LongBio, China's IgE Antibody Leader, Rings Hong Kong Listing Bell with 50.22% First-Day Surge

LongBio

Next-Generation Large Molecule Antibody Developer

On June 5, 2026, LongBio Pharma (Suzhou) Co., Ltd. (Stock Code: 01779.HK) was listed on the Main Board of the Hong Kong Stock Exchange, officially ringing the opening bell. On its first day of listing, LongBio opened at HK$144.3 per share, a 50.22% increase from its IPO price of HK$96.06. As of press time, LongBio's market capitalization stood at HK$10.7 billion.

From its establishment in 2020 to completing its listing on the Hong Kong Stock Exchange, LongBio took less than six years to navigate the critical stages from founding to capital market debut for an innovative pharmaceutical company.

During the pre-listing public offering phase, this innovative pharmaceutical company, which had not yet generated commercial revenue, attracted significant market attention. According to the prospectus and publicly disclosed information, the public offering portion recorded an oversubscription rate of approximately 4,470 times, with subscription funds exceeding HK$460 billion and around 268,000 subscribers, making it one of the most closely watched IPOs in the Hong Kong stock market's innovative pharmaceutical sector in recent years.

Amid the enthusiasm in the capital markets, a more noteworthy question arises: Why can a biotech company that has no commercialized products and remains in the R&D stage garner such high market attention in a short period?

LP-003 Realizing Commercial Value, LP-005 Anchoring Long-Term Growth

Unlike many biotech companies that simultaneously advance more than ten R&D pipelines, LongBio's development strategy appears notably restrained. As disclosed in the prospectus, the company has only two core products in the clinical stage: the anti-IgE antibody LP-003 and the dual-function complement inhibitor LP-005.

Behind this focus lies a relatively clear development path: LP-003 is tasked with commercialization, while LP-005 explores growth opportunities for the next stage.

Among these, LP-003 is the product closest to commercialization. It targets the allergic disease market, which has well-established clinical understanding and clear payment demand.

From the perspective of R&D strategy, LP-003 is not a drug with a novel mechanism of action; rather, it seeks iterative advancement within the already validated anti-IgE therapeutic pathway.

Currently, the only anti-IgE antibody approved for marketing worldwide is omalizumab, co-developed by Novartis and Roche. As a pioneering product in this field, omalizumab achieved global sales exceeding $4.3 billion in 2024. However, challenges remain in clinical practice, including frequent dosing, delayed onset of action, and insufficient response in some patients.

LP-003 aims to address these limitations through molecular design. According to company-disclosed data, its binding affinity for IgE reaches 2.08 pM, which is 860 times higher than that of omalizumab (approximately 1790 pM), indicating superior efficiency in capturing free IgE. Meanwhile, the Fc region (Fragment crystallizable) has been engineered with YTE mutations, reportedly extending its half-life by approximately twofold. This supports dosing every 8 to 12 weeks, compared to every 2 to 4 weeks for omalizumab. The reduced dosing frequency directly translates into improved adherence among patients with chronic conditions.

To date, the most compelling evidence for LP-003 stems from its head-to-head Phase II clinical trial against omalizumab. Data presented at the 2026 Annual Meeting of the American Academy of Allergy, Asthma & Immunology (AAAAI) showed that in 202 patients with chronic spontaneous urticaria, the proportion of patients achieving complete remission (UAS7=0) by Week 12 was 66.7% in the LP-003 200 mg every-8-weeks dosing group, compared to 43.6% in the omalizumab group. The improvement in disease activity also reached statistical significance. Meanwhile, LP-003 demonstrated a trend toward rapid onset of action early in the treatment course.

These data indicate that LP-003 is not merely a "me-too" drug, but rather demonstrates clinically meaningful differentiation at a validated target. Currently, patient enrollment for the Phase III clinical trial of LP-003 for seasonal allergic rhinitis has been completed, and the company expects to submit a Biologics License Application (BLA) to the National Medical Products Administration (NMPA) by the third quarter of 2026 or earlier. If approved, this would be the first next-generation anti-IgE antibody to file for marketing approval in more than two decades since the launch of omalizumab.

If LP-003 is tasked with near-term commercialization, then LP-005 represents LongBio's strategic layout for the future.

LP-005 is a bispecific antibody fusion protein that simultaneously targets C5 and C3b of the complement system. The complement system is a crucial component of innate immunity; its aberrant activation can sustain inflammation and tissue damage, and is considered closely associated with diseases such as IgA nephropathy (IgAN) and paroxysmal nocturnal hemoglobinuria (PNH).

Most currently marketed complement drugs focus on a single target. For example, AstraZeneca's eculizumab primarily inhibits the C5 pathway but offers limited coverage of upstream C3b-mediated inflammatory responses. In contrast, LP-005 aims to simultaneously intervene at two key nodes in the complement cascade, thereby achieving more comprehensive pathological blockade.

However, this design concept still awaits further clinical validation. Whether dual-target inhibition can deliver additional efficacy benefits and whether it will increase safety risks such as infection will depend on the results of subsequent Phase II and Phase III clinical trials. Currently, LP-005 has entered Phase II clinical trials in China and is one of LongBio's investigational projects with the most significant long-term potential.

Underpinning these two products are the company's independently developed high-affinity antibody discovery platform and bispecific antibody development platform. The former leverages proprietary technology to significantly enhance antibody affinity compared to traditional methods, while the latter overcomes the limitations of conventional antibody formats, enabling flexible combination of modules such as nanobodies, antibody fragments, receptors, and engineered Fc regions. This provides a technological foundation for the continuous output of future pipeline candidates (e.g., LP-00A, LP-00C, LP-00D).

Allergy and Complement Therapy Sectors Expand, with Growth Potential and Competition Heating Up Simultaneously

Leveraging its differentiated pipeline layout with LP-003 and LP-005, LongBio has precisely entered two high-growth niche sectors, where domestic and international market sizes are steadily expanding, while the industry competitive landscape is showing significant divergence.

According to Frost & Sullivan data, the global market size for allergic disease drugs has grown from $42.8 billion in 2018 to $68.8 billion in 2024, and is projected to further increase to $111.4 billion by 2030; during the same period, the Chinese market grew from $3.8 billion to $8.1 billion, and is expected to reach $22.9 billion by 2030, with a growth rate higher than the global average.

The core driver behind the continuous expansion of the overall market is the iterative upgrading of clinical treatment regimens. Taking allergic rhinitis as an example, there are approximately 245 million patients in China. In the past, patients primarily relied on antihistamines and glucocorticoids to control symptoms. However, with the gradual integration of biologics such as anti-IgE agents into clinical practice, the treatment penetration rate among patients with moderate-to-severe conditions is increasing, thereby creating new incremental growth opportunities for the sector in which LP-003 competes.

However, the expansion of market space also means that competition is accelerating. Currently, three anti-IgE drugs have been approved for marketing in China (including one original drug and two biosimilars), with several other similar products in clinical development; meanwhile, drugs targeting different mechanisms such as anti-interleukin-4 receptor alpha (IL-4Rα), anti-interleukin-13 (IL-13), and anti-thymic stromal lymphopoietin (TSLP) are also being actively advanced. Companies including Keymed Biosciences, Sunshine Guojian Pharmaceutical, and Zelgen Biopharmaceuticals have already entered this field.

Complement-mediated diseases are forming another growth curve after allergies. According to data from a Fortune Business Insights report, the global complement inhibitor market was valued at approximately USD 9 billion in 2025 and is projected to grow to USD 32.4 billion by 2034, representing a compound annual growth rate (CAGR) of approximately 15.4%. In terms of regional structure, the Chinese market is considered one of the key sources of future incremental growth, with revenue expected to reach approximately USD 560 million in 2026, accounting for about 5.48% of the global market.

From the perspective of the competitive landscape, this field remains highly concentrated. Globally, the C5 target has long been dominated by the AstraZeneca portfolio (eculizumab and its long-acting formulations). In the Chinese market, eculizumab remains the primary commercially available product for complement therapy, with the overall market still in an early stage of development driven by single-target drugs.

This landscape also indicates that there remains structural room for expansion of the complement pathway across multiple indications and exploration of multi-target mechanisms, providing a foundational market environment for the subsequent development and extension of LP-005 in indications such as IgA nephropathy and PNH.

For LongBio, the allergy and complement therapy sectors offer a sufficiently broad market landscape. However, whether these market opportunities can be translated into commercial value ultimately depends on whether the differentiated advantages of its products can be validated in future clinical and commercial competition.

49.96% Anchor Investment: Fundraising Completion Marks Start of Commercialization Validation Phase

If LP-003 and LP-005 constitute the product value of LongBio, then "people" are the critical foundation supporting its R&D pathway.

The founding team of LongBio represents a rare combination within the 18A chapter of the Hong Kong Stock Exchange. Dr. Sun Naichao, aged 89, is one of the principal inventors of omalizumab, the world's first anti-IgE monoclonal antibody. With a 55-year R&D career, more than 30 academic publications, and 16 U.S. patents, he has navigated the entire value chain from target validation to market approval. Liu Heng, aged 43, holds a Ph.D. in Molecular and Cellular Biology from the State University of New York. He previously participated in the clinical trial applications for Ryzneuta (approved by the FDA in 2023 and by the NMPA in 2024), demonstrating extensive expertise in execution within China's regulatory environment.

With a 46-year age gap, the two form a highly effective complementary partnership: Sun Naichao knows where first-generation anti-IgE therapies can be optimized, while Liu Heng knows how to drive drugs across the finish line in China. According to the prospectus, Sun Naichao is primarily responsible for R&D strategy and scientific decision-making, whereas Liu Heng oversees corporate operations management and the advancement of clinical development.

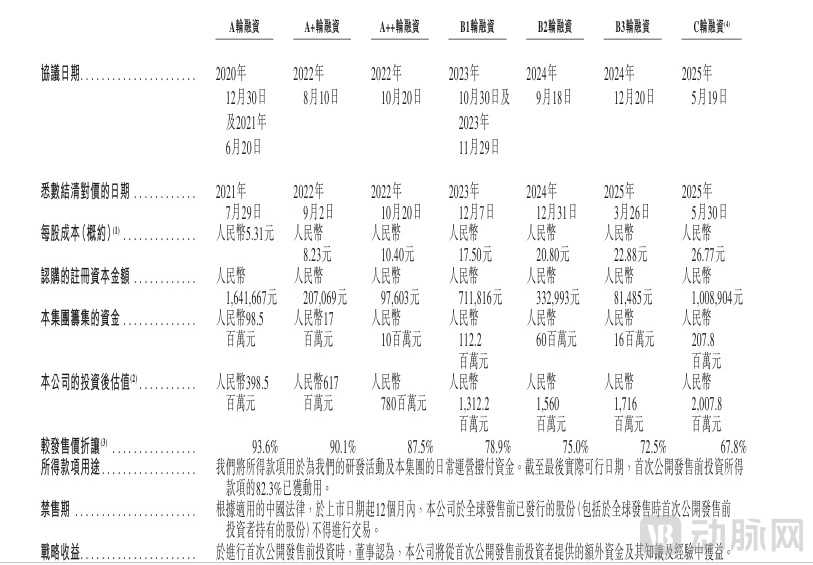

LongBio's pipeline and talent have underpinned the valuation trajectory across its seven rounds of financing. Investors including Oriental Fortune Capital, Highlight Capital, CSPC Pharmaceutical Group, and Qiming Venture Partners consistently participated in follow-on investments. Among the cornerstone investors for the IPO, ten institutions, including OrbiMed Funds, collectively subscribed to approximately USD 87 million, accounting for 49.96% of the shares offered, with a six-month lock-up period, signaling relatively optimistic market sentiment. The company's market capitalization at issuance was approximately HKD 7.127 billion, representing a 226.57% surge from its Series C valuation.

Key Terms of Pre-IPO Investments

However, the continuous infusion of capital does not mean that commercialization risks have disappeared.

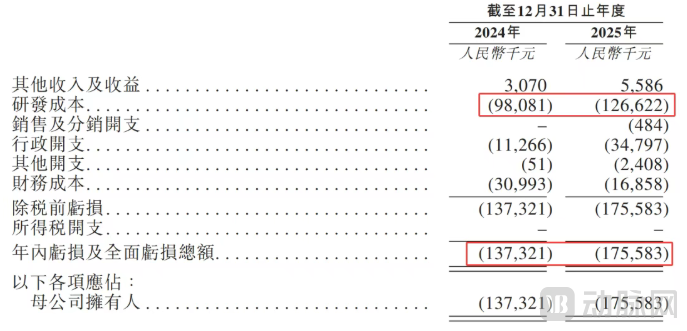

As a biotech company that has not yet commercialized any products, LongBio remains in the typical R&D investment phase. According to its prospectus, the company recorded zero drug sales revenue from 2024 to 2025, while R&D expenses increased from RMB 98.1 million to RMB 126.6 million. The net loss widened from RMB 137 million in 2024 to RMB 176 million in 2025, indicating an accelerating cash burn rate. As of the end of April 2026, the company's cash reserves stood at RMB 93.57 million. This Hong Kong IPO provides critical funding support for the submission of the Biologics License Application (BLA) for LP-003 and subsequent commercialization preparations.

Summary of Items in the Statement of Profit or Loss and Other Comprehensive Income

The net proceeds from this fundraising amounted to approximately HK$1.255 billion, with 75% allocated to the research and development and commercialization of LP-003 and LP-005. The company adopts an asset-light model, outsourcing production to contract development and manufacturing organizations (CDMOs) while retaining only target discovery and clinical trial design in-house. This approach reduces cash burn; however, it carries the risk of dependency on third parties during commercial scale-up.

LP-003 is expected to submit its BLA in the third quarter of 2026, with the first sales revenue potentially realized in 2027 if all goes smoothly. Until then, LongBio remains a typical example of a Chapter 18A-listed company: R&D-intensive, revenue-free, and heavily loss-making.

The next 18 months will be the most critical validation period for LongBio: Phase III data readout, BLA submission, regulatory review and approval, production preparation, and sales team establishment. The execution efficiency of each step will determine whether the pipeline's value can be translated into tangible commercial returns.

Sun Naichao's pioneering experience provides the R&D confidence for product iteration, while Liu Heng's localization capabilities ensure efficient project implementation. The listing bell-ringing ceremony marks a milestone, but the true test of commercialization has only just begun.