On January 30, Amgen announced its 2019 financial results, reporting total annual revenue of $23.362 billion, a 2% year-over-year decline, primarily driven by sharp decreases in sales of several core legacy products, including Neulasta (pegfilgrastim), Sensipar/Mimpara (cinacalcet), Epogen (epoetin alfa), and Neupogen (filgrastim).

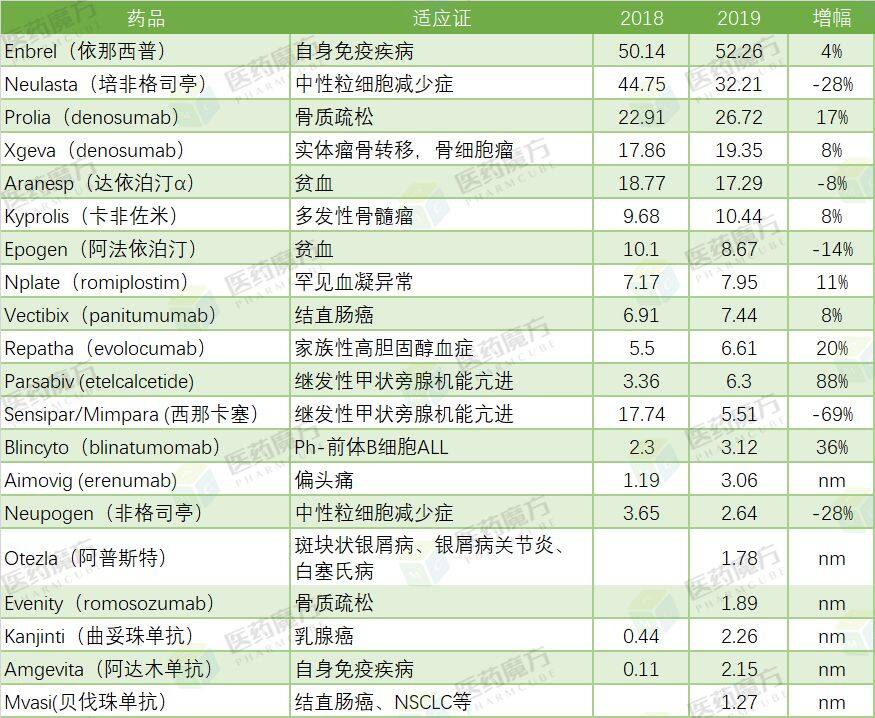

In 2018, the FDA approved the marketing of pegfilgrastim biosimilars from Mylan/Bicon and Coherus, respectively. These two drugs were sold at prices 33% lower than the original brand-name drug, causing significant damage to Neulasta. Meanwhile, Sensipar, used to treat secondary hyperparathyroidism, a common complication in patients with chronic kidney disease, fell off the patent cliff due to patent expiration and generic competition, with its sales shrinking directly from a peak of $1.774 billion in 2018 to $551 million.

Amgen's Major Drug Sales in 2019 (in $100 million)

However, Amgen is moving into a new era of growth driven by new products. The six innovative drugs approved in recent years—Kyprolis (multiple myeloma), Repatha (hyperlipidemia), Parsabiv (secondary hyperparathyroidism), Blincyto (acute lymphoblastic leukemia), Aimovig (migraine), and Evenity (osteoporosis)—have gradually grown to contribute over $3 billion in revenue to Amgen.

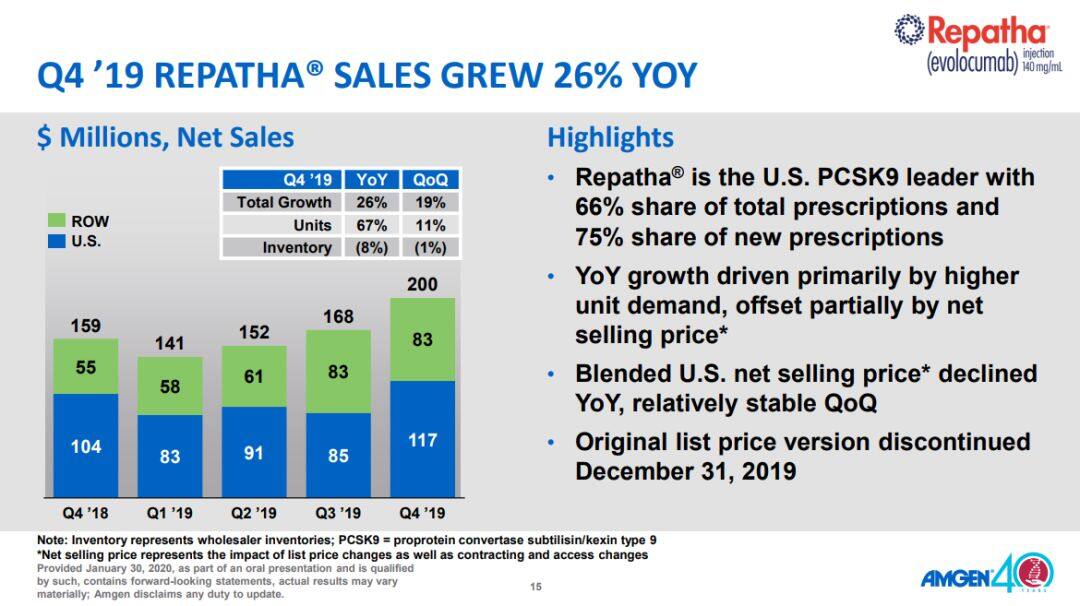

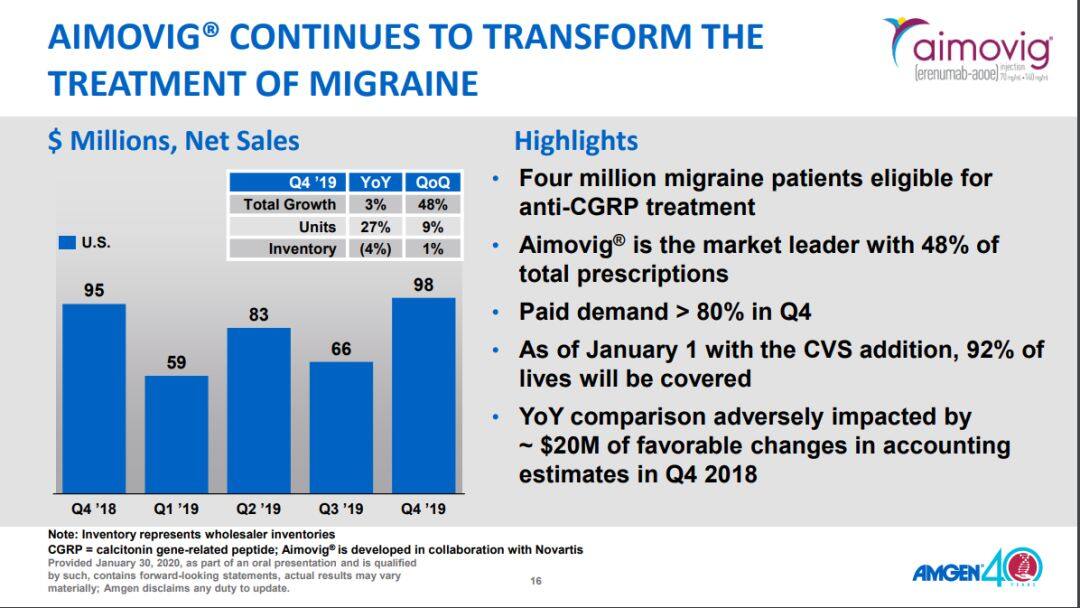

Amgen has achieved market-leading positions, particularly with Repatha, a PCSK9 monoclonal antibody for the treatment of hyperlipidemia, and Aimovig, a CGRP monoclonal antibody for the treatment of migraine.

Amgen’s other thriving business segment is biosimilars. It can be said that Amgen is both a victim and a beneficiary of biosimilars. Currently, three biosimilar products have been approved and launched on the market, generating a combined sales revenue of $568 million in 2019. On December 13, 2019, Avsola (infliximab) also received FDA approval, further expanding Amgen’s biosimilar portfolio.

Amgen also executed two major M&A transactions in 2019, including the $13.4 billion all-cash acquisition of Celgene’s psoriasis drug Otezla (apremilast) on August 27, 2019, which cleared the way for the merger between Bristol Myers Squibb (BMS) and Celgene. The deal was completed on November 21, 2019, generating $178 million in revenue for Amgen within just five weeks. Amgen’s revenue forecast for 2020 is $25–25.6 billion, representing an approximate $2 billion increase over 2019, with a significant portion attributable to contributions from Otezla.

On November 1, 2019, Amgen and BeiGene entered into a strategic collaboration, granting BeiGene the rights to develop and commercialize in China three established medicines—Xgeva (denosumab), Kyprolis (carfilzomib), and the bispecific antibody Blincyto (blinatumomab)—along with more than 20 other investigational oncology drugs. Simultaneously, Amgen acquired a 20.5% stake in BeiGene for $2.7 billion. This transaction also marked that Amgen’s expansion into the Chinese market primarily relies on partnerships rather than direct operational involvement.

Looking back at 2019, the most impactful event for Amgen and the industry was the release of clinical data for the KRAS G12C inhibitor AMG 510. This rekindled intense industry interest in this previously “undruggable” target, prompting major pharmaceutical companies to reassess their internal KRAS programs or actively seek external collaborations on related projects. In 2020, additional data on AMG 510 monotherapy across various solid tumors are expected to be presented, along with preliminary results from the combination of AMG 510 and Keytruda for the treatment of advanced non-small cell lung cancer (NSCLC), warranting continued attention.