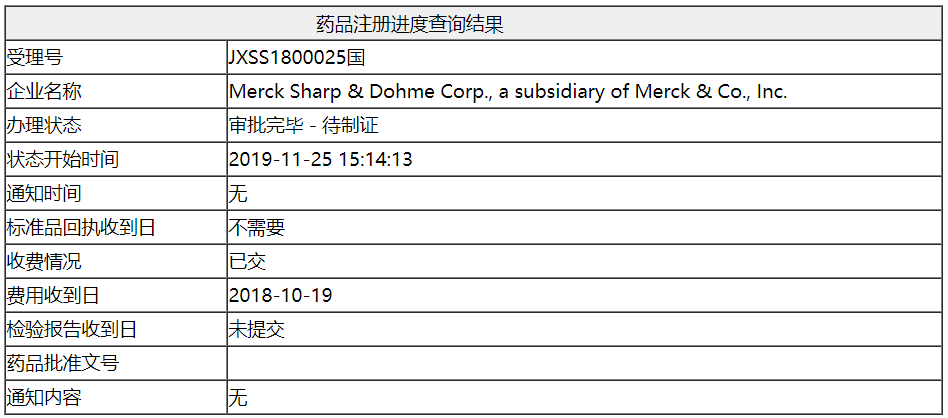

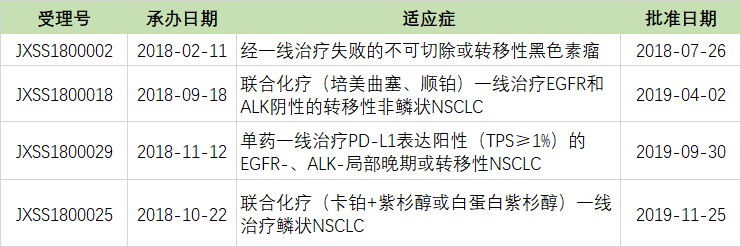

On November 26, the official website of the National Medical Products Administration (NMPA) announced the approval of another marketing application for Merck’s pembrolizumab (Keytruda) (acceptance number JXSS1800025). This approval covers the first-line treatment of metastatic squamous non-small cell lung cancer (squamous NSCLC) in combination with chemotherapy (carboplatin plus paclitaxel). This indication does not require consideration of patients’ PD-L1 expression status.

Pembrolizumab was approved in China in July 2018, March 2019, and September 2019 for the following indications: monotherapy for unresectable metastatic melanoma; combination with chemotherapy as first-line treatment for non-squamous non-small cell lung cancer (NSCLC); and monotherapy as first-line treatment for PD-L1-positive (TPS ≥1%) NSCLC. Thus, within just eight months, Keytruda accumulated three first-line NSCLC indications, becoming the PD-1 monoclonal antibody with the most approved indications in China and in the field of advanced lung cancer treatment.

Indications Approved for Keytruda in China

In the U.S. market, the three first-line indications for Keytruda in the treatment of non-small cell lung cancer (NSCLC) have contributed significantly to establishing Keytruda’s status as the “King of Immunotherapy.”

A review of the sales trajectory of Keytruda (K drug) from 2015 to the present reveals two inflection points of accelerated growth in Q4 2016 and Q2 2017. These were driven by the U.S. FDA’s accelerated approval of Keytruda as a monotherapy for first-line treatment of PD-L1 high-expressing (TPS ≥50%) non-small cell lung cancer (NSCLC), based on the KEYNOTE-024 study, and as combination therapy with chemotherapy for first-line treatment of non-squamous NSCLC, based on the KEYNOTE-021G study. These two conditionally accelerated approvals served as the key “milestones” that enabled Keytruda to ultimately surpass Opdivo (O drug) in Q2 2018. In October 2018, the FDA approved Keytruda in combination with chemotherapy for the first-line treatment of squamous NSCLC, based on the KEYNOTE-407 study.

Quarterly Sales Trends of Four PD-1/PD-L1 Monoclonal Antibodies from Q1 2015 to Q3 2019

In terms of sales revenue, Keytruda (K drug) achieved total sales of $7.973 billion in the first three quarters of 2019. It is projected that its sales this year (i.e., the fifth year since its market launch) will exceed $11 billion, with the first-line treatment market for advanced lung cancer contributing over 65% of Keytruda’s sales in the first three quarters.

It is undeniable that the clinical trials behind Keytruda’s “acquisition” of these three indications (KEYNOTE-189, KEYNOTE-407, and KEYNOTE-042) have played an indispensable role in achieving its current prominence. They are like pearls embedded in the crown of Keytruda’s “King of Immunotherapy,” bringing it brilliance and radiance.

Advantages and Challenges of Keytruda

Six PD-1 monoclonal antibodies have already been approved for marketing in China, and AstraZeneca’s and Roche’s PD-L1 monoclonal antibodies will soon enter the market. The competitive pressure facing Keytruda is no less than that in the US market.

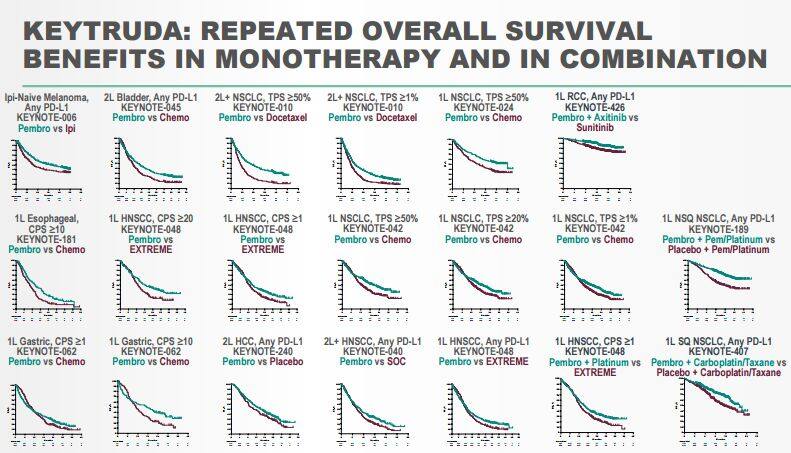

In response to how it would address domestically produced PD-1 inhibitors in the Chinese market, MSD’s global management stated that in the field of cancer immunotherapy, decisions must be guided by data. Keytruda has become the “King of Immunotherapy” precisely because of its compelling clinical data, particularly its advantage in overall survival (OS).

On June 20 this year, MSD held its Investor Day event for the first time in many years. During the event, MSD’s management showcased impressive overall survival (OS) data for Keytruda across a range of tumor types, conveying to the external audience a confident “who else but us” stance.

OS Data from Clinical Studies of Keytruda Monotherapy or Combination Therapy in Various Malignancies

On June 11, 2019, the U.S. FDA approved Keytruda as a monotherapy for first-line treatment of PD-L1-positive (CPS ≥ 1) recurrent or metastatic head and neck squamous cell carcinoma (HNSCC), and in combination with chemotherapy for first-line treatment of all patients with recurrent or metastatic HNSCC, regardless of PD-L1 expression. This brought the total number of first-line indications approved for Keytruda in the United States to eight (including conditionally accelerated approvals), ranking it first among all PD-1/PD-L1 immune checkpoint inhibitors.

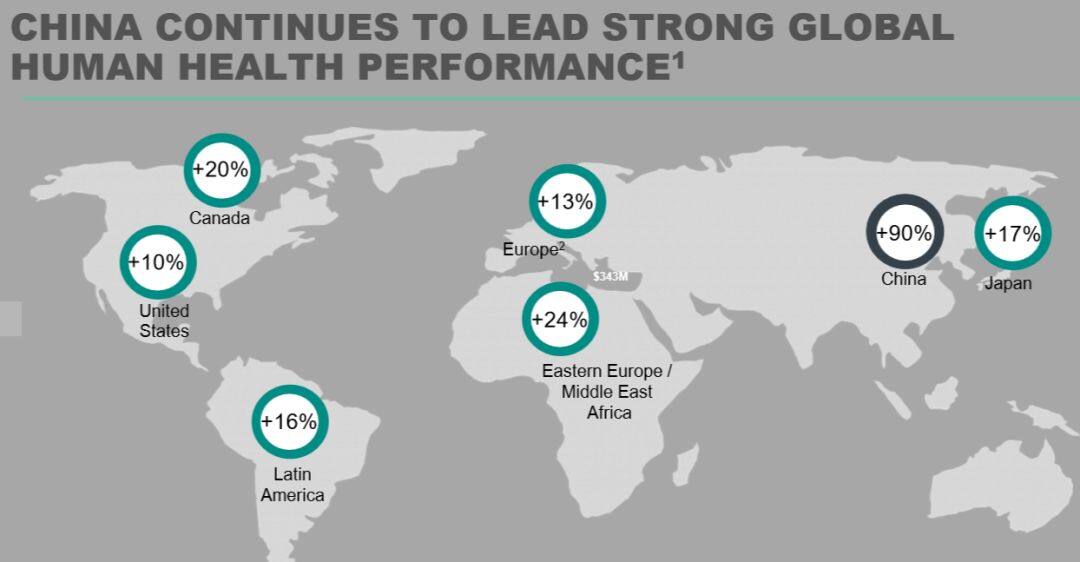

Keytruda’s market performance in China has also lived up to the expectations of MSD’s global management. Within one year of its commercial launch in September 2018, Keytruda achieved sales of RMB 2 billion, setting a historical record for prescription drugs in China. Meanwhile, driven by Keytruda’s strong performance in the Chinese market, MSD China recorded year-over-year growth rates of 67%, 41%, and 90% in the first, second, and third quarters of this year, respectively, making it MSD’s fastest-growing market globally in each of those quarters.

In Q3 2019, MSD China led all MSD markets with a 90% growth rate.

Multiple investment consulting firms predict that Keytruda will become the top-selling product in the global prescription drug market in 2025, replacing Humira as the global “blockbuster drug.” Undoubtedly, the Chinese market is crucial to Keytruda’s future growth.

But is merely erecting a “data wall” sufficient to drive the rise of Keytruda? Are the three pearls in Keytruda’s “crown” enough to illuminate its future in China and pave the way for a bright prospect?

Approximately 780,000 new cases of lung cancer are diagnosed annually in China, including nearly 660,000 cases (85%) of non-small cell lung cancer (NSCLC). Of these, approximately 400,000 patients (60%) have advanced or metastatic disease, with squamous NSCLC accounting for about 30%. Among patients with non-squamous NSCLC, approximately 60% (around 170,000 patients) lack driver gene mutations. As the only PD-1 monoclonal antibody approved in China for first-line treatment of advanced NSCLC, Keytruda (K drug) has substantial market potential and room for growth.

However, the lung cancer market in China differs from those in Europe and the United States. Internationally, Keytruda (K drug) only needs to directly compete with a few rivals by comparing clinical data. In China, however, Keytruda faces additional competition from several domestically produced PD-1 inhibitors. Although these domestic agents have not yet been approved for lung cancer indications—thereby currently affording Keytruda a more favorable market landscape—securing approval for lung cancer indications is a strategic imperative for all manufacturers. Consequently, future competition in China will be more intense than in international markets, particularly in terms of the number of competitors.

Furthermore, Keytruda must compete not only on clinical data with domestically produced PD-1 inhibitors but also on price. Although Keytruda enjoys a significant first-mover advantage in the Chinese lung cancer market, whether it can thrive, stand out, and sustain its remarkable success in such a competitive landscape remains to be seen.

Accelerating R&D, Rooted in China

Keytruda’s approval in the United States for 15 tumor types and 22 indications (excluding conditionally accelerated approvals) within just five years—covering melanoma, small cell lung cancer, non-small cell lung cancer, head and neck squamous cell carcinoma, gastric cancer, esophageal cancer, renal cell carcinoma, endometrial cancer, and other distinct tumor types, as well as all microsatellite instability-high/mismatch repair-deficient (MSI-H/dMMR) malignancies—would not have been possible without its substantial investment in research and development.

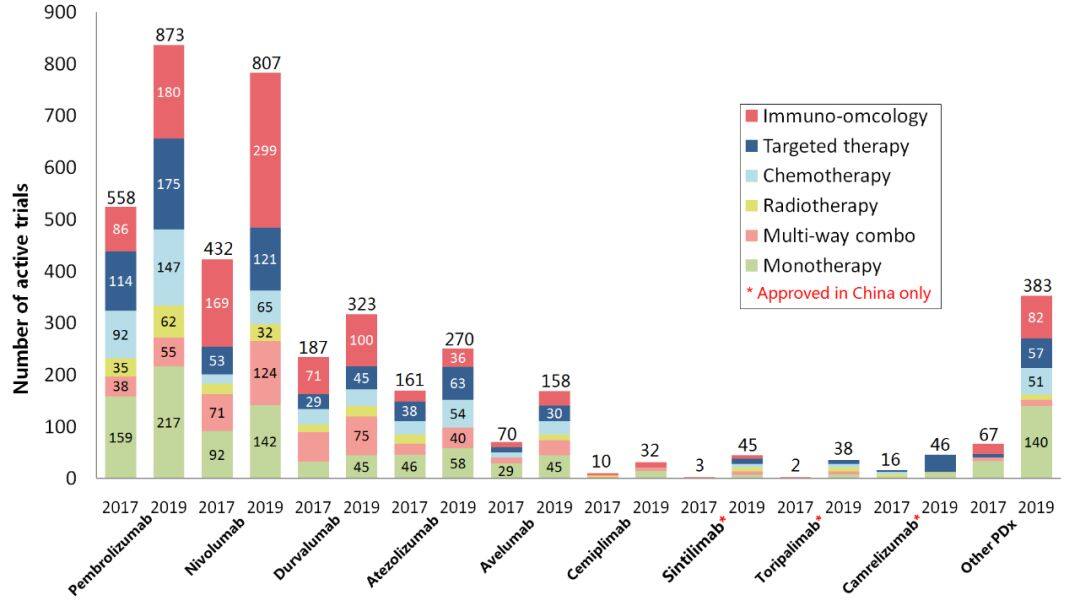

According to official data from MSD, there are currently more than 1,000 clinical studies related to Keytruda (K drug) being conducted globally. An article titled “Trends in clinical development for PD-1/PD-L1 inhibitors,” published in Nature Reviews Drug Discovery on November 4 this year, showed that the number of studies related to Keytruda reached 873, an increase of 315 from 2017, surpassing the 807 studies for Opdivo (O drug), making it the “king of clinical research” among today’s PD-1/PD-L1 immune checkpoint inhibitors.

Statistics on the Number of Clinical Studies Conducted with PD-1/PD-L1 Immune Checkpoint Inhibitors in 2017 and 2019

However, in China, for Keytruda to achieve success, it cannot rest on its currently approved four therapeutic indications; instead, it must rapidly “introduce” new indications into the Chinese market and secure regulatory approval. This, in turn, necessitates accelerating the advancement of its clinical research programs within China.

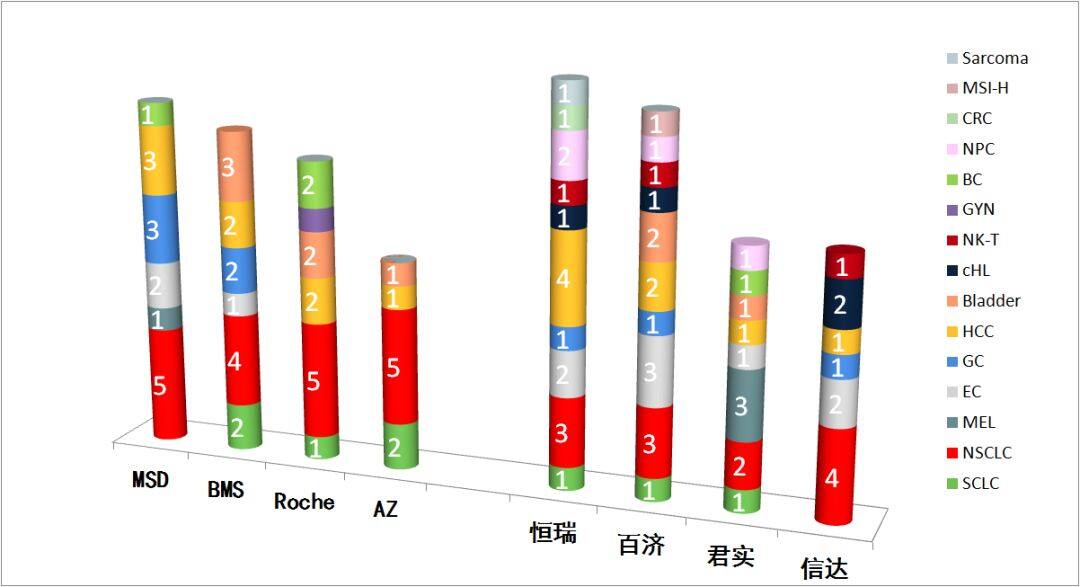

According to data retrieved from ClinicalTrials.gov, the number of Phase 3 registration clinical trials for Keytruda (K drug) in China reached 15, surpassing the 14 trials conducted by BMS, but still trailing behind Hengrui (17 trials) and BeiGene (16 trials).

Statistics on the Number of Clinical Studies Conducted with PD-1/PD-L1 Immune Checkpoint Inhibitors in Mainland China

Competition in the PD-1 market, both domestically and in Europe and the United States, hinges on the number of approved indications and the speed at which these indications are approved. To maintain its status as the “King of Immunotherapy” in China, Keytruda must deepen its roots in the Chinese market by intensifying and accelerating its domestic R&D efforts, particularly as other imported and China-made PD-1/PD-L1 monoclonal antibodies begin to “close in.”

Outstanding Efficacy in Chinese Patients

The KEYNOTE-042 study enrolled 262 Chinese patients; the KEYNOTE-407 study and its Chinese population expansion cohort enrolled 125 Chinese patients; and the KEYNOTE-181 study (evaluating pembrolizumab monotherapy for locally advanced or metastatic esophageal cancer with disease progression after first-line therapy) enrolled 123 Chinese patients.

A common finding across all these studies is that the efficacy data of Keytruda (K drug) in treating Chinese patients appear to be superior to those observed in the overall population. In contrast, there is currently no evidence-based medical data demonstrating such ethnic differences in efficacy for other PD-1/PD-L1 monoclonal antibodies (primarily imported agents).

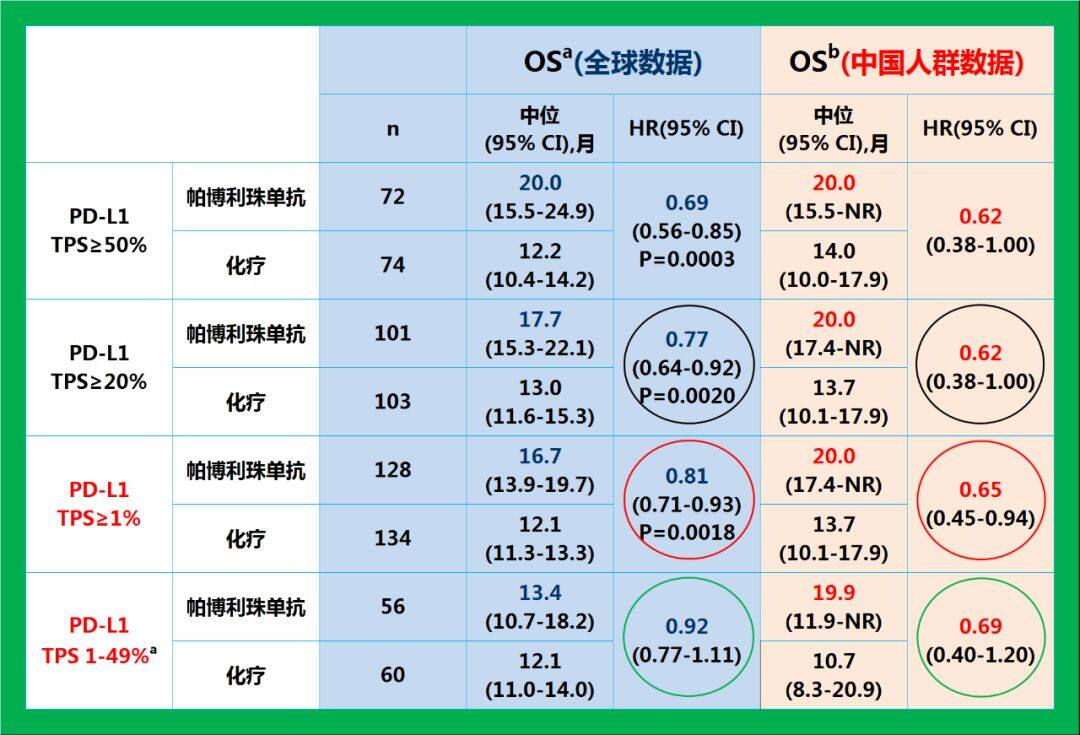

Results from the Chinese subgroup of the KEYNOTE-042 study and the extended study in the Chinese population demonstrated that the median overall survival (OS) with Keytruda treatment for non-small cell lung cancer (NSCLC) patients across different PD-L1 expression levels remained stable at 20 months, with the reduction in risk of death (hazard ratio [HR]) consistently ranging between 31% and 38%. In contrast, data from the global overall population showed a decline in both OS and risk reduction as PD-L1 expression decreased (see figure below).

Comparison of Data from the Chinese Subgroup in the KEYNOTE-042 Clinical Study and the Chinese Expanded Study with Global Overall Survival (OS) Data

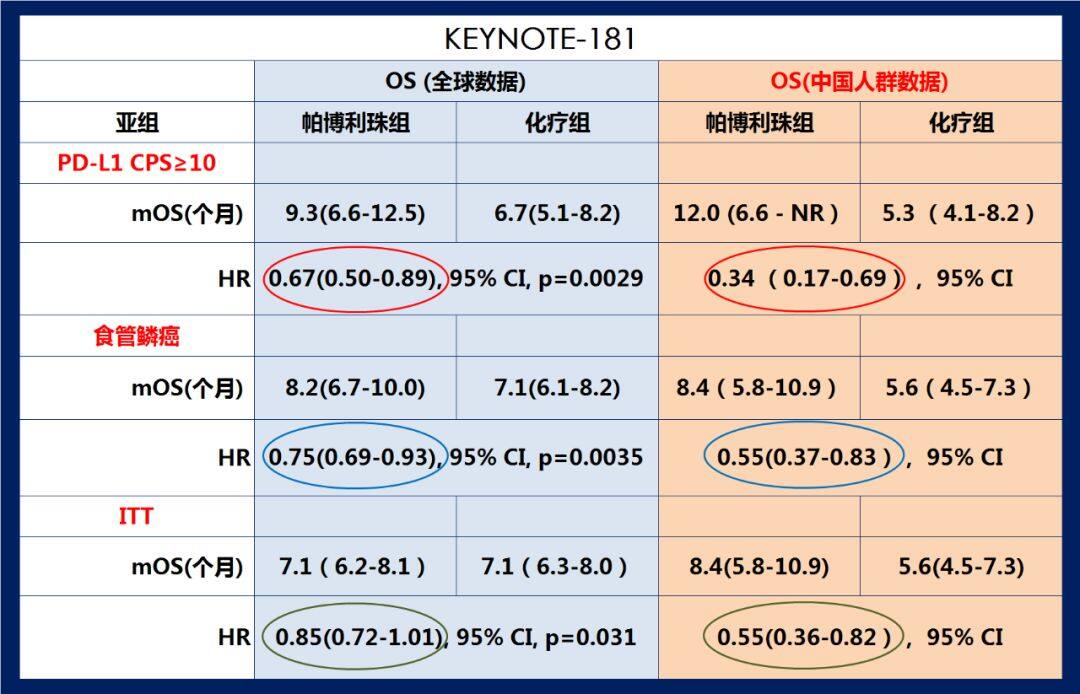

Similarly, a comparative analysis of data from the Chinese subgroup versus the global overall population in the KEYNOTE-181 study (see table below) demonstrated that Keytruda conferred a more pronounced overall survival (OS) benefit to Chinese patients with locally advanced or metastatic esophageal cancer than observed in the overall treated population, with a greater reduction in the risk of death (45% vs. 15%). In the PD-L1–positive subgroup, the median OS for Chinese patients reached one year, surpassing that of current first-line chemotherapy regimens, and the magnitude of risk reduction in mortality was twice that of the overall population (66% vs. 33%).

Comparison of OS Data Between the Chinese Subgroup and the Global Population in the KEYNOTE-181 Clinical Study

Is Keytruda a more suitable PD-1 monoclonal antibody for Chinese patients? This requires more clinical studies targeting Chinese patients, as well as clinical study results of Keytruda on tumors with Chinese characteristics (such as hepatocellular carcinoma, gastric cancer, etc.) to support this.

Will Keytruda’s “crown” be further adorned with an “Oriental Pearl”? Let us wait and see.