, having cultivated the market for many years, have already established stable distributor networks and possess significant brand influence. For latecomers aiming to penetrate this stable and mature network, substantial resource investment is required. Additionally, a highly skilled marketing team with extensive professional knowledge and expertise presents another barrier for new entrants. From the perspective of customer choice, the high-value consumables industry is heavily influenced by first-mover advantage.

Unlike conventional pharmaceuticals, high-value medical consumables exhibit strong irreplaceability. Taking orthopedic implantable consumables as an example, a single orthopedic surgery requires numerous small and intricate components, all of which necessitate the use of proprietary surgical tools provided by the manufacturer. Therefore, to mitigate potential risks, surgeons tend to use products and tools from the same brand in a coordinated manner during procedures. Meanwhile, physicians must undergo specific training to adapt to a particular brand’s products. Over time, major brands have established robust clinical tracking and training mechanisms. Through long-term educational promotion and clinical application, physicians have developed a certain level of acceptance for specific brands. In the absence of concrete evidence demonstrating significant advantages of new products, no one is willing to incur substantial risks by switching to and re-adapting to other brands.

China’s high-value medical consumables industry has a relatively short development history, spanning just over two decades. With the exception of a few leading enterprises, most domestic manufacturers of high-value consumables are small in scale, with limited market dominance and competitiveness. According to statistics, there are currently approximately 130 manufacturers of orthopedic implant consumables in China, with fewer than ten generating annual revenues exceeding RMB 100 million. As late as 2015, the combined market share of the top five companies in China’s orthopedic implant consumables sector was only 45.39%, indicating a low level of industry concentration. Meanwhile, international corporations, well-versed in the development patterns of the high-value consumables industry, have been expanding their market presence through mergers and acquisitions. For instance, Johnson & Johnson officially acquired Synthes in 2012, forming DePuy Synthes. During the same period, Medtronic acquired Kanghui Medical, a star enterprise in China’s high-value consumables sector, in 2012; and Stryker acquired Creation Medical in 2013. The trend toward industry consolidation is evident.

It is precisely because there are numerous small-scale manufacturers of high-value medical consumables that China’s high-value medical consumable industry lacked competitiveness in its early stages. Until 2016, foreign brands held a significant advantage in the domestic market, with well-known international companies leveraging their technological performance and quality standards to maintain a clear competitive edge in the high-end segment.

Import Substitution of High-Value Consumables Is Imperative

High-value consumables, primarily in orthopedics and cardiac intervention, offer substantial growth potential. According to an industry research report by Zhiyin Capital, the market size for high-value cardiovascular and orthopedic consumables in China was RMB 13.8 billion in 2013. By 2018, the market size for high-value cardiovascular consumables had rapidly climbed to RMB 38 billion, representing a nearly threefold increase compared to 2013. Meanwhile, statistics indicate that there are currently 290 million patients with cardiovascular disease in China. As the population ages, both the prevalence and mortality rates of cardiovascular disease are expected to continue rising. Furthermore, with the continuous improvement in the actual reimbursement rates of the New Rural Cooperative Medical Scheme (NRCMS) and the enhancement of primary healthcare capabilities, the demand for primary percutaneous coronary intervention (PCI) procedures will be unleashed. These factors will sustain rapid growth in China’s high-value cardiovascular consumables market, with the growth rate projected to remain at approximately 20%.

The market size of high-value orthopedic consumables reached RMB 11.8 billion in 2013 and grew to RMB 21.2 billion by 2018, representing an increase of nearly two-fold. Correspondingly, the prevalence of osteoporosis among individuals aged 50 and above in China is as high as 60%, which directly drives market demand for joint-related products. Forecasts indicate that the growth rate for high-value joint consumables will exceed 20%, outpacing the overall medical device industry average.

Like other industries in China, domestically produced high-value medical consumables have evolved from scratch, gradually narrowing the gap with international advanced standards amid fierce competition. Some leading enterprises have even achieved technological parity with global leaders. As domestic companies continue to enhance their technology, manufacturing processes, and R&D capabilities, China’s high-value medical consumables industry has been striving to achieve import substitution. In the future, import substitution will become the primary driver of rapid growth for domestic manufacturers of high-value medical consumables.

On the other hand, the high cost of imported high-value medical consumables has imposed significant financial pressure on both medical insurance payments and patients, making import substitution for these products imperative. In recent years, relevant national authorities have consistently provided policy support to promote the substitution of imported high-value consumables with domestic alternatives. The Outline of the 13th Five-Year Plan explicitly requires the establishment and improvement of the basic healthcare system, the comprehensive deepening of healthcare reform, the strengthening of the universal healthcare security system, and the enhancement of the medical service delivery system.

The “12th Five-Year” Special Plan for the Medical Device Science and Technology Industry, issued by the Ministry of Science and Technology, explicitly identified bone repair materials as high-end products prioritized for breakthroughs under the national 12th Five-Year Plan, aiming to promote technological breakthroughs and product innovation in domestically produced bone repair materials. The “Several Opinions on Promoting the Development of the Health Service Industry,” released by the State Council in 2013, clearly supported the research and development and industrialization of medical devices and novel biomedical materials; it called for strengthening policy support to increase the domestic market share and international competitiveness of medical equipment and materials with independent intellectual property rights. Furthermore, the “Guiding Opinions on Promoting the Healthy Development of the Pharmaceutical Industry,” issued by the General Office of the State Council in 2015, explicitly required accelerating the transformation and upgrading of the medical device industry, and developing high-end implantable and interventional products such as heart valves, cardiac pacemakers, fully biodegradable vascular stents, artificial joints and spinal implants, and cochlear implants.

In March 2015, the General Office of the State Council issued the Outline Plan for the National Healthcare Service System, and in May 2015, it released the Implementation Opinions on Comprehensively Promoting the Comprehensive Reform of County-Level Public Hospitals. These policies explicitly require a gradual increase in the allocation level of domestically produced medical equipment to reduce healthcare costs, mandating that medical institutions at all levels purchase domestically produced medical consumables under the premise of high quality and affordable prices. China’s medical insurance reimbursement system also has a significant impact on the development of medical devices.

Due to the wide variety of medical devices and their diverse raw materials, systematic classification and comparison are difficult. Consequently, China has not introduced a specialized reimbursement guidance catalog for high-value medical consumables, akin to the National Reimbursement Drug List or the National Essential Medicines List. As healthcare cost containment measures tighten, the pressure to control costs has become a Sword of Damocles hanging over hospitals. This environment makes it possible for high-quality, lower-priced domestic products to achieve import substitution. With the advancement of public hospital reforms, the implementation of tiered diagnosis and treatment, and the development of private hospitals, high-value medical consumables—particularly domestically produced orthopedic implants—are poised for rapid and robust growth.

Recent Changes in the Import Substitution of High-Value Medical Consumables in China

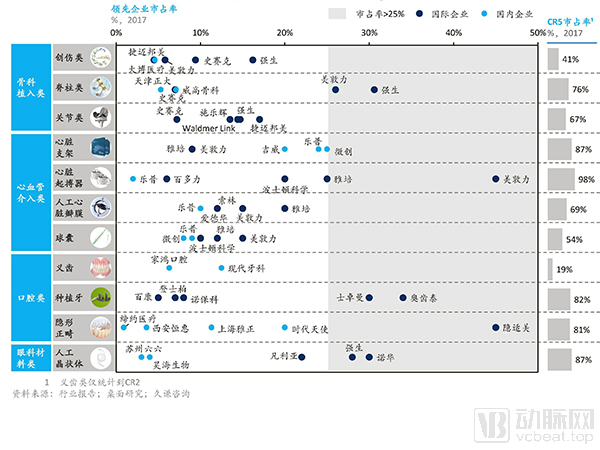

After years of development, numerous domestic companies have emerged as leaders in specific niches of the high-value consumables sector, including stents, artificial heart valves, orthopedic implants, and dentures.

The stent sector is currently one of the areas where import substitution for high-value medical consumables has been most successful. As early as 2011, Johnson & Johnson, a global leader in cardiovascular drug-eluting stents, announced its exit from the cardiac stent market, less than ten years after its Cypher stent became the first drug-eluting stent to receive FDA approval in 2003. In 2006, at the peak of its market share, Johnson & Johnson’s cardiac stent sales reached $2.6 billion, capturing over 60% of the global market, which was valued at $4 billion that year. However, by 2010, sales of Johnson & Johnson’s cardiac stents had dropped to just $627 million.

One of the key reasons for the sharp decline in Johnson & Johnson’s market share of cardiac stents is import substitution by domestically produced cardiac stents, which has gradually squeezed foreign manufacturers, represented by Johnson & Johnson, out of the market. In 2004, China’s cardiac stent market was essentially monopolized by foreign enterprises, led by Johnson & Johnson. However, by 2010, the respective market shares of foreign and domestic brands had shifted to 20% and 80%.

According to data released at the 21st National Interventional Cardiology Forum, the top three companies in China’s cardiac stent market by market share are Lepu Medical (24%), MicroPort (23%), and Jiwei Medical (20%, a wholly-owned subsidiary of Blue Sail Medical), all of which are domestic brands. The combined market share of these three domestic cardiac stent manufacturers has reached 67%, essentially achieving import substitution.

The heart valve market is another high-value consumables sector worth noting. Transcatheter Aortic Valve Replacement (TAVR), also known as Transcatheter Aortic Valve Implantation (TAVI), represents the latest technology for treating valvular heart diseases or defects. While it has become a standard procedure internationally, China, despite its later start, is making significant strides driven by national policies, entrepreneurs, and capital investment. Globally, two international giants, Edwards and Medtronic, dominate the TAVR market with shares of 65% and 30%, respectively. However, the domestically developed VenusA-Valve, co-developed by Venus Medtech, received marketing approval in 2017. By mid-2018, Venus Medtech had performed over 2,000 transfemoral TAVI implantations, ten times the volume of its competitors, presenting an optimistic outlook for import substitution.

In addition to cardiac stents, Chinese companies have also performed well in the emerging field of sinus stents. Pu Yi Biotech and US-based Intersect ENT have formed a duopoly on the global stage. Their products are currently the only two certified sinus stents worldwide.

The import substitution process for high-value orthopedic consumables has been relatively sluggish, primarily due to the loss of domestic industry leaders. Since 2012, Chuangsheng Medical and Kanghui Medical, which were previously ranked first and second in China’s high-value orthopedic consumables sector, have been acquired by international brands respectively. Leveraging their financial and brand advantages, these international companies have reduced production costs by acquiring domestic firms or outsourcing original equipment manufacturing (OEM) to Chinese enterprises, thereby further squeezing the market space for traditional domestic manufacturers. Nevertheless, some leading domestic manufacturers have gradually emerged. Companies such as Double Medical, Weigao Orthopaedics, Tianjin Zhengtian, and Shenzhen Keyi Tai are striving to achieve import substitution across various aspects. According to statistics, in 2018, the localization rates for products in the three major orthopedic sub-segments—trauma, spine, and joint—were 67.85%, 39.11%, and 26.73%, respectively.

Image source: Relevant reports from Jiuqian Consulting

These domestic enterprises and products are the main force in import substitution.

On February 27, 2019, Lepu Medical’s independently developed flagship product, the “Bioabsorbable Sirolimus-Eluting Coronary Stent System” (NeoVas), officially received certification from the China Food and Drug Administration (CFDA). Subsequently, on March 30, 2019, the NeoVas bioabsorbable stent made its official debut at the 17th Chinese Interventional Cardiology Conference, which represents the highest level of cardiac disease treatment. As the first bioabsorbable stent approved for market launch in China, this milestone signifies that China’s R&D and manufacturing capabilities in this field have reached a leading position.

Reviewing the evolution of interventional therapy, from the first balloon angioplasty in 1977 to the present, we have progressed through the eras of balloon angioplasty, bare-metal stents, and drug-eluting metal stents. The market launch of Lepu Medical’s NeoVas bioresorbable scaffold marks the dawn of the bioresorbable scaffold era. As the first bioresorbable scaffold approved for marketing in China, NeoVas is fundamentally different from the previous generation of drug-eluting metal stents, and its groundbreaking “bioresorbable” concept has gained widespread recognition among healthcare professionals.

Unlike traditional metallic stents, both the scaffold and drug-eluting coating of the NeoVas stent are made of polylactic acid. It fulfills its mission of supporting stenotic vessels within 6–9 months after implantation. Subsequently, the stent is absorbed by the human body in approximately three years, allowing the restoration of vascular elastic contraction and dilation functions and achieving vascular reconstruction. In contrast, traditional metallic stents remain in the body long-term, which can impede vascular elastic contraction and dilation, cause inflammatory responses due to intimal injury, and lead to platelet aggregation, thereby posing long-term risks such as plaque recurrence and thrombosis. Currently, NeoVas stent implantation procedures have been carried out in most provinces and cities across China, with its excellent clinical outcomes receiving widespread acclaim from both patients and healthcare institutions.

In addition to Lepu Medical, numerous domestic enterprises are also making concerted efforts to develop bioresorbable stents. For instance, the Xinsorb stent from Shandong Huaan Biotechnology Co., Ltd. is currently undergoing product registration. Meanwhile, similar bioresorbable drug-eluting stent systems, including MicroPort’s Firesorb, Jiwei Medical’s Excrossal (Xinyue), Shanghai Bioheart’s Galaxy, BIOMAGIC’s BioMagic, Beijing AMT’s AMSorb, and Shenzhen Salubris’ Alpha, are in clinical trials. Currently, more than 50 companies worldwide are engaged in research on bioresorbable vascular scaffolds, with Chinese firms accounting for over one-third of this total. This indicates that China’s vascular stent industry has achieved a leading global competitive position and is poised to be among the first high-end medical device sectors to realize import substitution.

The Firehawk drug-targeted eluting stent, which received CFDA approval in 2014 and CE certification in 2015, is a flagship product of MicroPort and the world’s first drug-targeted eluting stent. This product, brought to market after eight years of independent innovation and R&D, set several records in China and even worldwide at the time. First, it was the world’s first stent featuring single-side groove technology. Second, it achieved the “zero redundancy” standard, representing the lowest effective drug loading capacity among stents available at launch. Third, the TARGET series of studies conducted on this product constituted the first pre-market study in China strictly adhering to the “Guidelines for Clinical Trials of Coronary Drug-Eluting Stents” issued by the China Food and Drug Administration (CFDA). Fourth, it was the first domestically produced stent in China to demonstrate equivalence through head-to-head comparison with the Abbott XIENCE V stent, which was globally recognized as the top-tier device at the time. Fifth, it was the first domestically produced coronary stent with the potential to shorten the duration of dual antiplatelet therapy following interventional procedures.

In the field of cardiac stents, drug loading has been a challenging issue for professionals for over a decade. Prior to Firehawk, traditional mainstream cardiac stents relied on coating the metal stent surface with cell inhibitors to maintain vessel patency and reduce the incidence of restenosis. However, during vascular implantation, the coating on drug-eluting stents is prone to detachment or damage when encountering complex lesions such as calcification, which can compromise therapeutic efficacy and potentially exacerbate new thrombus formation. Furthermore, controlling the drug payload is difficult: insufficient loading may lead to premature depletion before reaching the lesion site, while excessive loading can cause adverse effects and impose a burden on the human body.

MicroPort’s Firehawk stent achieved the most technically challenging design—micro-groove drug encapsulation. This involves using lasers to engrave grooves on the surface of the metal stent and then loading the drug into these grooves. The grooves prevent the coating from detaching during delivery, ensuring no drug loss. Once the stent reaches the vascular lesion, the drug is precisely released from the fixed grooves, significantly enhancing efficacy while avoiding waste. This innovation has resolved a series of international challenges in the field of cardiac stents, including slow vascular repair and the need for patients to undergo prolonged dual antiplatelet therapy. The MicroPort Firehawk stent is also the first Chinese medical device to be published in The Lancet, a prestigious international medical journal, in over 200 years. This historic milestone was selected as one of the “Top Ten Scientific and Technological Events in China in 2018.” In 2014, MicroPort acquired the drug-eluting stent-related assets of Cordis, a subsidiary of Johnson & Johnson in the United States, marking a remarkable turnaround against international medical device giants. This acquisition enabled the Firehawk stent to enter overseas markets, including Asia, Europe, and South America, more rapidly.

In addition, MicroPort’s branched endovascular stent graft and delivery system, as well as its abdominal aortic stent graft and delivery system, have also been marketed through the CFDA’s Special Review Procedure for Innovative Medical Devices.

In the field of sinus stents, Pu Yi (Shanghai) Biotechnology Co., Ltd. and Intersect ENT from the United States have formed a duopoly on a global scale. In 2016, Pu Yi Biotech’s first product, the “Fully Bioresorbable Sinus Drug-Eluting Stent System” (brand name: Xiangtong), entered the green channel for special approval of innovative medical devices in China. In April 2017, the product obtained its registration certificate, becoming the first fully bioresorbable sinus stent approved in China. The application of fully bioresorbable drug-eluting stent technology in rhinology is actually quite broad, including but not limited to chronic rhinosinusitis; it can be used postoperatively for anti-inflammatory and anti-adhesion purposes in patients with allergic rhinitis accompanied by nasal polyps, patients with choanal atresia, patients with nasopharyngeal carcinoma, and those undergoing septal surgery.

Drug-eluting stents can minimize the side effects of hormones while ensuring therapeutic efficacy, making them particularly significant for younger patients. Pu Yi Biotech’s Xiangtong fully bioresorbable sinus drug-eluting stent offers three major advantages: First, precision. The stent is placed exactly where needed, akin to the concept of targeted therapy. While providing structural support, it delivers drugs directly and precisely to the lesion site. Second, sustained release. The bioresorption period of the fully bioresorbable sinus drug-eluting stent is approximately one month, meaning that during this time, the stent continuously and quantitatively releases medication at the lesion site 24 hours a day. This functions as a controlled-release drug delivery system. Over the 30-day degradation period, the total drug dosage delivered by a single stent is 652 micrograms. Specifically, during the first 3 to 4 days after implantation, approximately 50 micrograms are released daily. As the patient recovers, the daily drug release rate stabilizes at around 20 micrograms. Third, safety. Due to its precision and sustained release capability, the fully bioresorbable sinus drug-eluting stent significantly reduces hormone dosage while ensuring therapeutic effectiveness, thereby minimizing hormonal side effects.

Currently, only two sinus stents have received global regulatory approval: the Xiangtong Stent by Pu Yi Biotechnology and a product from Intersect ENT in the United States. In terms of degradation time, drug-loading capacity, and stent weaving technology, Pu Yi Biotechnology’s bioresorbable drug-eluting sinus stent outperforms Intersect ENT’s product, offering longer degradation time, higher drug-loading capacity, and more stable physical structure for better support. On June 29, 2019, Pu Yi Biotechnology completed its Series B financing, raising tens of millions of RMB.

In 2014, Venus Medtech’s VenusA-Valve transcatheter heart valve system was included in the first batch of the “Special Approval Procedure for Innovative Medical Devices” (Green Channel), received support from the National Science and Technology Support Program of the 12th Five-Year Plan under the Ministry of Science and Technology, and implemented key projects of the National Science and Technology Support Program during the 13th Five-Year Plan period.

In 2017, Venus Medtech’s Venus-A transcatheter heart valve system received approval from the China Food and Drug Administration (CFDA), becoming the first interventional artificial heart valve product approved for market launch by the CFDA and ushering in a new era of transcatheter valve replacement in China. In China, with the advent of an aging society, the incidence of degenerative valvular disease among the elderly is continuously increasing, with aortic stenosis gradually becoming the most common valvular heart disease in this population. Due to advanced age, poor physical condition, severe illness, or multiple comorbidities, these elderly patients are unable to undergo open-heart surgery. The emergence of transcatheter aortic valve replacement (TAVR), a minimally invasive surgical technique, has brought hope to these elderly patients. According to current indications, there are at least 500,000 patients in China who meet the criteria for TAVR, the vast majority of whom have not been hospitalized for treatment.

In addition to aortic valve disease, mitral and tricuspid valve disorders are also common cardiac valvular diseases. It is estimated that there are over 10 million patients in China with severe Mitral Regurgitation (MR) and Tricuspid Regurgitation (TR), yet less than 2% receive surgical treatment, indicating a particularly broad market prospect for therapeutic interventions in this field. Due to variations in femoral artery diameter among different patients, market requirements for Transcatheter Aortic Valve Replacement (TAVR) products differ across various regions worldwide.

Compared with overseas companies, Venus Medtech’s VenusA-Valve was developed specifically to address the characteristics of Chinese patients, who tend to have severe calcification and a higher prevalence of bicuspid aortic valves. By significantly enhancing radial force and the positioning system, supplemented by a skirt design, the device is better suited for the Chinese population and demonstrates clear differentiated advantages over imported products. Compared with domestic competitors, Venus Medtech has focused on improving radial force and retrievability, while adding a pre-loaded feature. In addition to retaining the traditional advantages of Venus Medtech, VitaFlow (MicroPort) features a smaller outer catheter diameter, thereby reducing vascular complications. Peijia Medical’s product, building on traditional strengths, has primarily enhanced catheter deliverability.

Identifying regenerative repair materials for bone defects to enhance the biosafety and clinical efficacy of bone grafts is a key research focus for scientists. Currently, commonly used bone graft materials in clinical practice for treating bone defects include autologous bone, allogeneic and xenogeneic bone, bioceramics, and polymer-based synthetic artificial bones. Autologous bone transplantation is limited by donor site availability and the risk of various complications at the harvest site; however, due to its osteoinductive properties and osteogenic potential, it has long been regarded as the “gold standard” for treating bone defects. Allogeneic bone grafts have not yet fully overcome post-transplant immune rejection, carry potential risks of pathogen transmission, and face medical ethical challenges. Although synthetic bone grafts are readily available, their efficacy is relatively inferior, and most such materials are non-degradable.

Leveraging patented technologies from Tsinghua University and over a decade of independent research and development, Beijing Allgens Medical Technology Co., Ltd. has introduced a biomimetic mineralization technology for artificial bone with fully independent intellectual property rights. This technology mimics the natural formation process of human bone to prepare biomimetic bone repair materials that are similar to human bone in composition, structure, and function, thereby achieving bone repair and regeneration effects comparable to those of autologous bone. Based on mineralized collagen (MC), a biomimetic composite material that simulates the chemical composition and microstructure of natural bone matrix, the company has successfully developed nanocrystalline mineralized collagen-based bone repair materials. Through proprietary in vitro biomimetic mineralization technology, this composite biomimetic material replicates the mineralization process of natural bone tissue, possessing a chemical composition and microstructure consistent with those of the natural human bone matrix. This provides a favorable microenvironment for osteoblasts to exert physiological activity during osteogenesis, thereby facilitating guided bone tissue regeneration.

This technology represents the world’s first use of in vitro biomimetic mineralization to fabricate biomimetic synthetic materials that replicate the chemical composition and microstructure of natural bone tissue. It has been extensively reported and positively evaluated by top-tier international academic journals such as Science and Nature Materials, as well as by the American Chemical Society website. Currently, Re-9, a product based on this material, has successfully obtained three Class III medical device registration certificates from the China Food and Drug Administration (CFDA) and market access approval from the U.S. Food and Drug Administration (FDA), covering numerous fields including orthopedics, dentistry, plastic surgery, and neurosurgery. To date, the product has been successfully applied in nearly one million cases domestically and internationally for the repair of bone diseases, with grafting efficacy approaching that of autologous bone.

Furthermore, Double Medical’s LCLP08 Minimally Invasive Standard Metal Locking Plate System and WEGO Orthopedics’ GBZ1-7 Posterior Spinal Internal Fixation System were also included in the Catalog of Innovative Medical Device Products (2018) released by the Department of Social Development Science and Technology of the Ministry of Science and Technology, positioning them as potential emerging forces for the import substitution of orthopedic consumables in the future.

References

Zhiyin Capital: The “Anchor” of Medical Devices? — Large-Scale Medical Equipment vs. High-Value Consumables

CFDA Southern Institute of Pharmaceutical Economics, Guangzhou Biaodian Medical Information Co., Ltd.: Market Research Report on China's High-Value Medical Consumables Industry

Jiuqian Consulting: Knowledge Compilation of the High-Value Medical Consumables Industry