Gilead Sciences: The Antiviral Pioneer Behind Remdesivir in the Fight Against COVID-19

Gilead Sciences

Antiviral Drug Developer

The sudden onset of COVID-19 bore a striking resemblance to the SARS epidemic that ravaged the world years ago. Faced with a more rapidly evolving outbreak, our response strategies were no longer as unprepared as they had been in 2003. After successfully restricting population movement and isolating suspected cases, the spread of the epidemic appeared to be somewhat contained. At this point, the treatment of patients became the primary focus of public attention.

Remdesivir, which frequently appeared in WeChat Moments in the recent past, has become hailed as a miracle cure for novel coronavirus pneumonia through word of mouth. Its developer, U.S.-based Gilead Sciences, Inc., also responded swiftly to the domestic epidemic by organizing clinical trials.

So why has remdesivir become hailed as a miracle cure? And how has pharmaceutical giant Gilead Sciences managed to maintain a stable stock price despite years of declining performance? Today, we take you on a deep dive to find out.

In public discourse, remdesivir has virtually become a miracle drug capable of curing diseases within a day. Although relevant authorities promptly debunked such misinformation, people seem more inclined to believe in the miracle of a one-day cure. This persists even though the entire body of evidence supporting the use of remdesivir for treating COVID-19 consisted only of some in vitro experiments and a single case report from the United States.

On January 31, the New England Journal of Medicine (NEJM), a top-tier medical academic journal, published a brief report on the first imported case of novel coronavirus infection in the United States. The patient sustained a fever above 38.8°C from January 21 to January 26 and began treatment with remdesivir on January 27. Subsequently, the patient’s clinical symptoms improved rapidly; supplemental oxygen was no longer required, and oxygen saturation levels returned to 94%–96%. The study lacked a control group and did not include data on peripheral blood viremia or viral load before and after treatment; only viral RNA data from nasopharyngeal/oral swabs were available. Furthermore, as the patient received various other supportive treatments concurrently with remdesivir, it was not possible to determine whether the symptom alleviation was directly attributable to remdesivir.

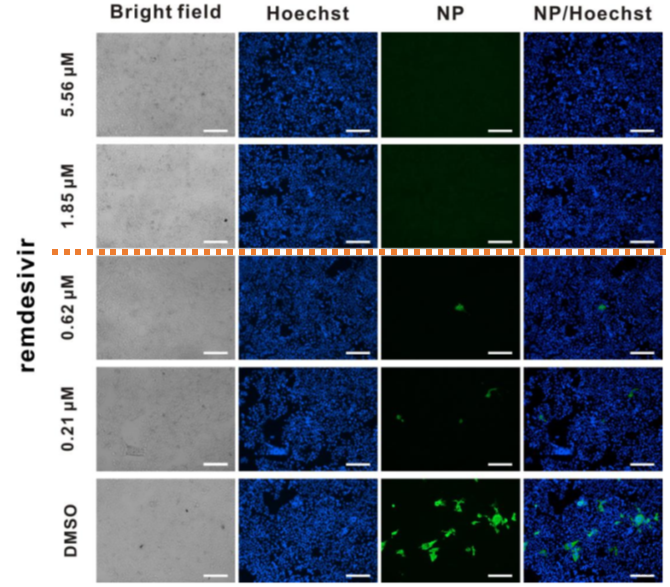

Inhibitory Effects of Remdesivir on SARS-CoV-2 at Different Concentrations

Subsequently, on February 4, 2020, the Wuhan Institute of Virology published a paper online in Cell Research, confirming the efficacy of remdesivir against coronaviruses in vitro. In this article, the team from the Wuhan Institute of Virology evaluated the effectiveness of seven different antiviral drugs against SARS-CoV-2 and found that remdesivir, chloroquine, and nafamostat exhibited inhibitory effects on the virus in vitro. Further cellular experiments demonstrated that remdesivir at a minimum concentration of 1.85 μM could completely eliminate SARS-CoV-2 infection in the Vero E6 cell line derived from African green monkey kidneys. These findings suggest that remdesivir may be a highly effective therapeutic agent against SARS-CoV-2.

Remdesivir is, in fact, an “old drug,” and one that could be considered a failure in certain respects. It was originally designed to inhibit RdRP, an RNA-dependent RNA polymerase protein in the Ebola virus that plays a critical role in viral replication.

In a WHO comparative trial of Ebola virus therapeutics, remdesivir was evaluated in parallel with REGN-EB3, ZMapp, and mAb114. However, among participants with low viral load at baseline, the mortality rate in the remdesivir group was the highest, reaching 33%. The excessively high mortality rate led to the early termination of the clinical trial.

Although remdesivir failed to fulfill its intended purpose, articles have continuously pointed out since 2017 that it may significantly inhibit coronaviruses. As early as January 10, 2020, before the outbreak of the novel coronavirus epidemic, a research institution published an article in Nature Communications confirming that remdesivir demonstrated more pronounced efficacy against MERS-CoV, another coronavirus, compared to lopinavir, ritonavir, and interferon-beta. Furthermore, mouse experiments showed that both prophylactic and therapeutic administration of remdesivir improved lung function, reduced pulmonary viral load, and ameliorated lung pathology post-infection. It was precisely on the basis of these studies that the United States authorized the use of remdesivir for COVID-19 patients under "compassionate use" provisions.

After learning that remdesivir might be effective against the novel coronavirus, Gilead Sciences began actively engaging with Chinese health authorities. On February 1, The Wall Street Journal published a report stating that Gilead was poised to launch Phase III clinical trials of remdesivir in China. Other reports also indicated that Gilead was actively procuring intermediate compounds for remdesivir. Subsequently, on February 2, the Center for Drug Evaluation of the National Medical Products Administration disclosed that the clinical trial application for remdesivir in the treatment of COVID-19 had been accepted. The trial, led by China-Japan Friendship Hospital, would be conducted in Wuhan.

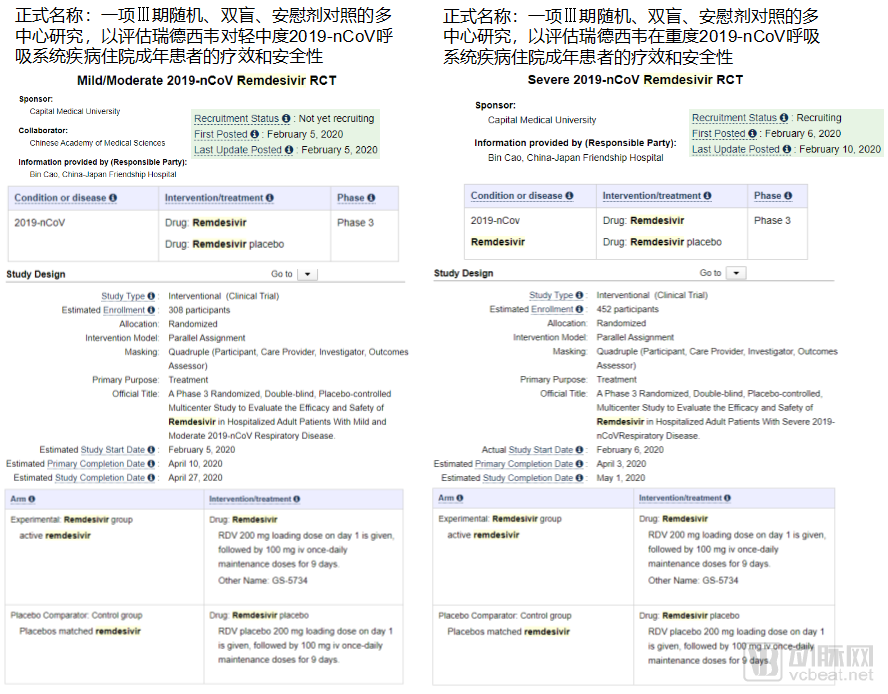

Two Pivotal Clinical Trials of Remdesivir for the Treatment of COVID-19

On February 5, the team led by Wang Chen and Cao Bin from China-Japan Friendship Hospital announced the initiation of a study on remdesivir for the treatment of novel coronavirus infection at Wuhan Jinyintan Hospital.

Two clinical trials, targeting patients with mild-to-moderate and severe conditions respectively, are both sponsored by China Medical University (with the Chinese Academy of Medical Sciences participating as a collaborator in the mild-to-moderate trial). Professor Cao Bin from China-Japan Friendship Hospital serves as the Principal Investigator (PI). The mild-to-moderate trial is expected to enroll 308 patients, while the severe trial is expected to enroll 452 patients. Patients enrolled in the trials will receive a 200 mg dose of placebo/remdesivir on Day 1, followed by a daily 100 mg dose for the next 9 days.

Both trials currently underway are multicenter studies conducted in a randomized, double-blind, placebo-controlled manner. In a double-blind trial, neither the participants nor the investigators are aware of the group assignments; the clinical trial protocol is entirely arranged and controlled by the study designers. This means that no one will know whether remdesivir is effective until the trials are unblinded. The expected completion dates for the two trials are April 27 (for mild to moderate cases) and May 1 (for severe cases). Only then will it be clear whether remdesivir is indeed the “miracle drug” for curing COVID-19.

Let us set aside, for now, the question of whether remdesivir is truly a “miracle drug.” Nevertheless, Gilead Sciences, the company behind remdesivir, has undoubtedly captured significant public attention during this period. People are eager to learn more about this company that has stepped forward with a “life-saving remedy” in times of crisis.

Gilead Sciences was founded in 1987 and has been dedicated to the research and development of antiviral drugs since its inception. In just 33 years of development, Gilead has fully demonstrated its strengths in the field of antivirals. Its hepatitis C drug Sovaldi achieved sales exceeding $10 billion in its first year on the market, becoming one of the fastest-growing drugs in pharmaceutical history. In the field of HIV/AIDS, Gilead’s antiretroviral therapies have long accounted for more than 50% of the global market share, a figure that continues to grow annually.

In 2014, driven by the strong performance of its hepatitis C drugs, Gilead Sciences, founded just 27 years earlier, broke into the list of the top ten global pharmaceutical companies, standing alongside century-old industry giants such as Pfizer, Novartis, and Roche. In the 2019 Pharmaceutical Innovation Index published by the renowned global pharmaceutical consulting firm IDE Pharma, Gilead also ranked first, thanks to its highly innovative product pipeline.

Michael O’Day, the founder of Gilead Sciences, contracted dengue fever in his early years, a fact that many believe is closely linked to Gilead’s strategic focus on antiviral drug development. During its initial phase, Gilead did not achieve significant success. Although its first marketed drug, cidofovir (Vistide), helped the company raise substantial capital in the secondary market, the drug itself recorded mediocre sales. It was the 1999 acquisition that truly enabled Gilead to escape its prolonged period of losses.

In 1999, Gilead Sciences acquired NeXstar Pharma for a total of $550 million, simultaneously gaining rights to two of its drugs: AmBisome, used to treat severe fungal infections, and DaunoXome, indicated for Kaposi’s sarcoma in patients with AIDS. Driven by the sales performance of these two products the following year, Gilead’s annual revenue exceeded $100 million for the first time, marking the first shift in its primary revenue source from collaboration income to product sales.

In 2001, Gilead Sciences’ first anti-HIV drug, tenofovir disoproxil fumarate, was approved for market launch. Since then, Gilead has focused its primary efforts on the research and development of anti-HIV therapies. Subsequently, the company has introduced a new anti-HIV combination therapy approximately every two years. Leveraging this consistent product pipeline, Gilead rapidly captured market share previously dominated by GlaxoSmithKline (GSK), a former leader in the anti-HIV sector. This trend has continued to the present day.

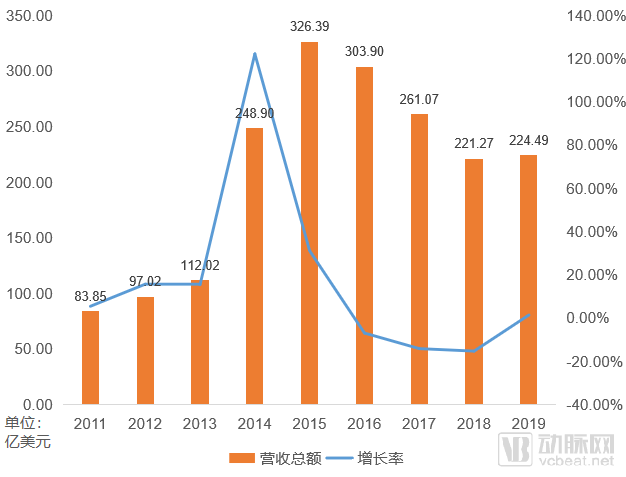

However, it was not anti-HIV drugs that ultimately propelled Gilead Sciences into the ranks of the top ten pharmaceutical companies. In 2011, Gilead acquired Pharmasset for $11.2 billion, thereby obtaining Sovaldi, a hepatitis C drug in Pharmasset’s pipeline. Whether this deal was worthwhile is evident from Gilead’s revenue figures.

Gilead Sciences' Revenue Trend Chart Since 2011

2014–2015 marked the most glorious period in Gilead Sciences’ development. Its revenue surged from $11.202 billion in 2013 to $32.639 billion in 2015. However, over the following three years, Gilead experienced three consecutive years of declining revenue, with figures falling from the 2015 peak of $32.639 billion to $22.127 billion in 2018. In just three years, performance dropped by more than 30%.

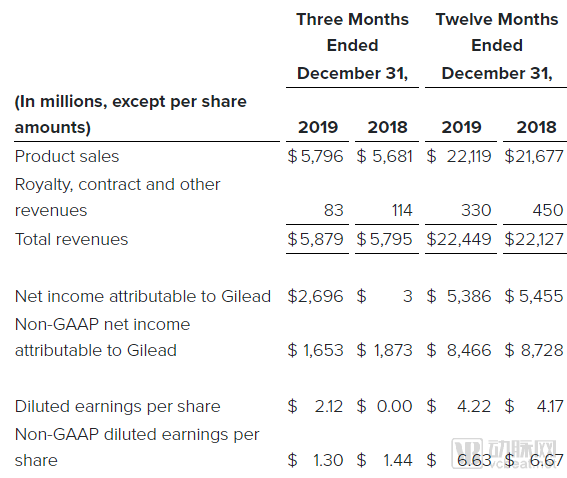

Gilead Sciences Announces Partial Financial Data for 2019

On February 6, 2020, Gilead Sciences announced its financial results for 2019, with revenue returning to growth and reaching a new milestone of $22.119 billion, thereby ending three consecutive years of declining performance. After deducting costs, Gilead’s net income amounted to $5.386 billion, while its adjusted net income reached as high as $8.466 billion.

Like most pharmaceutical companies, Gilead Sciences maintains a high gross profit margin of over 70%, with an adjusted gross profit margin exceeding 80%. In terms of research and development, Gilead significantly increased its R&D investment in 2019 as multiple clinical trials were underway, thereby securing safeguards for its future growth.

After significant fluctuations, performance has finally stabilized. The underlying reason is the hepatitis C drug mentioned earlier—Sovaldi.

Hepatitis C is a liver disease caused by infection with the hepatitis C virus (HCV). If patients do not receive timely treatment, chronic hepatitis C can progress to life-threatening conditions such as cirrhosis, liver failure, and liver cancer. The transmission routes of hepatitis C are similar to those of HIV, primarily through blood, mother-to-child, and sexual transmission. Additionally, there are sporadic cases of hepatitis C with unclear transmission pathways.

Prior to 2011, the primary treatment regimen was the combination of pegylated interferon-alpha (hereinafter referred to as “interferon”) injection and ribavirin. The cure rate for this two-drug combination was only around 40%. By 2011, oral antiviral drugs, such as Merck’s boceprevir, had significantly improved the cure rate for hepatitis C. However, the oral medications available at that time were not entirely oral-only regimens. Patients required a combination therapy of “oral medication + interferon injection + ribavirin” to increase the cure rate from 40% to approximately 80%. This figure represented a substantial breakthrough in the treatment of hepatitis C—had it not been for the emergence of Gilead Sciences.

In December 2013, Gilead’s hepatitis C drug Sovaldi was approved for market launch, outperforming competitors across three key dimensions: cure rate, adherence, and adverse reactions. A 12-week course of Sovaldi achieved a cure rate of approximately 90% for hepatitis C. Patients with certain hepatitis C genotypes no longer required concurrent interferon injections; oral administration of Sovaldi alone was sufficient to achieve therapeutic efficacy. More importantly, no serious adverse events were observed in Sovaldi’s clinical trials, and the overall incidence of adverse reactions was significantly lower than that of competing treatments. Consequently, Sovaldi rapidly captured market share after its launch, becoming the new standard of care for hepatitis C treatment. In 2014 alone, sales of Sovaldi surpassed the $10 billion mark.

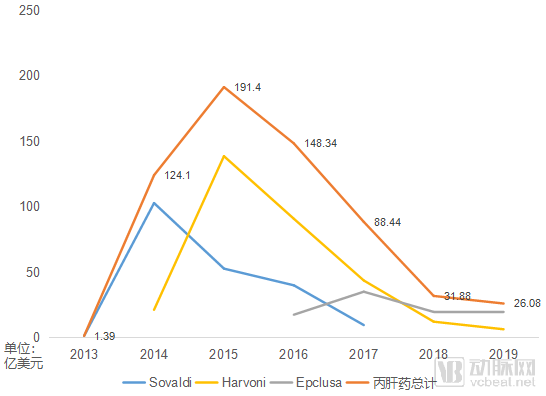

Annual Sales of Third-Generation Hepatitis C Drugs (Since 2018, Gilead No Longer Discloses Sovaldi Sales Separately)

Sovaldi significantly improved the cure rate and patient adherence for hepatitis C, but it also led to a decline in the patient population. Facing a shrinking pool of hepatitis C patients and pressure from competitors, Gilead Sciences had to price Sovaldi at $1,000 per pill, amounting to $84,000 per treatment course, to recoup R&D costs and generate profits within a short timeframe.

Subsequently, in the second year after Sovaldi’s launch, Gilead swiftly introduced Harvoni to the market, commonly known as “Gilead’s Second Generation.” Harvoni demonstrated even more remarkable efficacy, with an average cure rate of up to 95% across different types of hepatitis C patients. For specific patient populations, the cure rate reached 100% after 24 weeks of treatment. With the introduction of Harvoni, the hepatitis C drug market surged to its historical peak. Statistics show that the global hepatitis C market hit a record high of $23.7 billion in 2015, with Gilead’s two products accounting for over 80% of this market.

Sovaldi and Harvoni left the hepatitis C virus with nowhere to hide. Yet, as the saying goes, “when the birds are gone, the fine bow is put away”; the decline in the number of hepatitis C patients also accelerated the market contraction for Sovaldi and Harvoni. Gilead’s own third-generation therapy, Epclusa, rapidly declined after reaching only a peak annual sales figure of $3.5 billion. Gilead even established its own generic drug enterprise for hepatitis C medications to cover the tail-end market. By 2019, sales of Gilead’s three hepatitis C drugs had fallen to less than $3 billion, under one-sixth of their peak market value.

In November 2017, Gilead Sciences announced the official launch of Sovaldi in China under the brand name Suo Hua Di. Subsequently, Harvoni and Epclusa also entered the Chinese market under the brand names Xia Fan Ning and Bing Tong Sha, respectively. In the national medical insurance negotiations at the end of 2019, Xia Fan Ning and Bing Tong Sha, along with Merck & Co.’s Zepatier, were included in the National Reimbursement Drug List, with an average price reduction of 85%. The out-of-pocket cost per treatment course for patients decreased from approximately RMB 50,000 to around RMB 10,000.

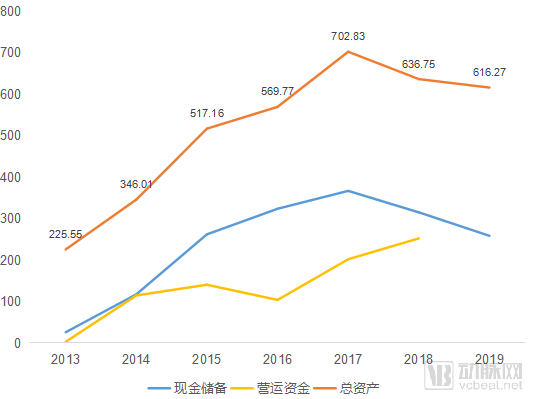

Changes in Gilead Sciences' Assets in Recent Years

Gilead’s performance in the hepatitis C market drove rapid corporate growth. In 2013, Gilead’s liquidity hit rock bottom, with cash reserves of just $2.571 billion and working capital dwindling to a mere $259 million. However, following the launch of Sovaldi, the company’s financial position improved dramatically within the first year. Both cash reserves and working capital surpassed the $10 billion mark, while total assets approached $35 billion. By 2017, Gilead had doubled its total assets once again in just three years, breaking through the $70 billion threshold.

But the reality is that Gilead Sciences has shrunk the hepatitis C market space because its drug therapies are too effective.

Gilead has also made significant contributions to the treatment of hepatitis B, which is more challenging to manage than hepatitis C. Launched in 2002, Hepsera (adefovir dipivoxil) was the first nucleotide analog approved by the FDA for the treatment of chronic hepatitis B. The drug achieved sales of $340 million in 2008; however, its performance was considered modest relative to the overall hepatitis B market.

Subsequently, in 2008, Gilead Sciences introduced its star anti-HIV drug Viread (tenofovir; Chinese brand name: Viread) into the hepatitis B market. Prior to its launch, Viread underwent head-to-head clinical trials against Hepsera; however, after its market entry, it still failed to help Gilead expand its competitive advantage in the hepatitis B sector.

In the following years, Gilead Sciences’ business experienced rapid growth in the fields of HIV and hepatitis C treatment, while there was seemingly no news from its hepatitis B segment. However, in reality, Gilead’s activities never ceased.

In November 2016, Gilead Sciences re-entered the hepatitis B market with its drug Vemlidy (Chinese brand name: Weilide). Vemlidy is an upgraded version of Viread. Compared to its predecessor, Vemlidy maintains equivalent efficacy while reducing the dosage to one-twelfth. Meanwhile, the lower dosage significantly reduces nephrotoxicity. Except for patients with end-stage renal disease, those with mild, moderate, or severe renal impairment can use Vemlidy under medical supervision. In December 2018, Vemlidy was also launched in China, becoming the newest hepatitis B medication available in the country.

Despite such a significant upgrade, Gilead has failed to fully supplant Viread’s market position. The key reason lies in Viread’s high price. The hepatitis B drugs currently in use that directly compete with Viread are primarily its predecessor, tenofovir, and Bristol Myers Squibb’s (BMS) entecavir; however, both of these medications have long since expired their patent protection.

Fortunately, patients in China no longer need to worry about the price of Vemlidy. In the latest round of national medical insurance negotiations conducted in December 2019, Vemlidy successfully passed the negotiations and was included in the national medical insurance coverage.

Even Viread can only ensure long-term survival of patients with chronic hepatitis B. As an expert in the field of antiviral therapy, Gilead Sciences has never given up the search for a cure for hepatitis B, and a turning point may already be emerging. In September 2018, Gilead Sciences announced a collaboration with Precision Biosciences to develop gene therapies aimed at completely eliminating hepatitis B virus infection from the human body.

After successfully conquering hepatitis C, Gilead Sciences saw its confidence surge and sought to build on this momentum by advancing further into the broader field of liver diseases. However, this time, Gilead has clearly encountered a tough challenge.

Gilead Sciences aims to tackle an unresolved clinical challenge: non-alcoholic steatohepatitis (NASH). Currently, there is not only a lack of appropriate treatment options for NASH, but its etiology also remains poorly understood. In early 2019, analysts considered it a pivotal year for NASH drug development, with Gilead’s selonsertib holding high expectations.

However, the situation was not as optimistic as many had hoped. In February 2019, Gilead Sciences regretfully announced that selonsertib failed to meet its clinical endpoints in the Phase III STELLAR-4 trial. Subsequently, in April 2019, another Phase III trial of selonsertib, STELLAR-3, also failed. Gilead Sciences promptly discontinued the development of this drug and redirected its efforts toward advancing two other candidates in its pipeline.

However, Gilead’s bad news did not end there. In December 2019, Gilead announced that cilofexor, another key drug in its pipeline for the treatment of non-alcoholic steatohepatitis (NASH), failed to meet the primary endpoints of its Phase II ATLAS clinical trial, both as monotherapy and in combination therapy. On a positive note, the combination of cilofexor and fisocostat met secondary endpoints, effectively alleviating various symptoms of NASH with good tolerability. This suggests that this drug combination still holds significant potential and room for further development.

In addition, the combination of cilofexor and firsocostat, another NASH drug from Gilead Sciences, also improved relevant symptoms in study participants. Although monotherapy has repeatedly hit roadblocks, combination therapy appears to have opened a window for Gilead. Judging by Gilead’s stance, the pharmaceutical giant’s battle against NASH is far from over.

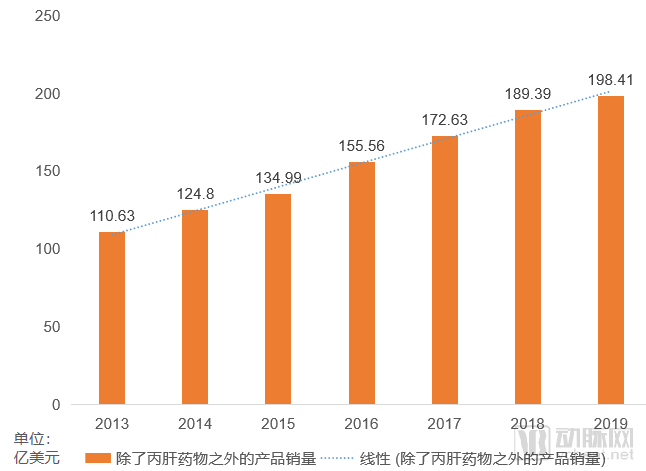

Gilead’s Revenue Trends Excluding Hepatitis C Drugs

Excluding the hepatitis C drug segment from its revenue, Gilead Sciences has never ceased to grow, with its growth rate remaining stable at approximately 10%.

Prior to the 2013 launch of Sovaldi, antiretroviral drugs had always been Gilead’s cornerstone products. Following the contraction of the hepatitis C market, Gilead’s revenue pillar shifted once again from hepatitis C medications back to anti-HIV drugs. In 2019, anti-HIV drugs generated $16.438 billion in revenue for Gilead, accounting for 73.22% of its total income, successfully succeeding hepatitis C drugs as the company’s primary revenue driver for the next phase.

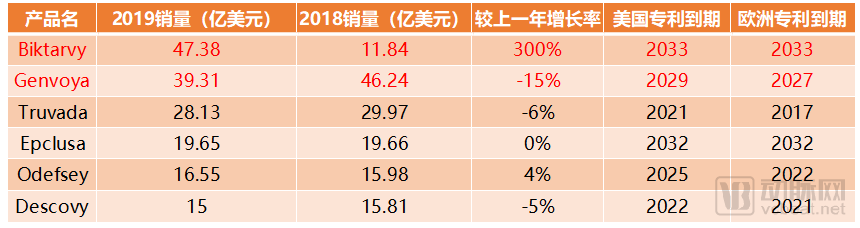

Gilead Sciences’ Products with 2019 Sales Exceeding $1 Billion

In 2019, six of Gilead Sciences’ products achieved annual sales exceeding $1 billion, among which only one was a hepatitis C drug: Epclusa (“Sofosbuvir/Velpatasvir”).

Among the remaining five anti-HIV drugs, Genvoya, with annual sales nearing $3.931 billion, experienced a slight decline but still ranked as the second best-selling drug. With 6–8 years remaining on its relevant patents, it continues to hold substantial market potential. Additionally, Biktarvy, approved for launch in early 2018, generated $1.184 billion in sales within less than a year of its release, and its revenue surged by 300% to $4.738 billion in 2019. Its market exclusivity extends until 2033, establishing it as another core product for Gilead Sciences. Driven by the sustained momentum of its anti-HIV portfolio, Gilead Sciences appears well-positioned to maintain its current performance stability in the coming years.

In 1996, Chinese-American scientists proposed the "cocktail therapy" for AIDS, which involves the combined use of three or more antiretroviral drugs to combat HIV. This combination approach is similar to mixing cocktails, hence the name "cocktail therapy."

Before the advent of combination antiretroviral therapy (commonly known as "cocktail therapy"), GSK’s zidovudine was the star drug for monotherapy in the treatment of HIV/AIDS. However, like all monotherapy regimens, zidovudine inevitably led to drug resistance after long-term use, compromising its efficacy. The introduction of combination antiretroviral therapy effectively resolved the issue of drug resistance, making long-term survival with HIV possible for patients.

However, more complex than cocktail therapy is patient medication adherence. So, can multiple drugs be condensed into a single pill? At that time, the AIDS giant GSK took the lead in research and successively produced several generations of products, but it always fell one step short of achieving cocktail therapy with a single drug. It was Gilead Sciences that accomplished this goal.

In 2006, Gilead Sciences’ triple-combination therapy, Atripla, was approved for market launch, becoming the first single-pill combination antiretroviral therapy. In clinical trials, 80% of the 244 HIV-infected patients treated with Atripla showed a significant reduction in HIV viral load and a marked increase in CD4 cells (the primary target of HIV). Given its landmark status and excellent efficacy, the FDA approved Atripla’s marketing application within just three months through the fast-track review program.

In the following years, Atripla maintained a rapid growth trajectory, and in 2010, it surpassed Truvada, the best-selling HIV medication, to become Gilead’s top-selling product of the year, with sales reaching $2.927 billion.

Truvada, dethroned by Atripla, is another legendary drug launched by Gilead Sciences in 2004. Initially, the FDA approved Truvada solely for the treatment of HIV/AIDS; due to concerns about its side effects, the FDA did not approve its use for prevention until 2012. The approval for preventive use not only extended Truvada’s market exclusivity period but also revitalized its sales, ushering in a second surge in demand. To this day, Truvada remains the gold standard for HIV pre-exposure prophylaxis (PrEP), maintaining annual sales of nearly $3 billion, and has become the best-selling product in the history of antiretroviral therapy.

In the field of antiretroviral drugs, perhaps only Gilead Sciences itself could surpass Gilead. Atripla maintained its dominance for many years. Ultimately, as Atripla’s patent expiration approached, Gilead launched Stribild as Atripla’s successor and soon followed with its upgraded version, Genvoya, thereby continuing its reign in the antiretroviral drug market.

Genvoya evolved from Atripla’s three-drug combination to a four-drug regimen. In addition to retaining emtricitabine, efavirenz was replaced by the new drug elvitegravir, tenofovir disoproxil fumarate was replaced by tenofovir alafenamide, which exhibits greater stability in plasma, and the pharmacokinetic enhancer cobicistat was added. Following its launch, Genvoya rapidly captured market share from Atripla and Stribild. It reached its sales peak in 2018, at $4.624 billion.

At this time, Gilead Sciences faced challenges from its long-standing rival in the HIV/AIDS field, GSK. The market share of GSK’s new drug, Triumeq, rose rapidly, with its growth rate even surpassing that of Genvoya in the short term.

Gilead Sciences did not remain idle in the face of such challenges. The clinical trials for Gilead’s latest product, Biktarvy, directly compared Biktarvy with the three-drug combination regimen of Triumeq, effectively constituting a head-to-head trial against Triumeq. Ultimately, Biktarvy demonstrated comparable efficacy to Triumeq but with fewer adverse drug reactions.

Driven by strong clinical trial data, Biktarvy, which was launched in 2018, has become the top-selling product in Gilead Sciences’ drug pipeline, with sales reaching $4.738 billion in 2019 and further growth potential in the future.

Gilead Sciences has long established a firm foothold in the field of HIV treatment, and its exploration in HIV prevention has not stopped with Truvada.

Descovy was first launched in the United States in 2016 and subsequently entered the Chinese market in 2018 under the brand name Dakewei. Since its commercial launch, Dakewei has become one of Gilead Sciences’ flagship products, with current annual sales exceeding $1.5 billion. However, with its patents expiring in the United States and Europe in 2021 and 2022, respectively, time appears to be running out for Gilead.

However, Gilead’s expectations for Descovy extend beyond HIV treatment. In November 2019, at the 17th Conference on Retroviruses and Opportunistic Infections (CROI), Gilead announced that Descovy demonstrated non-inferior efficacy and safety compared to Truvada in Phase III clinical trials for pre-exposure prophylaxis (PrEP) against HIV. Over a 96-week study period, the HIV infection rates among high-risk individuals receiving Descovy and Truvada were 0.16% and 0.30%, respectively, confirming the non-inferiority of Descovy relative to Truvada. Additionally, Descovy achieved therapeutic drug concentrations for HIV prevention more rapidly than Truvada, and its residual presence in the body after discontinuation was prolonged by over 60%.

Based on these clinical results, Gilead Sciences is highly likely to submit a new indication application for Descovy for PrEP in 2020, which will further drive the sales of Descovy.

Following monotherapy, long-acting antiretroviral drugs are poised to become the primary direction for the next generation of HIV medications. Currently marketed long-acting injectable antiretrovirals mostly require weekly administration, whereas ViiV Healthcare, jointly owned by GSK and Pfizer, is developing a new product that could extend the dosing interval to once monthly. In the face of this new challenge from GSK, Gilead Sciences will certainly not cede the market dominance it has cultivated over many years.

In March 2019, Gilead Sciences announced the clinical trial results for GS-6207. GS-6207 is an HIV-1 capsid inhibitor that is poised to become part of a long-acting combination therapy for HIV. A clinical trial involving 40 healthy subjects supported a three-month dosing interval for GS-6207 at doses above 100 mg, with virtually no adverse reactions. In November 2019, GSK further disclosed additional trial results indicating that the potential dosing interval for subcutaneously administered GS-6207 could be extended to once every six months. Whether Gilead can once again outperform GSK in the field of long-acting antiretroviral drugs remains to be seen.

Oncology has long been a fiercely contested battleground for major pharmaceutical companies. After reaping substantial profits from its hepatitis C and antiretroviral drugs, Gilead Sciences naturally sought to capture a share of the oncology market. However, its initial foray into this sector was not particularly successful.

In 2014, Gilead Sciences’ blockbuster oncology drug Zydelig was approved for market launch, simultaneously entering the U.S. and European markets for the treatment of three types of B-cell hematologic malignancies. From the outset, Zydelig’s labeling included a boxed warning alerting patients to potential adverse effects, including colitis, pneumonitis, and potentially fatal hepatotoxicity. By 2016, these safety concerns prompted the European Medicines Agency (EMA) to issue warnings regarding Zydelig and led to the termination of six ongoing clinical trials.

Following the failure of Zydelig, Gilead Sciences began shifting its oncology strategy from in-house development to collaborations and acquisitions. The most pivotal transaction was undoubtedly the $11.9 billion acquisition of Kite Pharma, which immediately granted Gilead access to Yescarta, the second cell therapy product approved globally.

Yescarta, approved just two years ago, is gradually demonstrating its remarkable revenue-generating potential. In 2018, its first year of commercial launch, sales reached $264 million. In 2019, with the opening of the European market, Yescarta’s sales surged to $456 million. Looking ahead, as costs decline and technological accessibility improves, there are strong reasons to believe that Yescarta still holds substantial growth potential in the coming years.

Gilead’s ambitions for cell therapy extend even further. Yescarta is currently advancing clinical trials for diffuse large B-cell lymphoma (DLBCL), with the aim of moving from its current role as a third-line treatment to a second-line option. Following Yescarta, another cell therapy product, the CD19-targeted KTE-X19, is poised for launch. In 2019, Gilead showcased the impressive performance of KTE-X19 in acute lymphoblastic leukemia (ALL) and mantle cell lymphoma (MCL).

In the Phase I ZUMA-3 clinical trial for the treatment of ALL, 68% of the 41 treated patients achieved complete response (CR) or complete response with incomplete hematologic recovery (CRi) after more than two months of follow-up. In the Phase II ZUMA-2 clinical trial for the treatment of MCL, 67% of the 60 evaluable patients achieved CR; at a median follow-up of 12.3 months, 57% of patients maintained their response, and the 12-month progression-free survival (PFS) and overall survival (OS) rates reached 61% and 83%, respectively. Although KTE-X19 may still cause serious adverse events such as stroke and multi-organ failure, these overall response data remain encouraging.

In other therapeutic areas, Gilead has primarily adopted a collaborative R&D strategy.

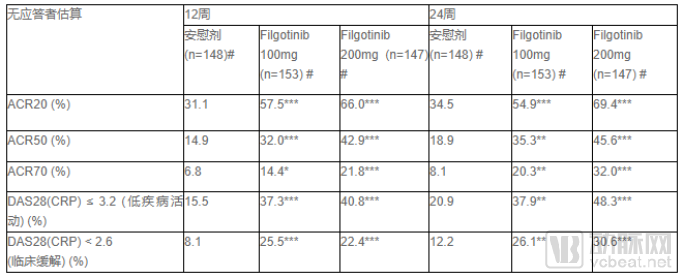

Gilead Sciences entered into an agreement worth up to $2 billion with Galapagos in late 2015 to co-develop its JAK1 inhibitor, filgotinib. The product has lived up to Gilead’s expectations. In August 2019, Gilead and Galapagos announced that the European Medicines Agency (EMA) had accepted the application for filgotinib for the treatment of adult patients with rheumatoid arthritis.

Clinical Trial Results of Filgotinib

Based on current Phase III clinical trial results, filgotinib is poised to be highly competitive among drugs in its class. In 2019, the FDA approved AbbVie’s JAK inhibitor, Rinvoq. In its disclosed clinical trial results, the proportion of patients achieving a 20% improvement rate remained between 65% and 71%. Filgotinib, at a dosage of 200 mg, achieved a comparable rate of 66% on the same endpoint, demonstrating efficacy equivalent to that of Rinvoq. However, filgotinib exhibited an excellent patient tolerability profile, with treatment-emergent adverse events limited to mild or moderate severity. Moreover, only 4.1% of patients in the 200 mg group experienced adverse events. Filgotinib is likely to emerge as a flagship product, heralding Gilead Sciences’ entry into the field of immunological diseases.

To date, Gilead Sciences has leveraged its unique vision to secure multiple high-quality drug pipelines. Beyond antiviral therapies, it has expanded its footprint into broader medical fields, including oncology and immunological diseases. With stabilizing performance, a robust pipeline of follow-on products, and $25 billion in cash reserves, 2019 may mark the beginning of a new era for Gilead. Can the company that defeated the hepatitis C virus triumph over even more formidable adversaries in this next chapter?